You can cancel a policy yourself online any time through your dashboard, and you will be refunded the unused premium.

Simply log into your initio dashboard and select the ‘Cancel Policy’ option on the policy you want to cancel. You can then select the date to cancel the policy from, and you will be instantly shown the refund amount, which will be refunded to your credit card or account with five working days.

The most common reason for cancelling a policy is because the property has been sold, with the date for cancellation of the policy being the settlement date. We realise that the settlement date may have already passed or be yet reached. You can cancel the policy with effect from a date within a 30 day window, subject to the current period of your policy, ie the current paid month or if you pay annually, the current year. If you are trying to cancel more than 30 days ahead, you will need to wait till you are within the available window.

Once the policy has been canceled it will move to being an inactive policy, which can still be viewed from your dashboard and you can still make a claim for that time period of cover.

Troubleshooting: Why can’t I choose the correct cancellation date?

To cancel your policy for a future date, such as when you sell your property, follow these steps:

1. Check your renewal date

If you want to cancel your policy next month, you might need to wait until your policy renews.

For example, if it’s mid-July and your policy renews at the start of August, and you want to cancel in mid-August, you need to wait until early August when the policy renews.

2. Refund details

You’ll get a refund for any unused portion of your policy after the cancellation date. The credit will be applied to the card initially used for payment, if this is not suitable please get in touch immediately to provide your preferred account details.

Example:

Current Date: Mid-July

Policy Renews: Start of August

Desired Cancellation Date: Mid-August

What would you need to do? Wait until early August for your policy renewal. This ensures your cancellation goes smoothly and you receive any eligible refunds.

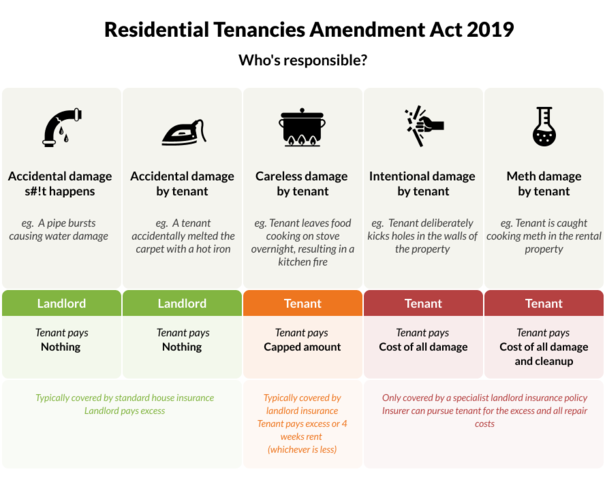

1. A tenant can be held fully responsible for intentional damage

A tenant who intentionally causes damage can be held liable, and the landlord can ask them to pay for the damage. This seems like common sense.

If the landlord has insurance cover for deliberate damage, they can lodge a claim with their insurance company. The insurer will pay for repairs, and try to recover the costs from the tenant later down the track (if it’s possible).

2. A tenant can be held partially responsible for careless damage

If a tenant has ‘carelessly’ caused damage they can be held responsible, but only up to a maximum of the landlord’s insurance excess, or four weeks of rent (whichever is less).

But what is considered careless? We’ll get to that shortly.

In this case, the tenant can share in with the benefits of the landlord’s insurance cover.

3. A tenant cannot be held responsible for accidental damage

If a tenant accidentally causes damage the act considers that sometimes; these things just happen, and the damage is the landlord’s responsibility.

However, this falls into the same problem. It’s often not crystal-clear whether damage is ‘careless’ or ‘accidental’, nor is it something the landlord and tenant may easily agree on.

Many things that would ‘sensibly’ be considered careless, have been ruled by the Tenancy Tribunal as accidental – such as knocking over and leaving a hot iron to melt into the carpet.

So it’s a good idea to read through some recent Tribunal decisions – this may be helpful for future tenant discussions.

A case of melted carpet

The 2019 changes to the act are still relatively fresh and we could still see its interpretation change. This 2020 example gives an indication of the Tribunal’s approach to the difference between careless and accidental damage.

Braziers v Guttman 2020

A landlord (Braziers) took their tenant (Guttmann) to the Tenancy Tribunal to recover damage.

The landlord alleged a patch of carpet was melted, and claimed the cost of carpet replacement from the tenant for $772. The tenant admitted the carpet was melted when they accidentally knocked over a hot clothes iron.

To avoid any liability the tenant needed to prove that they didn’t carelessly or intentionally cause the damage, and that it was a reasonable accident.

The tribunal decided the carpet damage was accidental in nature, and did not have enough ‘careless’ elements to render otherwise. There was no liability against the tenant for repair costs or excess, and the landlord would need to pay for the repairs themselves, or through their insurance (and pay the excess).

Accidental Tenant Damage vs Careless Tenant Damage

As we’ve mentioned, the Act’s definition of the difference between accidental and careless damage could be better, and we are now seeing the results of this coming through the Tenancy Tribunal process. Here’s our overview:

Accidental damage is something caused by the tenant, but outside their control (for example, tripping and putting a knee through a wall).

Careless damage is caused through lack of attention or concern for the consequences (for example, leaving a stove on while you go to do something else).

But ultimately these guidelines will be up for subjective judgement. We expect to see more disagreements between tenants and landlords over who’s liable for damage. If you’re a landlord that’s applying to the Tenancy Tribunal to see what they think, you should be prepared to prove that damage was caused intentionally – or at least carelessly to avoid paying an excess.

What’s our position on all this?

We believe a clearer division between what is accidental and careless tenant damage is needed. If no clear interpretation can be made then ideally all tenant damage – whether careless or accidental – should be treated as the responsibility of the tenant (up to the smaller of the excess or four weeks rent).

This will save a lot of time and arguments. However, based on recent cases the Tenancy Tribunal doesn’t quite see it the same way.

Why can’t the tenant use their own insurance to pay for the damage?

That’s a good question.

In the past tenants were considered completely responsible. If the tenant had their own contents insurance the landlord could rely on this to pay for damage by the tenant. Almost all contents insurance policies will include the tenant’s liability to at least $1 million for accidental damage.

For many landlords, confirmation of contents cover became a condition of tenancy; if the tenant accidentally burnt the house down, the landlord’s insurance company could get the money back from the tenant’s insurance company.

Then a couple of big things happened.

1) Court of Appeal decision on Holla v Osaki

This landmark ruling established that landlords and their insurance companies could no longer recover the costs of damage from tenants. In this case, it was $216,000 worth of damage caused by the careless action of the tenant leaving an unattended pot cooking on the stove.

2) Residential Tenancies Act 2019

This act reversed the effects of the Holla vs Osaki decision and brought back some responsibility for tenants who cause careless damage. Responsibility, however, was limited to the lesser of the landlord’s insurance excess or four weeks rent.

It established that the tenant is fully responsible for intentional damage and that the tenant cannot rely on the landlord insurance policy for this. Remember that; as you would expect, a tenant’s contents insurance won’t provide cover for damage that’s intentionally caused.

It’s the stuff of nightmares. The family car is booked in for a Warrant on Tuesday, but you still have to do the Monday school run.

Everything runs to plan until a distracted driver rear-ends you at the lights. Will your insurance still cover the damage?

Don’t worry, your insurance company won’t automatically decline your claim just because your WoF expired.

The government requires a WoF on cars to keep people and roads safe. It means a certified mechanic has confirmed the vehicle is safe to operate on our roads, including safety features, and mechanical components like tyres and brakes.

While a WoF is a legal requirement, we’ve all been in the position where you simply forgot, or just have to get through another few days before you can get it to the workshop.

When would your claim be declined?

