Search results for: {search_term_string}

House Insurance

Switching Payment Frequency

You can change how you pay for your policy. There are two key timings to be aware of when making a change:

- At renewal (your annual anniversary) – the change can be done as part of the renewal transaction.

- Mid-term (during the insurance year) – a new policy is required.

You should also check current premium rates before taking out a new policy. These may have changed since your last rates were set. You can check current premium rates at any time by using the quote options from your dashboard (home insurance + or car insurance +).

Changing from monthly to annual

If you want to change from monthly to annual payments at anytime, you will need to set up a new annual policy. Here’s how:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “Pay annually” option.

- Complete the application form and make the annual payment.

- Once the new annual policy is active, cancel your original monthly policy. Any unused portion of premium will then be automatically calculated and refunded.

Unfortunately, due to the different payment technologies used for monthly and annual payments, we’re unable to simply change an existing policy mid-term.

Changing from annual to monthly

What if I want to switch from annual to monthly payments?

How to achieve this depends upon the timing of your insurance year;

At your annual renewal

If your home policy is due for renewal, you can switch from annual to monthly by selecting the “Pay monthly” option during the renewal process from your customer account/dashboard.

Mid-term (during the insurance year)

If you want to change to monthly payments before or after your renewal date, you’ll need to set up a new monthly policy:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “pay monthly” option.

- Complete the application form and make the first monthly payment. The subsequent monthly payments will fall on the same day of the month that you start this policy from.

- Once the new monthly policy is active, cancel your original annual policy. Any unused portion of premium will then be automatically calculated and refunded.

Payment Options

Can I pay monthly by bank transfer or direct debit?

No, Monthly payments require a valid credit card or visa debit card and cannot be paid for by any other means.

Can I pay fortnightly, weekly or quarterly?

No, we only offer monthly or annual payment frequencies. We do not have alternatives available.

Remember, it’s always important to review your options carefully to make sure you’re selecting the best one for your needs.

Useful links:

Essential guide to home insurance

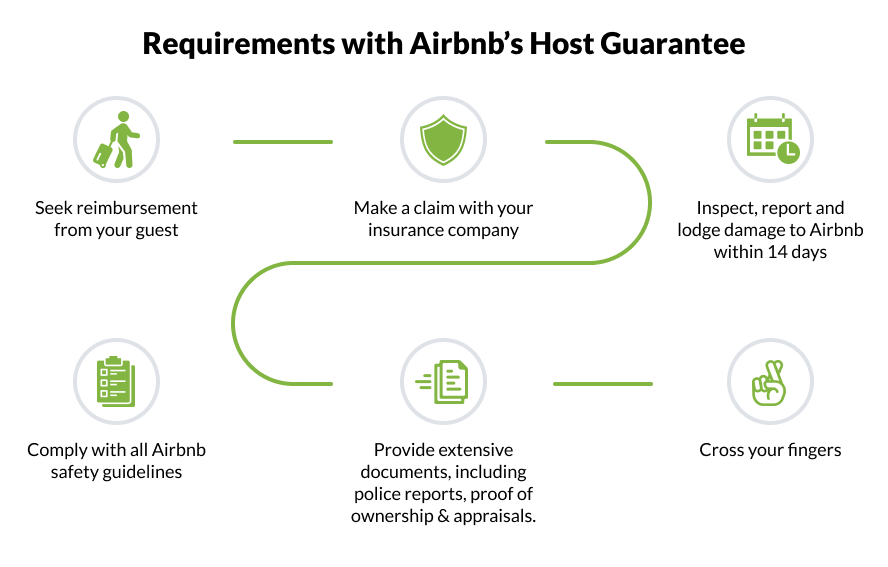

Should you rely on the Airbnb Host Guarantee?

Many hosts rely on Airbnb’s well-advertised $1USD million of free Host Guarantee cover. But be warned, this can lull you into a false sense of security leaving many disappointed when they make a claim but find they don’t tick the boxes.

The rules are specific, which can make it hard to claim especially when innocent hosts unknowingly violate the conditions.

What does it cover?

The Airbnb Host Guarantee isn’t a formal insurance policy, but rather a strongly-worded promise to rectify guest damage providing your situation meets certain conditions.

It isn’t regulated by the New Zealand Financial Markets Authority, so you would struggle to take them to court locally if things really turn sour.

Last Resort for Recovery

In Airbnb’s own words they say the Host Guarantee is not an insurance policy, and shouldn’t be considered a replacement.

Firstly, the guarantee can only be claimed on after trying to recover compensation from the guest, and then your own insurance (if you have this). Already the Host Guarantee is a last resort.

For a chance of recovery from the guarantee, you’re going to have to prove you persistently chased up that festival-goer to get $800 back for a living room wall repair.

There are many examples of people angry about their payout from the guarantee. Usually it’s because they aren’t aware of the conditions.

A main stump is that damage needs to be inspected, reported and lodged to Airbnb within 14 days, or else you’re out of luck.

