Search results for: {search_term_string}/house-flip-insurance/page/8/house-insurance-calculator/house-insurance

Liability cover in house and contents insurance protects you if you are legally responsible for accidentally injuring someone or damaging their property. In New Zealand, house insurance is not just about covering fire, natural disasters, or theft. The liability section can help pay legal costs and compensation if a claim is made against you. Understanding how liability cover works, what it includes, and when it applies can help you avoid significant out-of-pocket expenses.

Key takeaways in this article:

-

Liability cover in house and contents insurance protects you if you are legally responsible for accidental injury or property damage.

-

It can cover compensation payments and legal defence costs if a claim is made against you.

-

Cover can apply at your home and, in some situations, anywhere in New Zealand.

-

ACC covers medical treatment for injuries, but liability insurance may respond to other related claims.

-

Liability cover is automatically included in initio house and contents insurance policies.

What is liability cover in home insurance?

Liability insurance covers legal costs and compensation if you are legally liable for unintentional damage to another person’s property or for injuries they sustain due to your actions or negligence. It typically includes:

- Personal liability: If someone is injured at your home and you are responsible.

- Property damage liability: If you accidentally damage someone else’s property.

- Legal defence costs: If a claim is made against you, your policy may also cover legal expenses.

When might you need liability cover? Here are some common scenarios:

1. A visitor is injured on your property

If a guest trips over a loose step, slips on a wet floor, or is injured by a falling object in your home, they may seek compensation from you. The New Zealand ACC scheme typically covers injury-related costs, but it has gaps, such as claims for pain and suffering, property damage (e.g., clothing or personal items), and mental injury. In these cases, your home insurance liability cover may help with costs and legal fees if legal action is taken.

2. Your tree falls on a neighbour’s property

New Zealand’s strong winds and storms can cause trees to fall. If a tree from your property damages your neighbour’s home, car, or fence, you could be held responsible if you failed to take reasonable care.

3. Your kids or pets cause damage

If your child accidentally kicks a ball through a neighbour’s window or your dog escapes and damages someone else’s garden, liability cover can help pay for repairs or compensation.

4. You run into a vehicle while riding your bicycle

If you cause damage to other vehicles or property whilst navigating the streets on your bike, liability cover will cover those costs.

5. Water damage to a neighbour’s property

If a plumbing issue in your home causes water to leak into the adjoining unit or property, damaging walls, floors, or belongings, you may be liable for the cost of repairs.

6. You accidentally cause a fire that spreads

Fires can quickly get out of control, whether from a kitchen accident, an unattended candle, or a backyard BBQ. If a fire originating from your home spreads to neighbouring properties – damaging fences, homes, or belongings – you could be held responsible. If a neighbour makes a claim against you for repair costs or compensation, your liability cover may help cover the expenses, especially if negligence is a factor.

7. You accidentally cause damage while staying elsewhere

You’re visiting a friend’s house, and you accidentally knock over an expensive vase or damage a piece of furniture. Or, while browsing in a shop, you accidentally break a fragile item. You might be charged for the damage, but your liability cover may help cover the cost.

What’s typically not covered under the Home/Contents liability section?

While liability insurance provides broad protection, there are exclusions, such as:

- Intentional damage: If you deliberately cause damage, you won’t be covered.

- Business-related liability: If the incident occurs as part of a business activity, you would need separate business liability insurance.

- Liability due to unlawful activities: Any damage or injury resulting from illegal activities is not covered.

- Liability due to operating a motor vehicle (is covered under the vehicle’s insurance)

Conclusion

The liability section of a home insurance policy in New Zealand is crucial for protecting you from unexpected legal and financial consequences. Whether it’s accidental property damage, injury that falls outside ACC cover, or an unforeseen incident, this cover ensures you won’t face costly legal battles or compensation claims out of pocket.

All initio products automatically include liability protection.

You might also be interested in:

House insurance protects you financially when the unexpected happens to your home, like a fire, flood, or sudden water damage. Without it, you’d need to pay the full cost of repairs or rebuilding yourself, which can be extremely expensive.

Most New Zealand homes are worth hundreds of thousands of dollars. Rebuilding or repairing after a disaster is not something most homeowners can afford out of pocket, and these expenses often come without warning.

That’s why it’s important to set the right sum insured – the maximum amount your insurance will pay to rebuild your home. You can learn more about how to work this out in our guide to calculating your sum insured.

Tempted to skip it to save money?

In tough financial times, it can be tempting to look for areas to cut back, and insurance can feel like an easy one to drop, especially if you haven’t made a claim in years. But it’s worth asking yourself:

If disaster struck tomorrow, could you afford to recover without insurance?

A single fire or flood can destroy years of financial progress. Even minor repairs can cost tens of thousands, and that’s before factoring in things like temporary accommodation. When you don’t have cover, you’re gambling with your biggest asset.

When you pay for insurance, you’re not just buying cover, you’re paying a provider to take on the financial risk for you, so you’re not left to carry it alone if something goes wrong.

Insurance isn’t about being pessimistic; it’s about being prepared.

You can reduce your premium without losing cover

If you’re looking for ways to keep your costs down, one of the most effective options is to increase your excess. This is the amount you agree to pay if you make a claim.

By choosing a higher excess, you’re taking on a bit more risk upfront, but it usually means you’ll pay a lower premium year to year. It’s a good option for homeowners who:

- Want to keep their cover but lower their premium

- Haven’t made a claim in a while

- Could comfortably pay a higher excess in the rare event they do need to claim

At initio, our quick quoting tool makes it easy to adjust your excess when you get a quote, so you stay protected, without paying more than you need to.

Insurance is about protecting what matters most

Your home is likely your most valuable asset. House insurance is designed to shield it from things you can’t plan for: fires, floods, storms, and earthquakes.

With initio, you’re covered for sudden and accidental damage, and you can lodge a claim online in minutes. It’s fast, flexible protection, backed by real people.