If you make a claim on your car, and your insurance company discovers it doesn’t have an active WoF (they can easily find this), they will want to find out:

1. Was the cause of the accident an issue with the car?

2. Would the issue have been resolved by a WoF check?

Your claim could be declined if it’s proved that an issue with the car was the cause of the accident. This could be bald tyres with no tread causing you to spin out, or tattered brakes meaning you couldn’t stop in time to avoid a collision.

These are obvious causes that are easy to pick up. If the issue is something less obvious, your insurance company might determine whether the issue would’ve been picked up by a WoF. If it would’ve, your claim could be declined. These are all reviewed on a case-by-case basis.

What if the cause was not an issue with the car?

Generally, most accidents don’t involve an issue with the car, so it won’t affect the ability to make a claim.

If your car wasn’t being operated at the time of a crash, there’s no reason to deny your claim as the lack of warrant has nothing to do with the damage. If someone else reverses into you and caves in your front bumper while your car is parked, that’s hardly your fault and nothing a warrant would prevent so you won’t be pinged.

Remember not to drive your car if you notice an issue, and fix it as soon as you can. This way if you have an accident and forgot about your WoF, your insurance coverage is still valid.

Just use your bank app on your phone to make the payment. It’s quick, safe, and you don’t need to share your banking details, making it one of the most secure ways to pay online.

Currently available to ANZ, ASB, BNZ, The Co-operative Bank and Westpac customers.

*Available on annual payments only.

How to make a payment

Choose the online eftpos option from the payment screen when renewing your annual policy.

Select your bank and enter your mobile number.

Approve the payment request in your bank app.

That’s it! – the payment is made instantly if funds are available.

Key benefits

Direct account-to-account transfers

No need to share banking credentials

Secure payment process

Simple smartphone-based payments

Getting started

If you use your bank’s mobile app regularly, you shouldn’t need to do anything special. Just check you have the latest version of your bank’s app installed. Below are a few bank-specific requirements:

ANZ customers

Download or update to the goMoney banking app.

Have an ANZ everyday account (e.g. Go, Freedom, Business Current) or Flexible Home Loan account with sufficient funds.

Contact your bank to register a verified mobile phone number with OnlineCode or ANZ Pay to Mobile.

Online EFTPOS is one of the most secure payment methods available today. This is because it doesn’t ask you to enter your bank or payment details directly. Instead, you approve each payment through your bank’s app, adding an extra layer of security.

What is the maximum purchase limit for Online EFTPOS?

Each bank sets its own purchase limits:

Bank

Limit

ANZ

$5,000 per transaction

ASB

$30,000 per day

BNZ

$12,000 per day

Westpac

$5,000 per transaction (unless agreed otherwise)

Co-operative Bank

Flexible daily limit depending on your account agreement

You may also have specific limits set for your own account. Please contact your bank if you need to adjust those.

I don’t bank with one of these banks – when can I use Online EFTPOS?

The Online EFTPOS team is working to bring more banks on board. You can email [email protected] with your feedback or contact your bank directly to encourage them to join.

I don’t have the relevant bank app on my phone. Where can I get it?

We do our best to keep the information on our website about Online EFTPOS current. However, we can’t promise that everything is always accurate, complete, or up to date, and we can’t guarantee that it will meet your specific needs.

Digital only matters when it makes things easier at the moments that count.

You’ll often hear us described as a fully digital insurance provider. That’s true. But what does being digital actually mean for the people who insure with us?

For us, digital isn’t about removing people from the process. Removing the friction that gets in the way of something that should be simple is what it’s about.

Because our systems do the heavy lifting. Our support and claims teams avoid manual paperwork. They don’t have to re-enter details. They also don’t have to chase forms. Claims don’t need to be lodged through multiple phone calls. You don’t need to stitch insurance policies together by hand.

That time shifts to what truly matters when you feel overwhelmed, under pressure, or just want a clear answer.

It means we pick up the phone when you call or respond to you online in an instant.

Technology that gives time back to people

We use technology to make things faster and clearer. Things like online quotes, a customer dashboard, and a chatbot that can answer common questions at any time of day.

But here’s the key part: if our chatbot can’t give you the answer you need, it doesn’t trap you in a loop. It puts you through to a real person, straight away.

Digital tools should never be a barrier. They should be a shortcut.

That’s why we design everything we build on the technical side to give our team more time to help, not less.

People first, always

Have a look at our reviews, and you’ll see a common theme. People talk about being able to get hold of someone. About feeling listened to. About their insurance claims being handled with care.

Insurance claimscan be stressful for customers, and sometimes emotions run high; not every situation is simple. But when things are stressful, the last thing you need is to be playing phone tag with your insurance provider.

Digital insurance on its own isn’t enough. Digital only works if it makes human support easier to access when you need it most.

Why this matters when things go wrong

I saw this first-hand over Christmas when a family member was involved in a car accident. Thankfully, no one was seriously hurt.

In the middle of it all there were police, ambulances, fire trucks, people from the other vehicles, and broken glass mixed with Christmas pavlova scattered throughout the car, alongside tow trucks that needed organising. It was already stressful. Trying to get hold of someone, anyone, about the insurance only made it worse.

We couldn’t find details about their insurance policy details online, and their login didn’t show anything useful. There was no clear next step, just waiting and uncertainty at a time when answers mattered.

All I could think was how different this would have been if they’d been with initio. A claim could have been lodged immediately online; the system would have provided clear instructions on what to do next and what to expect from your insurance provider. All policy details and cover information would have been sitting there in one place.

Simple, transparent, and there when it counts

That’s one of the things we’re most proud of. With initio, your insurance policy, documentation, and details are available online through your dashboard. No digging through emails. No wondering what you’re covered for. No guessing who to call.

Insurance is stressful enough without added complexity.

Being a digital insurance provider isn’t about doing less for our customers. It’s about doing better. Using technology to remove the noise, so when you really need us, we’re available, responsive, and human.

Because at the end of the day, we’re not just digital. We’re people first.

Written by Megan Fisher, Head of Marketing at initio.

Megan has been with initio since 2022 and has over 20 years’ experience in marketing and product strategy. She works closely with initio’s claims and customer experience teams, giving her a first-hand view of how insurance works when customers need it most.

Working out the right sum insured can be harder when your home is not standard. Renovations, custom features, and specialist materials can all affect what it may cost to rebuild, and those details are easy to overlook.

Online calculators can be a helpful place to start. They are designed to give you an estimate based on typical building replacement costs, using the information entered along with available property and construction data.

Online calculators do not provide advice, and they may not capture every detail that could affect the rebuild cost of your home. If you would like a more tailored assessment for your specific property, a quantity surveyor or insurance valuation service may be the best option.

Key takeaways in this article

Renovations can increase rebuild costs

Unusual homes may cost more to rebuild

Non-standard materials can affect your sum insured

It’s worth checking whether the estimate feels right for your home

Why this matters for insurance

Your house insurance should reflect what it may cost to rebuild your home to a similar size and standard using today’s building costs.

For many homes, an online calculator can provide a useful estimate. But if your home has unique features, premium finishes, or non-standard construction, the cost to rebuild may be less straightforward. That is why it is worth taking a closer look before relying on the result.

What counts as an unusual feature?

An unusual feature is anything that could make your home more expensive or more complicated to rebuild than a typical home of a similar size. This might include:

architectural design features

high or vaulted ceilings

custom kitchens or bathrooms

bespoke joinery

imported fittings or finishes

unusual rooflines

heritage details

specialist glazing

detached studios or sleepouts

retaining walls or complex outdoor structures

These types of features can all add cost and may not always be fully reflected in a standard estimate.

How renovations can affect rebuild cost

Renovations can improve the layout, finish, or quality of a home, but they can also increase what it would cost to rebuild. For example, rebuild costs may be higher if you have added:

an extension

a new kitchen or bathroom

premium flooring

double glazing

custom cabinetry

upgraded cladding or roofing

decks or attached outdoor living spaces

Even if the work was done years ago, it can still affect what your home would cost to rebuild today.

