Search results for: {search_term_string}/house-flip-insurance/page/7/get-quote

Join our team!

Digitally savvy, human touch; The heart of initio

Since 2011 we have been redefining insurance. We are creating an insurance experience that customers love! At initio, we are all about creating better digital experiences for buying and managing insurance exclusively online. We’re best known for being the first insurance provider in New Zealand to quote and bind an insurance policy online. We consider ourselves to be the challenger brand to the domestic insurance market in New Zealand and as such we are on a mission to redefine the way insurance is managed and delivered to customers digitally.

At initio, we’re not just hiring; we’re on the lookout for thinkers, creators, and lively souls eager to influence the next chapter of insurance for our clients. If you’re brimming with creativity and ready to make an impact, you’re in good company.

Award-Winning Workplace

Yes, you read it right; we’ve got a brand-new accolade. initio has been named one of the Best Insurance Companies to Work for in Australia and New Zealand in 2023! If you want to be part of a company that’s officially recognised as a brilliant place to work, one that truly looks after its staff, then look no further. Come join our award-winning team and let’s transform those brilliant ideas into something that shines even brighter.

Open Positions

Here’s a sneak peek at our roles currently on offer. Can’t find the perfect role just yet? Keep swinging by – new opportunities land faster than you can say “Cheeseburger Fridays.”

myRent Insurance

Code of Compliance

Code compliance is generally required to insure a house. But don’t worry, there are situations where we can potentially provide cover.

Most Common Reasons for Non-compliance

House or addition built before code compliance requirements

The current building code compliance requirements came into force in 1992. Homes built before this date often do not have code compliance, as it was not a requirement at the time.

Records of building consent have been lost or are unknown

It is surprisingly common for houses to lack a record of their code compliance sign-off. Some councils in New Zealand lost their records in fires and floods before they began storing them electronically.

Code compliance was not obtained for part of the home (e.g., extension)

Previous owners may have made improvements to the property, such as adding a deck or building an unconsented garage, without obtaining full building consent or sign-off.

What would we require to insure?

If your home lacks a compliance certificate for any of the above reasons, we can consider insuring it. If your home does not have a code compliance certificate this does not always mean your home is non-compliant, especially if records have simply been lost. To insure your house, we would need confirmation of the following:

- House is structurally sound and well maintained, AND

- Confirmation that the building or addition would have met building requirements at the time it was built/completed

Essentially we want to make sure we only insure houses/renovations that are up to building standards.

You must disclose information regarding any unconsented work when you apply for insurance. Please answer “yes” to the question “Is there any further information likely to affect the acceptance of the insurance” on your application form, provide full information in the space provided along with any other disclosures.

Other Reasons for Non-compliance

New Build or Recently Built Property

When a house is built, it must legally obtain a Code Compliance Certificate (CCC) before being occupied. In most cases, homeowners cannot move in until this certification is issued. However, if your house is a new or recently built property, it may still be awaiting code compliance while requiring standard house insurance. In some cases, homeowners may have already moved in before obtaining consent, often due to minor works still in progress.

What Do We Require for a New Build?

Before we can consider insurance for a new build without a Code Compliance Certificate, the property must meet the following requirements:

- The house has practical completion,

- There is a functioning kitchen/bathroom

- Connection to services is complete, including power/water supply.

- The house is fully secure, and lockable.

- Someone is currently living in the property.

- No major or structural work remains to be completed.

- A final inspection is confirmed and booked with the council. In higher-risk locations, the inspection must have at least been completed.

If your property meets these criteria, we can consider providing cover. However, you must disclose that a Code Compliance Certificate has not yet been obtained.

Conditions That Will Apply

If we agree to provide cover on your house without code of compliance issued, there are conditions that will apply. It is important that you are aware of these and know what they mean. These conditions are as below:

1. Additional costs associated with making the home compliant may not be covered

For example, we will pay to rebuild a non-compliant deck on your home that has burnt down. However, you will need to pay for any extra costs if you want to get code compliance sign-off on the new deck.

2. Any loss that directly arises from the lack of compliance will not be covered

For example, where your non-compliant deck collapses and also causes damage to the house. If the collapse of the deck is later proved to be a direct cause of its non-compliance (i.e. the deck was not up to building standards), then damage to the deck and home may not be covered.

Note that any other loss that is not a direct result of non-compliance (such as a storm or fire) remains covered.

3. Any loss that arises from the construction perils to complete the home and obtain compliance are not covered

If there are still major works being done at your property these are not covered. If a roof is being installed and it collapses, this should be covered under a contract works or construction insurance policy as this is not covered under a standard house insurance policy.

4. Building consent to be obtained within a specified period, typically 30 days.

This gives you some time to get code compliance approved. If you need longer than this you will need to let us know.

How can I get a quote?

If your house does not have full code compliance but meets the above criteria you can go ahead and get a quote. If you proceed with the quote you will need to disclose that the property does not have full consent when you answer the declaration questions during the sign-up application. Cover will then be reviewed by our team who will be back in touch.

Examples of where we can provide cover

- Compliance certificate is not signed off as the driveway is unfinished. Driveway concrete will not be laid until construction is complete on the neighbouring home as trucks are using the driveway for access. The home is structurally complete, fully secure and lockable, and is being lived in. – Cover is able to be provided.

- Final code compliance check was completed by the council in December, minor and non-structural defects were identified, and repairs were completed. Due to the Christmas break, council staff were not able to return to issue the code compliance certificate until mid January. The home was structurally complete, fully secure and lockable, and being lived in. – Cover is able to be provided.

Examples of where we are unable to provide cover

We can not offer insurance if your home does not meet the above requirements, or does not have code compliance certificate for reasons such as the following:

- Code of compliance certificate was applied for, but the building work contained defects which were not rectified.

- House was self-built and consents were never obtained.

- Home is a converted building (such as a wool shed or garage) and the conversion was not consented.

- A certificate of acceptance was applied for and denied because the building work contained defects.

- A safe and sanitary report confirmed the building work was unsafe and/or unsanitary.

- The builder’s report on the home identified that the building was not structurally sound.

- A pre-built/existing home has been moved onto the site and code is yet to be obtained for the placement/connection to services, etc.

- A garage converted to a home/self contained unit/sleepout, where it does not meet building standards for an inhabitable building.

- Renovations involving structural walls without consent.

- An outbuilding was built without consent as floor area was below local government requirement for consent but was not built to building code standards

How do you legalise existing building work?