The bottom line: why you need house insurance

- Because disasters can happen to anyone at any time

- Because the cost to rebuild or repair is high

- Because insurance offers security when you need it most

- Because there are smart ways to stay covered without overspending

Still thinking it through? Get a quote online in minutes, or learn more about what our house insurance covers

Get a quote

Related articles:

Digitally savvy, human touch; The heart of initio

Since 2011 we have been redefining insurance. We are creating an insurance experience that customers love! At initio, we are all about creating better digital experiences for buying and managing insurance exclusively online. We’re best known for being the first insurance provider in New Zealand to quote and bind an insurance policy online. We consider ourselves to be the challenger brand to the domestic insurance market in New Zealand and as such we are on a mission to redefine the way insurance is managed and delivered to customers digitally.

At initio, we’re not just hiring; we’re on the lookout for thinkers, creators, and lively souls eager to influence the next chapter of insurance for our clients. If you’re brimming with creativity and ready to make an impact, you’re in good company.

Award-Winning Workplace

Yes, you read it right; we’ve got a brand-new accolade. initio has been named one of the Best Insurance Companies to Work for in Australia and New Zealand in 2023! If you want to be part of a company that’s officially recognised as a brilliant place to work, one that truly looks after its staff, then look no further. Come join our award-winning team and let’s transform those brilliant ideas into something that shines even brighter.

Open Positions

Here’s a sneak peek at our roles currently on offer. Can’t find the perfect role just yet? Keep swinging by – new opportunities land faster than you can say “Cheeseburger Fridays.”

Whether you’re considering becoming a landlord for the first time or looking to optimise your rental process, this guide covers some of the key aspects you need to know.

Key takeaways in this article:

-

Being a landlord comes with legal responsibilities.

-

Make sure your property meets Healthy Homes Standards.

-

Decide early between long-term or short-term renting.

-

Set rent based on local market research.

-

Screen tenants carefully and keep good records.

-

Standard home insurance does not cover rental risks.

-

Regular inspections and maintenance help avoid bigger costs.

-

Rental income is taxable, so check your obligations.

Renting out your home in New Zealand can be a great way to generate extra income, but it comes with responsibilities and risks.

Before you rent out your home

Get the right advice early

- Refer to Tenancy Services for the latest landlord specific advice such as healthy homes and legal requirements

- You may also want to join your local property investor association for support and advice – New Zealand Property Investors Association have various branches throughout New Zealand.

- Consider whether a professional property manager is right for you.

- Services like myRent can help with advertising, tenant management, and documentation.

Understand Healthy Homes requirements

Landlords must ensure their rental meets Healthy Homes Standards. This includes heating, insulation, ventilation, moisture control, and draught stopping.

Know your legal obligations

Under the Residential Tenancies Act, landlords must:

-

Keep the property in a reasonable state of repair

-

Lodge the bond with Tenancy Services

-

Provide proper notice for rent increases

-

Keep accurate records of agreements, inspections, and payments

Choosing the right strategy

Long-term rentals

Long-term rentals provide steady income and greater stability. They generally involve less turnover but require ongoing property management.

Short-term and holiday rentals

Short-term rentals, such as Airbnb, can earn more during peak seasons. However, they require more active management, cleaning, and compliance with council rules.

They also require commercial insurance, which can cost more than standard landlord cover.

Insurance differences to consider

Landlord insurance is designed to protect against tenant damage, loss of rent, and liability claims. Always check policy conditions, including inspection and tenant screening requirements.

Setting up your rental property

Set the right rent price

Research similar properties in your area to set a competitive rental price. Consider:

- Location and amenities

- Property size and condition

- Market demand

- Seasonal fluctuations

Websites like Trade Me Property and Tenancy Services can help you gauge market rents in your area.

Advertising your property

Advertise on platforms such as Trade Me Property, Facebook Marketplace, or use a property manager to find suitable tenants.

Screening tenants

Carry out proper checks before accepting a tenant. This may include:

Use Tenancy Services templates or services like myRent to ensure all legal terms are covered.

Protecting your investment

Why landlord insurance matters

Landlord insurance protects you from risks specific to renting, including malicious damage, loss of rent, and liability.

What standard home insurance does not cover

Home insurance is designed for owner-occupied properties, where the owner lives in the home. It is priced and structured around that lower risk profile. Once a property is rented out, the risk changes. There is less control over how the home is used, and there are additional exposures such as tenant damage, loss of rent, and liability issues.

Because of this, standard home insurance will not cover many rental-related risks. If your property is tenanted, you should have a landlord policy that is specifically designed for rental situations.

Your obligations under a landlord policy

Most landlord policies require reasonable tenant screening and regular inspections. Failing to meet these obligations can affect a claim.

Managing your property day to day

Routine inspections

Regular inspections help you identify issues early. Tenancy Services provides inspection checklists to guide you. myRent also have great resources in that regard.

Maintenance and repairs

Respond promptly to maintenance requests and budget for ongoing upkeep to avoid larger repair costs later.

Tracking rent payments

Use a clear system to track rent payments and maintain accurate financial records. Property management tools like myRent can assist with this.

Ending a tenancy correctly

Tenancy agreements

Ensure tenants sign a legally binding Residential Tenancy Agreement outlining rent, bond, and house rules.

Notice periods and bond refunds

When ending a tenancy, follow the correct notice periods and manage bond refunds according to legal requirements.

Understanding tax responsibilities

Rental income is taxable in New Zealand. You may also be able to claim expenses such as:

- Property management fees

- Mortgage interest (if applicable)

- Repairs and maintenance

- Insurance and rates

Check with an accountant or Inland Revenue (IRD) for guidance on tax obligations.

Final thoughts

Renting out your home can be financially rewarding, but success depends on understanding your legal duties, choosing the right rental strategy, and arranging proper landlord insurance. Taking time to plan now can help you avoid costly mistakes later.

If you’re considering renting your property, take the time to research and seek professional advice where needed to avoid common pitfalls.