Why non-standard materials matter

Some homes are built with materials or methods that are less common. This can make rebuilding more expensive, especially if the materials are harder to source or require specialist trades. Examples can include:

specialist cladding

imported tiles or finishes

plaster systems

unusual timber treatments

stone or decorative masonry

architectural glass

custom metalwork

If your home includes materials like these, it is worth making sure your sum insured reflects that.

Older homes can have hidden complexity

Older homes can also be more complex to rebuild than people expect. They may include features such as native timber, ornate detailing, decorative ceilings, original fittings, or older construction methods. Even if you would not replace every detail in exactly the same way, older homes can still involve more labour and higher rebuild costs.

Before relying on the estimate

If your home has been renovated or includes unusual features, it is worth asking yourself:

Have I upgraded parts of the home since I last reviewed my cover?

Does my home have high-spec or custom finishes?

Are there any specialist materials that may cost more to replace?

Is my home harder to rebuild than a standard house of similar size?

Would site access make demolition or rebuilding more expensive?

These questions can help you decide whether the estimate feels realistic for your home.

Why a calculator is still useful

An online calculator is still a helpful starting point. It can do a lot of the heavy lifting and help you get close to a realistic figure without having to work it all out from scratch.

Initio uses the Cotality Sum Insured calculator to help estimate what it could cost to rebuild your home. It uses the details you enter, or confirm, and compares them with construction industry data to generate an estimated rebuild cost for the improvements on your property. The main thing to remember is that it provides an estimate, not a tailored assessment. If your home has features that make it different from a more standard property, it is worth taking the time to sense-check the result.

Final thoughts

If your home has unusual features, renovations, or non-standard materials, it is worth giving your sum insured a bit more attention. These details can all affect rebuild cost, and they are easy to underestimate.

An online calculator can help you get started, but the final figure should still feel right for your home. If you are unsure, getting a more tailored assessment from a quantity surveyor or insurance valuation service may give you more confidence in the amount you choose.

Yes. Renovations can increase the cost to rebuild your home, especially if they involve extensions, upgraded finishes, or custom features.

What are non-standard materials in insurance terms?

These are materials or construction features that are less common and may cost more to source, replace, or rebuild.

Can a standard calculator still work for an unusual home?

Yes, it can still be a useful starting point. But if your home is more complex than average, you should review the result carefully.

Why would an architecturally designed home cost more to rebuild?

Architectural homes often include more complex design features, specialist materials, and higher-end finishes, which can increase rebuild cost.

Can site access affect the cost to rebuild?

Yes. Steep, narrow, or difficult-to-access sites can increase demolition and rebuilding costs.

Written by Toby Pudney – Initio’s Support Team Lead

Toby has been with initio since 2023 and is the Support Team Lead. He brings more than six years of experience in the insurance industry, giving him strong knowledge of general insurance. He has studied with ANZIIF and holds a qualification in New Zealand Compliance for Advisers (General Insurance Broking).

A total loss in house insurance is when a home is damaged so badly that it needs to be fully rebuilt, or partial repairs will cost more than the sum insured. In most cases, this happens after a major insured event such as a serious fire, severe flood, or natural disaster. It is the kind of event where your sum insured matters most, because that amount may affect how much is available to rebuild your home.

If you are reviewing your house cover, this is one reason it is important to make sure your sum insured is accurate.

Key takeaways in this article

A total loss means the home cannot reasonably be repaired

It usually means full rebuild or full replacement

Total loss can apply to your house, contents, or both

Your sum insured matters most in a total loss

The exact cover depends on your policy wording

What does total loss mean?

In insurance, a total loss generally means the insured property has been destroyed or damaged to the point where repairing it is no longer practical. In terms of property insurance (e.g house or landlord insurance), this usually means the house would need to be rebuilt from the ground up. For contents insurance, it usually means the belongings cannot be replaced within the sum insured and the policy amount is exhausted.

What is a total loss in house insurance?

A total loss in house insurance usually means the damage to the home is so severe that rebuilding is the only realistic option. This can happen when the house is:

left beyond practical repair after another insured event

Not every major claim is a total loss. Some homes can still be repaired, even after significant damage. The exact event is less important than the outcome. If the damage is severe enough that the property effectively needs full rebuild or replacement, it may be treated as a total loss.

Is a total loss the same as major damage?

No, not always. Major damage means the home has been seriously affected, but it may still be repairable. A total loss usually means the damage is so severe that full rebuild is needed instead.

This is an important difference, because not every large house insurance claim is treated as a total loss.

Why does sum insured matter in a total loss?

Your sum insured matters most in a total loss because it is the amount that may be available to rebuild your home, depending on the terms of your policy.

That is why your house sum insured should reflect what it would cost to rebuild your home to its current size and standard using today’s building costs.

If your sum insured is too low, it may not reflect the real rebuild cost of your home after a major loss. That is why it helps to calculate your sum insured carefully and review it over time.

Can total loss apply to contents insurance too?

Yes. A total loss can also apply to contents insurance if your belongings are damaged or destroyed to the point they need full replacement.

For example, after a major fire or flood, the claim may reach the full contents sum insured if everything inside the home is lost or badly damaged.

Does a total loss always mean the insurer pays the full amount?

Not necessarily. How a total loss is handled depends on your policy wording, your policy schedule, and the circumstances of the claim. The exact details can vary between policies and insurers.

That is why it is important to read your policy wording carefully and understand what applies to your cover.

Where can you check how total loss applies to your policy?

Your policy wording explains how your cover works, what limits apply, and how claims are assessed. Your policy schedule shows the details specific to your own policy.

Reading both together will give you the clearest picture of how total loss would be handled under your cover.

Why this matters when reviewing your insurance cover

Understanding total loss is important when reviewing any property insurance cover, whether that is house, landlord, holiday home or any other kind of property insurance. A total loss is the kind of event where your cover may be tested most heavily, so it is worth making sure the amount insured still reflects the real cost to rebuild or replace what is covered.

Final thoughts

A total loss in house insurance is when a home is damaged so badly that it needs to be fully rebuilt rather than repaired. It can also apply to contents when belongings need full replacement after a major insured event.

If you are reviewing your house insurance, it is a good time to check whether your sum insured still reflects the real cost to rebuild your home today.

A total loss in house insurance usually means the home has been damaged so badly that it needs to be fully rebuilt rather than repaired.

What is a total loss in contents insurance?

A total loss in contents insurance usually means the belongings have been destroyed or damaged to the point they need full replacement.

Is a total loss the same as a write-off?

Often, yes in general conversation. Both usually refer to damage so severe that repair is no longer practical. Generally, “write-off” is the term used when talking about vehicles.

Why does sum insured matter in a total loss?

Because in a total loss, the cost to rebuild or replace may reach the maximum amount available under your policy.

Where can I check how my policy handles total loss?

You should check your policy wording and policy schedule for the details that apply to your cover.

Does my landlord insurance cover a total loss?

Initio’s Landlord Insurance is designed to cover serious damage to the rental itself, including a total loss, on a replacement basis up to the house sum insured you select for the property, rather than just minor or partial damage.

Written by Hannah Gabbie – Initio’s Head of Support

Hannah has been with initio since 2023 and brings more than a decade of experience in fire and general claims. She joined the business as Claims Team Lead and quickly moved into the role of Head of Claims, reflecting her strong expertise and leadership in the claims space. She is a Senior Associate CIP of ANZIIF and holds a Diploma of Loss Adjusting.

As winter approaches in New Zealand, ensuring your home is ready to handle the colder months is crucial.

