Search results for: {search_term_string}/get-quote

As a landlord, the risks to which you are exposed are often not covered by a standard insurance policy. When taking this next step on the property ladder it is important to have the right Landlord Insurance cover in place to save yourself from headaches down the track.

Does your policy cover your tenanted house? While it seems obvious, a standard house insurance policy is designed to cover owner occupied homes, if you were to make a claim and the insurer discovered the house was tenanted your claim could be declined. If you have listed your holiday home for rent or if you have recently moved out of your own home and tenants have moved in, make sure you have notified your insurance provider, and they have the correct Landlord Insurance cover in place.

Does your policy cover loss of rents? Following a claim for property damage to your house, there will likely be a period where it is uninhabitable while you wait for the repairs to be carried out and completed. You are going to want your Landlord Insurance to pay for your lost rental income during this time. Make sure that the policy will pay out for at least 12 months, and that the limit is large enough to cover the week rent – ie $20,000 over 12 months is up to $385 per week.

Does your policy include cover the carpets? House insurance policies often only cover floor coverings that are glued to the floor, while most carpet is tacked. Therefore, it is important that your Landlord Insurance policy includes cover for your contents. Make sure this amount is enough (we recommend at least $20,000) to cover your appliances, carpets, drapes, blinds and other furniture that remains in the house while it is tenanted.

Does your policy include damage caused by your tenants? Generally, your insurance policy will exclude deliberate damage caused by a person living at the house, so if your tenants intentionally damage your house you may not be covered. A good Landlord Insurance policy will include cover for malicious or deliberate damage by tenants.

Does your policy continue if your house is vacant? Some policies will cease cover if the house is vacant. So, if it takes longer than expected to tenant your house, or if you have no bookings at your holiday home over the winter, you might not have any insurance cover. Look for a Landlord Insurance policy that will continue to provide cover even while the house is unoccupied.

If your tenants are holding the keys to your retirement savings, you don’t want to leave anything to chance. The initio policy was designed specifically for rental houses and holiday homes, so you can rest easy knowing that one of your largest assets is in safe hands. To get a quote visit initio.co.nz.

In a boarding house, each tenant rents a room rather than the whole house. They then share facilities such as the kitchen with the other tenants, and in many cases each tenant has their own bathroom.

We can insure boarding house’s with five or less rooms (tenants). If your boarding house has five or less rooms you can get a insurance quote here.

If there are more than six rooms we consider this to be a commercial building risk and we are unable to provide cover.

Initio, the first insuretech company in New Zealand to provide instant online house insurance, announces that it has given even more control to customers by launching another NZ first, Live Policy.

Live Policy means that customers can instantly modify or add to their insurance in an on-demand fashion without having to nervously wait for a confirmation.

The traditional process of getting and modifying insurance remains clunky and broken. When it launched in 2010 initio was transformative in giving homeowners and landlords the ability to effortlessly quote and purchase house insurance online and in real time through its website www.initio.co.nz. A process that takes less than five minutes without the need for paper applications or long winded phone calls.

Initio has today taken their market leading approach a step further. Through a personalised dashboard, Initio customers can now fully manage and modify their insurance policy instantly and whenever they want. This luxury does not exist with other insurers, who require the customer to make direct contact by phone or email to request the cover change.

Initio’s Live Policy means that the customer is in charge. Anytime, day or night, the customer can modify their insurance cover in a multitude of ways. This includes being able to increase or decrease the replacement value or excess of their own home, holiday home or rental property. Crucially, Live Policy also means that the customer can add to their cover an engagement ring they purchased on the weekend. Waiting till business hours on Monday to get insurance cover is now a thing of the past.

“It’s about giving the customer total control over their insurance and it’s about getting away from having to wait in-line at a call centre. We felt that being able to modify your insurance when you wanted adds significant value to a more transparent and responsive insurance experience – so we built Live Policy.” says initio CEO and co-founder, Rene Swindley.

Since its inception initio has always used technology to push the boundaries of insurance for the benefit of the end user. “Insurance doesn’t need to be complicated” says initio CTO and co-founder Sam Brook. “Our overriding mission is to make insurance more approachable for homeowners and landlords, Live Policy is a significant digital milestone for both initio and insurance in New Zealand”.

Put simply, monthly insurance means your insurance is renewed and paid for each month. Its a month to month policy rather than an annual policy paid monthly.

What does this mean?

Rather than pay an entire years worth of insurance up front in one go, you can enjoy smaller monthly insurance charges.

Monthly insurance with initio is just like a monthly gym subscription, providing you with the flexibility to unsubscribe whenever you choose.

What is the difference between annual and monthly insurance?

Monthly insurance is a month-to-month policy, so once you commence the cover online we automatically renew your policy and facilitate payment on a monthly basis. The cover will only stop if you go online and stop your cover, which is simple to do via your online dashboard.

Annual insurance means your policy is entered into upfront for a full 12 month period. Payment also occurs upfront and is then manually renewed and paid for by you each year. The cover will cease if you don’t renew it.

You can look at monthly insurance the same way you look at a floating mortgage, with an annual insurance policy similar to a fixed mortgage. With annual, because you have paid up-front you have locked that premium and cover in for the year. With monthly you have locked the premium and cover in for the month and if premiums or levies change, so does your monthly charge. This doesn’t happen very often, but if it does we will always let you know in advance by letting you know what your next month’s charge will be.

When does my credit/debit card get charged?

Your credit / debit card will be charged on the day you transact with initio (even if you choose a date in the future to start the cover). Then each month initio will charge your card on the same day of the month that your policy renews (ie the original commencement date).

What if premiums or levies change?

Premiums can go up or down depending on the local New Zealand insurance environment. Events such as storms, earthquakes, flooding to name a few major events (or lack thereof) can have an impact on insurance premiums. Also, the government makes changes to the levies they charge every now and again (Fire Service Levy, and Earthquake Commission Levy) which can impact on the cost of premiums. On the average initio insurance policy these government levies make up almost half of the premium.

So… that said, if premiums or levies change, then that change is effective from date after the your next policy period. For example if the fire service levies increase from 1 November 2019 then all monthly and annual policies renewing after this date will be charged at the new levy.

If you have a monthly policy we will always give you notice of any change.

How do I pay?

By Credit or Debit Card.

When you start your policy you will make the first month’s insurance payment with your Visa or Mastercard credit/debit card. Each month (on the same day you told us to start the policy), we will automatically renew and charge that same card each month (you can update your card online via your initio dashboard).

We will email you each month letting you know that your policy has been renewed and we will confirm the charge to your credit card.

We will also always let you know what next months charge will be.

You can stop the insurance payments by cancelling the insurance through your initio dashboard.

How does it work?

When you get an initio quote for your property you will be provided with both policy period options, yearly or monthly.

Example: on 20th of February Barney chooses to start his monthly cover from 1 March. $92 per month.

- Barney enters his credit card number (Visa or Mastercard).

- On that day, 20 Feb, his card is charged $92 for the insurance period 1 March to 1 April.

- Barney instantly receives confirmation of the insurance online and by email.

- On the 1st of April Barney’s policy automatically renews and initio charges Barney’s credit card $92 for the insurance period 1 April to 1 May.

- Barney receives a confirmation email from initio.

- The monthly process continues until Barney chooses to stop the insurance cover.

Just like our insurance signup process and our claims, we’ve kept it simple

What does it cost?

You’ll pay a bit more over an annual period if you are on a monthly policy, and that’s because its riskier for an insurer to provide a monthly policy compared to an annual one. Premiums are based on risk.

Is it secure?

Yes. We use well known secure payment provider, Stripe, to manage our monthly payments. Stripe operates in 120 countries world wide and uses the most stringent level of payment security certification available in the payments industry.

The requirement for 3 monthly property inspections forms part of most landlord insurance policies.

A rental property that is inspected regularly is less likely to be ill treated by its tenants, and if the property does suffer some damage it is easier to establish what and when it happened.

There is widespread debate among landlords, tenants, property managers and insurers as to whether 3 monthly inspections are too frequent and disruptive to tenants.

What is not well understood by landlords is that superior landlord insurance policies (like initio) provide insurance irrespective of whether property inspections are being completed or not.

So, here’s three things you need to know:

1. You are still insured if you don’t do property inspections

From an insurer’s perspective the landlord obligations are NOT a requirement to make ANY claim acceptable. At claim time, property inspection information will only requested when the claim is for a tenant related loss such as meth or malicious damage.

So if you are making a claim for intentional damage caused by the tenant or meth contamination – your insurer may ask to see copies of your property inspections. However, if your claim is for damage not related to the tenancy such as a burst water pipe, a storm blowing the roof off, an earthquake, or total loss house fire (to name just a few) the insurer will not be interested in your property inspections as they are not relevant.

2. 6 monthly inspections used to be the norm, until …. Meth.

It is only recently that insurers have moved to 3 monthly inspections. This is a direct consequence of the rising cost of methamphetamine contamination claims.

To put this in perspective, at its height Initio was receiving a new meth claim per day, and that cost a lot of money. We noticed that a large number of meth claims could have been avoided or at least mitigated by better risk management, namely more regular property inspections. So instead of pushing prices up further to offset this risk (or excluding meth cover all together) we decided that if landlords wanted ongoing meth cover they would need to take an active role in managing the risk through, among other things, property inspections.

Good insurers (like initio) will not use the landlord obligations as a way to avoid claims, but as a way to fast track claims for landlords with good risk management.

3. New Zealand Property Investors Federation members – 4 monthly inspections periods.

We are proud to be the insurance partner to the New Zealand Property Investors Federation (NZPIF). The NZPIF take an active role in professionalising property investing in New Zealand with knowledge, leadership and resources for members.

Our data shows that property investor members have approximately 50% lower incidence of meth and malicious damage claims, compared to non members.