You might also be interested in:

NZPIF and Initio have teamed up to provide Members with an extensive insurance offering that is specifically designed for rental properties. It covers the property itself and landlord risks

As a member of NZPIF you receive discounted pricing. Complete the property details below to get a quick quote. You can start the cover online with payment by credit card or bank transfer. The policy confirmation will be instantly emailed to you. It’s easy, which is the same approach Initio takes to claims.

As a landlord, the risks to which you are exposed are often not covered by a standard insurance policy. When taking this next step on the property ladder it is important to have the right Landlord Insurance cover in place to save yourself from headaches down the track.

Does your policy cover your tenanted house? While it seems obvious, a standard house insurance policy is designed to cover owner occupied homes, if you were to make a claim and the insurer discovered the house was tenanted your claim could be declined. If you have listed your holiday home for rent or if you have recently moved out of your own home and tenants have moved in, make sure you have notified your insurance provider, and they have the correct Landlord Insurance cover in place.

Does your policy cover loss of rents? Following a claim for property damage to your house, there will likely be a period where it is uninhabitable while you wait for the repairs to be carried out and completed. You are going to want your Landlord Insurance to pay for your lost rental income during this time. Make sure that the policy will pay out for at least 12 months, and that the limit is large enough to cover the week rent – ie $20,000 over 12 months is up to $385 per week.

Does your policy include cover the carpets? House insurance policies often only cover floor coverings that are glued to the floor, while most carpet is tacked. Therefore, it is important that your Landlord Insurance policy includes cover for your contents. Make sure this amount is enough (we recommend at least $20,000) to cover your appliances, carpets, drapes, blinds and other furniture that remains in the house while it is tenanted.

Does your policy include damage caused by your tenants? Generally, your insurance policy will exclude deliberate damage caused by a person living at the house, so if your tenants intentionally damage your house you may not be covered. A good Landlord Insurance policy will include cover for malicious or deliberate damage by tenants.

Does your policy continue if your house is vacant? Some policies will cease cover if the house is vacant. So, if it takes longer than expected to tenant your house, or if you have no bookings at your holiday home over the winter, you might not have any insurance cover. Look for a Landlord Insurance policy that will continue to provide cover even while the house is unoccupied.

If your tenants are holding the keys to your retirement savings, you don’t want to leave anything to chance. The initio policy was designed specifically for rental houses and holiday homes, so you can rest easy knowing that one of your largest assets is in safe hands. To get a quote visit initio.co.nz.

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: |

Initio Limited |

| FSP Number: |

FSP523166 |

| Website: |

www.initio.co.nz |

| Phone: |

0800 763 929 |

| Email: |

[email protected] |

| Address: |

6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: |

Suzanne (Suze) Ferry |

| FSP Number: |

FSP566306 |

| Contact Email: |

[email protected] |

| Qualifications: |

New Zealand Certificate in Financial Services (Level 5) |

| Experience: |

26 years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type |

Commission Rate |

| House and contents insurance |

22.5% of insurer premium portion |

| Motor vehicle insurance |

10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.

- Commission income: Initio receives commission from IAG on policies sold through us. This could create an incentive to recommend insurance cover that may not be in your best interests.

- Referral payments: We may pay commissions to partners and brokers who refer clients to us, which could influence the recommendations made to you by those third parties.

- Ownership Interest: Suze Ferry holds a shareholding interest in Initio. This means that Suze Ferry has a financial interest in the commercial success of Initio, including through the sale of Initio insurance products. This ownership interest could be perceived as creating an incentive for this adviser to recommend Initio products, or recommend a higher level of cover, in circumstances where that may not be in your best interests.

How We Manage These Conflicts

Initio manages these conflicts of interest in the following ways:

- Our financial advisers are paid a salary only and do not receive any commission, bonus, or incentive linked to the sale of policies or claims outcomes.

- We require all financial advisers to follow an advice process that ensures recommendations are based on your goals, circumstances, and needs.

- Where your needs fall outside the scope of our products, we will refer you to a specialist insurer or broker rather than recommend an unsuitable product.

- All financial advisers undergo training on how to manage and disclose conflicts of interest.

7. Reliability Events

A reliability event is something that might influence your decision about whether to seek or act on our financial advice. Examples include a successful regulatory action, a bankruptcy, a criminal conviction for dishonesty, or a prohibition order by a regulatory body.

Neither Initio, nor Suze Ferry, has been subject to a reliability event.

8. What to Do If Something Goes Wrong

Internal Complaints Process

If you are not satisfied with our financial advice service, we encourage you to contact us as soon as possible so that we can try to resolve your concern. You can make a complaint by:

- Email: [email protected]

- Phone: 0800 763 929

- Post: The Complaints Manager, PO Box 319, Hamilton 3204

When we receive a complaint, we will consider your concerns and let you know how we intend to resolve them. Where possible, we will try to resolve your complaint immediately. If we are unable to do so, we will acknowledge your complaint within 2 business days and work with you towards a resolution.

External Dispute Resolution

If you are not satisfied with the resolution of your complaint under our internal complaints process, you can refer the matter to our external dispute resolution scheme. This is a free and independent service.

Initio is a member of the Insurance & Financial Services Ombudsman Scheme (IFSO Scheme).

| Scheme: |

Insurance & Financial Services Ombudsman Scheme (IFSO) |

| Phone: |

0800 888 202 |

| Email: |

[email protected] |

| Website: |

www.ifso.nz |

| Post: |

PO Box 10-845, Wellington 6143 |

9. Privacy

We collect and use your personal information to provide you with financial advice and to arrange and administer your insurance policies. Your personal information is handled in accordance with the Privacy Act 2020 and our Privacy Policy, which is available on our website.

For more information about how we collect, use, store, and disclose your personal information, please refer to our Privacy Policy at https://initio.co.nz/privacy-policy/.

10. Further Information

You can check that Initio is a registered and licensed financial service provider, and verify the registration of your financial adviser, at the Financial Service Providers Register: www.fspr.govt.nz.

This Disclosure Statement is current as at the effective date shown. We will provide you with an updated disclosure statement if there is a material change to the information contained in it.