Building work carried out before 1 July 1992 without the appropriate building approval requires a safe and sanitary report. A “safe and sanitary report” does not serve as an approval of the unauthorised work, just a reassurance that the building is safe and sanitary. You will need to engage a professional such as a private building consultant or registered engineer to complete this report. It will be held on file with the local council.

A certificate of acceptance is the appropriate way to legalise any work done after 1 July 1992. It provides limited assurance that the council has inspected the home and the completed building work complies with the building code at the time and contains no obvious defects.

Articles of interest

Do you have a second dwelling on your property that your family lives in?

If you have two dwellings/units on your property and the second one is permanently occupied by a family member or friend who lives separately to you, it’s important to have the right insurance in place to cover both homes properly.

What counts as permanent family use?

If your second dwelling—such as a granny flat, unit, or cottage—is lived in independently by a family member or a friend, then it’s considered a separate household. Even though they are part of your extended family or close circle, the fact that they live there permanently and independently means the second home/unit needs to be insured separately as another home/unit.

What insurance do you need?

For this setup, you’ll need two separate home (Own Home) insurance policies, one for each dwelling. This ensures that:

- Each home/unit is covered.

Begin by getting a home insurance policy for your first property and then proceed to obtain another quote for the second home/unit.

If you rely on rent from your family member for the second home/unit, we would recommend considering the Landlord policy for the second home/unit.

Own Home, Partially Rented insurance

To ensure both dwellings are protected with the right level of insurance you’ll need to set up one policy first, then start a new quote for the other. The good news? Getting covered online only takes a few minutes, so setting up two policies is quick and easy. If you already have house insurance with us and need to add a second policy, login to your dashboard and click on the + add house policy to begin the process. While getting a quote and buying insurance online with us might be easy, our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

How to add a policy for a second dwelling on the same title:

-

Login to your dashboard and click on the ‘house insurance +’ button

-

Search for your home address & ‘see full quote’

-

On the full quote screen, click ‘back’ to edit the second dwelling’s details if needed.

.

-

If both properties are the same size or the details are already correct, no changes are needed.

-

-

Once you go back, edit the property details, then click ‘continue’

-

- This will adjust the quote to reflect the correct figures for the property.

Finish the quoting process from here per the usual process – Easy!

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

Holiday Home vs. Own-Home Insurance: What New Zealand homeowners need to know

Owning multiple properties can sometimes make insurance decisions tricky, especially for New Zealand homeowners who use their homes differently throughout the week. For example, you might have one home you stay in during the weekdays and another you visit mostly on weekends.

Understanding the right insurance policy for each property is crucial to ensure you’re fully covered.

The main difference between holiday home insurance and own home insurance lies in the occupancy and associated risks. Own Home insurance is for your primary residence where you would reside the majority of the home, not generally suitable if you leave it vacant for periods of 60 consecutive days or more. Holiday homes are not primary residences and are often empty for reasonable periods, increasing risks such as break-ins. Therefore, holiday home insurance has specific conditions and coverage tailored to these unique risks. If you aren’t using your holiday home all year round, you might rent it out between stays.

The following is a list of cover specific to each type of policy to help you determine which is the best policy for your property:

Holiday home insurance specific cover:

- Optional – Guests: Cover for damage, theft, and loss of rent if you host guests.

- Fixed contents: $20,000 standard cover for fixed contents at the home, with options to increase. This covers furniture that stays in your home permanently (not personal belongings). Cover is limited to the property address.

- Blocked pipes: Up to $1,000 to unblock an underground pipe, with no excess.

- Keys and locks: Up to $1,000 for replacing keys and associated locks, with no excess.

- Legal liability: $2 million legal liability costs if an accident damages other property or people.

- Optional – Loss of rent: Up to 12 months or $20,000 following damage to your house.

Own home insurance specific cover:

- Personal contents (available as an add-on to any Own Home policy): Replace or repair lost or damaged belongings, majority of items are insured on a new-for-old basis. Includes cover for contents including personal effects whilst at the property and temporarily removed anywhere in New Zealand.

- Temporary accommodation: $20,000 of alternative accommodation if your damaged house can’t be lived in.

- Reduced glass breakage excess: Reduced $250 excess for glass breakage claims.

What if you split your time equally between two homes?

If you divide your time equally between two homes, each property may require different insurance considerations. The home you use during the weekdays might need a standard home insurance policy, while the one you visit on weekends could be classified as a holiday home, or potentially you may need two Own Home (owner occupied) policies. It’s crucial to assess the specific usage patterns of each property to ensure you have the appropriate coverage. This should also take what belongings you use the majority of the time at each property into consideration.

Holiday home or rental?

Provided you use the home as your holiday home we can also offer the option of including short-term rental cover for you. If this describes your situation, select ‘Holiday Home – sometimes rented’ from the dropdown menu, and initio’s clever software will do the rest. If you’re not sure which cover is best for you – we’re here to help.

What special terms apply (regarding vacancy) on each policy?

Holiday Homes:

If no one has been living or holidaying at the home for a period of more than 60 consecutive days, and the home is recorded as a holiday home, expectations are that the following criteria can be met:

- the home is inspected inside and outside by you or a nominated person at least every 60 days, and

- the home and its grounds are adequately maintained, mail is cleared regularly and

- the water supply is turned off and

- all doors are locked and windows secured

If you are unable to meet those conditions, cover will continue with a higher standard excess of $5,000 applying to any claim. If however, a loss results from a break-in or attempted break-in at the home while it is fitted with an active, professionally-installed alarm or security system, then an excess of $1,000 applies.

Own Homes (primary residence):

If no one has been living at the home for a period of more than 60 consecutive days, we will only pay for loss that is:

- caused by fire, explosion or lightning, or

- covered under the ‘Natural disaster’ automatic additional benefit.

These terms can be reviewed upon request for special circumstances.

What if I only use the house for guests?

Under our cover, you need to use the house at least occasionally yourself over the course of a typical year. If you;

- don’t use the house yourself as your holiday home and as such also

- don’t keep personal items at the home, and

- it is only rented to short-term guests,

it is considered a commercial operation, similar to a motel. Our cover is domestic-based house insurance, and cannot be used if the above requirements are not met.

Are my personal contents covered under a holiday home policy?

Your personal contents items, like phones, jewellery, and laptops, won’t be covered under your holiday home cover as they should be protected by your contents cover at your main home. Belongings that remain at your holiday home, like furniture, TVs, and glassware, are covered. You can only insure your personal contents with initio as an add-on to an owner-occupied home you also insure with us.

What else can you do to ensure you choose the best insurance provider for your needs?