Members of the NZPIF who insure with Initio receive the benefit of 4 monthly inspection periods. Visit NZPIF to find out more about organisation, including how to become a member of a local property investors association. Associate membership starts from just $25 per year.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

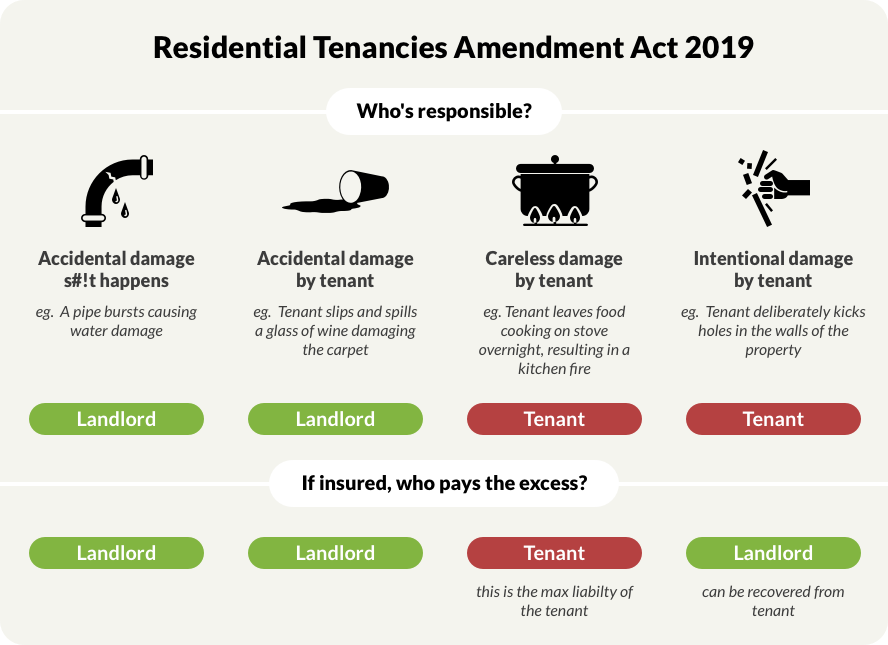

On 30th of July 2019 changes to the legislation around tenant damage and meth contamination were passed into law.

The Residential Tenancies Amendment Act 2019 will:

- limit tenants’ liability for careless damage in rental properties to the landlord’s insurance policy excess or 4 weeks rent (whichever is less)

- re-open the ability for the landlord to recover against the tenant for damage, albeit on a very limited basis

- allow tenants to share in and receive protection from the landlord’s insurance policy

- mean that landlords must provide confirmation of insurance cover to all new tenancies and their exisiting tenants on request

- prevent insurers from pursuing tenants for unintentional damage (ie careless or accidental damage)

- allow for regulations to be made to address how contamination (eg. meth) of rental properties is tested and managed

- give the Tenancy Tribunal full jurisdiction over cases concerning premises that are unlawful for residential purposes, such as garages and sleep-outs, which don’t meet minimum requirements for renting

- protect tenants living in those unlawful premises, as the Residential Tenancies Act will now apply

- give Tenancy Services the ability to take enforcement action against landlords who rent properties which don’t meet minimum standards

These changes are scheduled to take effect on 27 August 2019. The provisions of this new Act only apply to damage occurring after this date.

So, I’m a landlord, how do these changes affect me and my insurance?

It depends on how the damage has been caused. There are four ways a rental property can suffer damage:

Accidental Damage – S#!t Happens eg. storm damage

Accidental damage is damage that can’t be avoided, because sometimes s#!t happens. This could be caused by an ‘act of god’ type loss such as a storm causing damage to the roof of the property. Or it could be a leaking water pipe or an electrical fire. This type of damage is completely outside of the control of the tenant liability, and as such they have no liability for this damage. The landlord is responsible for this damage, and will usually have insurance to pay the claim.

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Accidental Damage by Tenant eg. spilling a glass of red wine on the carpet

Accidental damage can also be caused by a third party, such as a tenant. This could come in the form of a tenant tripping and spilling wine on the carpet, or their washing machine flooding. In both cases these are technically outside of the control of the tenant and there is no liability on the part of the tenant. So even if the tenant causes the accidental damage, the tenant has NO liability. The tenant can rely on the landlord’s insurance policy the repair the damage, and the tenant cannot be made to pay the insurance excess (or 4 weeks rent).

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Careless Damage by Tenant – eg. leaving a pot cooking on the stove and going to bed

Where a tenant (or their guest) carelessly causes property damage to the home, they are liable for those damages. This could be where the tenant leaves a pot cooking after going to bed and causes fire damage to the kitchen. While the amendment to the act now makes the tenant liable, the maximum amount the tenant can be held responsible for is the landlord insurance policy excess, or 4 weeks rent (whichever is lesser). The new Act effectively allows the tenant to share in and receive the benefit of the insurance arranged by the landlord.

- Who is responsible for the cost of the damage? answer: the tenant (but its capped at the lessor of the landlords insurance excess or 4 weeks rents)

- Who pays the insurance excess? answer: the tenant (see pain points below)

Intentional damage by Tenant – eg. smashing holes in the wall

A tenant is not excused from liability when the damage is intentional or where the damage they (or their guest) have caused constitutes an imprisonable offence. In such circumstances the responsibility is on the tenant to notify the landlord of the damage. The landlord can request that the tenant repair the damage, but if the landlord is properly insured (ie has an initio landlord insurance policy) they will be covered for intentional damage so its best to lodge a claim for the damage, and allow the insurer to pursue the tenant for the cost of repairs.

- Who is responsible for the cost of the damage? answer: the tenant

- Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the incurred to repair the damage)

What about Methamphetamine Contamination?

The Act allows landlords the right to enter the rental property (after providing notice to the tenant) to sample and test for meth contamination. If testing confirms that the property is contaminated to unsafe levels (currently higher than 1.5 μg per100 cm2) then the landlord, and the tenant, have rights to terminate the tenancy. The landlord can terminate with a minimum notice period of 7 days, whereas the tenant can terminate with only 2 days notice.

Meth testing must be done in accordance with the Standards New Zealand standard, and the landlord must notify the tenant within 7 days of receiving the test results.

If a landlord knowingly rents a property with meth contamination, the tenant can be awarded damages of up to $4,000.

We are still awaiting further details around this and exactly what standard will be set by the Housing Minister. Currently the NZ Standard, which the insurance industry follows says that a property is contaminated if the presence of meth exceeds 1.5 μg/100 cm2, however the Gluckman Report, which the tenancy tribunal follows says that a property is contaminated if it is more than 15 μg/100 cm2. We are expecting that the amendment to the Residential Tenancies Act will provide some consistency and that we will all move to 15 μg/100 cm2 as being the level where contamination occurs.

Given that the possession of meth can attract a penalty of up to 6 months imprisonment, and manufacture of meth a maximum penalty of life imprisonment, if use/possession or manufacture is proven at the property the tenant is NOT excused from liability and has NO protection from the landlords insurance policy. The landlord or their insurer can recover the cost of cleanup and repair from the tenant.

Who is responsible for the cost of the damage? answer: the tenant

Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the insurer incurs to remediate the property)

Important: The likelihood of recovering costs from a tenant for meth damage is extremely low. Firstly proving it was the tenant is difficult, and secondly meth addicts generally don’t have the financial resources to pay for such large repairs.

Where are the pain points with these changes?

Accidental vs Careless

As accidental damage means that the landlord pays the excess, and careless damage means that the tenants pays the excess, we expect to see disagreements between landlords and tenants about the cause of the damage. If the landlord and tenant cannot agree whether the tenant is liable for the damage, the landlord can apply to the Tenancy Tribunal for the matter to be resolved. Copies of relevant insurance policies, photos of the damage, and receipts or quotes for repair should be included to support the application.

Is meth contamination careless or intentional?

We believe it is intentional but fortunately the new Act catches meth under the category of imprisonable offence. We anticipate that tenants (and maybe the courts) will continue to argue that the resulting damage from smoking meth is careless not intentional. Our opinion is that there is now enough information in the public domain for people to understand that meth causes property damage.

A tenant has carelessly damaged my property, I’ll leave the tenant to pay the excess to the insurer/repairer?

If you establish that the tenant has been careless this won’t mean that its a slam dunk on the tenant physically paying the excess.

We foresee there will be arguments over who physically pays the excess to the insurer or the repairer. Is it the insurer or is it landlord? Given that the policy owner is the landlord this suggests that the landlord would need to pay the excess and then recover it from their tenant. This may change in time as the new Act is tested with real loss scenarios.

We recommend that as soon as the landlord becomes aware of, and can establish that “careless damage” has occurred, that they hold their tenant responsible for the excess and request immediate payment.

What do I need to do?

You will need to provide a confirmation of insurance certificate to your tenant

Landlords are now required to provide all new tenants, and existing tenants where they request it, details of their property insurance. Any changes made to your insurance, also need to be notified to your tenants. Failure to do so could result in a $500 fine to be paid to the tenants. You can provide the tenant with a standard certificate of insurance but this will have more information on it than you are required to disclose (such as the Bank that has a mortgage over your property). Some insurers like initio have produced a specific Tenant Certificate. To obtain a Tenant Certificate of insurance to provide to your tenant or property manager you can get this through your initio dashboard.

Seeing the tenant is paying should I increase my excess?

Probably not – as the tenant only responsible for paying the excess some of the time.

A number of landlords have mis-interpreted that the tenant will pay the excess on all types of claims, and have moved to increase their insurance excess to align with approximately 4 weeks rent.

Remember that if you increase your excess, the higher excess will apply to ALL claims, not just the ones that the tenant is responsible for. The measure of tenant responsibility is carelessness so as a landlord you need to be able to establish that your tenant was careless in order to recover your excess from the tenant.

How do I increase my excess?

With initio you can easily do this by logging in to your dashboard and modifying your policy excess, and the credit premium adjustment will be refunded to you.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

When you think about claims, people generally jump to their own worst fear of their property burning to the ground, and that’s exactly why we all buy insurance. Big marketing hypes insurance products as providing ‘peace of mind’, but what you’re literally purchasing is compensation in the event you submit a claim – and a reasonable expectation that any such claim will be processed and paid to you. What do you need to know about claims when it comes to your property insurance?

Don’t sweat the small stuff

Claims are there for the major events – think fire, earthquake, storm damage – but also the slightly smaller but still very costly incidents such as a leaking pipe that damages flooring that your tenant didn’t notice. Insurance isn’t there for the day-to-day maintenance of a property, so don’t use your policy for repairs, ware and tear, and upkeep, as your insurer may deny those types of claims.

What about damage and the new legislation amendments?