This information is also available in writing, on request.

This disclosure statement was prepared on: 15th March 2021

This disclosure statement was updated on: 31st March 2026

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: |

Initio Limited |

| FSP Number: |

FSP523166 |

| Website: |

www.initio.co.nz |

| Phone: |

0800 763 929 |

| Email: |

[email protected] |

| Address: |

6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: |

Rene Swindley |

| FSP Number: |

FSP122087 |

| Contact Email: |

[email protected] |

| Qualifications: |

New Zealand Certificate in Financial Services (Level 5) |

| Experience: |

20 years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor Vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type |

Commission Rate |

| House and contents insurance |

22.5% of insurer premium portion |

| Motor vehicle insurance |

10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.

- Commission income: Initio receives commission from IAG on policies sold through us. This could create an incentive to recommend insurance cover that may not be in your best interests.

- Referral payments: We may pay commissions to partners and brokers who refer clients to us, which could influence the recommendations made to you by those third parties.

- Ownership Interest: Rene Swindley holds a shareholding interest and directorship in Initio. This means that Rene Swindley has a financial interest in the commercial success of Initio, including through the sale of Initio insurance products. This ownership interest could be perceived as creating an incentive for this adviser to recommend Initio products, or recommend a higher level of cover, in circumstances where that may not be in your best interests.

How We Manage These Conflicts

Initio manages these conflicts of interest in the following ways:

- Our financial advisers are paid a salary only and do not receive any commission, bonus, or incentive linked to the sale of policies or claims outcomes.

- We require all financial advisers to follow an advice process that ensures recommendations are based on your goals, circumstances, and needs.

- Where your needs fall outside the scope of our products, we will refer you to a specialist insurer or broker rather than recommend an unsuitable product.

- All financial advisers undergo training on how to manage and disclose conflicts of interest.

7. Reliability Events

A reliability event is something that might influence your decision about whether to seek or act on our financial advice. Examples include a successful regulatory action, a bankruptcy, a criminal conviction for dishonesty, or a prohibition order by a regulatory body.

Neither Initio, nor Rene Swindley, has been subject to a reliability event.

8. What to Do If Something Goes Wrong

Internal Complaints Process

If you are not satisfied with our financial advice service, we encourage you to contact us as soon as possible so that we can try to resolve your concern. You can make a complaint by:

- Email: [email protected]

- Phone: 0800 763 929

- Post: The Complaints Manager, PO Box 319, Hamilton 3204

When we receive a complaint, we will consider your concerns and let you know how we intend to resolve them. Where possible, we will try to resolve your complaint immediately. If we are unable to do so, we will acknowledge your complaint within 2 business days and work with you towards a resolution.

External Dispute Resolution

If you are not satisfied with the resolution of your complaint under our internal complaints process, you can refer the matter to our external dispute resolution scheme. This is a free and independent service.

Initio is a member of the Insurance & Financial Services Ombudsman Scheme (IFSO Scheme).

| Scheme: |

Insurance & Financial Services Ombudsman Scheme (IFSO) |

| Phone: |

0800 888 202 |

| Email: |

[email protected] |

| Website: |

www.ifso.nz |

| Post: |

PO Box 10-845, Wellington 6143 |

9. Privacy

We collect and use your personal information to provide you with financial advice and to arrange and administer your insurance policies. Your personal information is handled in accordance with the Privacy Act 2020 and our Privacy Policy, which is available on our website.

For more information about how we collect, use, store, and disclose your personal information, please refer to our Privacy Policy at https://initio.co.nz/privacy-policy/.

10. Further Information

You can check that Initio is a registered and licensed financial service provider, and verify the registration of your financial adviser, at the Financial Service Providers Register: www.fspr.govt.nz.

This Disclosure Statement is current as at the effective date shown. We will provide you with an updated disclosure statement if there is a material change to the information contained in it.

This information is also available in writing, on request.

This disclosure statement was prepared on: 15th March 2021

This disclosure statement was updated on: 31st March 2026

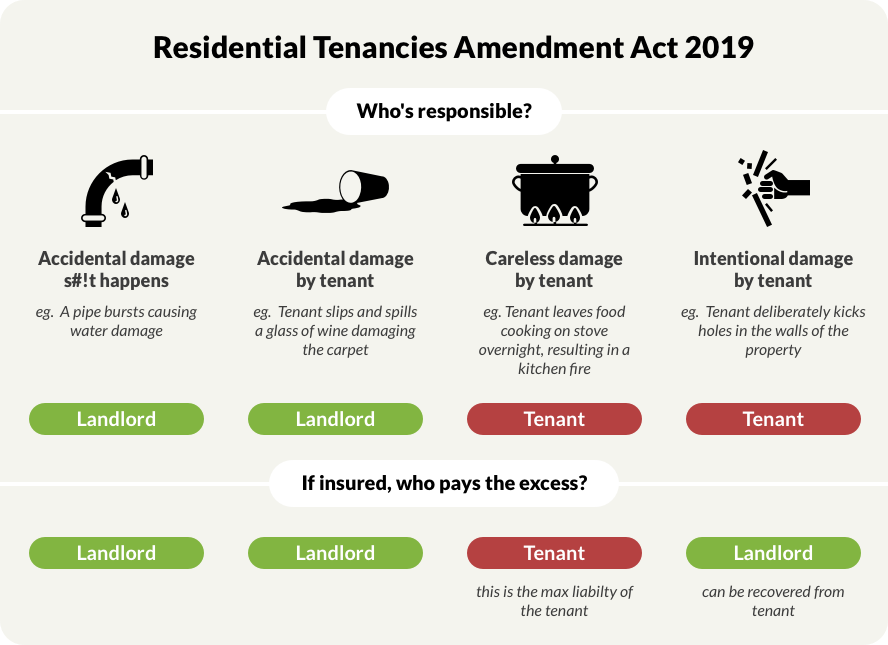

On 30th of July 2019 changes to the legislation around tenant damage and meth contamination were passed into law.