When researching and comparing insurance providers, it’s essential to evaluate them based on their reputation, customer satisfaction, and claims processing efficiency. Reading customer reviews and testimonials can provide valuable insights into real-world experiences with different insurers. Additionally, carefully reviewing policy details, such as coverage limits, exclusions, excess amounts, and additional features, is crucial. Don’t hesitate to ask questions or seek clarification on any confusing terms or conditions.

Key takeaways

- Tailored insurance coverage: Ensure each property has the appropriate insurance policy based on its usage, whether it’s a primary residence or a holiday home.

- Personal belongings: Secure and appropriately insure personal belongings at both properties, ensuring valuables are covered and managed efficiently.

- Maintenance and security: Maintain regular upkeep and robust security measures for both homes to prevent risks associated with extended vacancies.

- Be aware of policy restrictions/conditions relating to how long a home is vacant for.

- Thoroughly research and compare to make an informed decision.

USEFUL LINKS

Smart Loyalty

Bachcare

Liability cover in house and contents insurance.

Liability cover in house and contents insurance protects you if you are legally responsible for accidentally injuring someone or damaging their property. In New Zealand, house insurance is not just about covering fire, natural disasters, or theft. The liability section can help pay legal costs and compensation if a claim is made against you. Understanding how liability cover works, what it includes, and when it applies can help you avoid significant out-of-pocket expenses.

Key takeaways in this article:

-

Liability cover in house and contents insurance protects you if you are legally responsible for accidental injury or property damage.

-

It can cover compensation payments and legal defence costs if a claim is made against you.

-

Cover can apply at your home and, in some situations, anywhere in New Zealand.

-

ACC covers medical treatment for injuries, but liability insurance may respond to other related claims.

-

Liability cover is automatically included in initio house and contents insurance policies.

What is liability cover in home insurance?

Liability insurance covers legal costs and compensation if you are legally liable for unintentional damage to another person’s property or for injuries they sustain due to your actions or negligence. It typically includes:

- Personal liability: If someone is injured at your home and you are responsible.

- Property damage liability: If you accidentally damage someone else’s property.

- Legal defence costs: If a claim is made against you, your policy may also cover legal expenses.

When might you need liability cover? Here are some common scenarios:

1. A visitor is injured on your property

If a guest trips over a loose step, slips on a wet floor, or is injured by a falling object in your home, they may seek compensation from you. The New Zealand ACC scheme typically covers injury-related costs, but it has gaps, such as claims for pain and suffering, property damage (e.g., clothing or personal items), and mental injury. In these cases, your home insurance liability cover may help with costs and legal fees if legal action is taken.

2. Your tree falls on a neighbour’s property

New Zealand’s strong winds and storms can cause trees to fall. If a tree from your property damages your neighbour’s home, car, or fence, you could be held responsible if you failed to take reasonable care.

3. Your kids or pets cause damage

If your child accidentally kicks a ball through a neighbour’s window or your dog escapes and damages someone else’s garden, liability cover can help pay for repairs or compensation.

4. You run into a vehicle while riding your bicycle

If you cause damage to other vehicles or property whilst navigating the streets on your bike, liability cover will cover those costs.

5. Water damage to a neighbour’s property

If a plumbing issue in your home causes water to leak into the adjoining unit or property, damaging walls, floors, or belongings, you may be liable for the cost of repairs.

6. You accidentally cause a fire that spreads

Fires can quickly get out of control, whether from a kitchen accident, an unattended candle, or a backyard BBQ. If a fire originating from your home spreads to neighbouring properties – damaging fences, homes, or belongings – you could be held responsible. If a neighbour makes a claim against you for repair costs or compensation, your liability cover may help cover the expenses, especially if negligence is a factor.

7. You accidentally cause damage while staying elsewhere

You’re visiting a friend’s house, and you accidentally knock over an expensive vase or damage a piece of furniture. Or, while browsing in a shop, you accidentally break a fragile item. You might be charged for the damage, but your liability cover may help cover the cost.

What’s typically not covered under the Home/Contents liability section?

While liability insurance provides broad protection, there are exclusions, such as:

- Intentional damage: If you deliberately cause damage, you won’t be covered.

- Business-related liability: If the incident occurs as part of a business activity, you would need separate business liability insurance.

- Liability due to unlawful activities: Any damage or injury resulting from illegal activities is not covered.

- Liability due to operating a motor vehicle (is covered under the vehicle’s insurance)

Conclusion

The liability section of a home insurance policy in New Zealand is crucial for protecting you from unexpected legal and financial consequences. Whether it’s accidental property damage, injury that falls outside ACC cover, or an unforeseen incident, this cover ensures you won’t face costly legal battles or compensation claims out of pocket.

All initio products automatically include liability protection.

You might also be interested in:

Two dwellings on the same title

Thinking about becoming a Landlord and renting your home?

Whether you’re considering becoming a landlord for the first time or looking to optimise your rental process, this guide covers some of the key aspects you need to know.

Key takeaways in this article:

-

Being a landlord comes with legal responsibilities.

-

Make sure your property meets Healthy Homes Standards.

-

Decide early between long-term or short-term renting.

-

Set rent based on local market research.

-

Screen tenants carefully and keep good records.

-

Standard home insurance does not cover rental risks.

-

Regular inspections and maintenance help avoid bigger costs.

-

Rental income is taxable, so check your obligations.

Renting out your home in New Zealand can be a great way to generate extra income, but it comes with responsibilities and risks.

Before you rent out your home

Get the right advice early

- Refer to Tenancy Services for the latest landlord specific advice such as healthy homes and legal requirements

- You may also want to join your local property investor association for support and advice – New Zealand Property Investors Association have various branches throughout New Zealand.

- Consider whether a professional property manager is right for you.

- Services like myRent can help with advertising, tenant management, and documentation.

Understand Healthy Homes requirements

Landlords must ensure their rental meets Healthy Homes Standards. This includes heating, insulation, ventilation, moisture control, and draught stopping.

Know your legal obligations

Under the Residential Tenancies Act, landlords must:

-

Keep the property in a reasonable state of repair

-

Lodge the bond with Tenancy Services

-

Provide proper notice for rent increases

-

Keep accurate records of agreements, inspections, and payments

Choosing the right strategy

Long-term rentals

Long-term rentals provide steady income and greater stability. They generally involve less turnover but require ongoing property management.

Short-term and holiday rentals

Short-term rentals, such as Airbnb, can earn more during peak seasons. However, they require more active management, cleaning, and compliance with council rules.