Not only can a well-prepared home offer more comfort, but it can also help you avoid common winter hazards, reduce your energy bills, and prevent potential damage. Here’s a practical checklist for homeowners to get their homes winter-ready.

1. Maximising home insulation and warmth

Enhancing your home’s insulation is key to staying warm and efficient during winter. Here are crucial updates to consider:

Quality curtains: Choose thermal or lined curtains to significantly reduce heat loss through windows, a common escape point for warmth.

Flooring insulation: Add rugs or carpets over hardwood or tile floors for extra warmth. Consider investing in underfloor insulation for long-term benefits.

Roof insulation: Ensure your roof insulation is sufficient and in good condition to prevent heat from escaping upwards, thereby maintaining a warmer home environment.

Draft excluders and door stops: Use draft excluders or door stops to seal gaps under doors, particularly external doors or those leading to infrequently used rooms.

Keeping doors closed: Keep doors shut to unused rooms to help contain heat in occupied areas, making heating more efficient.

Additional sealing and weatherstripping: Seal any cracks or gaps around windows and doors with weatherstripping or caulking to further prevent heat loss.

2. Fireplace safety

If you have a fireplace, ensuring it is safe and ready for use is essential:

Chimney cleaning & inspections: Have your chimney inspected and cleaned to prevent chimney fires and carbon monoxide buildup.

Keep your wood dry: Store wood in a dry, covered area to avoid moisture, which can lead to more smoke and less efficient burning.

Use a wood moisture meter: To ensure your firewood burns efficiently and safely, use a wood moisture meter. Firewood should ideally have a moisture content of less than 20%. Properly prepared wood reduces the risk of chimney fires, thereby preventing potential damage and insurance claims.

3. Smoke alarms and CO2 monitors

Smoke alarms and carbon monoxide detectors are vital year-round, but especially during winter when the use of fireplaces and heaters increases:

Test and replace batteries in all smoke alarms and carbon monoxide detectors.

Install carbon monoxide detectors near any fuel-burning appliances.

Ensure that there’s at least one smoke alarm on each level of your home, including the basement and near sleeping areas. Regularly testing and maintaining these devices can be a lifesaver, preventing catastrophic events and the associated costs and claims from fire or gas-related incidents.

4. Managing slippery decks and concrete

Slippery decks and walkways can be a hazard as frost and moisture accumulate. Here are some tips to prevent slips and falls:

Apply anti-slip coatings to decks.

Use sand or salt to improve traction on concrete paths and steps.

Regularly clear away leaves and debris, which can become slippery when wet.

These measures not only ensure safety but also help prevent accidental damage to the property, reducing the need for repairs.

5. Maintain a healthy indoor temperature

Keeping your home at a healthy temperature during winter is essential for comfort and health. The World Health Organization recommends a minimum of 18°C in living areas, with higher temperatures advisable for homes with elderly residents, children, or anyone with health issues. Consider the following to maintain a healthy indoor temperature:

Use timers on heaters to warm the house before you get up or before you return home.

Seal gaps and drafts in windows and doors to keep warm air inside.

Consider using a programmable thermostat for better temperature control.

Maintaining a proper temperature helps prevent issues like burst pipes and the structural damage caused by freezing and thawing, which are common winter insurance claims.

Additional tips

Inspect your roof: Check for any damages or leaks and repair them to prevent water damage.

Gutter cleaning: Clear your gutters and downspouts to ensure water can freely flow away from your home, preventing icicles and ice dams.

Prepare an emergency kit: Winter storms can come unexpectedly. Have an emergency kit with essentials like flashlights, batteries, water, and non-perishable food.

These proactive steps not only make your winter more comfortable but also protect your home from potential damage, reducing the likelihood of having to file an insurance claim.

Running a business from home has become increasingly common, but knowing when your home insurance is enough – and when you need to look at commercial insurance – can be tricky. Here’s what you need to know.

Initio’s home products cover your residential home and any domestic outbuildings used for residential purposes, so long as they’re within your home’s residential boundaries.

Unless agreed otherwise, your policy will usually not cover any part of the home or any outbuilding used for business or commercial purposes, other than a home office.

Does house insurance cover your home office?

If you have a room in your home or an outbuilding that you use solely as a home office for clerical purposes then your policy will cover that part of the home. This is especially true if you’re simply using a space for paperwork, meetings, or computer-based work – something that doesn’t involve much physical activity or storage of stock.

If you have home contents insurance insured with initio, your own home contents cover is also extended to include office furniture and office equipment that is used for earning income. The furniture and equipment are covered for up to $10,000 whilst at the home and for up to $1500 whilst temporarily removed within New Zealand.

When you need Commercial Insurance;

For your Home

As soon as your home business goes beyond a simple home office or consultancy work, you’ll likely need a commercial insurance solution or special terms. If you’re storing stock, using specialised equipment, or running a business that involves physical labour (even if it’s within a garage or basement), it’s likely that standard home insurance won’t be enough. When you run any business from your residence (outside of a home office) we recommend getting in touch for specific advice. Depending upon the type and extent of the business, you may require commercial insurance. An example of such, would be a wood-working business run from the garage, whereas an occupation such as beauty therapy being run from one room can potentially be included in your home policy by agreement with the insurer.

For your contents

If you use tools or equipment from home to earn income, such as a builder’s or mechanic’s tools, it’s important to know that they are not covered under your standard home contents insurance policy. Even if you use these items for personal reasons, they require commercial insurance if they’re also used for work.

A common scenario is when tools are stolen from a car or home. You make a claim, but the insurer declines it because the tools are classified as income-earning equipment. Some may assume they can claim under their employer’s commercial policy, which often provides for ’employee tools.’ However, these claims are usually subject to a much higher theft excess, typically $2500.

To avoid this, it’s best to organise your own commercial insurance for tools and contents used for business purposes. Keep in mind, commercial policies come with higher excesses. Typically, these might look like:

$500 standard excess

$1,000 burglary excess (forced entry or exit)

$2,500 theft excess (no forced entry or exit)

By getting the right cover in place, you can avoid surprises if something goes wrong.

Your liability

Our owner-occupied home policy covers your liability for activities you undertake as a homeowner and our landlord policy covers your liability for activities you undertake as a landlord or provider of short term holiday home accommodation . There is no cover provided for any liability arising from other business activities. If you own or run a business from home, you would need to arrange separate liability insurance cover through a commercial insurance provider or broker, which may include a public and products liability policy, and statutory liability policy.

Case-by-case

Ultimately, each business is different, and insurers will assess whether your business falls under home insurance or requires a commercial policy on a case-by-case basis. If you’re unsure, it’s always best to check with your insurance provider to make sure you’re properly covered.

In summary, once your business grows beyond a simple home office, it’s time to consider a commercial insurance solution to protect your assets and operations.

Burglary prevention is as equally important for holiday homeowners and landlords, as it is for one’s own personal residence. Burglary is not just about having your contents stolen; there is also the damage that thieves can cause trying to gain access to the property.

Holiday homes are particularly vulnerable as they are often left unoccupied for extended periods of time.

Landlord Insurance cover is designed to protect you when the worst happens, but as a landlord and property owner there steps that you can take to prevent having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy. Here are some tips to prevent opportunistic burglars from targeting and gaining access to your property.

Check window joinery and replace or repair any loose latches.

Consider installing security stays on windows.

Fit deadlocks / deadbolts to all external doors; especially older doors and ranch sliders which can be easier to obtain access.

Install a burglar alarm and advertise the presence of an alarm.

Install exterior sensor lights, or check that existing lights are working correctly

Don’t advertise that you are away; keep the lawns mowed and the mail box clear.

Good security makes people feel safe; it also has the added benefit of retaining good and long term tenants.