The Residential Tenancies Amendment Act 2019 will:

- limit tenants’ liability for careless damage in rental properties to the landlord’s insurance policy excess or 4 weeks rent (whichever is less)

- re-open the ability for the landlord to recover against the tenant for damage, albeit on a very limited basis

- allow tenants to share in and receive protection from the landlord’s insurance policy

- mean that landlords must provide confirmation of insurance cover to all new tenancies and their exisiting tenants on request

- prevent insurers from pursuing tenants for unintentional damage (ie careless or accidental damage)

- allow for regulations to be made to address how contamination (eg. meth) of rental properties is tested and managed

- give the Tenancy Tribunal full jurisdiction over cases concerning premises that are unlawful for residential purposes, such as garages and sleep-outs, which don’t meet minimum requirements for renting

- protect tenants living in those unlawful premises, as the Residential Tenancies Act will now apply

- give Tenancy Services the ability to take enforcement action against landlords who rent properties which don’t meet minimum standards

These changes are scheduled to take effect on 27 August 2019. The provisions of this new Act only apply to damage occurring after this date.

So, I’m a landlord, how do these changes affect me and my insurance?

It depends on how the damage has been caused. There are four ways a rental property can suffer damage:

Accidental Damage – S#!t Happens eg. storm damage

Accidental damage is damage that can’t be avoided, because sometimes s#!t happens. This could be caused by an ‘act of god’ type loss such as a storm causing damage to the roof of the property. Or it could be a leaking water pipe or an electrical fire. This type of damage is completely outside of the control of the tenant liability, and as such they have no liability for this damage. The landlord is responsible for this damage, and will usually have insurance to pay the claim.

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Accidental Damage by Tenant eg. spilling a glass of red wine on the carpet

Accidental damage can also be caused by a third party, such as a tenant. This could come in the form of a tenant tripping and spilling wine on the carpet, or their washing machine flooding. In both cases these are technically outside of the control of the tenant and there is no liability on the part of the tenant. So even if the tenant causes the accidental damage, the tenant has NO liability. The tenant can rely on the landlord’s insurance policy the repair the damage, and the tenant cannot be made to pay the insurance excess (or 4 weeks rent).

- Who is responsible for the cost of the damage? answer: the landlord (ie. their insurer)

- Who pays the insurance excess? answer: the landlord

Careless Damage by Tenant – eg. leaving a pot cooking on the stove and going to bed

Where a tenant (or their guest) carelessly causes property damage to the home, they are liable for those damages. This could be where the tenant leaves a pot cooking after going to bed and causes fire damage to the kitchen. While the amendment to the act now makes the tenant liable, the maximum amount the tenant can be held responsible for is the landlord insurance policy excess, or 4 weeks rent (whichever is lesser). The new Act effectively allows the tenant to share in and receive the benefit of the insurance arranged by the landlord.

- Who is responsible for the cost of the damage? answer: the tenant (but its capped at the lessor of the landlords insurance excess or 4 weeks rents)

- Who pays the insurance excess? answer: the tenant (see pain points below)

Intentional damage by Tenant – eg. smashing holes in the wall

A tenant is not excused from liability when the damage is intentional or where the damage they (or their guest) have caused constitutes an imprisonable offence. In such circumstances the responsibility is on the tenant to notify the landlord of the damage. The landlord can request that the tenant repair the damage, but if the landlord is properly insured (ie has an initio landlord insurance policy) they will be covered for intentional damage so its best to lodge a claim for the damage, and allow the insurer to pursue the tenant for the cost of repairs.

- Who is responsible for the cost of the damage? answer: the tenant

- Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the incurred to repair the damage)

What about Methamphetamine Contamination?

The Act allows landlords the right to enter the rental property (after providing notice to the tenant) to sample and test for meth contamination. If testing confirms that the property is contaminated to unsafe levels (currently higher than 1.5 μg per100 cm2) then the landlord, and the tenant, have rights to terminate the tenancy. The landlord can terminate with a minimum notice period of 7 days, whereas the tenant can terminate with only 2 days notice.

Meth testing must be done in accordance with the Standards New Zealand standard, and the landlord must notify the tenant within 7 days of receiving the test results.

If a landlord knowingly rents a property with meth contamination, the tenant can be awarded damages of up to $4,000.

We are still awaiting further details around this and exactly what standard will be set by the Housing Minister. Currently the NZ Standard, which the insurance industry follows says that a property is contaminated if the presence of meth exceeds 1.5 μg/100 cm2, however the Gluckman Report, which the tenancy tribunal follows says that a property is contaminated if it is more than 15 μg/100 cm2. We are expecting that the amendment to the Residential Tenancies Act will provide some consistency and that we will all move to 15 μg/100 cm2 as being the level where contamination occurs.

Given that the possession of meth can attract a penalty of up to 6 months imprisonment, and manufacture of meth a maximum penalty of life imprisonment, if use/possession or manufacture is proven at the property the tenant is NOT excused from liability and has NO protection from the landlords insurance policy. The landlord or their insurer can recover the cost of cleanup and repair from the tenant.

Who is responsible for the cost of the damage? answer: the tenant

Who pays the insurance excess? answer: the landlord (but the insurer will attempt to recover the value of the excess from the tenant along with the costs the insurer incurs to remediate the property)

Important: The likelihood of recovering costs from a tenant for meth damage is extremely low. Firstly proving it was the tenant is difficult, and secondly meth addicts generally don’t have the financial resources to pay for such large repairs.

Where are the pain points with these changes?

Accidental vs Careless

As accidental damage means that the landlord pays the excess, and careless damage means that the tenants pays the excess, we expect to see disagreements between landlords and tenants about the cause of the damage. If the landlord and tenant cannot agree whether the tenant is liable for the damage, the landlord can apply to the Tenancy Tribunal for the matter to be resolved. Copies of relevant insurance policies, photos of the damage, and receipts or quotes for repair should be included to support the application.

Is meth contamination careless or intentional?