By the time you’ve checked in your next guest it could already be too late. This could be enough to kill any claim through the Guarantee if you live away from your Airbnb.

Remember that you need to seek recover from the guest, and then your insurance before you lodge a claim in the 14 day window. The requirements almost seem like a trap to get you to exceed the strict 14-day deadline.

Watch out for Exclusions

- Only damage that happens during the booking period is covered. If an unwelcome guest overstays their welcome and causes damage, there won’t be cover.

- Cover only applies to part of the house that’s in your listing. If you rent a room, but your guest uses another bathroom and causes damage, you’ll need to foot the plumber’s bill yourself.

- It’s full of various exclusions; like damage from excessive water utility use (a sink overflow won’t be covered), and any damage by animals or pets (are you sure your guests won’t bring their dog?).

- Be prepared for stacks of bureaucracy when you make a claim. Airbnb require extensive police reports, proof of ownership and request form documents for damage.

The list of exclusions goes on. To read the full terms, conditions and exclusions see here.

No Liability Insurance

Finally, the Host Guarantee doesn’t help when it comes to legal liability. If your guest suffers an injury and they sue you, the Host Guarantee will fall seriously short.

The idea of someone stubbing their toe on the coffee table and suing might seem ridiculous, but legal liability also extends to things like sickness (if an illness is caused by the condition of your house) or freak accidents.

Is it worth the Risk?

One-in-seven Kiwi Airbnb hosts report damage. That’s about a 15% chance you’ll suffer damage one-day.

While most reports are minor and hosts voluntarily pay to avoid the lengthy resolution process, we’ve heard some shocking stories ranging from vomit-covered walls to 100-person guest parties.

Hosts should ask themselves if relying on the Guarantee is worth the risk? After all, Airbnb themselves recommend having robust insurance in place in the first instance.

Learn more today about our specialist short-term guest cover.

Initio Insurance are the pioneers of online house insurance in New Zealand, with cover specifically designed for own homes and holiday homes also rented on Airbnb.

Related articles:

Holiday Home vs. Own-Home Insurance: What New Zealand homeowners need to know

Owning multiple properties can sometimes make insurance decisions tricky, especially for New Zealand homeowners who use their homes differently throughout the week. For example, you might have one home you stay in during the weekdays and another you visit mostly on weekends.

Understanding the right insurance policy for each property is crucial to ensure you’re fully covered.

The main difference between holiday home insurance and own home insurance lies in the occupancy and associated risks. Own Home insurance is for your primary residence where you would reside the majority of the home, not generally suitable if you leave it vacant for periods of 60 consecutive days or more. Holiday homes are not primary residences and are often empty for reasonable periods, increasing risks such as break-ins. Therefore, holiday home insurance has specific conditions and coverage tailored to these unique risks. If you aren’t using your holiday home all year round, you might rent it out between stays.

The following is a list of cover specific to each type of policy to help you determine which is the best policy for your property:

Holiday home insurance specific cover:

- Optional – Guests: Cover for damage, theft, and loss of rent if you host guests.

- Fixed contents: $20,000 standard cover for fixed contents at the home, with options to increase. This covers furniture that stays in your home permanently (not personal belongings). Cover is limited to the property address.

- Blocked pipes: Up to $1,000 to unblock an underground pipe, with no excess.

- Keys and locks: Up to $1,000 for replacing keys and associated locks, with no excess.

- Legal liability: $2 million legal liability costs if an accident damages other property or people.

- Optional – Loss of rent: Up to 12 months or $20,000 following damage to your house.

Own home insurance specific cover:

- Personal contents (available as an add-on to any Own Home policy): Replace or repair lost or damaged belongings, majority of items are insured on a new-for-old basis. Includes cover for contents including personal effects whilst at the property and temporarily removed anywhere in New Zealand.

- Temporary accommodation: $20,000 of alternative accommodation if your damaged house can’t be lived in.

- Reduced glass breakage excess: Reduced $250 excess for glass breakage claims.

What if you split your time equally between two homes?

If you divide your time equally between two homes, each property may require different insurance considerations. The home you use during the weekdays might need a standard home insurance policy, while the one you visit on weekends could be classified as a holiday home, or potentially you may need two Own Home (owner occupied) policies. It’s crucial to assess the specific usage patterns of each property to ensure you have the appropriate coverage. This should also take what belongings you use the majority of the time at each property into consideration.

Holiday home or rental?

Provided you use the home as your holiday home we can also offer the option of including short-term rental cover for you. If this describes your situation, select ‘Holiday Home – sometimes rented’ from the dropdown menu, and initio’s clever software will do the rest. If you’re not sure which cover is best for you – we’re here to help.

What special terms apply (regarding vacancy) on each policy?

Holiday Homes:

If no one has been living or holidaying at the home for a period of more than 60 consecutive days, and the home is recorded as a holiday home, expectations are that the following criteria can be met:

- the home is inspected inside and outside by you or a nominated person at least every 60 days, and

- the home and its grounds are adequately maintained, mail is cleared regularly and

- the water supply is turned off and

- all doors are locked and windows secured

If you are unable to meet those conditions, cover will continue with a higher standard excess of $5,000 applying to any claim. If however, a loss results from a break-in or attempted break-in at the home while it is fitted with an active, professionally-installed alarm or security system, then an excess of $1,000 applies.