The recent amendments to the Residential Tenancies Act provide that a tenant is liable to pay their landlord’s insurance excess or four weeks’ rent – whichever is lesser – but only for careless or intentional damage. Accidental damage, such as spilling a glass of red wine onto fluffy white carpet, may still be the responsibility of the landlord; further Government guidance and future Tenancy Tribunal decisions will provide more certainty on this.

A snapshot of Initio’s last 12 months of rental property claims shows that unexpected events such as house fires and storms take the lion’s share of the number and value of claims:

|

|

|

| Type of claim |

Number of claims |

Cost of claims |

| Accidental loss (e.g. storm damage, fire, burst pipe) |

55% |

70% |

| Accidental damage caused by tenants |

14% |

5% |

| Careless damage caused by tenants |

7% |

1% |

| Intentional damage caused by tenants (including meth) |

16% |

23% |

| Other/third party claims |

8% |

1% |

What types of claims are the most common?

As the insurance provider to over $2.5 billion of Kiwi property, Initio has its fair share of claims – so based on our experience, we can give you an insider’s view on what to look out for. In the last 12 months to end of August 2019, our 4 most common claims in order:

#1 Sudden water leak (eg burst pipe) – average claim value $5,916

#2 Tennant damage (eg malicious damage) – average claim value $2,960

#3 Weather damage (eg storm, flood) – average claim value $5,732

#4 Hidden gradual water damage (eg slow dripping pipe) – average claim value $1,980

The best insurance of all is the proactive management of the risks faced by the property. For example actively keeping an eye on areas where hidden leaks are most likely to occur (under the kitchen sink and in the bathroom) will reduce the likelihood of damage. But should you get hit with a nasty loss – well, that’s exactly what insurance is for.

Take action

Many customers seem to think that they must leave their water sodden carpet festering away until the insurance assessor turns up or their insurer says it can be taken out. This is definitely not the case. My advice is to act and to start the clean-up process; take photos and get on with things. It is important to note that most insurers want you to take steps to reduce any further loss, and taken action aligns with this. The exception here is fire damage, following a fire you will want to take steps to secure the property (eg. boarding up entry doors) but you should leave the property as is so that fire investigators have the best chance of determining the origin of the fire.

Know the process

The process around submitting and receiving payment for claims can be frustrating if you don’t know how long you’ll be kept waiting, and what is required of you as a claimant. So, when choosing an insurer it’s good to take the time to understand this upfront – so if and when you suffer a loss, you know what to expect and can have confidence in the process.

Get a quick quote online, insure online, lodge and see the progress of your claim online Initio.

Learn more about landlord insurance

Learn more about house insurance

Learn more about how claims work at initio

Having started a company that challenged the way things have always been done in insurance, our director, Rene Swindley, who is the recipient of the 2018 Young Insurance Professional of the Year, was asked to speak to the 2019 Insurance Council of New Zealand Conference on how insurers need to change to meet the expectations of tomorrows insurance buyer. Here is the abridged transcript of his presentation.

Young insurance professional view

I turn 35 this month so I’m no spring chicken… but I’m arguably still very young by industry standards (something I would love to see change).

After finishing Law school, at 23 years of age, I co-founded a company called Frank… so I suppose you could say that I’ve taken an immature approach to insurance over the last decade. Back then I had a lot more hair, a lot less stress, and couldn’t understand why insurance was so clunky.

The early days (2009) – Tristram Street, Hamilton

It was this Naïve approach to insurance that has allowed us to challenge the way “things have always been done”.

By way of background Frank Risk. Is our Commercial Insurance Broking brand – it rebates commissions to clients and charges a disclosed fee for service, and this approach removes the conflict of interest most other brokers face. From its inception 10 years ago Frank has challenged the market to do insurance the way we do.

Frank Risk (Nov, 2018) – Celebrating 10 years in business

Frankie is the digital version of Frank – we built this in-house to be a client-facing tech lead platform for business insurance.

Initio is our domestic brand – it’s a digital provider of domestic insurance (houses, contents). The platform, which we built from scratch, is a full on-demand, customer-facing quote, bind, manage, claim online. It’s customer-centric and it’s faster, easier, smarter. It was the first of its kind in 2011, and back then insurers were in denial about tech lead custom driven insurance….. These days they call it “Insuretech”.

So with that background on how we’ve been trying to effect change for the benefit of the customer – here’s my opinion on how we (the industry) needs to change for the next generation of insurance buyers:

Initio (2019)

How insurers need to change

Insurers need to provide value

Tomorrow’s customer is buying on value – not price or $50 pressie cards. They want an insurer that provides flexibility, provides assistance with managing risk, and communicates with them in plain English.

So let’s cut the jargon, let’s give the customer control, let’s help the customer reduce risk.

We are starting to see examples of insurers and tech companies providing tools for managing the things people own. Trov in the US pioneered single-item, micro duration insurance. The founder, Scott Walchek asked ‘What would happen if you could give individuals control over the information about their things’. What happens is the customer sees value in the relationship with their insurer as it departs from a pure transactional relationship.

Value for the business customer is by way of tools that help to identify their commercial risks in real-time – I’m talking about connected devices that tell a line manager that a steel saw is becoming blunt and causing heat. Insurance becomes secondary.

The provision of value like this is just the beginning. The buyer of tomorrow won’t be thinking of insurance as a primary service – it will be secondary to the provision of other core business tools and personal management strategies.

Make insurance accessible

Insurance lags way, way behind millennial’s expectations of obtaining intangible services.

For a product that does not need to sit on a shelf, has no physical logistics associated with it, and for many risk lines, has no short supply issues – insurance is nowhere near as accessible as it should be.

We need to change to adapt to the buying and living patterns of the next generation, which means on-demand insurance cover that’s also available at point of sale, and aligns intricately with how the customer works, lives, eats, plays. What I’m proposing is a policy of the future that wraps around the customer not what they own. Just imagine an insurance world with fewer policies and less fragmentation.

One of the reasons insurance is not as accessible is it should be is because of the human factor. Let’s get smarter about this and use computing power not humans to do the soul-destroying processing work for no complex risks. I challenge you to work out how many humans need to be involved in a single material damage placement. I’m guessing its 6+.

Increase the trust

Insurers don’t trust their customers, and customers don’t trust their insurers. By any relationship standard – that’s a pretty bad one.

The next generation of insurance buyer wants to trust their insurer and they want to be trusted.

Let’s compare it to the taxation system in New Zealand. It trusts the end-user implicitly. For example – with a GST return, if you claim a cash refund [by disclosing that your GST collected on sales income is less than the GST paid on expenses] you receive the refund to your bank account – no questions asked. But god help you if you are dishonest. It’s a trust everyone until proven otherwise approach – and it works.

That used to be the way insurance worked (absolute good faith – uberiemae fidea) but it seems to have evolved into a “prove your loss” approach including proofs of purchase, photographs, assessors, investigators – all at great cost.

I totally accept that insurance fraud is a real issue – but there are smart ways to combat this. We are seeing examples of how technology and analytics are providing huge value gains here. Insurers are using anti-fraud algorithms to detect fraud and some US insurers are employing social scientists and psychologists to senior positions in their companies so that they can understand the mentality of their customers and build it into the technology.

So, in short, the industry’s current approach does not align with the expectation of what a millennial expects of their insurance experience.

As an industry, we can also increase trust by getting rid of the ‘black box’ stigma of insurance. We all know insurance but the customer doesn’t. We can start but introducing smart, searchable, plain English wordings. Wordings that are opensource that are a collaboration between the insurer and the buyer is my vision here. Tomorrow’s buyer doesn’t want a ‘gotcha’ moment. The next generation wants to contribute to how their policy is built – and for that insurers will get respect, earn trust, and have a customer for life.

Education also increases trust. Everyone believes that there’s a pot of money for earmarked for them. “I’ve been a customer for 20 years and I’ve never Claimed”.

I even had someone say to me the other day “I’ve just returned from overseas and all went well – no issues, do I still need to pay my travel insurance premium”

These comments seem odd to people who are in the insurance industry but I can’t emphasize enough that there is a widespread misunderstanding among customers of how insurance actually works. And this isn’t the fault of the customer – the insurance industry is the one who has dropped the ball here.

We need to teach customers that insurance is, in fact, a community-based pooling of resources administered by an organization [an insurer] who charges a margin for the privilege.

Know your customer – Know your data

Tomorrow’s insurance buyer expects that their insurance provider knows them and their stuff intricately.

The next generation expects this because they have willingly shared personal data with their insurer (and in many cases the public at large) already.

So to this end when they make a claim they don’t want to be asked how old they are or what their name is. Think about the current claims process… “Here you go customer – please repeat everything we already know about you on this manual form”. Not a great experience.

And when it comes to starting insurance, the things they own are data mapped and the next generation knows this. So let’s not ask the customer how many KM’s their vehicle has done or how susceptible their house is to flood.

Often the customer struggles with accuracy on these pieces of information and there is a fear that if they get them wrong they will invalidate their insurance. So, let’s NOT put that responsibility on the customer when we all have data we can access already. My point here is that its the insurer’s responsibility not the customers

I think as an industry we have been missing the real opportunity here. Data is where the real value is – and it’s a huge opportunity to impress our customers. Once you have data the sky is the limit, and insurers are the biggest data houses in the world.

You may have heard all the buzz words like AI, machine learning, and blockchain. But put simply we need to find patterns in the data and share this knowledge with the customer. Transparency breeds loyalty.

To recap the insurance buyer of tomorrow wants:

We can be smart with technology and achieve all of these things

I’m excited about the next few years for insurance. The insurance industry will continue to go through some dramatic change – there will be some winners and some losers but one thing is for sure, the customer will benefit immensely.