They also require commercial insurance, which can cost more than standard landlord cover.

Insurance differences to consider

Landlord insurance is designed to protect against tenant damage, loss of rent, and liability claims. Always check policy conditions, including inspection and tenant screening requirements.

Setting up your rental property

Set the right rent price

Research similar properties in your area to set a competitive rental price. Consider:

- Location and amenities

- Property size and condition

- Market demand

- Seasonal fluctuations

Websites like Trade Me Property and Tenancy Services can help you gauge market rents in your area.

Advertising your property

Advertise on platforms such as Trade Me Property, Facebook Marketplace, or use a property manager to find suitable tenants.

Screening tenants

Carry out proper checks before accepting a tenant. This may include:

-

Credit checks

-

Previous landlord references

-

Employment verification

Use Tenancy Services templates or services like myRent to ensure all legal terms are covered.

Protecting your investment

Why landlord insurance matters

Landlord insurance protects you from risks specific to renting, including malicious damage, loss of rent, and liability.

What standard home insurance does not cover

Home insurance is designed for owner-occupied properties, where the owner lives in the home. It is priced and structured around that lower risk profile. Once a property is rented out, the risk changes. There is less control over how the home is used, and there are additional exposures such as tenant damage, loss of rent, and liability issues.

Because of this, standard home insurance will not cover many rental-related risks. If your property is tenanted, you should have a landlord policy that is specifically designed for rental situations.

Your obligations under a landlord policy

Most landlord policies require reasonable tenant screening and regular inspections. Failing to meet these obligations can affect a claim.

Managing your property day to day

Routine inspections

Regular inspections help you identify issues early. Tenancy Services provides inspection checklists to guide you. myRent also have great resources in that regard.

Maintenance and repairs

Respond promptly to maintenance requests and budget for ongoing upkeep to avoid larger repair costs later.

Tracking rent payments

Use a clear system to track rent payments and maintain accurate financial records. Property management tools like myRent can assist with this.

Ending a tenancy correctly

Tenancy agreements

Ensure tenants sign a legally binding Residential Tenancy Agreement outlining rent, bond, and house rules.

Notice periods and bond refunds

When ending a tenancy, follow the correct notice periods and manage bond refunds according to legal requirements.

Understanding tax responsibilities

Rental income is taxable in New Zealand. You may also be able to claim expenses such as:

- Property management fees

- Mortgage interest (if applicable)

- Repairs and maintenance

- Insurance and rates

Check with an accountant or Inland Revenue (IRD) for guidance on tax obligations.

Final thoughts

Renting out your home can be financially rewarding, but success depends on understanding your legal duties, choosing the right rental strategy, and arranging proper landlord insurance. Taking time to plan now can help you avoid costly mistakes later.

If you’re considering renting your property, take the time to research and seek professional advice where needed to avoid common pitfalls.

You might also be interested in:

- What does landlord insurance cover?

- Landlord insurance fundamentals

- Guide to landlord insurance

- What is landlord insurance?

- Landlord insurance for multiple rentals

- Can I complete remote property inspections?

Five Tips to Insuring in a Flood Zone

Floods are the biggest cause of natural damage to property in New Zealand. Much of our country has a high flood risk, meaning many properties lie in or near flood zones. This makes insurers cautious when it comes to flood-prone houses.

The 2017 Edgecumbe flood was one of New Zealand’s worst in recent history.

If you’re looking at buying a flood zone house, we recommend you follow these five steps.

1. Check the LIM Report

The easiest way to find out if your house is in a flood zone is to read over the LIM [Land Information Memorandum] report for the house.

If the house has been identified by the council as being at risk to any natural hazards (including floods) this will be included in the LIM report. The Certificate of Title will inform you if a Section 36, 73 or 74 of the Building Act has been issued.

In simple terms, this means when getting building consent on the house, a natural hazard risk is declared.

The LIM report should provide you a good overview of the extent of the flood risk to the house.

2. Check online council hazard maps

If you don’t have access to a LIM report or do not want to pay for one, you may be able to find flood risk information online.

Most local councils now release public online Geo Mapping for natural hazard risks on houses. Unfortunately, each regional council has different maps so you will need to find the relevant one for your home.

Try searching the internet for your local council’s name and adding ‘hazard maps’ to your search term.

If you can find your council’s online mapping tool you will then need to filter through the different natural hazard types. Then enter your address and add the flood zone layers and you will be able to see how and if your property lies over a flood zone. There should also be information available about the extent of the flood risk.

3. Be prepared to pay more

If your house is in a flood zone it is likely you will be able to get cover. But it may not be with your first choice as insurers are more likely to decline cover in flood-prone areas.

Depending on the extent of the flood risk at your house, you may either pay more for a premium or have a significantly higher flood damage excess.

If we accept cover on your flood zone property, we may apply an imposed flood endorsement with a higher excess. An example of this endorsement can be seen below.

Example Flood Endorsement

| We will not pay for any costs of additional materials, work or expense required solely to comply with Government or local authority bylaws and regulations, if those costs are required solely to meet the requirement of Government or local authorities to reduce the exposure to a natural hazard at the home.

|

4. Check how extensive the flood zone is

Flood zones cover much of New Zealand. Some are higher risk while others might only be minor, meaning it’s important to get an idea of the extent of the flood risk.

Risk is usually defined by the yearly frequency. The most common are 100-year flood zones. This means research and history predicts there is a 1-in-100 chance of a flood event each year.

If there is a 1-in-50 year, this means a flood is twice as likely to occur in any given year. A lower risk flood zone might only be a 1-in-200 year.

You can generally find this information either on the LIM report or mentioned on the council data.

5. Check the property isn’t at risk to other natural hazards

If you have a LIM report or found information online, it also pays to check the house is not at risk of other natural hazards.

Common natural hazard risks to houses in New Zealand include landslips and subsidence, or coastal erosion if the house is near the ocean.

Places like Whangarei are particularly prone to both landslips and flooding. It’s also common for flood zones to be around coastal erosion areas. Checking this will give you a much better understanding of the overall risk to the home.

How do I get insurance on my home that is within a flood zone or is within another high natural hazard area?

You can apply for insurance on your flood zone property by getting an instant quote via the button below. Please note the flood risk will need to be disclosed to us when you send an application. If you fail to disclose this to us, you risk having a future claim declined for non-disclosure.

In some cases, we can’t provide cover

As an online insurer we have limited scope to provide custom or bespoke terms. Properties within some of the higher natural hazard zones often require adjusted premium and terms. If we are sure that your property is one of several identified zones we will do our best to let you know up front when you check for a quote. Therefore, in some cases our system will let you know instantly, the hazard zone identified and that we won’t be able to provide terms at this time.