We believe it is intentional but fortunately the new Act catches meth under the category of imprisonable offence. We anticipate that tenants (and maybe the courts) will continue to argue that the resulting damage from smoking meth is careless not intentional. Our opinion is that there is now enough information in the public domain for people to understand that meth causes property damage.

A tenant has carelessly damaged my property, I’ll leave the tenant to pay the excess to the insurer/repairer?

If you establish that the tenant has been careless this won’t mean that its a slam dunk on the tenant physically paying the excess.

We foresee there will be arguments over who physically pays the excess to the insurer or the repairer. Is it the insurer or is it landlord? Given that the policy owner is the landlord this suggests that the landlord would need to pay the excess and then recover it from their tenant. This may change in time as the new Act is tested with real loss scenarios.

We recommend that as soon as the landlord becomes aware of, and can establish that “careless damage” has occurred, that they hold their tenant responsible for the excess and request immediate payment.

What do I need to do?

You will need to provide a confirmation of insurance certificate to your tenant

Landlords are now required to provide all new tenants, and existing tenants where they request it, details of their property insurance. Any changes made to your insurance, also need to be notified to your tenants. Failure to do so could result in a $500 fine to be paid to the tenants. You can provide the tenant with a standard certificate of insurance but this will have more information on it than you are required to disclose (such as the Bank that has a mortgage over your property). Some insurers like initio have produced a specific Tenant Certificate. To obtain a Tenant Certificate of insurance to provide to your tenant or property manager you can get this through your initio dashboard.

Seeing the tenant is paying should I increase my excess?

Probably not – as the tenant only responsible for paying the excess some of the time.

A number of landlords have mis-interpreted that the tenant will pay the excess on all types of claims, and have moved to increase their insurance excess to align with approximately 4 weeks rent.

Remember that if you increase your excess, the higher excess will apply to ALL claims, not just the ones that the tenant is responsible for. The measure of tenant responsibility is carelessness so as a landlord you need to be able to establish that your tenant was careless in order to recover your excess from the tenant.

How do I increase my excess?

With initio you can easily do this by logging in to your dashboard and modifying your policy excess, and the credit premium adjustment will be refunded to you.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

Has your home insurance premium changed recently? Your insurance cost can shift for a few reasons. Let’s break it down:

What makes up your insurance cost?

Your home insurance cost is made up of three things:

The Insurer Premium

This is the main part of your insurance cost. It reflects the level of risk associated with your home and a few key factors, including (but not limited to):

-

Your sum insured (the amount your home is covered for)

-

The location of the property

-

Your chosen policy excess

-

Global insurance costs (reinsurance)

-

Current construction costs for materials and labour, which influence typical claim costs

-

The frequency and severity of past or expected weather events

The Fire and Emergency NZ Levy

The Fire & Emergency NZ Levy is a Government charge that funds emergency response and firefighting services.

The Natural Hazard Insurance Levy

Previously known as the Earthquake Commission (ECQ) levy, the Natural Hazard Insurance (NHI) Levy is for a Government-provided insurance that helps with the cost of repairing or replacing residential homes that are damaged by:

-

- Earthquake

- Tsunami

- Landslip

- Volcanic eruption

- Hydrothermal activity

So right now, what’s changed, and how does it affect my insurance costs?

- Rebuild value of your home: Each year, we may raise the amount your home is insured for. We do this to account for the increasing cost of building a house, and we call it indexation. If the insured value goes up, your policy cost will also go up. Remember, you’re the one who decides the final insured value of your home. You can always change or undo any updates we make. Any changes to this value will change the cost of your insurance. Learn more about changes to rebuild values.

- Premium rate changes: Each year, the cost of your policy might change. This happens because the pool of money needed to cover claims can vary. Insurance providers, like us, look at the number of claims made and the likelihood of future events, such as storms.

- If many people make claims, for example, after bad weather, the cost for everyone can go up, even if you didn’t make a claim. The money you pay helps create a fund that covers these claims, ensuring there is enough money to cover losses when needed. So, if there are more claims, the cost could increase for everyone.

- Fire and Emergency NZ levy change: From 1 July 2024, the FENZ levy rate will increase by 12.7%. Being a change from 10.60c per $100 sum insured (capped at $119.50 per house/living unit, and $21.20 for contents) to 11.95c per $100 sum insured (capped at $119.50 per house/living unit, and $23.90 for contents)

- Average Claims Costs: The average cost of each claim has increased in line with local materials and trade costs.

A further explanation on why premium rates are increasing

- Earthquake risks: New Zealand is earthquake-prone, it’s in the ‘ring of fire’, and is considered one of the highest quake-risk countries in the world. This affects premium rates, and reinsurers (the insurers of the insurers) charge more.

- Global insurance costs: It’s not just disasters in New Zealand that affect our premium rates. When something happens on the other side of the world, it impacts the reinsurers that provide cover to the New Zealand market

- Reserve Bank risk charge: Since its 2020 review, the Reserve Bank has applied an extremely high catastrophe risk charge to New Zealand insurers. Most insurers globally have to hold sufficient re-insurance or capital reserves to cover the risk of a 1-200 year catastrophe event. New Zealand insurers have to hold sufficient re-insurance or capital reserves for a 1-in-1000 year catastrophe event.

- 2023 Weather events: Big storms and floods mean more people need help from insurance, pushing up the cost. The quantity and severity have been steadily increasing over the last few years, with 2023 being off the chart. These events tend to have a longer-lasting impact on the amount and cost of re-insurance. As a result, the effects can take longer to reach the local market.

To ensure you have the latest updates on weather events, we’ll regularly update our blog with a link to the IAG Wild Weather Tracker report.

The graphic below, provided by IAG, provides more detail on the average New Zealand house insurance premium. Most of the recent premium increases are the consequence of the 2023 major weather events, reinsurance changes (insurance of the insurer) and increases in government levies:

Will I always be notified of changes?

Yes, you will. If there’s a change to your yearly or monthly insurance cost, we’ll let you know a month in advance. Generally speaking, your insurance cost will change each year.

Remember, you can also check your cover and make instant changes to things like excess and sum insured from your online dashboard.