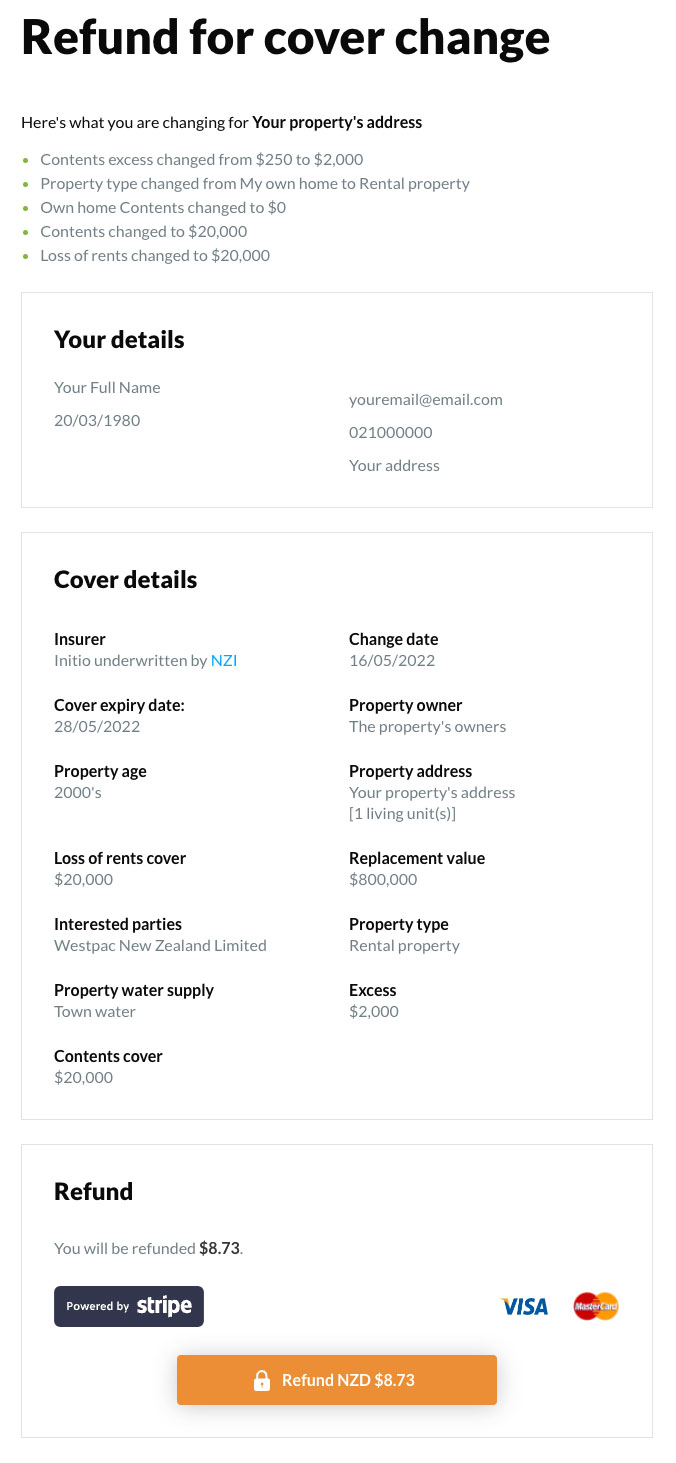

With the exception of correcting the Insured Name or Interested Party, please note you can only change a policy once it’s active (ie. once effective date is reached). If you’ve incorrectly set up other details for a policy in advance, you must cancel the policy and do a new one with the corrected details. We will give you a full refund for the original policy.

You cannot switch from a monthly policy to an annual one, but you can change from an annual to a monthly policy at renewal. Changing from monthly to an annual cover would require taking out a new annual policy and then cancelling the original monthly cover. For more details, check out our article on ‘Switching Payment Frequency‘.

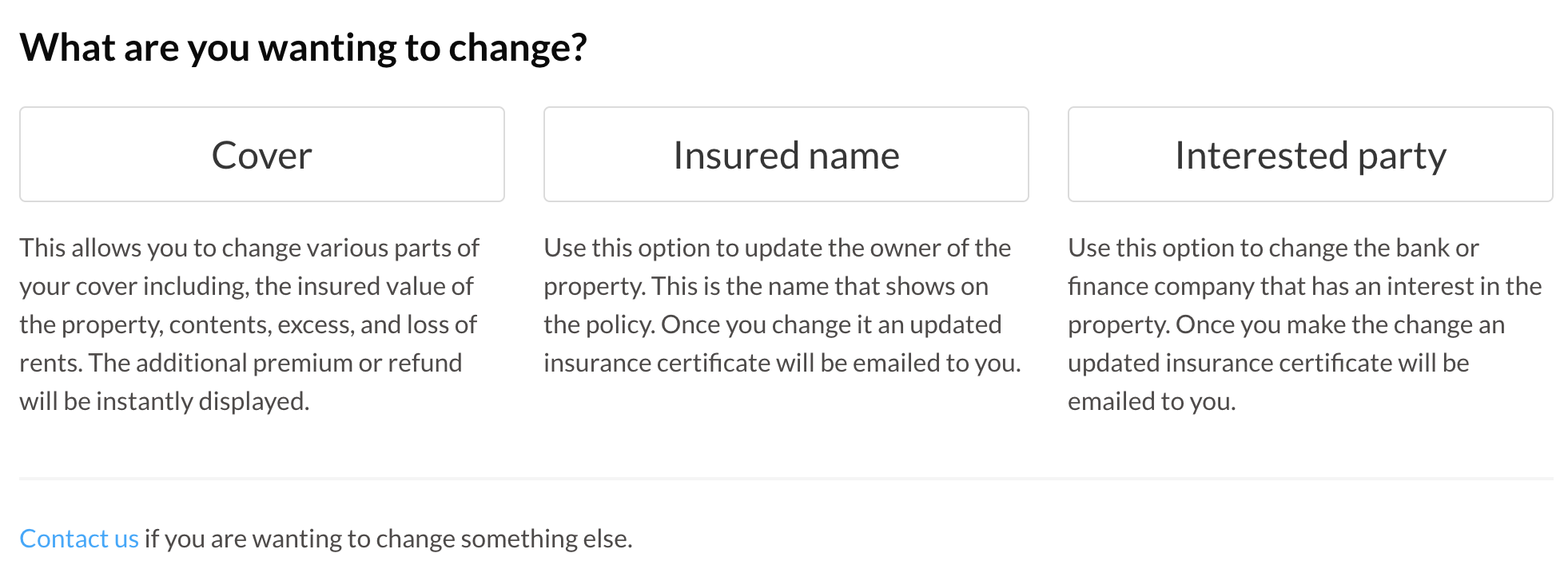

Where do I start?

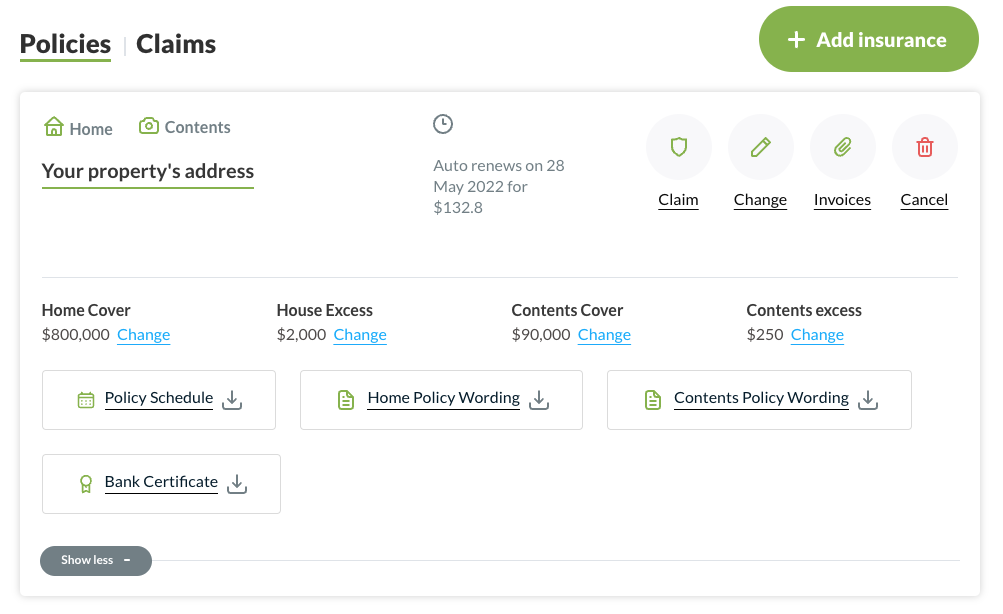

Changes are made to your policy online by logging in to your initio dashboard and selecting the “Change” button from the right-hand side action menu or one of the Quick Change buttons shown beneath the address by expanding the Cover Details option.

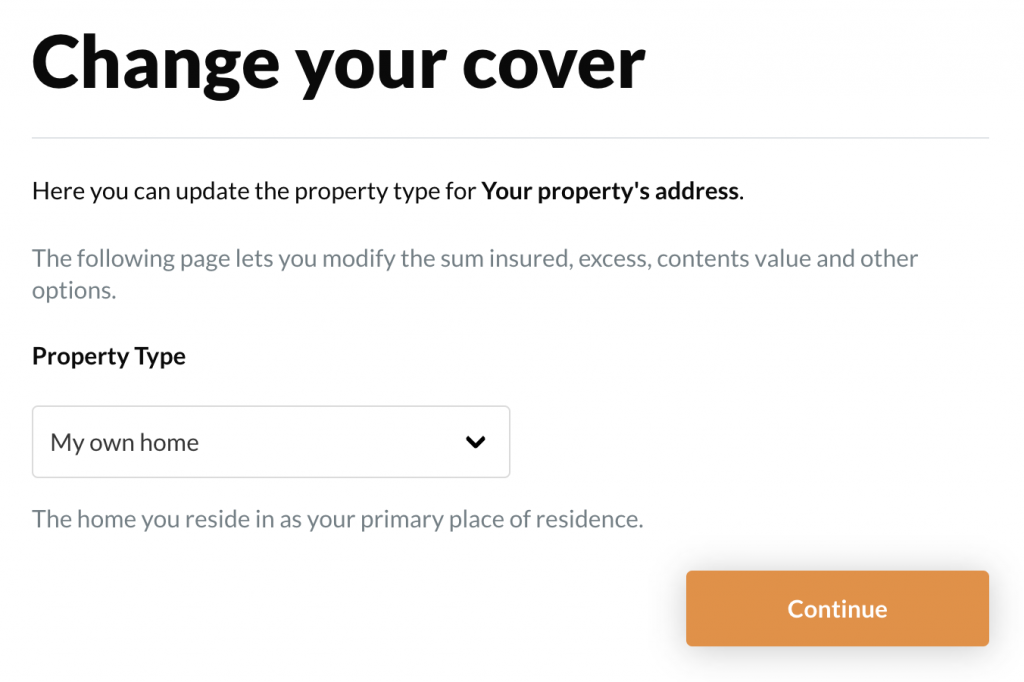

Changing cover?