Submitting a referral

If you are able and would like to proceed with your quote, select your preferred payment option at the bottom of the quote. You will then need to disclose the flood risk and any other relevant information during the declaration questions in the application.

This will submit a referral to us which we can then review. You will not have to pay for the policy at this stage.

We may confirm to provide insurance cover on your home, or we will ask for further information if required.

Flood & Landslip Questionnaire

If you still have questions, you can complete our Flood and Landslip Questionnaire and email it to [email protected] along with any supporting documentation. We will then review your application and confirm if we can provide insurance on your home.

If you have suffered a flood and are wanting advice on your claim, please refer to our helpful claim guide.

Privacy Policy

This is the website of Initio Limited (initio). The administration of the website is performed by initio. The arranging of insurance contracts on this website, as well as policy and claims management is the responsibility of initio. ‘We’, ‘us’, and ‘initio’ refers to Initio Limited.

The postal address for initio is:

PO Box 319, Hamilton 3204

The physical address for initio is:

Level 1, 6 Garden Place, Hamilton Central, Hamilton, New Zealand

All email correspondence can be directed to [email protected]

Our telephone contact number is + 64 7 929 4126.

Our web server automatically recognises a user’s domain name.

We collect:

- Email addresses of those users that communicate with us via email.

- Email addresses of those who make postings via online chat.

- Email addresses (and other personal information as supplied by the customer) of customers who chose to transact with us, including users who email themselves a quote from our website.

- Aggregate information, data, and record of pages unidentified users access or visit, and how they interact with those pages.

- User-specific information, data and record of pages a customer accesses, completes, or visits, and how they interact with those pages.

- Information volunteered by the customer/user during the quote, sign-up and claims process.

- Specific personal contact and other information as supplied by the customer/user during the insurance signup and claims process.

- Risk data about properties or vehicles that we may quote on or insure. We may use third parties in order to collect this data.

- Personal contact information (including but not limited to email address, property location, and phone number) and risk information supplied to us by our partners, affiliates, and resellers through referral programs and other methods.

We Store:

The above information on our secure servers and related software and database applications.

The information we collect is:

- Shared with insurers (and their agents) who assist in providing support for the insurance placement, our internal operations, and underwriting of risk.

- Shared with an association, club, buying group or other business that are partners of initio and that our customer is a member or customer of. This information is limited to the customers name, the address of the insured property or vehicle year/made/model, effective date of cover, expiry date of cover, insurer premium, type of transactions (eg renewal), and payment type and interval

- Shared with broker partners who have advised their customer to insure with initio, and that cover has been placed through that broker’s dedicated gateway or page.

- Used by us to contact consumers by phone, email, or text message for marketing, follow-up or feedback purposes.

- Disclosed when legally required to do so, at the request of governmental authorities conducting an investigation and audit.

- Used to verify or enforce compliance with the policies governing our website and applicable laws or to protect against misuse or unauthorised use of our website.

- Disclosed to any successor entity in connection with a corporate merger, consolidation, sale of assets or other corporate change.

- Used to underwrite and bind insurance policies.

- Used to submit claims to insurers.

- Shared with associated suppliers, current or prospective insurance capacity providers,and service providers for claims processing and management.

- Used for all other purposes relating to the placement and management of a customer’s insurance.

- Shared with storage providers (including “cloud storage”) within New Zealand and overseas. We use reasonable endeavours to ensure people we disclose your personal information to outside New Zealand are required to protect it in a way that provides comparable safeguards to those set out under New Zealand privacy law

We Share:

With referrers/affiliates: where you have been introduced to initio by a Referrer or Affiliate we will share with that Referrer your name, your initio client number, and when you transacted with us.

If the Referrer is the market comparison website Quashed, as per your arrangement with them, we will share additional information including the address of the insured property and provide to them a copy of the initio policy schedule.

With partners: Where you have been introduced to initio by a Partner organisation (such as the New Zealand Property Investors Association or a Mortgage Advisor), of which you are a customer or member, we will share with that Partner the location of the risk (eg address of house insured), the period of insurance cover, the premium, the type of transaction (eg renewal, or new), the payment type and interval (eg annually or monthly), and if applicable the particular business, branch, office or region you are associated with.

With insurance brokers: Where your insurance placement has been facilitated through a broker, we will share with that broker the information we collect (as defined above). The way we do this is through reporting, and by providing your broker with copies of all communications and documents. For example, any email a customer receives from us will also be copied to that customer’s broker. This includes sharing with the broker the information about and correspondence we have with you, relating to any claims you make with us. We may also share information with the customer’s broker on specific request from the broker, and this may include but is not limited to claims records, claims status, policy insured values, excesses and the like.

With insurers: Initio is underwritten by a registered Insurer. We will share the collected information with this insurer either automatically or on request from the insurer. The insurer holds the ultimate risk for the customer’s insurance, and the information we collect is relevant for that insurer’s underwriting of the risk and assessment of claims.

With advertising providers: We may share certain information with advertising platforms to deliver and improve our marketing campaigns. This includes identifiers, website interaction data, and transaction information necessary for campaign measurement and optimisation.

You have the right to:

1. Request all information that is held about you by us.

2. Request that information held about you is corrected.

Cookies:

Cookies are small data files that a website host computer sends to, or installs on, a user’s computer to help it remember information you enter, by passing a unique ID between your computer and the initio website that identifies you.

We use ‘first party’ and ‘third party’ (including, but not limited to, Google Analytics, Google Signals and Hotjar) cookies on our website. The information recorded and tracked includes:

- Information that users/consumers input when obtaining quotes or filing in the online forms.

- User-specific information on pages users access, visit, complete.

- Past activity on our site in order to provide better service when visitors return to our site.

- Data on user behaviour and their devices (and across those different devices), including device screen size, device type, browser information, country location,

We use this information to help us understand how you engage with our website and enhance your experience while visiting our website.

Google Analytics & Signals

This technology enables initio to obtain visitation information across multiple devices (eg laptop, phone) when a user is signed-in and who have consented for this association with google. The google information may include end user location, search history, youtube history, and data from other sites that partner with Google. The information is aggregated and anonymised.

You can access your Google Analytics data and / or delete it by visiting My Activity.

