Search results for: {search_term_string}/page/house-insurance-calculator

At Initio Insurance, we require an agent or a trusted representative physically present at the property for inspections. This ensures a thorough evaluation of the property’s condition and facilitates real-time reporting, serving as your on-the-ground resource.

Advantages of having an in-person representative include:

- Real-time condition verification and data reporting during the inspection process.

- Being your dedicated eyes and ears on the ground, diligently checking the property’s condition.

- Early identification of any potential issues, damages, or repairs that could potentially be missed in a purely remote inspection.

However, we understand there may be special circumstances such as illness or lockdowns where remote inspections become necessary. These should be exceptions rather than the norm. In such cases, a trusted representative or official agent’s physical presence during the inspection is critical to maintain the assessment’s accuracy and comprehensiveness.

Looking ahead, we’re mindful of emerging technologies that could potentially streamline remote inspections. However, as of now, the value of in-person inspections is paramount. Always remember that our advice serves as a guideline, not an inflexible rule. Each property and situation may require a different approach, and decisions should be tailored to your specific circumstances and needs.

Learn more about how often you need to inspect your property

Heading out for a holiday or needing to leave your home for a bit? There are some easy steps you can take to make sure your home doesn’t become a victim to unwanted attention without you.

Take holiday precautions

When you’re planning to leave your home for a holiday or any reason, there are practical steps you can take to keep it safe and secure. It’s not just about locking doors or turning off appliances. We’ve got straightforward advice to help you relax, knowing your home is looked after while you’re away. Here’s how to prepare your property for your absence, which also helps in maintaining your insurance cover.

Engage a Trusted Person

Ask a neighbour, friend, or family member to look after your property. They can collect mail, water plants, and make the property appear lived in. This is important for keeping your home safe and meets the requirement for regular check-ups, especially for holiday homes.

Utilise Smart Home Technology

Investing in smart home technology can offer peace of mind while you’re away. Smart lights can be programmed to turn on and off at set times, mimicking the presence of someone at home. Smart water sensors can alert you or a trusted contact to any potential leaks, reducing the risk of water damage.

Garden and Exterior Maintenance

Ensure your garden and the exterior of your property are well-maintained before leaving. Overgrown gardens can signal an unoccupied home, attracting unwanted attention. If you’re away for the long haul, maybe hire someone to look after your gardens to keep things looking loved.

Secure Valuables

If possible, secure valuables in a safe or take them with you. This reduces the risk of theft and ensures that your most precious items are not left unattended in an empty property.

Update Your Contact Information

Ensure your insurance provider has your current contact information, including an emergency contact number. This allows us to reach you promptly if any issues arise with your property while you’re away.

Review Your Policy

Before leaving, review your policy details to ensure you understand your cover and any actions you need to take to maintain this coverage. If you have any questions or need clarification, it’s a good idea to contact us for peace of mind.

By following these steps, your home will remain secure, ready for your return from any adventure.

Make sure your unoccupied property qualifies for cover

On the subject of taking holidays, perhaps you’re wondering about cover for your unoccupied property? If your property is left empty, vacant, or unoccupied, you don’t need to notify us. But there are some conditions.

- For rental and owner-occupied properties, your coverage remains unchanged for up to 60 consecutive days of being unoccupied. However, if unoccupied for over 60 days, a standard excess of $5,000 applies to all claims, reduced to $1,000 if there’s a break-in with a professionally installed (and monitored) alarm*.

- For owner-occupied homes, after 60 days, coverage is limited to major risks like fire, explosion, and natural disasters, excluding theft and vandalism.

- Holiday homes can be unoccupied for over 60 days, but require regular inspections, maintenance, mail clearance, water shut-off, and secure locking. Failure to meet these conditions results in a standard $5,000 excess, reduced to $1,000 for break-ins with a professional alarm system* that provides external alerts.

