How to calculate your sum insured

Your rebuild sum insured is one of the most important parts of your house insurance policy. It determines the maximum amount payable if your home needs to be rebuilt after major damage.

This guide explains what sum insured means, how to calculate it correctly, and why market value is not the right number to use.

Quick summary

-

Your sum insured should reflect rebuild cost, not market value.

-

Include demolition, fences, pools and other structures.

-

Add a buffer for rising building costs.

-

Minimum and maximum limits are based on your floor area.

-

All sums insured include GST.

-

You are responsible for selecting the correct amount.

What is sum insured?

Sum insured is the amount it would cost to fully rebuild your home to its current size and standard, using today’s building costs. It is not:

-

The market value of your home

-

What you paid for the property

-

The land value

It should reflect rebuild cost only.

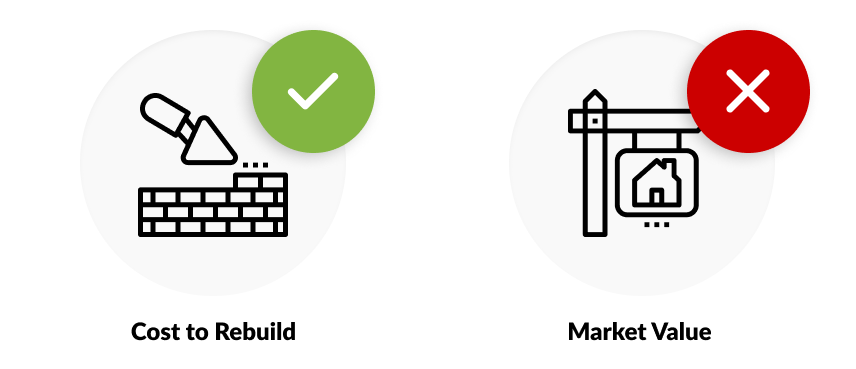

Rebuild cost vs market value

Market value includes land and location demand. Rebuild cost only covers construction.

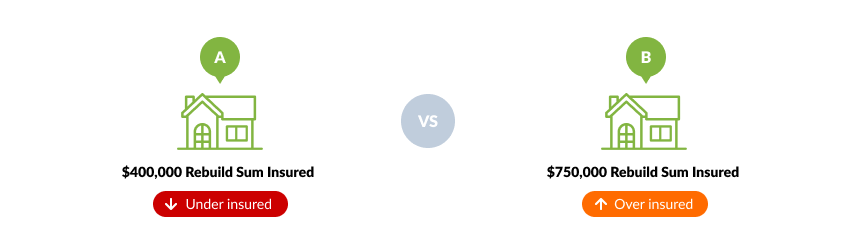

Example: Under-insured vs over-insured

Imagine two neighbours with identical homes that would cost $500,000 to rebuild.

-

Neighbour A insures for $400,000 using a rough estimate of $2,000 per square metre.

-

Neighbour B insures for $750,000, thinking market value is the right number.

After an earthquake:

-

Neighbour A receives $400,000 and is $100,000 short.

-

Neighbour B receives $500,000 (the rebuild cost), but has paid higher premiums than necessary.

Getting it right avoids both financial shortfall and overpaying.

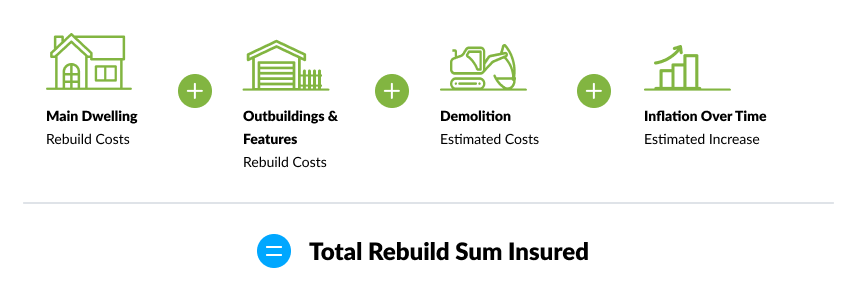

What should be included in your rebuild sum insured?

When calculating your sum insured, include:

-

The house itself

-

Fences

-

Swimming pools

-

Retaining walls

-

Other permanent structures

You should also factor in:

-

Demolition and debris removal

-

Professional fees

-

Inflation and rising building costs

Adding a reasonable buffer can help protect against cost increases over time.

Why is there a minimum and maximum sum insured?

When selecting your sum insured, you will see a minimum and maximum value range.

These are calculated based on:

-

The floor area of your home

-

Any declared outbuildings

Minimum sum insured

This reflects the lowest realistic rebuild cost per square metre for a basic home. It helps prevent serious underinsurance.

Maximum sum insured

This reflects the upper realistic rebuild cost based on floor area.

Selecting a figure above this will not increase your payout. It may only increase your premium.

If your situation genuinely requires a higher amount, contact our support team to discuss your circumstances.

💡 Building costs vary depending on materials, design and location, but most homes fall within the provided range.

Does my sum insured include GST?

Yes. Any nominated sum insured on an initio policy includes GST.

Before confirming your GST preference, ensure your selected amount includes the GST component.

How can I estimate my rebuild cost?

If you are unsure where to start, you can use the Cordell Sum Sure Calculator.

It uses council data, floor area, and building details to estimate rebuild costs. You can compare this estimate with your own assessment.

You may also wish to consult:

-

A registered builder

-

An architect

-

A quantity surveyor

Cordell Rebuild Calculator

Who is responsible for setting the sum insured?

While we can provide guidance on how our products work, we are not qualified to value homes.

You are responsible for determining the correct rebuild sum insured for your property.

If your calculated amount falls outside the available range, please contact our support team.

Frequently asked questions

Should I insure for market value?

No. Your sum insured should reflect rebuild cost, not market value.

What happens if I under-insure?

Your maximum payout will be your selected sum insured, even if rebuild costs are higher.

What happens if I over-insure?

Your payout is capped at the actual rebuild cost. You may pay higher premiums without receiving additional benefit.

Do I need to include demolition costs?

Yes. Rebuilding after major damage includes demolition and debris removal.

Related Articles