Own Homes (primary residence):

If no one has been living at the home for a period of more than 60 consecutive days, we will only pay for loss that is:

- caused by fire, explosion or lightning, or

- covered under the ‘Natural disaster’ automatic additional benefit.

These terms can be reviewed upon request for special circumstances.

What if I only use the house for guests?

Under our cover, you need to use the house at least occasionally yourself over the course of a typical year. If you;

- don’t use the house yourself as your holiday home and as such also

- don’t keep personal items at the home, and

- it is only rented to short-term guests,

it is considered a commercial operation, similar to a motel. Our cover is domestic-based house insurance, and cannot be used if the above requirements are not met.

Are my personal contents covered under a holiday home policy?

Your personal contents items, like phones, jewellery, and laptops, won’t be covered under your holiday home cover as they should be protected by your contents cover at your main home. Belongings that remain at your holiday home, like furniture, TVs, and glassware, are covered. You can only insure your personal contents with initio as an add-on to an owner-occupied home you also insure with us.

What else can you do to ensure you choose the best insurance provider for your needs?

When researching and comparing insurance providers, it’s essential to evaluate them based on their reputation, customer satisfaction, and claims processing efficiency. Reading customer reviews and testimonials can provide valuable insights into real-world experiences with different insurers. Additionally, carefully reviewing policy details, such as coverage limits, exclusions, excess amounts, and additional features, is crucial. Don’t hesitate to ask questions or seek clarification on any confusing terms or conditions.

Key takeaways

- Tailored insurance coverage: Ensure each property has the appropriate insurance policy based on its usage, whether it’s a primary residence or a holiday home.

- Personal belongings: Secure and appropriately insure personal belongings at both properties, ensuring valuables are covered and managed efficiently.

- Maintenance and security: Maintain regular upkeep and robust security measures for both homes to prevent risks associated with extended vacancies.

- Be aware of policy restrictions/conditions relating to how long a home is vacant for.

- Thoroughly research and compare to make an informed decision.

USEFUL LINKS

Holiday home insurance basics

If you’re lucky enough to own a holiday home, you’ll want to make sure you’ve got the best insurance protection, especially considering you’ll not always be there in person to look after it. Whether you keep it for personal use or decide to rent it out to short term guests – we’ve got you covered.

Standard house insurance requires someone to be living at the home for more than 60 consecutive days. If it’s vacant for longer than this, it’s considered a holiday home. Because a holiday home isn’t your primary residence there are more risks involved, for example; the property may be empty for long periods of time, increasing its chances of break-ins.

What are my obligations?

We expect holiday houses to be empty more often, so our conditions are a little more lenient, but we do require:

- You or your family stay at the holiday house at least once a year

- The house is inspected (inside and outside) by you or a nominated person at least every 60 days

- The home and its grounds are maintained

- Mail is cleared regularly

- Water supply is turned off

- All doors and windows are secured when the home is vacant.

If you can’t meet these conditions, then a standard $5,000 excess will apply to your policy. Alternatively, if it’s fitted with a professional alarm* this will reduce to $1,000 when you claim for a break-in or burglary.

* Systems which include surveillance cameras only do not meet this criteria – the system needs the ability to provide an external alert (audible or direct to a monitoring company)

How do I get holiday home cover?

It’s as simple as selecting holiday home as the property type when you generate your instant quote. Alternatively, if you are changing your current home into a holiday home, all you need to do is change your cover in the property type drop down menu. The monthly costs will automatically update and will take effect as soon as you confirm the change online.

Holiday home or rental insurance?

The main difference between holiday homes and year round short term rentals is how often they are rented out. We have multiple options available depending on how frequently you rent your house out – just select the right option in the dropdown menu and initio’s clever software will do the rest. If you’re not sure which is the best cover for you, get in touch anytime. We’re here to help.

At initio, we offer comprehensive protection for your bach or holiday home, with flexible cover if you also rent to guests. Learn more: https://initio.co.nz/holiday-home-insurance/

This guide is intended to be a quick reference to vacant houses. We recommend reading the full policy wording for the full details of your holiday home coverage.

Useful articles:

What are my obligations as a landlord?

Initio’s landlord insurance policy requires landlords to meet the ‘Landlord Obligations’ for cover under the Landlord Protection and Meth Contamination extensions. The cover in these extensions are:

Landlord’s Protection

- Malicious damage by tenants, and associated loss of rents.

- Theft by tenants.

- Loss of Rent following a tenant vacating the property.

- Loss of Rent following a tenant eviction for non-payment of rent.

- Meth Contamination, and associated loss of rents.

If a landlord has a property manager, it is usually the property manager’s responsibility to meet the obligations. Otherwise, the landlord will need to meet these themselves.