Click on the “Cover” button to make changes to your policy and select the relevant option;

“Cover”

- Property Type, eg. From owner occupied to rental or holiday home, etc. For example, if you initially insure your home as owner occupied and partway through the year you decide to rent the home out, you can easily amend your cover to a landlord policy.

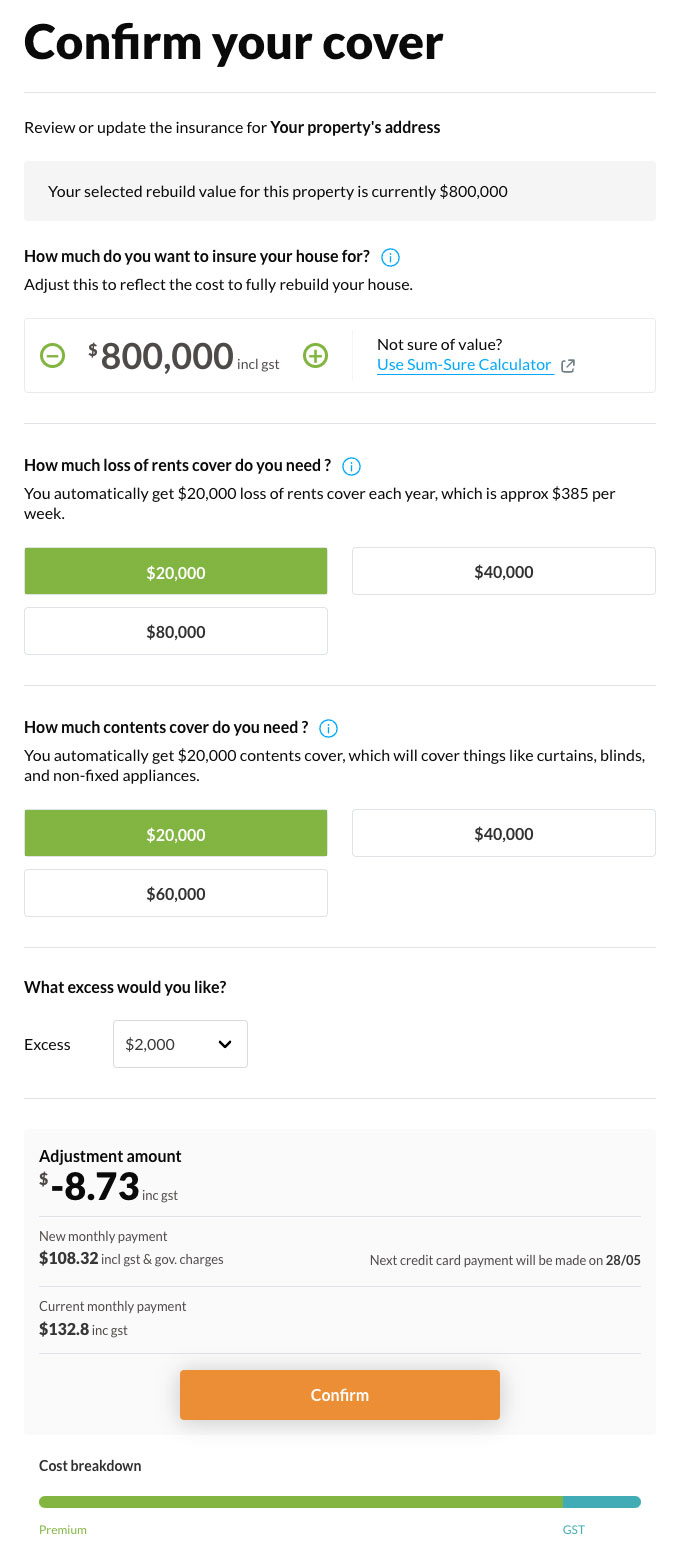

- Sum Insured

- Add or remove contents section

- Add or remove specified items

- Amend your current excess

- Adjust ‘Loss of Rents’ cover

Not living in your own home anymore and have turned it into a rental?

Simply click on the “Property Type” drop-down box and change it to ‘Rental Property’. If you need help deciding on which policy you need, please Contact us or refer to our support page here.

You can also use the Property Type change option to switch back to an Own Home (owner occupied), or change to our Holiday Home product (your own holiday home).

Need to increase your replacement value or adjust your excess? Add Contents?

Click continue from the Property Type page and here’s where you can make these types of changes.

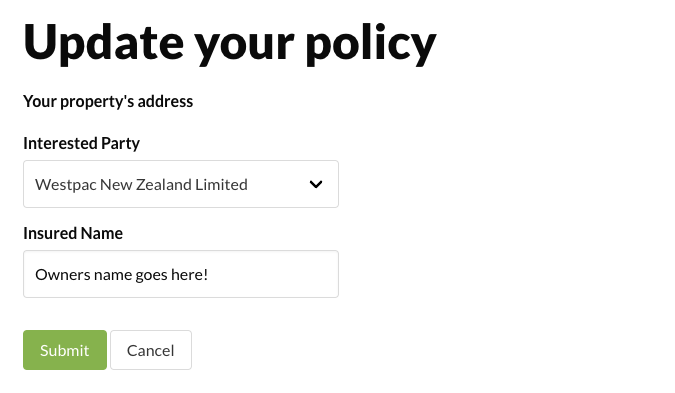

Changing Insured Name or Interested Party

“Insured name”

- You can correct the Insured Name here, but please note if there has been a change in ownership (entities), a new application/policy will be required.

“Interested Party”

- If you’ve paid off the mortgage and want the bank’s details removed, or you’ve re-financed/mortgaged the property and want to change or add the name of the bank/financial institute.

Need to correct an insured name spelling or add a spouse? Change the name of the recorded bank? Click on the “Insured name” or “Interested party” buttons. Select whichever Interested party applies (select ‘other’ if yours is not listed) and enter either your name, company or trust name (whoever owns the property) as your Insured name then click ‘Submit’.

After you have made your changes, click ‘confirm’ at the bottom of the page to proceed to the confirmation and payment sections, where you will either be refunded or required to pay a difference based on the changes made.

Review and confirm

Review your new cover details under ‘Confirm Change’, and the smart quote system automatically adjusts the price of your policy according to your changes. If a refund is due, we’ll process this within 1-3 working days.

You can make more than one change at once. Each time you make a change, the premium will recalculate and show you any difference in cost (calculated up to the policy renewal date). If you change your mind, cancel the transaction and no changes will occur. If you want to proceed with a change, click confirm and pay the additional premium (or confirm the refund). Alterations take effect immediately. A current certificate of insurance is also then immediately available on your dashboard.

After making changes, your online certificates and documentation will be updated and a copy sent to your registered email address.

Still haven’t found the answer you’re looking for? Here are some frequently asked questions that might help:

FAQ’S

Q. I’ve accidentally put the wrong start date on my policy, can I change it now?

A. Unfortunately, we are unable to alter the inception date of a policy once it’s been purchased. You can, however, cancel the policy from your dashboard back to the original inception date and re-purchase the policy (from your dashboard) with the correct date. Our system will automatically provide you with a full refund from the original policy.

Q. How do I amend or correct the home floor area on a policy I have already purchased?

A. Please contact our support team to make this amendment for you – [email protected].

Q. The water supply on my property is incorrectly noted, how do I change that from Town to Own Supply or from Own Supply to Town?

A. Please contact our support team to make this amendment for you – [email protected].

Q. How do I correct the property address on a policy I have already purchased?

A. Please contact our support team to make this amendment for you – [email protected].

Q. How do I change my details or password on my account?

A. From your dashboard, click on the “Account” option in the top-right corner of your screen and select “Profile”. Here, you can update your email address, phone number, postal address, and change your password to something more personal.

If you’ve forgotten your password, click the “Forgot my password” option to reset it. Simply follow the instructions to complete the process.

But it’s not all doom and gloom.

Homeowners and Landlords are facing significant financial pressure in 2023.

The increase in mortgage rates, combined with rising property insurance costs, has put a strain on homeowners cash flow and the budgets of landlords, who are facing increased costs without a corresponding increase in rental income.

In addition, over the last couple of years tax changes have meant that landlords who don’t own new builds can no longer fully deduct the cost of interest as part of their annual tax return. So it’s a double whammy when it comes to interest rates; pay more, less tax relief.

As well as mortgage interest and council rates, a major expenditure item for homeowners is insurance. This article looks at house insurance costs, where they are heading, average cost per region, and what you can do to keep yours at bay.

Why are insurance costs rising?

Build costs:

The significant increase in construction costs over the last 3 years has meant that landlords (and homeowners alike) need to increase the insured value of their homes if they are to remain fully covered.

Increasing the insured value of a house means more risk to the insurer, which ultimately means more premiums to cover that risk. In short, it costs more to buy more. In some cases, homeowners have had to buy 20%+ more cover to keep the ‘full cover’ they want. If the house is located in a remote region then the supply of materials and labour to that location will cost more.

Regulatory changes:

Contrary to popular belief, a house insurance policy does not provide cover for land damage (e.g landslides), and the cost of repairing a house damaged by an earthquake is funded (to a certain level) by the Government through the New Zealand Earthquake Commission (EQC)

In October 2022 the EQC increased their levy. For most houses this is an increase of over $200. This levy is included in the insurance bill you receive from your house insurer.

Learn more about how EQC cover works

Reinsurance:

This is the insurance that insurers buy so that they can pay claims in a major event. For example if an event, such as a flood, causes losses to an insurer that exceed a certain amount, e.g. $20m, then the reinsurers pick up the tab after that.

Insurers in New Zealand are required by the Reserve Bank to carry enough capital reserves or reinsurance to pay all claims arising from a 1 in 1000 year natural hazard or weather event. This is an incredibly significant event. To put it in perspective the Auckland 2023 floods were a 1 in 200 year event.

In most other countries the requirement for insurers is 1 in 250 years, meaning that New Zealand has the highest threshold for cover imposed on its insurers compared to anywhere in the world.

This high level of cover costs insurers a lot of money, and they pass this cost onto individual homeowners.