*Surveillance cameras only do not meet this criteria – the system needs the ability to provide an external alert (audible or direct to a monitoring company)

OTHER ARTICLES OF INTEREST

This article is only meant as a general guide. We recommend reading the full policy wording for the full details of the coverage.

Do you know what goes on in your property?

One of initio’s first ever claims was a large fire caused by a child playing with matches in a wardrobe. While this is rather cliche, it does happen, and the consequences can be very serious. Fortunately, working smoke alarms meant no one was injured, and initio picked up the tab for the damage to the house.

Please use this as a friendly reminder that all your properties should have working smoke alarms which are tested regularly.

It’s common for older houses to have un-consented garages. Usually this is because a garage was added to the house without a full code of compliance being approved. This doesn’t necessarily mean the garage isn’t up to standards and can’t be covered.

To cover an un-consented garage it will need to meet the below requirements:

- Garage is structurally sound, well maintained and has no known defects.

- Structure would have met building requirements at the time it was built.

- If code of compliance was requested, it would have been issued.

If you can meet the above then it’s likely we can provide cover on our standard terms. However, if there’s a loss that’s directly cause by the garage’s non-compliance or because it isn’t built to standards, it may not be covered.

You’ll also need to disclose the un-consented garage on your application.

For more information see our full guide on insuring un-consented houses here.

Other articles of interest

Do you need confirmation of cover?

What is initio and how does it work?

Initio’s policy wordings

What we do not cover at initio

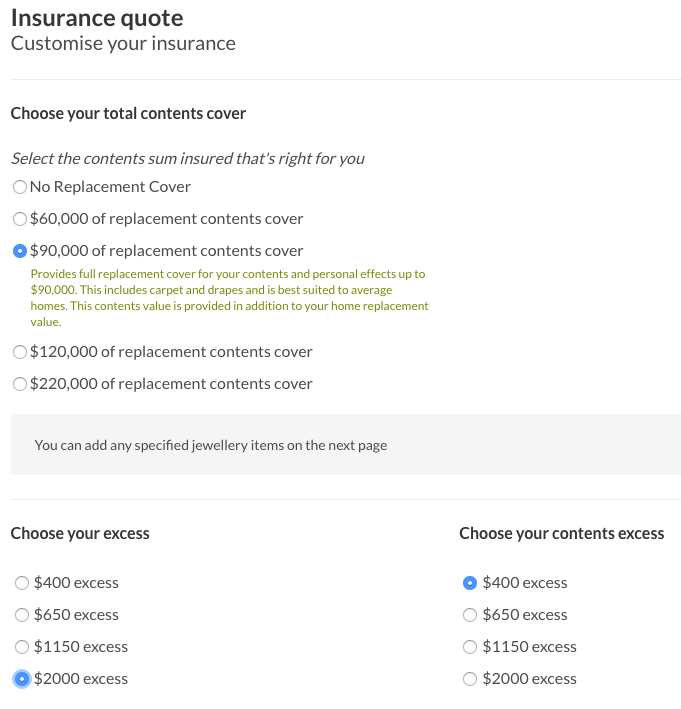

Often when we talk to our customers, and they tell us how much they love initio; unfortunately that can be followed by a but…. The most common ‘but’ we hear is that they don’t want the same excess for their home and contents. We agreed that was a reasonable request and put our developers to work.

The benefit of having an in house development team is that we can make changes on the fly. So even though this wasn’t a schedule update; we found some time between two larger development projects and got it done. The best part about making a change like this is the validation. The very next day after rolling out the update, we had an exisiting customer log in to their dashboard and insure their own home and contents. They were able to choose a $2,000 excess on their home, and a $400 excess on their contents.

Initio loves satisfied customers, which is why when something isn’t quite right, we make the necessary changes to improve it. And on that note, it is back to our next project – monthly payments.

Do you know what goes on in your property?

One of our customers suffered a devastating house fire at their multi-unit rental property. Here are some basic proactive steps you can take to protect your property.