If you don’t meet the Landlord’s Obligations all the standard cover included in the policy remains in place. You are still covered for natural disasters such as an earthquake as this does not involve the risk of the tenant. However, if you do NOT meet the obligations but then lodge a claim for meth contamination at your property, your claim may be declined.

Landlord’s Obligations

You, or the person who manages the tenancy on your behalf, must:

- Exercise reasonable care in the selection of the tenant(s) by at least obtaining satisfactory identification and written or verbal references for each adult tenant and when a reasonable landlord would consider it appropriate also check their credit and Tenancy Tribunal history.

- Keep written records of pre-tenancy checks conducted for each adult tenant, and provide to us a copy of these if we request it.

- Collect a total of 3 weeks’ rent in any combination of rent in advance and bond that will be registered with Tenancy Services.

- Complete an internal and external inspection of the home at a minimum of 3-monthly intervals at the relevant residential dwelling upon every change of tenant(s).

- Keep photographs and a written record of the outcome of each inspection, and provide us a copy of these if we request it.

- Monitor rents on a weekly basis with written notification being sent to the tenant(s) whenever rent is 14 days in arrears, together with a personal visit to determine if the tenant(s) remains in residence.

- Make application to the Tenancy Tribunal for vacant possession in accordance with the provisions of the Residential Tenancies Act 1986 if:

(a) the rent is 21 days in arrears, or

(b) you become aware of any illegal activity by the occupant(s) at the home, or

(c) intentional damage to the home is caused by the occupant(s).

What if the home is occupied by employees as part of their employment package?

If the home is provided to and occupied by your employee as part of their employment package with you, then obligations 3, 6. and 7.(a) do not apply.

What if this is my holiday home which is occasionally let to short term paying guests?

If the home is occupied by short-term paying guests such as a AirBnB or BookaBach, then the obligations do not apply to have cover for damage and theft by guests.

What if the home is occupied by Family Members?

You would need to decide if a Landlord policy is the right product for you. Are you wanting to cover Loss of Rents and Intentional Damage by Tenants? Does the family member pay rent? Get in touch with our support team to discuss the available options.

Protect your rental with initio’s landlord insurance

Related Articles:

Demystifying Insurance Excess

Choosing the right insurance excess can feel confusing. Your excess is the amount you pay towards a claim before your insurer contributes.

Understanding how excess works helps you balance your annual premium against what you would need to pay if something goes wrong.

Quick summary

-

An excess is the amount you pay when you make a claim.

-

A higher excess usually lowers your annual premium.

-

A lower excess usually increases your premium.

-

An excess applies per incident.

-

The right choice depends on your financial situation and risk tolerance.

What is an insurance excess?

An insurance excess is the portion of a claim you pay yourself.

For example, if you have a $1,000 excess and make a $10,000 claim, you pay $1,000 and your insurer pays the remaining $9,000.

Excess applies per incident. If multiple separate incidents occur, more than one excess may apply.

High excess vs low excess

When selecting an excess, you are balancing two costs:

-

Your yearly insurance premium

-

Your potential out-of-pocket cost at claim time

High excess

-

Lower annual premium

-

Higher payment if you make a claim

Low excess

-

Higher annual premium

-

Lower payment when you claim

A higher excess can work well if you are financially able to fund the excess and want to protect yourself mainly against major events.

How insurers calculate excess levels

Insurers use claims data and risk modelling to determine how excess levels affect premiums. They analyse:

-

How often claims occur

-

The average size of claims

-

Risk trends in different regions

-

Historical claims behaviour

The balance between premium reduction and excess size is based on these numbers. While some policyholders expect larger premium discounts for higher excesses, insurers must maintain a balance between premiums collected and claims paid.

When does a higher excess make sense?

Insurance is most valuable for significant events such as fires, floods or earthquakes.

Some property owners prefer a higher excess, such as $1,150 or $2,000, because they:

-

Are less concerned about small claims

-

Want lower annual premiums

-

Have the savings available to fund the excess

For landlord or owner-occupied properties, the highest available excess option is currently $2,000.

A practical example

Consider an Auckland property with a $700,000 replacement value.

-

With a $400 excess, the annual premium may be around $2,000.

-

With a $2,000 excess, the premium may reduce to around $1,500.

That saves $500 per year. However, if you make a $10,000 claim:

-

With a $400 excess, you pay $400.

-

With a $2,000 excess, you pay $2,000.

In that scenario, the higher excess leaves you approximately $1,100 worse off after factoring in the premium saving.

Over time, if you rarely claim, the savings from a higher excess can accumulate. The key question is whether you can comfortably afford the excess if a claim occurs.

Is choosing a high excess a form of self-insurance?

Yes, in a sense.

Selecting a higher excess means you are sharing more of the risk with your insurer. You are effectively self-insuring smaller losses while relying on insurance for large, financially stressful events.

Your personal circumstances matter

The right excess depends on:

-

Whether you are a homeowner or landlord

-

Your cash flow and savings

-

The age and condition of your property

-

Your claims history

-

Your tolerance for financial risk

New homeowners or landlords may prefer lower excesses for certainty. More experienced property owners, particularly those with multiple properties, may choose higher excesses to manage long-term premium costs.