Location of property:

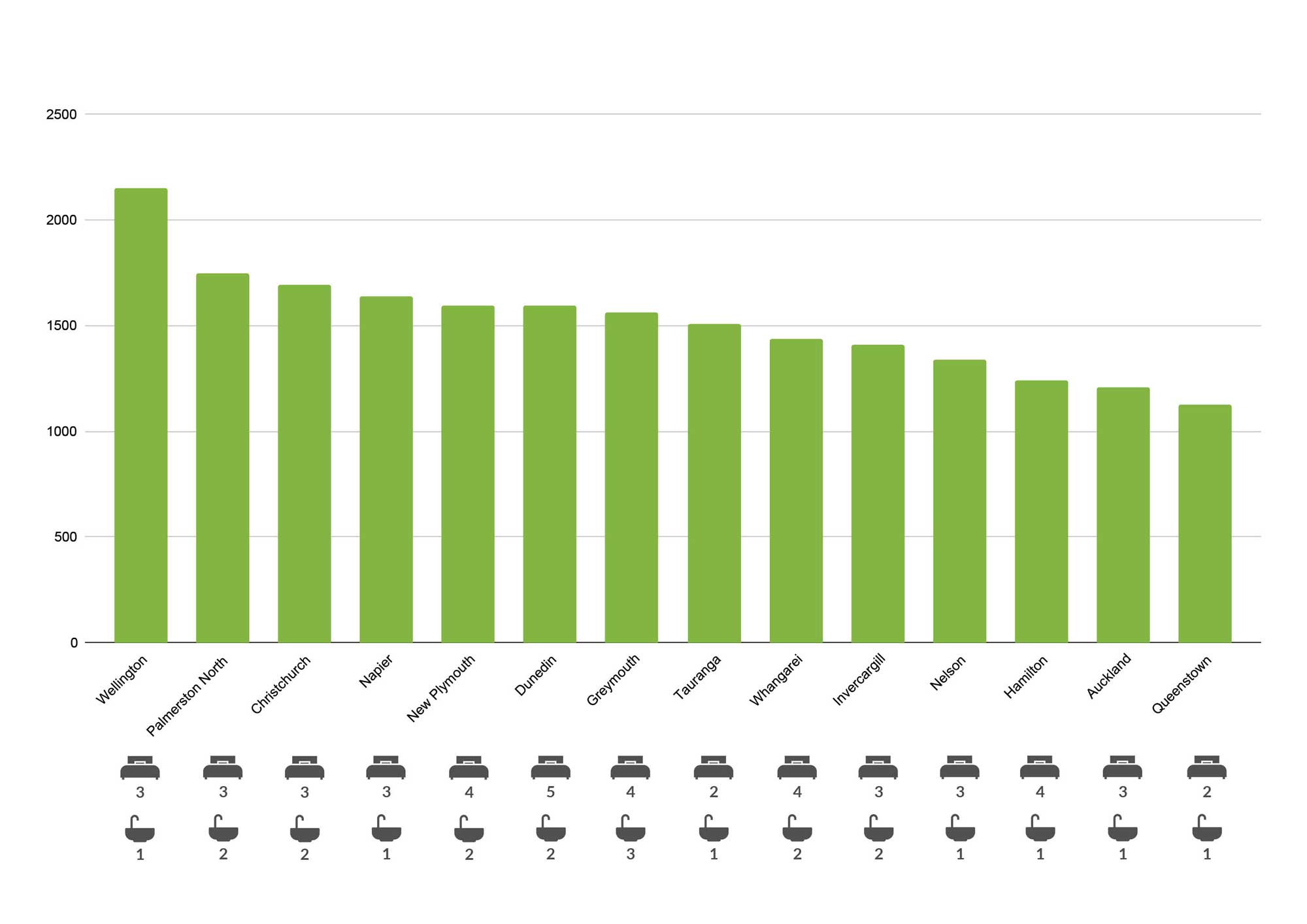

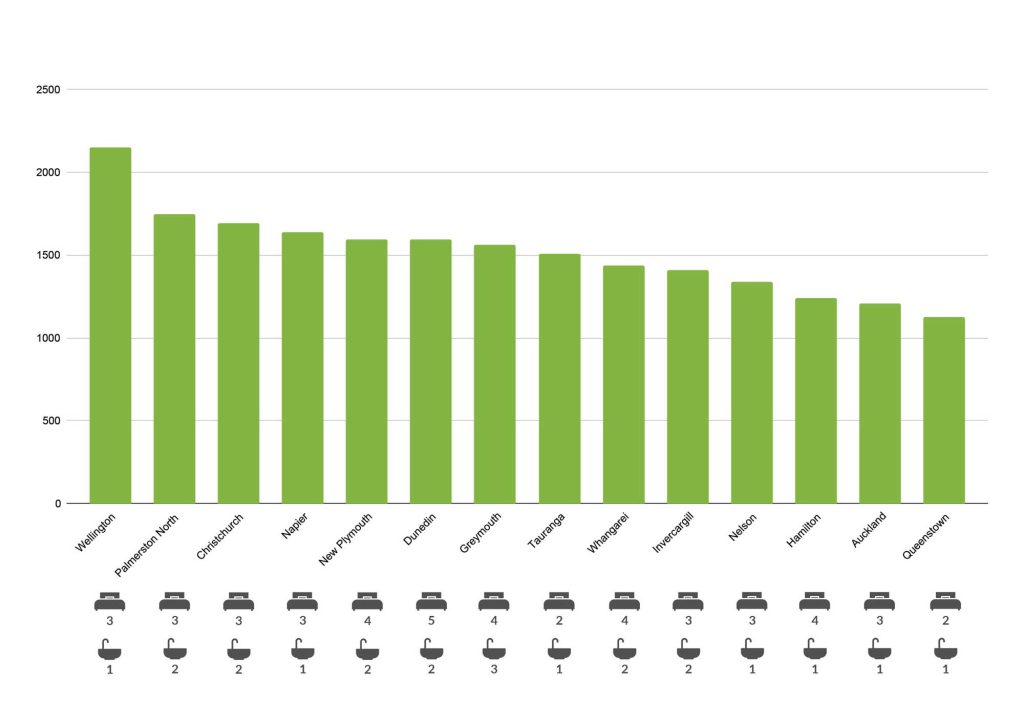

The location of your property has a major influence on premium.

For example, Wellington properties are notably more expensive to insure (with insurance cover increasingly difficult to obtain). The seismic risk in Wellington, and other parts of NZ, mean that it is a lot more expensive to insure in Wellington compared to much safer areas such as Dunedin and Hamilton.

Insurers are also starting to use premium modelling called ‘risk-based pricing’. What this means is that instead of a cross-subsidisation approach, the insurer will charge a premium for a house that is directly related to the risk of that house. Traditionally insurance has been a ‘premium pool’ based approach where the many pay into the pool to help the few that need to claim – but this approach lacks fairness given that homeowners in lower-risk areas start to subsidise those that claim a lot more due to seismic risk or adverse weather. The risk-based pricing approach has its own shortcomings as it means that for some people, e.g. coastal properties, the house insurance premium becomes so high that it is not affordable.

This graph provides a snapshot of the average premiums across different regions (without pure risk-based pricing):

The above graph is based on Feb 2023 homes.co.nz insurance cost estimates (powered by Initio) – for properties valued between $695,000 – $710,000. Insurance cost (incl gst) is based on an excess of $650 and does not include contents.

Attention to age of the house:

Some insurers are paying more attention to the age of the home to calculate its insurance premium. Houses built in the 1980’s for example are attracting higher premium loading due to issues with the plumbing of the era.

Similarly, houses built before 1940 are now considered ‘older homes’ by most insurers, and as well as additional requirements on the homeowner to verify that the roofing, plumbing and wiring have been replaced or are in good condition, the cost of insurance is higher than houses built post the 1940 decade.

By large newer homes (post 2010) attract the lowest premium for age.

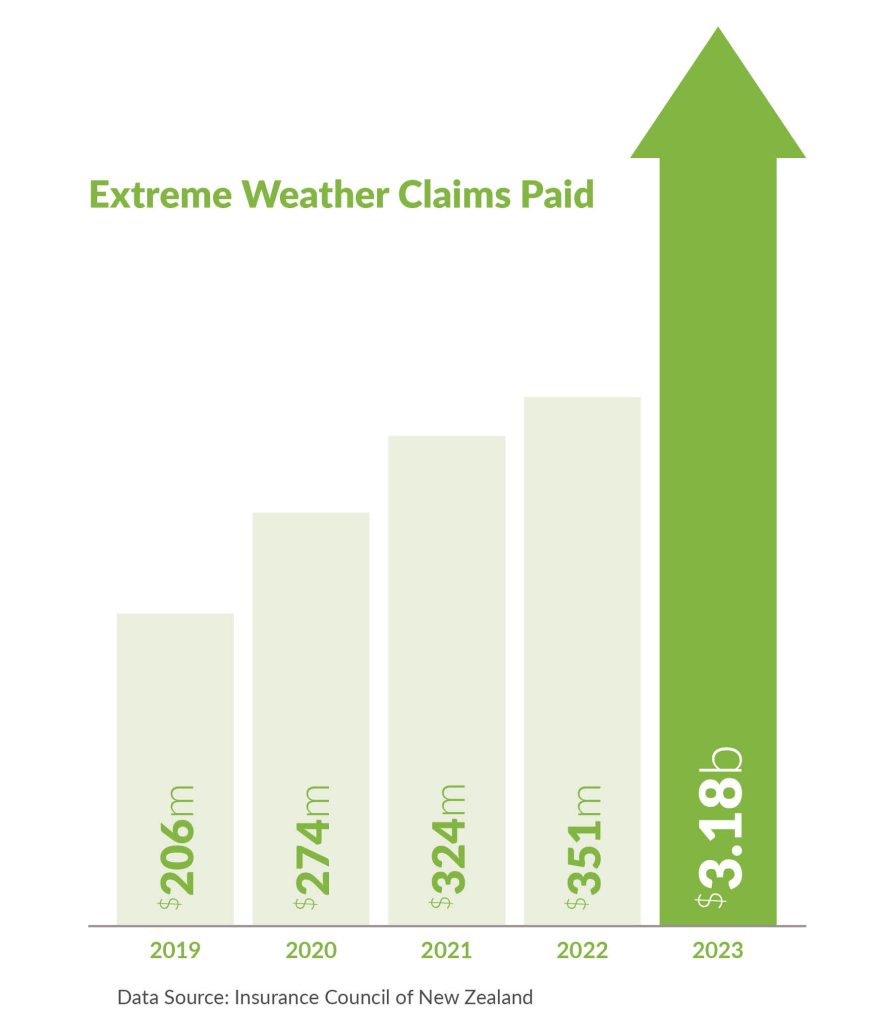

Increase in the frequency and severity of weather events:

The average number of significant weather events for the decade ending 2020 was 9.7 per year. In 2021-22 there were 21. So far in 2023 we have seen 3 significant weather events.