Hotjar

Hotjar is a technology service that helps us better understand our users’ experience (e.g. how much time they spend on which pages, which links they choose to click, what users do and don’t like, etc.), it enables us to build and maintain our service by means of user feedback, and it allows us to track user specific information including sign-up form errors and the completion of online forms, such as claim forms. Hotjar also uses cookies and other technologies to collect the data For further details, please see Hotjar’s Privacy Policy.

Specifically, we use Hotjar’s User Attributes service which includes Personally-Identifying-Information (PII). On your request, by email to the address above, we will delete the Hotjar PII we hold on you.

Changing or disabling cookies

If you do not want to be recorded by Hotjar, you can disable it by setting the DoNotTrack header in your browser. For more information and more about Hotjar’s data processing, please visit: www.hotjar.com/legal/compliance/opt-out.

You can choose to delete or change the settings of your cookies from your internet browser.

NZ Motor Vehicle Register

Waka Kotahi NZ Transport Agency (NZTA) administers the New Zealand Motor Vehicle Register, which contains information about vehicles in New Zealand and the people they are registered to.

Initio Limited may access the Motor Vehicle Register for the purposes of assessing or processing an insurance policy or claim in relation to a vehicle, pursuant to section 241 of the Land Transport Act 1998 (LTA) and Gazette Notice 2022-au4072 of 28 September 2022.

If you prefer not to have your name and address accessible through the Motor Vehicle Register under section 241 of the LTA, you can notify NZTA. Visit www.nzta.govt.nz for details on what the Motor Vehicle Register entails and how to opt-out.

General:

- If you do not want to receive email from us in the future, please let us know by sending us an email to the address noted at the top of this page.

- If you supply us with your postal address online you may receive periodic mailings from us with information on new products and services or upcoming events. If you do not wish to receive such mailings, please let us know by emailing or calling us. You may also receive emails from us with a quote to insure that address if it is a residential address that is not already insured with initio.

- Persons who supply us with their telephone numbers online may receive telephone contact from us with information regarding renewals, support, new products and services. If you do not wish to receive such telephone calls, please let us know by sending us email at the above address.

- If our information practices change at some time in the future we will post a new version of the privacy policy to our site. Once updated you are deemed to be given notice of our new policy.

- Through the customer dashboard, which can be accessed by the customer with a password protected login, we provide customers with access to transaction information (e.g., dates on which customers made purchases, amounts and types of purchases) contact information (e.g., name, address, phone number) that we maintain about them, current and historical invoices and covers, current and previous claims information.

- Customers can have this information corrected by updating the information on the dashboard or by email to the above address.

- We ask for customer reviews of our service. We do this online after a new policy, a renewal of a policy, or after a policy alteration. If the customer provides a review or star rating, we may use this customer provided star rating and the feedback provided to let other customers know what other customers think of initio. The review or star rating will display as a first name, the date the review was provided, the geographic location, and the insurance cover the review relates to. For example, John from Hamilton, 8 August, Landlord Cover. We will never reveal a customer’s full name or contact information.

- We may use this review feedback on our website or as part of marketing material that is published outside of our website.

- By providing a review, you consent to the way we will use this information. We can remove or adjust your review on your request by email to the above address.

- With respect to payment security and when we pass financial and credit card information we use secure third partes, Windcave Hosted Solution, and Stripe.

If you feel that this site is not following its stated Privacy policy, please contact us to discuss.

Last updated: 19/01/2026

Top 5 things to check for in your Landlord Insurance policy

As a landlord, the risks to which you are exposed are often not covered by a standard insurance policy. When taking this next step on the property ladder it is important to have the right Landlord Insurance cover in place to save yourself from headaches down the track.

Does your policy cover your tenanted house? While it seems obvious, a standard house insurance policy is designed to cover owner occupied homes, if you were to make a claim and the insurer discovered the house was tenanted your claim could be declined. If you have listed your holiday home for rent or if you have recently moved out of your own home and tenants have moved in, make sure you have notified your insurance provider, and they have the correct Landlord Insurance cover in place.

Does your policy cover loss of rents? Following a claim for property damage to your house, there will likely be a period where it is uninhabitable while you wait for the repairs to be carried out and completed. You are going to want your Landlord Insurance to pay for your lost rental income during this time. Make sure that the policy will pay out for at least 12 months, and that the limit is large enough to cover the week rent – ie $20,000 over 12 months is up to $385 per week.

Does your policy include cover the carpets? House insurance policies often only cover floor coverings that are glued to the floor, while most carpet is tacked. Therefore, it is important that your Landlord Insurance policy includes cover for your contents. Make sure this amount is enough (we recommend at least $20,000) to cover your appliances, carpets, drapes, blinds and other furniture that remains in the house while it is tenanted.

Does your policy include damage caused by your tenants? Generally, your insurance policy will exclude deliberate damage caused by a person living at the house, so if your tenants intentionally damage your house you may not be covered. A good Landlord Insurance policy will include cover for malicious or deliberate damage by tenants.

Does your policy continue if your house is vacant? Some policies will cease cover if the house is vacant. So, if it takes longer than expected to tenant your house, or if you have no bookings at your holiday home over the winter, you might not have any insurance cover. Look for a Landlord Insurance policy that will continue to provide cover even while the house is unoccupied.

If your tenants are holding the keys to your retirement savings, you don’t want to leave anything to chance. The initio policy was designed specifically for rental houses and holiday homes, so you can rest easy knowing that one of your largest assets is in safe hands. To get a quote visit initio.co.nz.

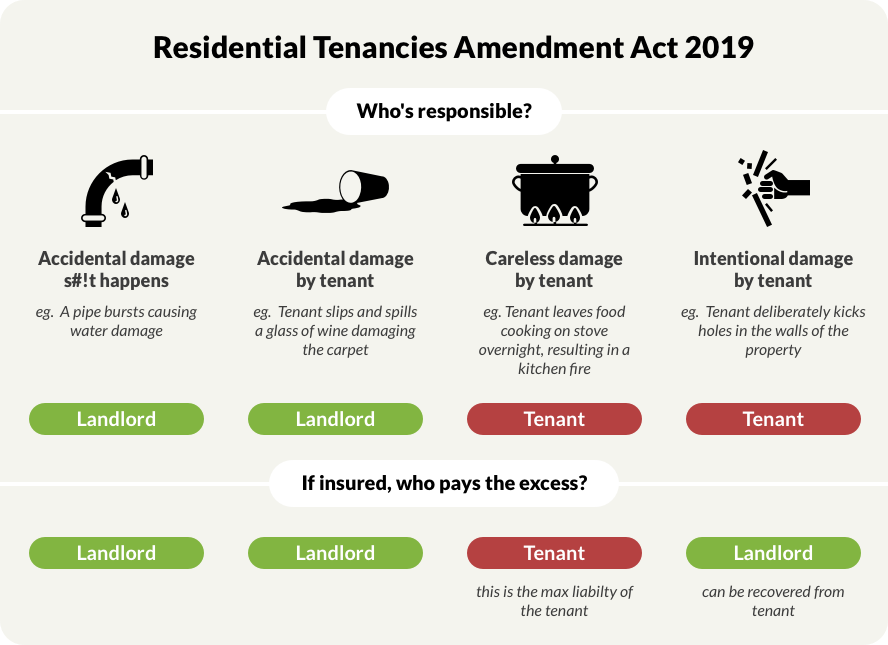

Residential Tenancies Amendment Act – who now pays for damage?