Methamphetamine contamination in a rental property can be an alarming and confusing time for property owners. There are conflicting theories on what levels are acceptable and what needs to be done to get the house livable again. Initio keeps it simple and adheres to the Ministry of Health Guidelines which state that any house reading more than 1.5mg of methamphetamine per 100 cm2 needs to be decontaminated.

If your short or long term rental property has tested positive for the presence of methamphetamine and you have house insurance with Initio, here’s what you need to do:

If you haven’t already, you need to get a detailed room-by-room test completed. This will show you which specific areas of the house are contaminated.

Log into your dashboard on the initio website and click on the make a claim button.

Fill in the form and attach your test results.

We’ll email or call you within one business day.

FAQ’s:

Does my initio landlord insurance policy cover methamphetamine contamination?

Yes; however, the cover is specific and limited to $30,000:

Where the contamination damage occurs in connection with any tenancy or occupancy of:

More than 90 days, there is no cover unless you, or the person who manages the tenancy on your behalf, have fully met the ‘landlord’s obligations’ under the ‘Policy conditions’; or

90 days or less, there is no cover unless the contamination damage was caused by an accidental incident in connection with the manufacture, distribution or storage (but only where the storage is in connection with supply or distribution) of methamphetamine at the home.

What is the excess?

All methamphetamine contamination claims have a specific excess of $2,500.

Can I start cleaning the house?

Not yet, please follow steps 1-3 above and then we’ll work together on getting the house livable again.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

Methamphetamine is not a discriminatory drug … anyone could be using or manufacturing methamphetamine in your rental property … even your tenants!

New tenancy legislation comes in effect today under the Residential Tenancies Amendment Act 2019 (RTAA). Among other things, the RTAA attempts to clarify liability for property damage between tenants and landlords.

As a specialist online landlord property insurance provider, Initio handles landlord property damage claims on a daily basis. Initio asserts the RTAA’s approach to property damage is misconstrued, creating uncertainty for both landlords and tenants.

Intention of the act

For property damage, the Residential Tenancies Amendment Act, seeks to:

Make tenants liable for ‘careless damage’ caused to the rental property; but

Allow tenants to share in and receive protection from the landlord’s insurance policy; and

Limit tenant liability for careless damage to the amount of the landlord’s insurance policy excess or 4 weeks rent (whichever is less).

Re-open the ability for the landlord to recover against the tenant for damage, albeit on a very limited basis.

Practical reality of property damage

Determining who pays for the cost, or insurance excess, of property damage is going to lead to disagreements between landlords and tenants.

“Many landlords have misunderstood the changes to the RTA and believe that the tenant will be responsible for the insurance excess on all types of claims,” said Rene Swindley, Initio CEO.

“The reality is that the tenant is only responsible for the excess on careless damage claims, which are uncommon. Over the last 12 months only 7% of our claims would be considered careless, meaning that for the remaining 93% it is the landlord who will be funding the insurance excess.”

The type of damage determines who pays

Initio has analysed its last 12 months of claims and determined that there are five broad ways a rental property can suffer damage:

Damage (g. storm damage to the roof, or a leaking pipe). These account for 55% of Initio’s rental property claims. If the landlord is insured, the landlord pays the excess.

Accidental damage by tenant(e.g. tenant slips and spills a glass of red wine on the carpet). This loss type accounts for 14% of initio claims. If insured, the landlord pays the excess for this damage.

Careless damage by tenant(e.g. tenant leaves a pot cooking on the stove and goes to bed). Only 7% of initio claims are considered careless, meaning that the tenant is rarely responsible for the excess.

Intentional damage by tenant(e.g. tenant smashes holes in a wall, meth contamination). Due to meth still dominating this damage type, 16% of initio claims are considered intentional. Landlords can obtain insurance for this type of damage. A landlord or their insurer can hold a tenant fully liable for this type of damage, but historically it is a difficult and lengthy process recovering costs (or an excess) from the tenant for intentional damage.

Damage by a third party(e.g. a third-party vehicle impacts the fence). Only 8% of initio claims fall into this category. The landlord is responsible for the excess, but the landlord’s insurer has the right to recover the excess from the third party for the benefit of the landlord.

Accidental or careless? Arguments to come

While the RTAA assumes that the landlord and tenant will agree on the damage, there are many subjective damage scenarios where this may be unclear. For example, a glass of wine dropped on the carpet or hot pot burn on the kitchen bench can be construed as either ‘careless’ or ‘accidental’. As the classification of the damage has financial implications to tenant and landlord alike, it is inevitable that disagreement will arise.

Given that the cause of the damage determines who pays, Initio expects disagreements between landlords and tenants as to responsibility. If the landlord and tenant cannot agree on the type of damage the parties can apply to the Tenancy Tribunal for the mater to be resolved.

Change of insurance excess

Initio is a digital insurer that allows landlords to make on-demand policy changes.

“As Initio’s digital insurance offering makes it so easy for landlords to change an excess our technology has become a landlord sentiment barometer,” said Initio CEO Rene Swindley.

Initio does not recommend that landlords increase excesses as a reaction to the RTAA, as the higher excess will apply to all claims, not just the rare situation in which the tenant can be held responsible for payment. Swindley says that initio is watching its ‘barometer’ with interest.

When deciding on a policy excess, landlords need to think about the insurance excess in terms of both their own and their tenants’ ability to fund and cope with the excess. Given that it is a requirement for the landlord to provide details of insurance to a tenant, it’s clear that the level of insurance excess will form part of a tenant’s decision to rent a property.

In coming weeks as real-life damage to rental properties meets the new RTA, it remains to be seen how much tension is put on the landlord-tenant relationship.

About Initio

Initio is a New Zealand based online property insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home & contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with loss of rent, and cover for damage by the tenant.

Initio’s market-leading policies can be quoted, bought and amended online – all in an instant. Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

Covering yourself for an unexpected event that leads to damage and financial loss is exactly what insurance is for. For house and contents insurance, you are most likely to think of your typical risks that might include fire, property flooding or theft of contents. However, insurance goes much further the ‘usual’ losses.

At initio we come across our fair share of unusual claims. As part of our ‘2019 in Review’ we go over our top 5 most unexpected claims – with a few honourable mentions. We are calling this the ‘Annual Initio Claims Awards’

Expect the Unexpected?

#1. Runaway Trailer

Sometimes damage can come from something outside of your control and your property. In late 2019, an initio customer in Te Awamutu was taken by surprise by a runaway trailer. Concrete was being laid at the building site next door and one the contractors loaded trailers became unhitched. The trailer was sent rolling down the hill and ended its journey by colliding the corner of our customers house and garage door.

This resulted in significant damage to the interior lining, exterior cladding and the garage door. Lucky for the insured their vehicles were not parked in the garage at the time, however a shelving unit and set of golf clubs were also destroyed. Saturday golf was put on hold unfortunately.

Total claim cost $19,187. In this instance, the concrete layers public liability insurer was pursued for the costs of this claim.

# 2. Colouring-in competition

When a customer rented their holiday home to short term guests they were not counting on their TV taking part in a kids colouring competition. The guest’s toddler thought they would hone their colouring in skills on the large flatscreen TV.

The artistic crayon drawings were cleaned off but the hard crayons left permanent scratches across the screen that could not be removed. A claim was made under their ‘landlord-holiday home contents’ which meant that the homeowner was able to replace their TV.

#3 . The Phantom Bather

An initio client with a multi-unit rental property was expecting it to be unoccupied for eleven days between tenancies. Two days into the property being untenanted, they received a call from their neighbour to say that there was water coming out of the property. It appeared an intruder had entered the property gone up the stairs and decided to run a bath.

Extensive water damage included saturated carpet upstairs that then seeped through the floor to downstairs. The ceiling in the kitchen and dining room downstairs collapsed, and significant water damage and clean-up was required through the property.