More floods, cyclones and natural disaster events lead to more damage, and the majority of the repair and rebuild costs are borne by insurers. In simple terms, an insurer wants to make sure that its costs do not exceed its premium income. The single biggest cost to an insurer is what it spends on responding to and paying for insurance claims, but things like reinsurance (discussed above) and operating costs (staff, compliance costs etc) are also major expenses.

Increases in claims, at a macro level, put significant pressure on the premiums charged to homeowners, and because recent years have seen a large increase in claims, house insurance premiums have been adversely affected.

Here’s the good news! There are ways you can combat rising insurance costs.

Homeowners and landlords can adopt some strategies to help control their rising insurance costs, and also help prevent damage from occurring in the first place, as let’s face it, whether insured or not, no homeowner wants to deal with damage or loss:

Pay annually: For most home insurance, if you pay your premium annually it will be cheaper than the annualised equivalent of paying monthly.

Increase excess: The higher the excess the lower the premium. Insurers are now offering excesses as high as $2,000. This means that you will have to contribute $2,000 every time you have a claim. If you don’t claim often and you can sustain a higher excess then this is a good way of reducing your insurance costs.

Combine policies: Purchasing policies like house and personal contents together will often help reduce the overall premium, as combined to buying these policies separately.

Shop around for the best deals: Shopping around for insurance coverage can help ensure you are getting the best deal. There are comparison tools available to help you compare policies from multiple insurance providers. Remember that cheapest is not always best, so it pays to check what you are getting for your insurance spend.

Regular maintenance: A leading cause of water damage to the home water entering through overflowing pipes and gutters. Ensuring gutters are cleared regularly may just prevent that wet ceiling.

Electrical appliances: Powerboards or multi-plugs can cause house fires if they are old or low quality. Take the time to check these items in your homes or during a tenancy inspection.

Security: At home security is now more accessible than ever. The last few years have seen a number of connected security devices become available to homeowners. Products such as the Nest Protect Smoke Alarm not only save lives but can save houses too. Security cameras and alarms are a useful way to discourage intruders and reduce the risk of burglary.

Fire extinguishers: Too many kitchen fires could have been brought under control with the use of a simple, and low-cost, fire extinguisher. Having fire extinguishers in your home or rental property will reduce the severity of damage. It is also important to ensure everyone in the household knows where they are located and how to use them. Learn more about fire extinguishers.

Initio insurance; Quote in seconds, cover in minutes, claim in an instant.

As an insurance provider committed to pushing the boundaries of innovation, it gives us immense pride to announce that Initio has been awarded the Editor’s Choice for Home Insurance Innovation by MoneyHub. This prestigious award validates our unwavering commitment to revolutionise the insurance industry and deliver unparalleled service to our customers.

Understanding MoneyHub’s Editor’s Choice Awards

MoneyHub’s Editor’s Choice Awards are a symbol of excellence and are the result of extensive research conducted by the MoneyHub team. As winners of the Home Insurance Innovation category, we are honoured to be recognised for our dedication to redefining the insurance experience for everyday New Zealanders.

Challenges in the Insurance Market

The insurance market, particularly home and contents coverage, presents unique challenges. With numerous providers and varying prices, it is difficult to identify a single “best” insurer. MoneyHub understands this complexity and strives to showcase insurers and products that go above and beyond standard offerings. Their focus lies in identifying providers that bring real value and benefits to policyholders.

Initio: Pioneering Home Insurance Innovation

We have always believed in challenging the status quo and embracing innovation at Initio. Our groundbreaking technology has transformed the insurance landscape, providing customers with an exceptional experience. By using our unique technology, we have entirely transformed the insurance process. Now, prospective customers can get a thorough assessment of their insurability and receive a quote for property premiums in less than six seconds. This remarkable achievement is unparalleled in our industry and sets us apart from traditional insurance providers.

In 2022, our collaboration with partners such as homes.co.nz allowed us to generate over 40,000 automated home insurance quotes daily. This partnership has played a vital role in bringing much-needed transparency to the New Zealand home insurance market. We understand the importance of empowering customers with readily available information to make informed decisions about their coverage.

MoneyHub’s Perspective on Initio

Christopher Walsh, MoneyHub’s editor, shared his insights on why Initio emerged as the deserving recipient of the Editor’s Choice for Home Insurance Innovation:

“The recent cyclone and flood devastation in early 2023 highlighted the urgent need for insurers to prioritize technology for claims and risk-pricing. In addition, immediate quotes for renewals and new policies are crucial for customers to compare and save. Initio, a forward-thinking insurer, has been at the forefront of technological innovation. The company received industry award nominations in 2019 and 2022 for their advancements in quoting and claim technology. Unlike many players in the industry, Initio embraces change and is dedicated to propelling the insurance industry forward, ensuring ordinary New Zealanders can obtain insurance pricing as swiftly as possible.”

Receiving MoneyHub’s Editor’s Choice for Home Insurance Innovation is a testament to our unwavering commitment to revolutionizing the insurance industry. We are proud of our innovative technology that provides customers with unparalleled speed and convenience in obtaining insurance coverage. At Initio, we will continue to push boundaries, leverage technology, and prioritize customer-centric solutions. Our mission is to empower ordinary New Zealanders by delivering cutting-edge insurance experiences that truly make a difference.

To Offer Unique Insurance Product for Holiday Homeowners

New Zealand insurance provider, initio, is excited to announce an alliance with Bachcare, the country’s leading holiday home management company. This unique partnership will provide an innovative insurance product meticulously tailored for holiday homeowners.

Initio, in conjunction with Bachcare, will provide instant online coverage for holiday homes, including those that are also partially rented out. The extensive coverage includes not only holiday homes, but also primary residences, contents, vehicles, and rental properties. With initio’s customer-friendly online platform, obtaining comprehensive insurance coverage for your holiday home is quick and easy.

Initio stands out from competitors due to its forward-thinking approach and unwavering focus on customer satisfaction and simplicity. With initio, you can get a quote in 5 seconds by simply entering the property address. Once insured, customers can also update their insurance cover on the fly with the live policy dashboard.

Smart Claims enhance the experience

To provide an even better customer experience, initio recently upgraded its innovative Smart Claims platform. Having proved its worth in handling claims during severe weather events earlier in the year, this platform brings a new level of efficiency and transparency to the claims process. With features like tailored questionnaires for different types of loss and real-time claims tracking, this technology provides a more streamlined and personalised claims experience. The recent upgrade enhances the comprehensive insurance coverage initio provides, making the process of filing and tracking claims for holiday homes even easier and more convenient.

Specialised Holiday Home cover

Initio developed their specific holiday home insurance product around a decade ago, realising that there were no dedicated holiday home insurance products available from competitors. Rather, competitors simply offered a regular house and contents policy that would often not meet the requirements of the holiday homeowner. Initio understands the unique insurance requirements of holiday homeowners and has meticulously designed their policies to cater to these needs. Whether homeowners use the holiday home for personal enjoyment, or as a rental, initio provides the necessary insurance coverage to protect their investment. With their unique feature of instant online cover in either of these scenarios, holiday home owners can get unparalleled peace of mind.

“We are thrilled to be collaborating with Bachcare, providing an exceptional insurance product that has been designed for holiday homeowners,” said Rene Swindley, CEO at initio. “Our innovative approach and commitment to excellence align perfectly with Bachcare’s mission of providing customers with the best possible experience”.

More about initio & Bachcare

Initio is a pioneering insurance provider based in New Zealand, committed to revolutionising the insurance industry. They offer comprehensive coverage to meet the unique needs of homeowners, covering holiday homes, primary residences, contents, vehicles, and rental properties.

Bachcare is New Zealand’s leading holiday home management company, offering an array of holiday homes throughout the country, focusing on exceptional service and enabling homeowners to maximise returns on their holiday home investment.

Learn more about initio’s Holiday Home insurance options

From Seagulls to Scribbles

Life can be full of surprises. This year, our clients’ experiences range from the utterly unexpected to the charmingly chaotic. We understand the need for comprehensive property insurance that covers these unforeseen events.

This year, initio has processed a record number of claims, almost doubling from last year. Our payouts have increased significantly by over 230%, a substantial rise compared to the 45% increase from 2021. The major storms and flooding we saw at the beginning of the year (along with other significant events) meant more people needed help from their insurance provider, which in turn pushed up the cost of insurance premiums. The intensity and frequency of these events have been steadily increasing, with 2023 being off the chart, as shown in the graph below:

It’s worth noting that the above figures are across all New Zealand insurers and were calculated in August 2023, these numbers will be even higher now.

The growing number of Kiwi homeowners choosing initio has also influenced these increased numbers. We’re delighted that many have selected us as their insurance provider, indicating our ongoing growth and success. A heartfelt thank you to those who have recently joined us and to our loyal customers who have continued with us this year.

As we wrap up the year, let’s explore the lighter side of insurance with a look at some of the most unique claim trends we’ve encountered in 2023:

Nature is wild

Nature can be unpredictable, and it certainly was for a few of our clients this year. In one instance, a drone was unexpectedly taken out by a seagull, while in another, a bird decided to make a home in a client’s chimney, causing a mess and eventually meeting an untimely end. Nature’s surprises can sometimes be costly! Domesticated pets also caused their fair share of claims this year, the majority of which were caused by them not making it outside in time to use the bathroom. These types of claims alone caused thousands of dollars worth of damage.

The artistic and the audacious: Children at play

Children bring joy and, occasionally, a bit of chaos. From a child’s artistic scribblings using foundation makeup that unfortunately left lasting marks on furniture and décor, to the regrettable incident where a backpack met its fate under the blades of a lawnmower, and those inventive yet ill-fated attempts at cleaning up spills with a vacuum cleaner, the innocence and spontaneity of children can sometimes come at a cost. Not to mention the numerous TV and tech accidents involving toy hammers, building blocks and balls, all leading to thousands of dollars of damage.