How data can help your decision

Claims probability plays a role in choosing an excess.

For example, if you own 10 properties, statistics suggest you may expect at least one reasonable claim each year across the portfolio.

Understanding the following can help you make a more informed decision about your excess level:

-

Local weather patterns

-

Crime rates

-

Property condition

-

Historical claims data

Frequently asked questions about insurance excess

Does excess apply per claim?

Yes. An excess is applied per incident. If multiple incidents occur, more than one excess may apply.

Does choosing a higher excess always save money?

It reduces your premium, but may cost more overall if you claim frequently.

What is the highest excess available?

The highest available excess for landlord and owner-occupied properties is currently $2,000.

Should landlords choose a higher excess?

Some landlords with multiple properties prefer higher excesses to reduce premiums, but this depends on financial flexibility.

Making a confident decision

Insurance excess is about balance. It is not about choosing the lowest premium or the lowest out-of-pocket cost. It is about selecting an amount that matches your financial comfort level and long-term strategy.

Understanding how excess works allows you to make a clear, informed decision rather than guessing.

You might also be interested in:

Guide to landlord insurance in New Zealand

Landlord Insurance is designed specifically for rental property owners. It protects not only the house itself, but also the additional risks that come with renting to tenants. Unlike standard house insurance, landlord insurance includes cover for tenant damage, loss of rent and other landlord-specific exposures.

What is landlord insurance?

Landlord insurance is a specialised policy for long-term residential rental properties. It covers the physical building against events like fire, floods, and earthquakes, while also protecting landlords from risks that do not apply to owner-occupied homes.

While standard house insurance focuses on homeowner risks, landlord insurance extends cover to include tenant-related damage, rental income loss, eviction scenarios and other risks unique to renting out your property.

Quick summary

-

Landlord insurance covers rental property risks not included in standard house insurance.

-

Includes tenant damage, intentional damage and vandalism.

-

Covers loss of rent due to damage, eviction or abandonment.

-

Includes meth testing and cleaning cover.

-

Provides automatic landlord contents cover.

-

Designed for long-term residential rental properties in NZ.

What extra cover does Landlord Insurance provide?

Damage by Tenants Loss of Rents Meth Contamination Landlord Contents

Tenant damage cover

Standard house insurance may cover accidental damage caused by tenants, but it does not cover intentional damage.

Landlord insurance protects you against both accidental and intentional tenant damage. This includes vandalism, theft, and deliberate damage such as holes punched in walls or damage from unruly gatherings.

Under our landlord insurance policy :

-

Accidental tenant damage is covered up to your full sum insured.

-

Intentional damage, vandalism or theft is covered up to $25,000 per event.

-

Serious fire or explosion damage is covered above the $25,000 limit and up to your full property sum insured.

Cover applies to damage caused by your tenant, paying guests, or anyone occupying the home, including their guests.

Loss of rent cover

Rental income is essential for most landlords. If your property cannot be rented, you may still have mortgage payments and other costs to meet. Landlord insurance includes loss of rent protection in two main scenarios:

Loss of rent due to property damage

If physical damage makes your rental unlivable, we cover:

-

Up to 52 weeks of rent, or

-

The loss of rent sum insured you select, whichever comes first.

We automatically include $20,000 of loss of rent cover in all landlord policies, with options to increase this to $40,000 or $80,000.

This applies while repairs are completed following insured damage, such as flood or fire.

Loss of rent due to eviction or abandonment

Loss of rent can also arise when there is no physical damage. If your tenant:

-

Is evicted for non-payment after falling 21 days behind, or

-

Leaves without giving the required notice, we cover lost rent for up to six weeks.

This also extends to situations where tenants can legally cease rent payments under their tenancy agreement, such as when access to the property is prevented or essential utilities fail.

Meth contamination cover

Meth contamination is a serious risk for landlords in New Zealand. Cleaning a contaminated property can cost tens of thousands of dollars and may render the home unlivable for months.

Standard house insurance does not cover meth contamination. Landlord insurance includes cover for:

-

Laboratory testing

-

Cleaning costs where a positive meth result is confirmed

Meth cover with initio

We provide up to $30,000 for meth testing and cleaning costs.

Loss of rent cover applies over and above this $30,000 limit. We will pay your weekly rent while the property is being cleaned, for up to 52 weeks or up to your selected loss of rent sum insured.

You might also be interested in:

- Is my rental property covered for meth?

- What to do after a positive meth test

- How do meth claims work?

- Understanding the gluckman report

Landlord contents cover

Many rental properties are furnished or partially furnished. This can include appliances, curtains, rugs, heaters and other non-fixed items. Some landlord policies require contents to be added separately. Our landlord policy automatically includes contents cover.

How much landlord contents cover is included?

We include $20,000 of landlord contents cover as standard. This is the minimum level and cannot be reduced.

If your property is more fully furnished, you can increase this to $40,000 or $60,000.