On 30th of July 2019 changes to the legislation around tenant damage and meth contamination were passed into law.

The Residential Tenancies Amendment Act 2019 will:

- limit tenants’ liability for careless damage in rental properties to the landlord’s insurance policy excess or 4 weeks rent (whichever is less)

- re-open the ability for the landlord to recover against the tenant for damage, albeit on a very limited basis

- allow tenants to share in and receive protection from the landlord’s insurance policy

- mean that landlords must provide confirmation of insurance cover to all new tenancies and their exisiting tenants on request

- prevent insurers from pursuing tenants for unintentional damage (ie careless or accidental damage)

- allow for regulations to be made to address how contamination (eg. meth) of rental properties is tested and managed

- give the Tenancy Tribunal full jurisdiction over cases concerning premises that are unlawful for residential purposes, such as garages and sleep-outs, which don’t meet minimum requirements for renting

- protect tenants living in those unlawful premises, as the Residential Tenancies Act will now apply

- give Tenancy Services the ability to take enforcement action against landlords who rent properties which don’t meet minimum standards

These changes are scheduled to take effect on 27 August 2019. The provisions of this new Act only apply to damage occurring after this date.

So, I’m a landlord, how do these changes affect me and my insurance?

It depends on how the damage has been caused. There are four ways a rental property can suffer damage:

Accidental Damage – S#!t Happens eg. storm damage

Accidental damage is damage that can’t be avoided, because sometimes s#!t happens. This could be caused by an ‘act of god’ type loss such as a storm causing damage to the roof of the property. Or it could be a leaking water pipe or an electrical fire. This type of damage is completely outside of the control of the tenant liability, and as such they have no liability for this damage. The landlord is responsible for this damage, and will usually have insurance to pay the claim.

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Accidental Damage by Tenant eg. spilling a glass of red wine on the carpet

Accidental damage can also be caused by a third party, such as a tenant. This could come in the form of a tenant tripping and spilling wine on the carpet, or their washing machine flooding. In both cases these are technically outside of the control of the tenant and there is no liability on the part of the tenant. So even if the tenant causes the accidental damage, the tenant has NO liability. The tenant can rely on the landlord’s insurance policy the repair the damage, and the tenant cannot be made to pay the insurance excess (or 4 weeks rent).

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Careless Damage by Tenant – eg. leaving a pot cooking on the stove and going to bed

Where a tenant (or their guest) carelessly causes property damage to the home, they are liable for those damages. This could be where the tenant leaves a pot cooking after going to bed and causes fire damage to the kitchen. While the amendment to the act now makes the tenant liable, the maximum amount the tenant can be held responsible for is the landlord insurance policy excess, or 4 weeks rent (whichever is lesser). The new Act effectively allows the tenant to share in and receive the benefit of the insurance arranged by the landlord.

- Who is responsible for the cost of the damage? answer: the tenant (but its capped at the lessor of the landlords insurance excess or 4 weeks rents)

- Who pays the insurance excess? answer: the tenant (see pain points below)

Intentional damage by Tenant – eg. smashing holes in the wall

A tenant is not excused from liability when the damage is intentional or where the damage they (or their guest) have caused constitutes an imprisonable offence. In such circumstances the responsibility is on the tenant to notify the landlord of the damage. The landlord can request that the tenant repair the damage, but if the landlord is properly insured (ie has an initio landlord insurance policy) they will be covered for intentional damage so its best to lodge a claim for the damage, and allow the insurer to pursue the tenant for the cost of repairs.

- Who is responsible for the cost of the damage? answer: the tenant

- Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the incurred to repair the damage)

What about Methamphetamine Contamination?

The Act allows landlords the right to enter the rental property (after providing notice to the tenant) to sample and test for meth contamination. If testing confirms that the property is contaminated to unsafe levels (currently higher than 1.5 μg per100 cm2) then the landlord, and the tenant, have rights to terminate the tenancy. The landlord can terminate with a minimum notice period of 7 days, whereas the tenant can terminate with only 2 days notice.

Meth testing must be done in accordance with the Standards New Zealand standard, and the landlord must notify the tenant within 7 days of receiving the test results.

If a landlord knowingly rents a property with meth contamination, the tenant can be awarded damages of up to $4,000.

We are still awaiting further details around this and exactly what standard will be set by the Housing Minister. Currently the NZ Standard, which the insurance industry follows says that a property is contaminated if the presence of meth exceeds 1.5 μg/100 cm2, however the Gluckman Report, which the tenancy tribunal follows says that a property is contaminated if it is more than 15 μg/100 cm2. We are expecting that the amendment to the Residential Tenancies Act will provide some consistency and that we will all move to 15 μg/100 cm2 as being the level where contamination occurs.

Given that the possession of meth can attract a penalty of up to 6 months imprisonment, and manufacture of meth a maximum penalty of life imprisonment, if use/possession or manufacture is proven at the property the tenant is NOT excused from liability and has NO protection from the landlords insurance policy. The landlord or their insurer can recover the cost of cleanup and repair from the tenant.

Who is responsible for the cost of the damage? answer: the tenant

Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the insurer incurs to remediate the property)

Important: The likelihood of recovering costs from a tenant for meth damage is extremely low. Firstly proving it was the tenant is difficult, and secondly meth addicts generally don’t have the financial resources to pay for such large repairs.

Where are the pain points with these changes?

Accidental vs Careless

As accidental damage means that the landlord pays the excess, and careless damage means that the tenants pays the excess, we expect to see disagreements between landlords and tenants about the cause of the damage. If the landlord and tenant cannot agree whether the tenant is liable for the damage, the landlord can apply to the Tenancy Tribunal for the matter to be resolved. Copies of relevant insurance policies, photos of the damage, and receipts or quotes for repair should be included to support the application.