While we don’t know what the motives were for running the bath, we know that the landlord was happy to have an initio landlord insurance policy come to the rescue. With further costs still to come in the claim cost of repairs so far exceeds $32,000.

#4 . Rampant Puppies

After a tenancy had ended at an initio rental property early in 2019, an initio client lodged a claim for damage to the underfloor insulation. When repairers investigated the cause of loss, it appeared that the previous tenants family of puppies had found their way under the house, and shredded the flooring insulation from below.

Unlike many domestic insurance policies in New Zealand, the initio landlord insurance policy does not exclude damage caused by pets. After the landlord’s excess, Initio paid out $2,225.16 to repair and reinstate the insulation.

#5. Clumsy Chopping Board

While renting a holiday home, the guests popped down the road only to return to water running out the front door. They certainly didn’t expect to find water everywhere, a swelling to the kitchen, kitchen bench, cupboards, walls and floor.

It turns out that while they were out of the house a bread chopping board fell from its stand and landed on the sink tap. Not only did this turn the tap on, the awkward way it landed meant it also redirected the water away from the sink, running down the bread board and into the kitchen cabinets.

The aftermath damage resulted in water damage to the kitchen structures, damage to electrical components, and loss of rent payments as the sodden kitchen meant the property could no longer be rented. Total repairs amounted to $21,151.38 and are covered as sudden accidental water damage under the customers initio holiday home policy.

2019’s Honourable Vehicle v House Mentions

From AirBnB guests throwing a party to lightning strikes – we have had some interesting ‘honourable mentions’ lodged throughout the year.

Six claims were lodged with initio in 2019 for vehicle damage to properties – where a member of the public lost control of their vehicle and damaged our customers houses.

Three were involved in a police chase, whilst a further two were caused at the hands of drunk drivers.

Drivers who are responsible for damage caused are liable to cover the costs of repair. However in reality it’s difficult to get those responsible to accept liability (especially where it involves a police chase or drunk driving). Regardless of the driver accepting responsibility or being insured themselves (not that they would have insurance if drunk or in a police chase) initio provides cover for the damage caused to the property. We then pursue the driver.

The average claim for vehicle house damage in 2019 was $4,761.

‘Expect the Unexpected’ – You never know what could happen to your property. This is why it’s best to make sure you are covered for such unexpected and unusual events.

For more information on insuring different types see our insurance covers designed specifically for:

Home Insurance – for your own home, and contents. Holiday Home Insurance– for the bach and for holiday homes that are also rented out (eg Bookabach, AirBnB) Landlord Insurance– all in one house and landlord insurance, including loss of rents, malicious damage & more.

Christmas is the busiest time of year …. for burglars. House insurance is just one part of managing your house and contents risk. Heres a guide on protecting your property.

It’s coming into that time of year where we like to take a load off – relax for a couple of weeks, put the feet up at the bach, or even head off overseas – but it’s also the time of year when burglars tend to be more active. Leaving houses empty for periods of time can be risky in several ways, and among other factors, result in an uptick of property insurance claims. We’ve all seen Home Alone!

Holiday homes are particularly vulnerable as they are often left unoccupied for extended periods of time, but even our own homes need to stay secure and damage-free over the silly season.

Burglary prevention is equally important for holiday homeowners, landlords, and people with a single main residence. Importantly, burglary isn’t only about having your contents stolen, but also the fact that thieves can cause significant damage to other possessions and the property itself whilst trying to gain access.

Property insurance cover is designed to protect you if the worst should happen, but as a property owner there are several steps you can take to avoid having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy.

Prevent opportunistic burglars from targeting your property by:

Keeping all valuables out of sight. Gifts under the tree are tempting for thieves so make sure they, and other valuables, can’t be seen from the outside the home. Also be careful when disposing of any tell-tale packaging

Checking window joinery, and promptly replacing or repairing any loose latches

Installing security stays on windows

Fitting deadlocks or deadbolts to all external doors, especially older doors and ranch sliders which can be more easily broken into

Installing a burglar alarm and advertising the presence of an alarm

Installing exterior sensor lights, and checking any existing lights are working correctly

If possible, make it difficult for someone to break into your home. Trim trees and shrubs so there are no places for burglars to hide and move wheelie bins and other large objects away from fences, ledges and drop-offs wherever possible. Lock your shed and put away any tools, to remove the temptation of them being used to aid access.

Something else to consider is not advertising that you are away: keep your lawns mowed, gardens tidy, the mailbox clear and avoid leaving messages on social networking sites and answering machines with dates and other specific details of your absence. Let your neighbours know if you’re going to be away, give them your contact phone number, and have if you a good relationship with your neighbour – ask them to clear your mail, or park in your driveway to keep up the ruse.

Good security makes people feel safe; it also has the added benefit of retaining good and long-term tenants – and for holiday homes, a reputation for a safe and secure property.

This week, law changes to the Residential Tenancies legislation is set to strengthen renter’s rights. It aims to transition a landlord’s rental house into a tenant’s home.

Looking specifically at landlord insurance, the change that will have the most ramifications on landlord insurance is the removal of no-cause evictions.Essentially, it will be more difficult for landlord’s to remove bad tenants and from a risk management perspective this is not a good thing. Other changes to the legislation such as limiting rent increases, and banning rent bidding are unlikely to have a direct impact on landlord insurance.

Landlord insurance provides cover for intentional damage by tenants. If troublesome tenants are harder to remove then landlord insurers will consider that there is a higher risk that the tenant will cause damage to the property. It remains to be seen but this could lead to an increase in the value of deliberate damage insurance claims. Working out how and when the damage occurred could be further protracted when there is a tenant that is unwilling to co-operate and cannot be removed from the property. It has always been about working with the landlord, the tenant, and the property manager (if applicable) and this will not change when it comes to insurance.

While tenant damage could increase under the new rules, the legislation changes could in fact improve risk management and reduce the incidence of damage. Our view is that with bad tenants being hard to evict, it will mean that landlords increase their scrutiny during tenant selection. So, ultimately tenants with a poor record and lack of supporting references may find it harder to get rent a property, which would filter out bad tenants and lead to lower claims payouts for insurers.

The ultimate outcome of the law changes is difficult to predict. It is unlikely that insurers will make any adjustments to premiums or policy conditions as a result of the reforms.

The bulk of the legislative changes are set to be put into practice in early 2021. We expect that it will take at least 12 months before we see any outcomes or trends on claims.

About Initio

Initio is a New Zealand-based online house insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Having completed over 35,000 automated insurance transactions, Initio’s market-leading policies can be quoted, bought and amended online – all in an instant.

Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

For any new tenancy agreement signed after 01 July 2021 your property will legally have to comply with all five Healthy Homes Standards within the first 90 days.

To keep on top of things here’s a reminder of what the changes mean, and what’s required.

The changes

Any new or renewed tenancy (whether it’s fixed term or periodic) in effect after 01 July 2021 has just 90 days to be fully compliant with Healthy Homes. For example, if new tenants move in on 01 July, you’ll have until 01 October to make the necessary changes.

Does your rental meet the five standards?

Heating Standard

At least one built-in heater capable of heating the main living room to 18°C or more.

Some types of heaters that are unhealthy, too energy inefficient or unaffordable to run won’t meet the requirements.

Insulation Standard

Meet minimum requirements for insulation levels in ceilings and under-floors. Levels required depend on what part of the country the property is in (zone 1, 2 or 3).

Insulation installed before 01 July 2016 acceptable under 2008 standards, and

Insulation installed after 01 July 2016 acceptable under current, post 2016 thickness levels.

Learn more about the different levels for the three zones here.

Ventilation Standard

An extractor fan that vents to the outside (not another room), in all kitchens & bathrooms. They also need to meet some performance and size levels.

Open-able ventilation (like windows) to the outside in all liveable parts of the house. Size of windows is more than 5% compared to the size of the room they are in.