What is covered?

Cover applies to fixtures and fittings and landlord-owned contents included in the tenancy.

-

Items five years old or less are replaced with new items.

-

Items over five years old are paid at present value.

This does not cover your personal belongings.

Frequently asked questions about landlord insurance

Can I reduce the $20,000 landlord contents limit?

No. The $20,000 landlord contents cover is automatically included as the minimum under our landlord policy. This amount cannot be reduced. You are covered for landlord contents up to that figure as standard, with options to increase the limit for more fully furnished properties.

Is furnished property covered under landlord insurance?

Yes. Whether your rental property is furnished or unfurnished, it is covered.

Landlord insurance automatically includes cover for landlord contents such as non-fixed appliances, curtains, rugs and heaters. If the property is fully furnished, you can increase the contents limit to ensure everything is adequately protected

Does landlord insurance cover intentional tenant damage?

Yes. Our landlord insurance policy covers intentional damage caused by tenants.

Intentional damage, vandalism or theft by tenants is covered up to $25,000 per event. In cases of serious fire or explosion damage, cover can extend beyond this limit and up to your full property sum insured.

More information about landlord insurance

Explore these additional articles that may interest you:

- Five fundamentals of landlord insurance

- What is landlord insurance?

- Are you thinking of renting our your home and becoming a landlord?

- What does landlord insurance cover?

What is a Multi-Unit rental property for the purpose of insuring under our Multi-Unit Rental policy?

What can be insured under our Multi Unit Rental Policy?

At initio we have a multi-unit rental policy which was designed to insure a block of flats owned by a single landlord. For the purposes of this policy, a Multi-Unit Rental Property is defined as;

- two or more units, townhouses or flats that are combined under one building, so connected under the same roof or are physically connected in some other way (e.g. car-port or deck) and

- with each unit being self contained and

- having the same owner and

- on a standard long-term residential lease

Some examples of multi-units that we can insure under this policy are;

- a two story house where each level has a separate tenancy

- a block of flats owned by one person/entity – up to 8 units

- cross lease units, connected by a carport

- duplex townhouses

- rental house with physically attached self contained studio / granny flat – also rented out

There are some limitations as to what the multi unit properties we can insure.

- We cannot insure more than 8 units.

- We cannot insure properties that are more than 3 stories.

- The tenancies must not be short term or holiday lets.

- The property must be residential use only.

- We cannot insure individual or multiple units that form part of a body corporate.

- We cannot insure more than one rental unit at different addresses under this policy.

Related Articles:

Loss of Airbnb rental income due to Covid 19? Am I covered by insurance?

Homes that are rented out to short-staying paying guests are experiencing booking cancellations and reduced occupancy (loss of income) due to fears and government restrictions relating to Covid-19. We take a look at whether insurance provides cover.

Covid-19, also known as the Coronavirus has caused major impact to visitor travel arrangements. The reduced sentiment to travel as well as New Zealand’s move to protect itself from the rest of world with Government imposed restrictions on travel and self-isolation will and has lead to holiday home (Bookabach, AirBnB etc) cancellations and reduced future bookings.

So, as a AirBnB or Bookabach property owner is there insurance for loss of income where there is no physical damage to the property?

The short answer is No. Let’s explain;

- Most insurance policies include a Loss of Rents provision that specifies an amount of cover (e.g. $20,000) and a payment period (e.g. 12 months)

- This cover is triggered by a physical loss to the home or property that results in house being unliveable.

- Some common examples include, a fire at the property, a burst pipe that floods the house, earthquake damage or rising flood waters.

- The policy responds to cover the damage from these things and also the associated loss of rental income while the damage is being repaired.

- So, if the property is a holiday home and is damaged the loss of income would include the confirmed bookings you know about that need to be cancelled, and the other future bookings you miss because the property is not available to be booked. Its the perfect solution…. until non-physical things like Covid-19 come long.

No physical damage – the Covid situation

As Coronavirus (or any other illness, virus or disease for that matter) does not cause any physical loss to the property, it does not trigger the loss of rents cover. The key component for cover is missing.

But wait, what about cover loss of rents due to tenant eviction and prevention of access and the like – that’s not physical damage? Yes, some policies like Initio, have a special benefits that provide loss of rental income cover from other causes that are not necessarily physical.

The one that is most relevant here is the ‘prevention of access’ policy benefit. Prevention of access relates to not being able to access the property, and typically comes in the form of a road closure or a washed out driveway for example. While Covid-19 is causing bookings to be cancelled, access to the property is not actually prevented, meaning that this part of the cover does not provide any assistance for Corona virus related income losses.

It is also important to note that most house insurance policies out-rightly exclude cover for “financial loss or expense of any type in connection with a Notifiable Infectious Disease under the Health Act 1956”.

While this provides little comfort to holiday home and own home owners who rent out their properties to short term guests, it does mean that home owners can make informed decisions about how to manage their lower income risk over the coming months.

About Initio

Initio is a New Zealand-based online house insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home and contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with built-in cover for loss of rent and damage by the tenant.