- Check power points for overloading and consider installing additional power points

- Install safe and efficient heating sources such as a heat pump

- Remove curtains from kitchen windows as these are excellent fuel sources for fires

- Have registered electrician check the condition of the electrical wiring if there are any concerns.

Please use this as a friendly reminder that all your property should have working smoke alarms which are tested regularly….. And never let your kids play with matches.

Initio is loving local real estate ‘disruptor’, Hermitty, the new website that helps people save time, stress and thousands of dollars by swapping homes permanently instead of selling them.

Swapping homes creates an even playing field. It doesn’t matter what each property is worth, it only matters what the value gap is. The difference between agreed house values may be addressed by a cash payment or you could decide to include chattels or even a boat. It’s up to you how you swap.

Thought about trading that inner-city apartment for a lifestyle block further South? Why not list your property and see what future home may be out there? It’s free to list and you pay a one-off fee of $98 to chat to as many home owners as you like. They’re like a dating agency for homeowners!

Hermitty is for everyone who owns a home and wants to swap. It’s all about the chat so no legal agreements happen on the site. Once you’ve found someone to swap with then all the contract negotiation happens directly between the two parties and their lawyers.

Find out more about Hermitty here.

Getting in touch with us

We are all about online insurance so we can better understand your query if you send us an email or chat with us online (see the green button at the bottom right of screen). But do feel free to give us a call.

Phone:

0800 763 929

From Overseas:

+64 7 929 4126

Email:

[email protected]

Claims

Claims can be lodged and you can follow progress on your Initio dashboard. But you can also get hold of us using the following:

Claims Assistance (monday-friday 8.30-5.00):

0800 763 929

Claims Emergency Only (IAG after hours)

0800 560 333

Post

By Mail:

PO Box 19497, Hamilton

In Person:

6 Garden Place, Hamilton

Identifying and eliminating risks in your holiday home is important for the ongoing enjoyment of your property.

In 2013 the biggest cause of loss in holiday homes for Initio was water damage. This occurred in a number of cases where leaking or burst pipes caused significant damage while properties where unattended. Unfortunately this is only discovered when the would-be holiday makers arrive at the property to start relaxing.

Risk management includes prevention of loss or damage as well as general up keep of your property, our top tips for counteracting loss include:

- Turn off the water at the mains whenever tenants and family leave the property for periods of more than a week

- Clear guttering yearly

- Unplug your television, oven and other appliances to protect them from power surges

- Respond immediately to any concerns that tenants or visitors may have about the property’s condition

- Visit the property at least every 6 months to check for any signs of damage or run down structures, and repair if applicable

Be sure to practice these tips throughout the 2014 insurance period so that you can look forward to your next break.

Choosing the right tenant for your property

Choosing who you have living in your property can be one of the most stressful parts of being a landlord. Your property may have lot of your own time, effort, and finance in to getting your property just right, and having a “bad tenant” can put this all at risk.

Having insured against deliberate or malicious damage by tenants, we have seen our fair share of claims. From tenants have been just a bit reckless with the property, to the extreme of taking a golf club to the walls.

While having insurance will help get your property back to where it should be, it’s better to avoid the headache altogether by getting the right tenants in place. To help with this, we have prepared 3 tips for selecting the right tenant:

1. Beware of negotiators

Some negotiation can be expected on items such as dates, rent, or lawns. When the tenant is trying to negotiate down a bond, it can raise questions as to their financial position and cash reserves. Similarly, if they start haggling on the credit check or overdue payments, this may be a sign of trouble to come.

2. Rental property is a business

It can be tempting to rent your property to a friend or relative. You know the tenant, and don’t have to hassle with time consuming background checks or other formalities. However if something goes does wrong, you may find yourself in the tough spot of having to take a dear friend or relative to the tenancy tribunal or losing out on income.

3. Watching for the signs

When it comes down to choosing whether or not to select a tenant, there may be some red flags (frequent movers, no professional references, urgency to secure the tenancy) which could be explained. Others – such as wanting to pay in cash, or providing incorrect information/fake references – are a clear sign that this is not the best tenant for the property. Being familiar with the red flags will help you make the best decisions in who you let your properties to.