Is meth contamination careless or intentional?

We believe it is intentional but fortunately the new Act catches meth under the category of imprisonable offence. We anticipate that tenants (and maybe the courts) will continue to argue that the resulting damage from smoking meth is careless not intentional. Our opinion is that there is now enough information in the public domain for people to understand that meth causes property damage.

A tenant has carelessly damaged my property, I’ll leave the tenant to pay the excess to the insurer/repairer?

If you establish that the tenant has been careless this won’t mean that its a slam dunk on the tenant physically paying the excess.

We foresee there will be arguments over who physically pays the excess to the insurer or the repairer. Is it the insurer or is it landlord? Given that the policy owner is the landlord this suggests that the landlord would need to pay the excess and then recover it from their tenant. This may change in time as the new Act is tested with real loss scenarios.

We recommend that as soon as the landlord becomes aware of, and can establish that “careless damage” has occurred, that they hold their tenant responsible for the excess and request immediate payment.

What do I need to do?

You will need to provide a confirmation of insurance certificate to your tenant

Landlords are now required to provide all new tenants, and existing tenants where they request it, details of their property insurance. Any changes made to your insurance, also need to be notified to your tenants. Failure to do so could result in a $500 fine to be paid to the tenants. You can provide the tenant with a standard certificate of insurance but this will have more information on it than you are required to disclose (such as the Bank that has a mortgage over your property). Some insurers like initio have produced a specific Tenant Certificate. To obtain a Tenant Certificate of insurance to provide to your tenant or property manager you can get this through your initio dashboard.

Seeing the tenant is paying should I increase my excess?

Probably not – as the tenant only responsible for paying the excess some of the time.

A number of landlords have mis-interpreted that the tenant will pay the excess on all types of claims, and have moved to increase their insurance excess to align with approximately 4 weeks rent.

Remember that if you increase your excess, the higher excess will apply to ALL claims, not just the ones that the tenant is responsible for. The measure of tenant responsibility is carelessness so as a landlord you need to be able to establish that your tenant was careless in order to recover your excess from the tenant.

How do I increase my excess?

With initio you can easily do this by logging in to your dashboard and modifying your policy excess, and the credit premium adjustment will be refunded to you.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

Financial Advice Provider Disclosure Statement

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: | Initio Limited |

| FSP Number: | FSP523166 |

| Website: | www.initio.co.nz |

| Phone: | 0800 763 929 |

| Email: | [email protected] |

| Address: | 6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: | Suzanne (Suze) Ferry |

| FSP Number: | FSP566306 |

| Contact Email: | [email protected] |

| Qualifications: | New Zealand Certificate in Financial Services (Level 5) |

| Experience: | 26 years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type | Commission Rate |

| House and contents insurance | 22.5% of insurer premium portion |

| Motor vehicle insurance | 10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.

- Commission income: Initio receives commission from IAG on policies sold through us. This could create an incentive to recommend insurance cover that may not be in your best interests.

- Referral payments: We may pay commissions to partners and brokers who refer clients to us, which could influence the recommendations made to you by those third parties.

- Ownership Interest: Suze Ferry holds a shareholding interest in Initio. This means that Suze Ferry has a financial interest in the commercial success of Initio, including through the sale of Initio insurance products. This ownership interest could be perceived as creating an incentive for this adviser to recommend Initio products, or recommend a higher level of cover, in circumstances where that may not be in your best interests.

How We Manage These Conflicts

Initio manages these conflicts of interest in the following ways:

- Our financial advisers are paid a salary only and do not receive any commission, bonus, or incentive linked to the sale of policies or claims outcomes.

- We require all financial advisers to follow an advice process that ensures recommendations are based on your goals, circumstances, and needs.

- Where your needs fall outside the scope of our products, we will refer you to a specialist insurer or broker rather than recommend an unsuitable product.

- All financial advisers undergo training on how to manage and disclose conflicts of interest.

7. Reliability Events

A reliability event is something that might influence your decision about whether to seek or act on our financial advice. Examples include a successful regulatory action, a bankruptcy, a criminal conviction for dishonesty, or a prohibition order by a regulatory body.

Neither Initio, nor Suze Ferry, has been subject to a reliability event.

8. What to Do If Something Goes Wrong

Internal Complaints Process

If you are not satisfied with our financial advice service, we encourage you to contact us as soon as possible so that we can try to resolve your concern. You can make a complaint by:

- Email: [email protected]

- Phone: 0800 763 929

- Post: The Complaints Manager, PO Box 319, Hamilton 3204

When we receive a complaint, we will consider your concerns and let you know how we intend to resolve them. Where possible, we will try to resolve your complaint immediately. If we are unable to do so, we will acknowledge your complaint within 2 business days and work with you towards a resolution.

External Dispute Resolution

If you are not satisfied with the resolution of your complaint under our internal complaints process, you can refer the matter to our external dispute resolution scheme. This is a free and independent service.

Initio is a member of the Insurance & Financial Services Ombudsman Scheme (IFSO Scheme).

| Scheme: | Insurance & Financial Services Ombudsman Scheme (IFSO) |

| Phone: | 0800 888 202 |

| Email: | [email protected] |

| Website: | www.ifso.nz |

| Post: | PO Box 10-845, Wellington 6143 |

9. Privacy

We collect and use your personal information to provide you with financial advice and to arrange and administer your insurance policies. Your personal information is handled in accordance with the Privacy Act 2020 and our Privacy Policy, which is available on our website.

For more information about how we collect, use, store, and disclose your personal information, please refer to our Privacy Policy at https://initio.co.nz/privacy-policy/.

10. Further Information

You can check that Initio is a registered and licensed financial service provider, and verify the registration of your financial adviser, at the Financial Service Providers Register: www.fspr.govt.nz.

This Disclosure Statement is current as at the effective date shown. We will provide you with an updated disclosure statement if there is a material change to the information contained in it.

This information is also available in writing, on request.

This disclosure statement was prepared on: 15th March 2021

This disclosure statement was updated on: 31st March 2026

Financial Advice Provider Disclosure Statement

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: | Initio Limited |

| FSP Number: | FSP523166 |

| Website: | www.initio.co.nz |

| Phone: | 0800 763 929 |

| Email: | [email protected] |

| Address: | 6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: | Rene Swindley |

| FSP Number: | FSP122087 |

| Contact Email: | [email protected] |

| Qualifications: | New Zealand Certificate in Financial Services (Level 5) |

| Experience: | 20 years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor Vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.