Having completed over 35,000 automated insurance transactions, Initio’s market-leading policies can be quoted, bought and amended online – all in an instant.

Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

Insurance for a non-rented second home on your property

Is it only used as extra space for your household?

If you have two dwellings on your property and the second one is used only by you or your family—without being rented out—it’s important to have the right insurance to cover both spaces.

What counts as an extension to your own home?

If the second unit/home is;

- Used like a sleepout for members of your immediate family, such as teenagers or elder family members.

- And you all predominantly share meals and/or facilities OR

- Used as a hobby room such as an art or music room OR

- Used as a home office space, then

It’s considered as an extension to your home and counts towards the one home unit/dwelling.

What insurance do you need?

For this setup, you only need one home insurance policy, which will cover both your main home and the second dwelling under the same policy. This ensures protection for:

- Your home and any structures used as part of your home for residential purposes on the property

Get covered today

With initio, you can get a quick quote and buy insurance online in minutes, making it easy to ensure your home and second dwelling are fully protected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

Need help? If you’re unsure about what policies are right for your situation, contact us to make sure you’re fully protected.

Get covered today with initio – Quick quotes, easy online cover.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

- Do you have a second dwelling on your property that you rent out?

- Renting out part of your home short-term

- Renting out a second dwelling solely for short-term stays

- Second dwelling on your property that your family lives in

- Renting out two dwellings on your property

Initio and Bookabach team up

Initio is pleased to announce that it has teamed up with Bookabach to provide insurance for holiday homes and baches that are rented out on occasion. Our specialist rental property insurance policy has been tailored to meet the needs of properties with long term tenants and also those properties which are rented out on a short term basis (eg holiday homes).

If you own a holiday home and this sounds like you…. Even if you don’t rent it out that often, our policy is for you.

The main question is do you have the right covers. Your existing insuring may take exception to the fact that your property is let our on occasion. Get it right from the beginning and insure with initio.

See the recent bookabach article for some great things to think about: Got insurance (no, Really)

Holiday Home Insurance

Owning a Holiday Home means you’re a little different. That’s why you need an insurance policy that provides good cover when you’re not there or when someone else is using it.

At Initio we understand that your holiday home could be advertised online, and that on occasion you may have paying guests staying. Or perhaps your holiday home is only used by your friends and family. When you insure with Initio we give you the choice, so you get the right cover for the right price.

Holiday homes are often left vacant for extended periods, we know this and we make sure that the cover continues regardless of when the property was last occupied. We also know that your holiday home is furnished and that some of your personal items may remain at the property, and this is why we provide you with a range of contents insurance options.

[initio_review_rating_total property_type=”holiday-home” get_quote_button=”Get Quote” get_quote_button_classes=”cta-button cta-button–orange”]

Here are some of the great features of the cover:

| Description of Cover | Limit of Cover | Excess |

|---|---|---|

| Full replacement Holiday Home Cover up to Sum Insured | Your Sum Insured | Your Choice of $400 / $650 / $1,150 / $2,000 |

| Major Malicious Damage by Guest (Fire & Explosion) | Your Sum Insured | Greater of $500 or Your Chosen Excess |

| Deliberate Damage by Guest | $25,000 | Greater of $500 or Your Chosen Excess |

| Loss of Rents Cover (following property damage) | $20,000 – $80,000 | Nil |

| Owners / Landlords Contents Options for present day & replacement value cover |

$20,000 – $220,000 | Your Chosen Excess |

| Hidden Gradual Damage Cover | $3,000 | Your Chosen Excess |

| Owners Legal Liability Cover | $2,000,000 | Your Chosen Excess |

| Unoccupancy exceeding 60 days | Your sum insured | $5,000 or $2,000 with intruder alarm** |

| Full Earthquake Cover | Your sum insured | $5,000 |

** Where your property is a Holiday Home or Bach your chosen excess will apply if the property is kept in a tidy condition, all external doors and windows are securely locked, all papers and mail are collected regularly, and the home is under regular supervision.

IMPORTANT This is a summary of the policy only. Please refer to the policy wording for full details of cover.

Initio allows you to buy insurance online and enjoy some of the best policy coverage and claims service available for Holiday Home owners.

[initio_quote_calculator title=”Instant free Holiday Home quote & buy online”]

[initio_review_list property_type=”holiday-home”]

Multi-Unit Insurance

If you’re serious about property investing, it is likely that you have a block of units in your portfolio. We have the insurance policy designed to keep premiums low and help your yeilds.

Initio provides an all-in-one cover for your residential multi unit rental property (up to six attached units) and the extra risks you take on as a landlord, such as one of the tenants deliberately damaging your property.