These points are a general view from claims that Initio has seen over the years. If you have specific queries about a tenant or application, or for further advice on tenants and property management, your local Property Investors Association is a great starting point.

AA Financial Strength Rating

We know that the most important thing for our customers is knowing that we have the financial strength to be able to pay their claims.

In accordance with the Insurance (Prudential Supervision) Act 2010, we provide you with updated information on our financial strength.

Initio Limited policies are underwritten by IAG New Zealand Limited (IAG). IAG has received a financial strength rating of AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency.

A rating of AA means IAG has a ‘very strong’ claims-paying ability.

The rating scale for S&P Global Ratings is:

| AAA |

(Extremely Strong) |

| AA |

(Very Strong) |

| A |

(Strong) |

| BBB |

(Good) |

| BB |

(Marginal) |

| B |

(Poor) |

| CCC |

(Weak) |

| CC |

(Very Weak) |

| C |

(Extremely Weak) |

| D |

(Default) |

| R |

(Regulatory Supervision) |

| NR |

(Not Rated) |

Note:

The Ratings from “AA” to “CCC” may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major ratings categories.

The rating scale above is in summary form. A full description of this rating scale can be obtained from www.standardandpoors.com.

In its Annual Solvency Return filed with the Reserve Bank of New Zealand, IAG New Zealand Limited had a Solvency Margin as at 30 June 2023 as follows:

| |

$m |

| Actual Solvency Capital |

782.1 |

| Minimum Solvency Capital |

501.8 |

| Solvency Margin |

280.4 |

| Solvency Ratio |

155.8% |

Accident loss claim – November 2017

Background

Simon took out a landlord’s insurance policy with Initio for his property in Palmerston North in September. Not having used Initio before and only having one policy, he was like many clients and a bit unsure how his policy would respond if he had a claim. Two months after his policy inception date he got his chance to find out. Simon received a call from his tenant advising his daughter when going into the shower had slipped and crashed through the shower door.

Claim Process

Simon phoned a repairer straight away and organised them to come out and provide a quotation for a replacement door. He took some photos of the damage and called initio. Initio advised Simon to lodge his claim online and send through copies of the photos and quotation he had obtained from the repairer. Simon’s policy protects him again sudden and accidental loss to his property. The damage to the shower door was consistent with a sudden and accidental loss and he knew the exact time of loss the damage happened.

Outcome

It really doesn’t get more straightforward then this. Simon provided all the information required when lodging his claim. From the photos he supplied his insurer were able to assess the damage. After his policy excess was deducted a payment was made into Simon’s nominated bank account for repairs and replacement of the shower door. This claim was lodged and settled within 24 hours for just under $1,000.

All claims are different, and they are assessed on their own merits and facts. The above profiles do not imply a guaranteed approached all such claims

Until the government changes the standard, contamination over the current 1.5mg/100cm2 limit will trigger a landlord insurance claim.

It is concerning that the Real Estate Agents Authority moved so quickly to only declaring limits over 15mg/100cm2. Continue to do your due diligence when purchasing property as contaminated homes (over 1.5mg/100cm) are untenantable and uninsurable.

Status quo remains at Tenancy Tribunal post-Gluckman report

The Tenancy Tribunal has published its first orders on methamphetamine since the Gluckman report sent shockwaves through New Zealand last month.

The orders have been eagerly anticipated after the Prime Minister’s former Chief Science Advisor published a report last month saying that there was no evidence third-hand exposure to methamphetamine caused adverse health effects.

As a result, Housing New Zealand and the Real Estate Agents Authority quickly established new contamination levels of 15 micrograms/100cm2 for their businesses.

But it appears the status quo will remain at the Tenancy Tribunal until the Government establishes new ‘official’ standards in this contentious area.