We also display on your dashboard if there have been changes to your premium rates for any expiring policy, along with a visual cost breakdown specific to your policy. You can find that immediately above any “renew & confirm button” on your dashboard.

We aim to keep you in the loop so there are no surprises.

Will making a claim on my home or contents policy affect my premium?

No. Your premium won’t change just because you make a claim. Our home and contents policies don’t include a “no claims bonus” or discount, so your premium is not directly affected by your claims history.

See how we compare

Useful Links

How are house insurance premiums calculated?

Am I covered for natural disasters?

Why does my rebuild value change?

Top 4 mistakes people make when insuring their house

Why do Premiums Increase?

How to set up an account with a visa debit card

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: |

Initio Limited |

| FSP Number: |

FSP523166 |

| Website: |

www.initio.co.nz |

| Phone: |

0800 763 929 |

| Email: |

[email protected] |

| Address: |

6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: |

Carmen Jones |

| FSP Number: |

FSP1011244 |

| Contact Email: |

[email protected] |

| Qualifications: |

New Zealand Certificate in Financial Services (Level 5) |

| Experience: |

35+ years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type |

Commission Rate |

| House and contents insurance |

22.5% of insurer premium portion |

| Motor vehicle insurance |

10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.

- Commission income: Initio receives commission from IAG on policies sold through us. This could create an incentive to recommend insurance cover that may not be in your best interests.

- Referral payments: We may pay commissions to partners and brokers who refer clients to us, which could influence the recommendations made to you by those third parties.

How We Manage These Conflicts

Initio manages these conflicts of interest in the following ways:

- Our financial advisers are paid a salary only and do not receive any commission, bonus, or incentive linked to the sale of policies or claims outcomes.

- We require all financial advisers to follow an advice process that ensures recommendations are based on your goals, circumstances, and needs.

- Where your needs fall outside the scope of our products, we will refer you to a specialist insurer or broker rather than recommend an unsuitable product.

- All financial advisers undergo training on how to manage and disclose conflicts of interest.

7. Reliability Events

A reliability event is something that might influence your decision about whether to seek or act on our financial advice. Examples include a successful regulatory action, a bankruptcy, a criminal conviction for dishonesty, or a prohibition order by a regulatory body.

Neither Initio, nor Carmen Jones, has been subject to a reliability event.

8. What to Do If Something Goes Wrong

Internal Complaints Process

If you are not satisfied with our financial advice service, we encourage you to contact us as soon as possible so that we can try to resolve your concern. You can make a complaint by:

- Email: [email protected]

- Phone: 0800 763 929

- Post: The Complaints Manager, PO Box 319, Hamilton 3204

When we receive a complaint, we will consider your concerns and let you know how we intend to resolve them. Where possible, we will try to resolve your complaint immediately. If we are unable to do so, we will acknowledge your complaint within 2 business days and work with you towards a resolution.

External Dispute Resolution

If you are not satisfied with the resolution of your complaint under our internal complaints process, you can refer the matter to our external dispute resolution scheme. This is a free and independent service.

Initio is a member of the Insurance & Financial Services Ombudsman Scheme (IFSO Scheme).

| Scheme: |

Insurance & Financial Services Ombudsman Scheme (IFSO) |

| Phone: |

0800 888 202 |

| Email: |

[email protected] |

| Website: |

www.ifso.nz |

| Post: |

PO Box 10-845, Wellington 6143 |

9. Privacy

We collect and use your personal information to provide you with financial advice and to arrange and administer your insurance policies. Your personal information is handled in accordance with the Privacy Act 2020 and our Privacy Policy, which is available on our website.

For more information about how we collect, use, store, and disclose your personal information, please refer to our Privacy Policy at https://initio.co.nz/privacy-policy/.

10. Further Information

You can check that Initio is a registered and licensed financial service provider, and verify the registration of your financial adviser, at the Financial Service Providers Register: www.fspr.govt.nz.

This Disclosure Statement is current as at the effective date shown. We will provide you with an updated disclosure statement if there is a material change to the information contained in it.

This information is also available in writing, on request.

This disclosure statement was prepared on: 31st March 2026

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.

All Initio policies are underwritten by IAG New Zealand Limited (IAG). IAG has received an AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. A rating of AA means IAG has a ‘very strong’ claims-paying ability. IAG’s Financial Strength Rating

Contact Details

| Provider: |

Initio Limited |

| FSP Number: |

FSP523166 |

| Website: |

www.initio.co.nz |

| Phone: |

0800 763 929 |

| Email: |

[email protected] |

| Address: |

6 Garden Place, PO Box 319, Hamilton 3204 |

2. Your Financial Adviser

Your financial adviser is a registered Financial Service Provider engaged by Initio under our FAP licence to give regulated financial advice on our behalf.

| Adviser Name: |

Jessica (Jess) Clark |

| FSP Number: |

FSP635990 |

| Contact Email: |

[email protected] |

| Qualifications: |

New Zealand Certificate in Financial Services (Level 5) |

| Experience: |

9 years in the insurance industry |

3. Nature and Scope of Our Advice

We provide financial advice on the following general insurance products issued by Initio (underwritten by IAG New Zealand Limited):

- Homeowner’s house and contents insurance

- Landlord and holiday home insurance

- Multi-unit rental property insurance

- Motor vehicle insurance

Limitations on Our Advice

Important: The scope of our advice is limited to Initio’s own insurance products. We do not provide financial advice on products offered by other insurers and we are unable to offer comparisons with alternative providers’ products.

Our advice is based on the information you provide to us at the time. It is designed to help you select insurance cover from the Initio product range that is suitable for your circumstances and needs, as communicated to us.

Where your insurance needs fall outside the scope of the products we offer, we may suggest that you contact a specialist insurer or insurance broker who can assist you further. In such cases, we will not be providing financial advice on those alternative products.

Before purchasing any insurance product through us, you should read the applicable Policy Wording, which is available on our website. The Policy Wording contains important information about the product, including what is and is not covered, to help you make an informed decision.