Drainage and Moisture Standard

Able to manage and drain normal rainfall levels. This includes working gutters, downpipes and drains for water flow.

Houses with a closed off sub-floor (area beneath flooring) need a barricade to stop water flowing in, where feasible.

Draught Standard (air-type)

Air tight with no gaps that cause noticeable airflow into the house.

Unused fireplaces are airtight, unless there’s an agreement with tenants otherwise.

What’s the penalty?

If you haven’t already, now is a great time to make a start. If you don’t comply and there’s tenants living in the property, you’re at risk of getting a penalty of up to $4,000 (per property). Anyone can claim a breach, including your tenants. If you haven’t already, the time’s now to make the changes to avoid future problems with your tenants.

Please Note: This is simply a summary of the five standards. To get the full details and piece of mind, we recommend going to the official Tenancy Services’ Guide.

A self-contained dwelling must have facilities to cook, sleep, live, wash, and use the toilet.

These facilities do not have to be in one building, but they must be for the exclusive use of that home.

Shared facilities usually mean the property is not self-contained.

Most home or landlord policies cover one self-contained dwelling only.

If your property has more than one self-contained living area, you may need separate policies.

Is your property considered self-contained?

To be self-contained a premises must contain the facilities necessary for day-to-day living on an indefinite basis. There must be somewhere:

• to cook;

• to sleep;

• to live;

• to wash; and

• to carry out ablutions.

The facilities needed to live in a self-contained manner do not have to be in one building, but must be for the exclusive use of the dwelling.

For example, a property may have an external ablutions building in the grounds. As the whole property has the facilities to enable the people using the house to live in a self-contained manner, and the facilities are not shared with other homes, this property will be self-contained for NHC (Formally EQC) cover purposes. NHC is the Natural Hazards Commission.

How this affects your insurance cover

A typical home or landlord policy is designed to cover one self-contained unit being used as a dwelling either by the owner or a long term tenant (over 90 days). If you have a second self contained area at the property also used as a home, you may need a second policy, please check out our support page here to assist with determining the correct cover for you.

A closer look at property damage for New Zealand Landlords

Rental properties, for all their promise of steady income and long-term value can, if not managed correctly, become ground zero for an array of unforeseen problems and potential hazards.

The reality is that damages, an often neglected aspect of rentals, pose a considerable risk to your investment. These risks are as varied as they are prevalent, raising a pertinent question in the minds of property owners: “What damage is most likely to occur at my rental property?”

Safeguarding your investments and mitigating potential losses, and understanding these risks is essential to success as a landlord.

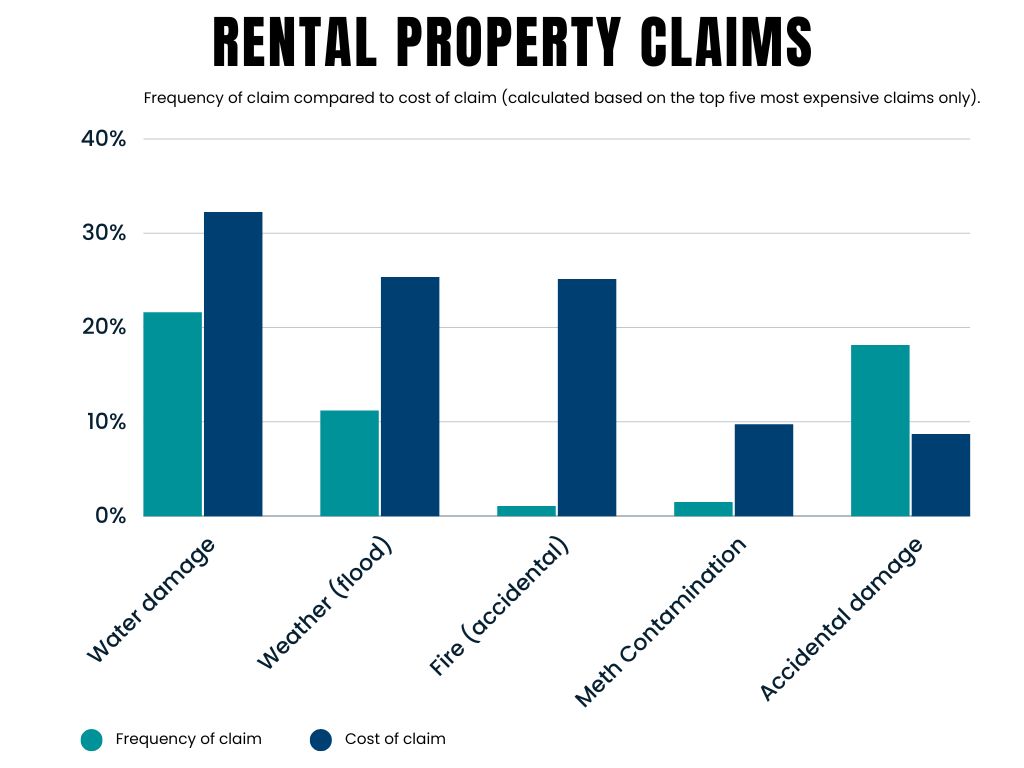

A thorough examination of our 2022 loss data provides a detailed analysis of the challenges faced by New Zealand property owners. Last year, claims related to rented properties — including traditional rental properties, own homes partially rented, and properties with multiple rentals, made up 35% of all the claims we received. When focusing on these rental-specific claims, we identified a broad spectrum of loss types, which we’ve classified below in terms of number of claims:

Water-related damage: At 21.6%, this was the most common type of damage. These losses typically involved scenarios including suddenly bursting pipes and rodent damage, while blocked pipes accounted for 6.4%.

Accidental damage: This category, representing 18.1% of the claims, includes an array of unexpected incidents, from minor mishaps to substantial accidents, illustrating the diverse risks property owners encounter. The losses range from outdoor misadventures, such as balls shattering windows or trees falling onto the property (while being pruned), to indoor accidents like stains on carpets and damaged rugs, often due to spills or pet-related incidents. There were also multiple kitchen bench damage incidents – caused by hot pots.

Weather-related damage: Severe weather events substantially contributed to the claims we received, with flood-related incidents constituting 11.2% and wind-induced damage representing 9.9% of the total claims. These statistics do not include the severe flooding and storms experienced earlier this year. Weather damage events are hard for property owners to mitigate.

Other incidents: Some more specific types of damages also occurred, albeit less frequently. These included

Malicious damage by tenants (4.6%),

Fire – accidental or unknown reasons (1.1%),

Meth contamination (1.5%),

Issues with keys and locks (3.5%),

Impact damage, typically involving a vehicle (5.5%) eg car versus house

Loss of rent: There were several circumstances that led to a loss of rental income, resulting in insurance claims. Property damage rendering the property uninhabitable was one such factor and is the most common.

However, issues such as tenant abandonment, non-payment of rent, and eviction also significantly contributed. These loss-of-rent-only situations accounted for 3.3% of the total claims made.

Frequency of claim vs. cost

The above numbers are based on frequency (i.e number of claims made). We also analysed the payout values for rental property claims. The graph below shows the top five losses by value. This data is presented alongside the frequency of each of these claims. It illustrates that losses like fire are uncommon but are high in value.

Fire-related claims constituted a mere 1.1% of the overall number of rental property claims, but made up 25% of the total value of claims paid. This underscores the potential devastation that fires can cause to rental properties. The significance of this cannot be overlooked, highlighting the importance of equipping your rental properties with smoke alarms, and fire extinguishers. By taking these simple proactive measures, you can significantly reduce the risks associated with fires and safeguard your valuable assets and your tenants.

Final word

Understanding the potential risks involved in rental property ownership can help landlords to better prepare for and protect their investments.