All six orders published since the Gluckman report was released on May 29 follow Standards New Zealand’s NZS 8510:2017, which has a contamination level of 1.5mg/100cm2.

Only one Tenancy Tribunal order, application number 4128761, referenced the Gluckman report.

“There is currently some debate about the health impact of methamphetamine however I agree that the use of premises for an unlawful purpose is something to be discouraged,” the adjudicator wrote.

So it appears it’s business as usual for landlords and property managers until any legislative changes are made in this space.

For more information, read the full tenancy.co.nz article here.

There needs to be an inspection done every three months and in between tenancies to meet our landlord obligations under our landlord insurance policy. This can be done yourself or by the person who manages your tenancy (e.g. property manager). The inspection will need to confirm the interior and exterior condition of the property and you need to keep a record of the results.

These landlord obligations and inspections only need to be met if you are making a tenancy-related claim. These include tenant damage, meth contamination and loss of rent after a tenant is evicted or leaves.

If you don’t fully complete your inspections it won’t void your policy. The cover for non-tenancy claims like floods and sudden water damage are still covered.

Full Landlord Obligations

Can I complete inspections remotely?

At initio, we require an agent or a trusted representative physically present at the property for inspections. This ensures a thorough evaluation of the property’s condition and facilitates real-time reporting, serving as your on-the-ground resource. Advantages of having an in-person representative include:

- Real-time condition verification and data reporting during the inspection process.

- Being your dedicated eyes and ears on the ground, diligently checking the property’s condition.

- Early identification of any potential issues, damages, or repairs that could potentially be missed in a purely remote inspection.

However, we understand there may be special circumstances such as illness or lockdowns where remote inspections become necessary. These should be exceptions rather than the norm. In such cases, a trusted representative or official agent’s physical presence during the inspection is critical to maintain the assessment’s accuracy and comprehensiveness.

Looking ahead, we’re mindful of emerging technologies that could potentially streamline remote inspections. However, as of now, the value of in-person inspections is paramount. Always remember that our advice serves as a guideline, not an inflexible rule. Each property and situation may require a different approach, and decisions should be tailored to your specific circumstances and needs.

What happens if I can’t inspect my property every three months due to illness?

Initio’s landlord guidance is that you, or someone on your behalf, should carry out an internal and external inspection at least every three months, and also between tenancies. These inspections are an important part of meeting landlord obligations for tenancy-related claims, such as tenant damage, meth contamination, or loss of rent after eviction.

That said, if inspections aren’t completed exactly on time, your policy is not automatically void. Claims that aren’t tenancy-related (like fire, flood, or sudden water damage) remain covered.

For tenancy-related claims, inspections generally need to be done in person by you, a property manager, or another trusted representative. We do recognise that there may be special circumstances, like illness, where remote inspections are the only option. These should be the exception rather than the norm, and having someone physically present is always preferred to keep records accurate.

If you’re in a situation where inspections are difficult, please reach out to our team. We’ll be happy to talk through your options and help make sure you’re covered.

Further information

Please refer to the New Zealand tenancy services site for specific information around property inspections, including;

- your rights

- your tenant’s rights

- a sample inspection form

Get a quote

Related articles

Want to pay monthly but prefer not to use a Credit Card? Our card option also works with Visa Debit Cards

Most standard accounts with New Zealand banks offer the option to link a Visa debit card to an ordinary bank account. Debit cards work like credit cards but use the money in your connected bank account, avoiding interest fees. They can be used for:

- Contactless payments in-store

- Online shopping

- Overseas purchases and ATM withdrawals

You can control your debit card options, such as enabling or disabling contactless payments. Debit cards are useful for paying policy premiums with Initio, either monthly or annually. Each bank has its own criteria, fees, and application processes.

Contact your bank for further information on how to set up a Visa debit card should you wish to use this option.

This information provides general guidance. For the latest details on fees and conditions, please check each bank’s website.

Useful links

How can I pay my premium?

How does monthly insurance work?

Switching payment frequency

Can I pay with direct debit?