4. Our Duties

Initio and our financial advisers have duties under the Financial Markets Conduct Act 2013 (FMCA) and the Code of Professional Conduct for Financial Advice Services (the Code) relating to the way we give advice. When providing financial advice, we are required to:

- give priority to your interests by taking all reasonable steps to ensure our advice is not materially influenced by our own interests or the interests of any other person;

- exercise care, diligence, and skill that a prudent person engaged in the same occupation would exercise in the same circumstances;

- meet the standards of competence, knowledge, and skill set out in the Code;

- meet the standards of ethical behaviour, conduct, and client care set out in the Code;

- ensure that the information we make available to you is not false, misleading, or incomplete.

A copy of the Code of Professional Conduct for Financial Advice Services is available at www.financialadvicecode.govt.nz.

5. Fees, Expenses, and Commissions

Transaction Fees

For new house, contents, and car insurance policies, and for the subsequent renewal of those policies, Initio charges a transaction fee of between $3 and $50 + GST per policy. This fee is shown on your quote and invoice and is payable by you when the transaction is processed on the Initio platform.

Initio does not charge a fee for policy changes, alterations, certificates of insurance, or policy cancellation transactions.

Commissions

Initio receives commission from the insurer (IAG New Zealand Limited) on insurance policies. The commission is included in the premium you pay and is not an additional charge to you.

| Product Type |

Commission Rate |

| House and contents insurance |

22.5% of insurer premium portion |

| Motor vehicle insurance |

10.0% of insurer premium portion |

Claims Handling Fees

Initio may handle claims on behalf of IAG under delegated authority for certain in-scope claims. A fixed claims handling fee is paid by the insurer to Initio for claims handled and settled on behalf of the insurer. This fee is not charged to you.

Referral Partners

Where you have been introduced to Initio by one of our partners or referrers and you decide to purchase an insurance policy, we may pay the partner or referrer. The payment amount depends on the product type, insurance cost, and the specific arrangement with that partner or referrer. Any remuneration paid to our partners or referrers is not charged directly to you and does not affect the amount you pay.

Adviser Remuneration

All Initio financial advisers are paid a salary and are not incentivised by the selling (or claims settlement outcome) of insurance products. Our financial advisers do not receive any commission or other incentives for giving financial advice or selling an insurance policy.

6. Conflicts of Interest

We recognise that conflicts of interest can arise from the way we are remunerated. The following are conflicts of interest that a reasonable client would expect to be told about:

- Limited product range: We only provide advice on Initio’s own products (underwritten by IAG). We do not compare Initio’s products with those of other insurers. This means our advice may not cover all insurance options available to you in the market.

- Commission income: Initio receives commission from IAG on policies sold through us. This could create an incentive to recommend insurance cover that may not be in your best interests.

- Referral payments: We may pay commissions to partners and brokers who refer clients to us, which could influence the recommendations made to you by those third parties.

How We Manage These Conflicts

Initio manages these conflicts of interest in the following ways:

- Our financial advisers are paid a salary only and do not receive any commission, bonus, or incentive linked to the sale of policies or claims outcomes.

- We require all financial advisers to follow an advice process that ensures recommendations are based on your goals, circumstances, and needs.

- Where your needs fall outside the scope of our products, we will refer you to a specialist insurer or broker rather than recommend an unsuitable product.

- All financial advisers undergo training on how to manage and disclose conflicts of interest.

7. Reliability Events

A reliability event is something that might influence your decision about whether to seek or act on our financial advice. Examples include a successful regulatory action, a bankruptcy, a criminal conviction for dishonesty, or a prohibition order by a regulatory body.

Neither Initio, nor Jess Clark, has been subject to a reliability event.

8. What to Do If Something Goes Wrong

Internal Complaints Process

If you are not satisfied with our financial advice service, we encourage you to contact us as soon as possible so that we can try to resolve your concern. You can make a complaint by:

- Email: [email protected]

- Phone: 0800 763 929

- Post: The Complaints Manager, PO Box 319, Hamilton 3204

When we receive a complaint, we will consider your concerns and let you know how we intend to resolve them. Where possible, we will try to resolve your complaint immediately. If we are unable to do so, we will acknowledge your complaint within 2 business days and work with you towards a resolution.

External Dispute Resolution

If you are not satisfied with the resolution of your complaint under our internal complaints process, you can refer the matter to our external dispute resolution scheme. This is a free and independent service.

Initio is a member of the Insurance & Financial Services Ombudsman Scheme (IFSO Scheme).

| Scheme: |

Insurance & Financial Services Ombudsman Scheme (IFSO) |

| Phone: |

0800 888 202 |

| Email: |

[email protected] |

| Website: |

www.ifso.nz |

| Post: |

PO Box 10-845, Wellington 6143 |

9. Privacy

We collect and use your personal information to provide you with financial advice and to arrange and administer your insurance policies. Your personal information is handled in accordance with the Privacy Act 2020 and our Privacy Policy, which is available on our website.

For more information about how we collect, use, store, and disclose your personal information, please refer to our Privacy Policy at https://initio.co.nz/privacy-policy/.

10. Further Information

You can check that Initio is a registered and licensed financial service provider, and verify the registration of your financial adviser, at the Financial Service Providers Register: www.fspr.govt.nz.

This Disclosure Statement is current as at the effective date shown. We will provide you with an updated disclosure statement if there is a material change to the information contained in it.

This information is also available in writing, on request.

This disclosure statement was prepared on: 31st March 2026

1. About Initio

This Disclosure Statement provides important information about the financial advice services provided by Initio Limited (Initio, we, our, or us). This information is required under the Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 and is designed to help you decide whether to seek or act on financial advice from us.

Initio is a Financial Advice Provider (FAP), licensed by the Financial Markets Authority (FMA) to provide financial advice under the Financial Markets Conduct Act 2013 (FMCA). You can verify this by checking the Financial Service Providers Register at www.fspr.govt.nz and searching our Financial Service Provider (FSP) number: FSP523166.