Proactive and pragmatic management of landlord risk is a form of insurance in its own right. In our experience, with the losses we see on a daily basis, a landlord that focuses on tenant selection, tenant vetting, regular property inspections, fire extinguishers in kitchens, regular maintenance including plumbing and electrical checks will outperform and not contribute to the statistics in this article.

Choosing an insurance provider that knows landlord insurance and who provides an insurance policy that is dedicated to the diverse needs of rental property owners is the icing on the cake for a well-rounded risk mitigation approach to landlording.

Learn more about initio’s Landlord insurance cover

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2022, spanning our entire claims portfolio. Please note that all figures are approximate and have been calculated to provide a representative view of the claim trends during this period.

No, we do not provide boat and/or marine insurance products.

Can I insure my motorcycle with initio?

No, we do not provide motorcycle insurance.

Can I change my payments from monthly to annual at renewal?

If you wish to change from monthly to annual (yearly), please take out a new annual policy from your initio dashboard and then cancel the original monthly policy. The system will also automatically arrange a refund for any unused portion of the monthly policy.

If I’m going to rent out one of the rooms in the house I live, do I need to get a landlord insurance policy?

If the boarder/tenant will be sharing facilities with you, such as kitchen and/or bathroom, then you will not need a separate policy. Our “Own Home, that’s also rented” will suit that purpose.

If the area they will be living in is self-contained (either attached to or separate from the main dwelling) with it’s own facilities, to the extent that they don’t share rooms/areas with you, then you will need to take out an additional landlord policy for that part of the property. That policy would be in addition to your Own Home policy for the portion of the home that you occupy. Together, both policies should make up the total sum insured required over the whole property.

Can I pay for one or some of my policies using a different credit card?

If you are purchasing annual insurance, you can use a different card for each and every purchase. If you are purchasing monthly insurance, we are only currently able to facilitate one card for any monthly payments under your account. If you wish to use a different card for a monthly policy, you will need to set up a new initio account using an alternative email address for any policy to be paid via the new card.

How do I login?

If you are a current policy holder already with initio you will have an initio dashboard where you can manage your insurances. You will have been emailed your login details following your first purchase with initio. Please login to your initio account here.

Your email is the first login credential required, followed by your password. If you can’t recall the email you used when you purchased your policy, please contact initio staff.

If you’ve forgotten your password, click the “Forgot my password” option to reset it. Simply follow the instructions to complete the process.

Please note that logins are only provided upon purchase of a home policy with initio.

Where do I find my renewal invoice to pay?

We don’t send invoices for the upcoming year in the traditional sense, if you are looking for the cost to renew your annual policy for the upcoming year, you can find that information by using the “review & confirm” button on the relevant policy. More information regarding that can be found here.

Once the renewal has been completed and paid, the paid invoice information is immediately emailed to you and is thereafter available on your initio dashboard for viewing. All of your historical Invoices/Receipts will remain available via your initio dashboard.

How do I determine the amount of replacement cover to take for my home? Does the amount of replacement cover includes demolition costs?

To insure a rental property set up as one self contained dwelling that you lease to tenants on a long term residential lease, please use our Landlord policy. We also have a multi-unit landlord cover for small blocks of flats or if you own more than one connected rental unit.

If I hire a car, does my vehicle policy insure the hired car?

No, your initio policy does not cover the hire vehicle, we recommend arranging cover with the hire company.

Getting the right house insurance is an important decision you want to get right. Here’s the top 4 mistakes we see, so you don’t make them.

1. Reducing your sum insured to save on your premium

People often think to reduce their sum insured for a lower premium. Insuring something for less than what it’s worth is called ‘under-insurance’.

This is a risky move where you’re banking that you won’t have major damage to your house that costs more than your sum insured to repair.

The idea of insurance is to put you in the same position you were in before the damage. If a fire fully burns down your house and you’re not fully insured, you could easily face being thousands (if not, hundreds of thousands!) of dollars short when you want to rebuild.

You will notice the effect of decreasing (or increasing) your sum insured actually has a relatively small affect on the premium. So you’re best off fully insuring your house, as it might only cost around $50 more to do.

2. Not thinking about an accurate sum insured

People often expect their insurer to know how much their house should be insured for. The reality is that you will need to come up with an approve a replacement cost estimate for your house.

Our quote calculator will give you a ‘base’ replacement sum insured from a fixed amount of rebuild cost we apply per square metre. You’ll then need to fine-tune this figure to one you think is enough to fully rebuild your house.

If you’re not sure there’s some useful tools available to help. The Cordell Sum Sure Calculator uses council data on houses to give you an estimate, and works for most house across New Zealand.

One of the most common mistakes people make is not considering all the factors in the sum insured figure. The most common being demolition costs, which can be significant. You should also take in account value of outbuildings and other things like fences, retaining walls or swimming pools. Lastly, it’s a good idea to allow for the affect of building cost inflation on top of this.

3. Not choosing the right excess

People can be caught out by selecting excesses that are either too high, and low.

Sometimes we see people select a higher excess like one over $1,000, but then when they make a claim find it’s too high and they struggle to afford to pay it. When selecting your excess ask yourself: “how much money can I comfortably afford to stump up if something goes wrong?”. If the answer is less than $1,000, you should pick an excess below this.

There are also people that tend to select excesses that are too low. If you keep enough cash on the sidelines and you don’t claim for smaller losses, you can take a higher excess to save on your premium. If you wouldn’t bother claiming for anything less than $1,000; you shouldn’t spend your money insuring it.

4. Choosing the cheapest or most expensive policy

Cheap doesn’t always mean the best value for money. Generally cheaper policies tend to have lower levels of cover. But this isn’t always the case, so it’s important you do the work to compare cover between insurers with the premium you’re paying to see where the best value is.

By the same token the most expensive policy doesn’t necessarily mean the best cover for your needs. You could be paying extra for cover you don’t need. Do you need extra cover with a higher limit for swimming pools if you don’t have one?

Taking the time to find a suitable policy could save you hundreds.

There needs to be an inspection done every three months and in between tenancies to meet our landlord obligations under our landlord insurance policy. This can be done yourself or by the person who manages your tenancy (e.g. property manager). The inspection will need to confirm the interior and exterior condition of the property and you need to keep a record of the results.

These landlord obligations and inspections only need to be met if you are making a tenancy-related claim. These include tenant damage, meth contamination and loss of rent after a tenant is evicted or leaves.

If you don’t fully complete your inspections it won’t void your policy. The cover for non-tenancy claims like floods and sudden water damage are still covered.

At initio, we require an agent or a trusted representative physically present at the property for inspections. This ensures a thorough evaluation of the property’s condition and facilitates real-time reporting, serving as your on-the-ground resource. Advantages of having an in-person representative include:

Real-time condition verification and data reporting during the inspection process.

Being your dedicated eyes and ears on the ground, diligently checking the property’s condition.

Early identification of any potential issues, damages, or repairs that could potentially be missed in a purely remote inspection.

However, we understand there may be special circumstances such as illness or lockdowns where remote inspections become necessary. These should be exceptions rather than the norm. In such cases, a trusted representative or official agent’s physical presence during the inspection is critical to maintain the assessment’s accuracy and comprehensiveness.

Looking ahead, we’re mindful of emerging technologies that could potentially streamline remote inspections. However, as of now, the value of in-person inspections is paramount. Always remember that our advice serves as a guideline, not an inflexible rule. Each property and situation may require a different approach, and decisions should be tailored to your specific circumstances and needs.

What happens if I can’t inspect my property every three months due to illness?

Initio’s landlord guidance is that you, or someone on your behalf, should carry out an internal and external inspection at least every three months, and also between tenancies. These inspections are an important part of meeting landlord obligations for tenancy-related claims, such as tenant damage, meth contamination, or loss of rent after eviction.