Another client unexpectedly went into labour while at home, an experience filled with surprise and natural wonder. But when her water broke, it soaked the carpet in the process.

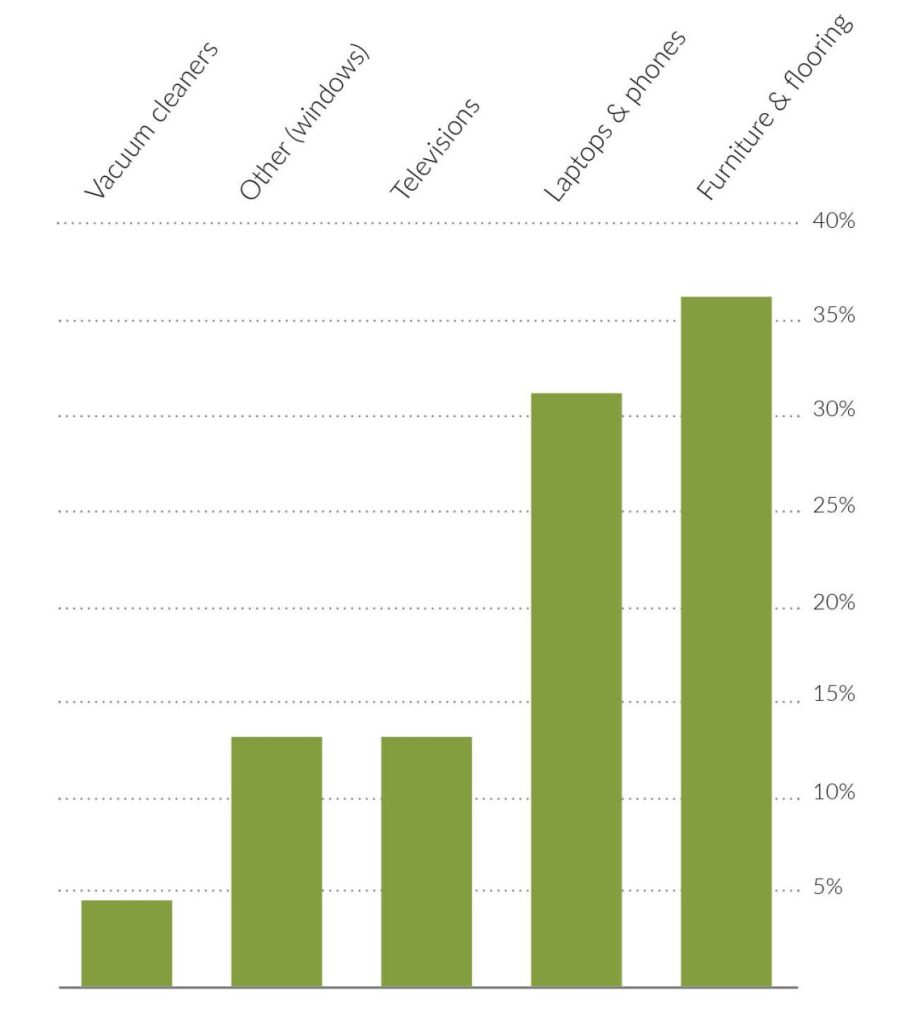

CHILDREN VS HOUSEHOLD ITEMS 2023:

Tesla tales: The perils of parking

This year, our Tesla owners have navigated various challenges, notably a rise in claims for windscreen damage and parking incidents. Even the most advanced vehicles aren’t immune to the quirks of daily life. One advantage of owning a Tesla is the reduced petrol costs, coupled with comprehensive camera coverage. This feature ensures most incidents are recorded, providing valuable evidence. It’s important to remember if you accidentally collide with a parked Tesla, chances are, it’s on camera.

Candles and pianos don’t mix

Coincidently we saw two cases of candle wax melting onto pianos this year, making them unplayable. These two incidents alone cost thousands of dollars of damage (pianos are expensive!). While they might create a beautiful ambience, the takeaway lesson would be perhaps don’t have lit candles on top of your piano.

At initio, we’ve seen it all, from feathered fiascos to technology tragedies. These stories showcase the unpredictable nature of life and the essential role of comprehensive property insurance. Whether it’s a mischievous child or a parked Tesla, we’re here to ensure that when life happens, you’re covered. Discover the ease of getting a quote and the simplicity of insuring with initio for yourself.

Percentages in this article have been rounded.

Crack the champagne – a toast to our focus on insurance claims!

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

Initio stands out not just for its technology, but for its practical, impactful applications that significantly improve the customer experience. Let’s explore the technological innovations at the core of our submission, which we call Smart Claims:

A fully digital, seamless claims process

Initio is one of the few insurance providers offering customers a 100% online claims process from start to finish, setting a new standard for convenience and efficiency in the insurance industry. Our Smart Claims platform eliminates the need for traditional phone calls to confirm details, handling everything online with ease and precision. This approach not only simplifies the claims process but also significantly speeds it up, allowing customers to focus on recovery and rebuilding without unnecessary stress.

Key features of our Smart Claims process:

- Streamlined submission: Customers can submit claims quickly and effortlessly, without the traditional hassles of paperwork and long waiting times.

- Efficient claims management: Our system ensures claims are managed efficiently, significantly reducing wait times and allowing our staff to focus on expediting claim processing rather than making follow-up calls.

- Reduced need for customer calls: Our online dashboard’s transparency and instant access mean fewer calls are needed, making us more available to pick up when you do call. This enhancement significantly improves your experience while allowing our support team to assist you more efficiently..

Proactive customer support and real-time updates

During Cyclone Gabrielle, Initio leveraged its advanced mapping tool, Locatio, to proactively identify and contact customers likely affected by the disaster. This not only ensured timely assistance but also demonstrated our proactive approach to customer care.

Enhancements in customer support:

- Claim support and updates: Our efficient system freed up our claims consultants to provide personalized support, focusing on those in critically affected areas.

- Continuous availability: Despite the digital focus, our claims consultants remained available via phone for those needing personal interaction, further supported by continuous online chat and easy claim access.

- Transparency and real-time updates: Customers could monitor the status of their claims through their dashboards, which included detailed updates such as site visits by builders and a comprehensive communication history.

Initio’s offerings are not only innovative but also distinctly superior to what is currently available in the market, both domestically and internationally.

What makes smart claims different?

- Complete online management: Our website allows customers to fully manage their policies independently, from purchase to claims, providing unparalleled control and flexibility.

- Advanced risk assessment: Utilising data from Regional and Government Councils and updates from the LINZ database, we provide precise risk assessments, enhancing our underwriting process.

- Synergy of smart claims and Locatio: The integration of these technologies not only reduces administrative burdens but also accelerates claims resolution, improving overall customer satisfaction.

What the Canstar judges said about initio’s online insurance experience

The awards panel recognised that initio is the pioneering insurance provider in New Zealand. We enable customers to secure quotes, arrange cover, and file claims swiftly via a digital platform. They praised initio for its effective service that simplifies insurance management for homeowners, utilising technology to evaluate risks promptly and precisely.

The judges were most impressed by the ease and efficiency of receiving a quote with Initio. There was consensus around the judging table that this could be disruptive as other insurers look to adopt a similar approach.

Our ongoing promise

Initio will continue to refine and enhance our platform, committed to providing the finest digital experience available in New Zealand, ensuring our customers receive outstanding service tailored to their needs.

For more information

Smart moves, part III

In this third instalment, we shift gears from payment strategies to practical protection. Graeme Fowler shares the habits that help landlords avoid disputes, speed up claims, and stay on top of their obligations, starting with inspections.

How important are regular inspections?

“Very. You should be inspecting every three months, no excuses. If something goes wrong and you can’t show a pattern of regular checks, you could run into problems during a claim.”

Graeme says inspections aren’t just about identifying damage, they’re also about proving you’ve taken reasonable steps to manage risk. This becomes especially important if a claim is disputed or complex.

What kind of documentation helps at claim time?

“Keep your paperwork tidy – inspection reports, tenancy agreements, anything that proves what’s happening at the property. When you do need to make a claim, it makes life much easier.”

Graeme has seen how missing or disorganised documents can cause claim delays – or worse, denials. His approach: prepare like you’ll need it, even if you never do.

From initio: Quarterly inspections are a requirement under our landlord policy. We recommend keeping clear records and photos. While we don’t currently offer a document upload feature, we suggest using a service like myRent to store these securely. As well as acting as a digital filing cabinet, myRent also helps with tenant communication, rent collection, inspection reminders, and more – making it a handy tool for busy NZ landlords. They also offer helpful guidance on how to handle your first routine inspection. Learn more about your obligations as a landlord here.

Any other overlooked mistakes landlords should avoid?

“Choosing a really low excess thinking it’s safer. But it often just means you’re paying more in premiums – and if you’re unlikely to claim, it doesn’t make sense.”

Graeme says newer landlords sometimes prioritise a lower excess out of caution, but over time that strategy can backfire.

From initio: You can update your excess at any time through your online policy dashboard. We’ll show you the premium difference in real time so you can make an informed choice.

What about monthly payments?

“They’re convenient, but they tend to cost more. If you can pay annually, do it.”

While this topic was covered earlier in the series, it’s worth reinforcing: consistent cost-saving habits (like paying annually) make a difference when you own multiple properties.

From initio: Annual payments are the most cost-effective option. We clearly show the difference between monthly and annual payment on our quick quote tool, so you can choose what works for you.

Coming up next in the Smart Moves Series:

How to think about risk – why location isn’t everything when it comes to insurance.

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Related articles:

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: |

Initio Limited |

| FSP Number: |

FSP523166 |

| Website: |

www.initio.co.nz |

| Phone: |

0800 763 929 |

| Email: |

[email protected] |

| Address: |

6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: |

Carmen Jones |

| FSP Number: |

FSP1011244 |

| Contact Email: |

[email protected] |

| Qualifications: |

New Zealand Certificate in Financial Services (Level 5) |

| Experience: |

35+ years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type |

Commission Rate |

| House and contents insurance |

22.5% of insurer premium portion |

| Motor vehicle insurance |

10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.