[initio_review_rating_total property_type=”rental-multi” get_quote_button=”Get Quote” get_quote_button_classes=”cta-button cta-button–orange”]

Here are some of the great features of the Initio combined multi-unit policy:

| Description of Cover | Limit of Cover (across all units) |

Excess |

|---|---|---|

| Full replacement Dwelling Cover up to Sum Insured | Your Sum Insured | Your Choice of $400 / $650 / $1,150 / $2,000 |

| Major Malicious Damage by Tenant (Fire & Explosion) | Your Sum Insured | Greater of $500 or Your Chosen Excess |

| Deliberate Damage by Tenant | $25,000 | Greater of $500 or Your Chosen Excess |

| Methamphetamine Contamination – manufacture | Your Sum Insured | Your Chosen Excess |

| Methamphetamine Contamination – consumption | $30,000 | $2,500 |

| Loss of Rents Cover (following property damage) | $20,000 – $80,000 | Nil |

| Landlords Contents – present day value cover | $20,000 – $40,000 | Your Chosen Excess |

| Hidden Gradual Damage Cover | $3,000 | Your Chosen Excess |

| Owners Legal Liability Cover | $2,000,000 | Your Chosen Excess |

| Full Earthquake Cover | Your sum insured | $5,000 |

IMPORTANT This is a summary of the policy only. Please refer to the policy wording for full details of cover

What if I live in one of my units?

The Multi-Unit Rental policy is designed for rental properties. If you own a block of units and personally reside in one unit, this will need to be insured individually as an owner occupied home. This way you can include cover for your contents and personal effects, and get premium savings on your own home. The remainder of the units in the block can be insured either together or individually.

What if it is a Body Corporate?

Sorry we are unable to insure properties which are part of a Body Corporate.

How do I note the ownership of each unit?

If each unit has a different owner the unit will need to be insured individually. To qualify for the multi-unit policy the units must have the same ownership and be under the same roof.

How many units can I insure on one policy?

You can insure up to SIX attached residential units under a single Initio multi-unit policy. So as long as all units are attached you can insure the lot under one Initio policy.

Initio allows you to buy insurance online and enjoy some of the best policy coverage and claims management available to Landlords of multi units.

[initio_quote_calculator title=”Instant free quote & buy online” pre_selected_cover=”rental-multi”]

[initio_review_list property_type=”rental-multi”]

Join our team!

Digitally savvy, human touch; The heart of initio

Since 2011 we have been redefining insurance. We are creating an insurance experience that customers love! At initio, we are all about creating better digital experiences for buying and managing insurance exclusively online. We’re best known for being the first insurance provider in New Zealand to quote and bind an insurance policy online. We consider ourselves to be the challenger brand to the domestic insurance market in New Zealand and as such we are on a mission to redefine the way insurance is managed and delivered to customers digitally.

At initio, we’re not just hiring; we’re on the lookout for thinkers, creators, and lively souls eager to influence the next chapter of insurance for our clients. If you’re brimming with creativity and ready to make an impact, you’re in good company.

Award-Winning Workplace

Yes, you read it right; we’ve got a brand-new accolade. initio has been named one of the Best Insurance Companies to Work for in Australia and New Zealand in 2023! If you want to be part of a company that’s officially recognised as a brilliant place to work, one that truly looks after its staff, then look no further. Come join our award-winning team and let’s transform those brilliant ideas into something that shines even brighter.

Open Positions

Here’s a sneak peek at our roles currently on offer. Can’t find the perfect role just yet? Keep swinging by – new opportunities land faster than you can say “Cheeseburger Fridays.”

What is a total loss in house insurance?

A total loss in house insurance is when a home is damaged so badly that it needs to be fully rebuilt, or partial repairs will cost more than the sum insured. In most cases, this happens after a major insured event such as a serious fire, severe flood, or natural disaster. It is the kind of event where your sum insured matters most, because that amount may affect how much is available to rebuild your home.

If you are reviewing your house cover, this is one reason it is important to make sure your sum insured is accurate.

Key takeaways in this article

- A total loss means the home cannot reasonably be repaired

- It usually means full rebuild or full replacement

- Total loss can apply to your house, contents, or both

- Your sum insured matters most in a total loss

- The exact cover depends on your policy wording

What does total loss mean?

In insurance, a total loss generally means the insured property has been destroyed or damaged to the point where repairing it is no longer practical. In terms of property insurance (e.g house or landlord insurance), this usually means the house would need to be rebuilt from the ground up. For contents insurance, it usually means the belongings cannot be replaced within the sum insured and the policy amount is exhausted.

What is a total loss in house insurance?

A total loss in house insurance usually means the damage to the home is so severe that rebuilding is the only realistic option. This can happen when the house is:

- destroyed by fire

- badly damaged by flood

- affected by earthquake or another natural disaster

- left beyond practical repair after another insured event

Not every major claim is a total loss. Some homes can still be repaired, even after significant damage. The exact event is less important than the outcome. If the damage is severe enough that the property effectively needs full rebuild or replacement, it may be treated as a total loss.

Is a total loss the same as major damage?

No, not always. Major damage means the home has been seriously affected, but it may still be repairable. A total loss usually means the damage is so severe that full rebuild is needed instead.

This is an important difference, because not every large house insurance claim is treated as a total loss.

Why does sum insured matter in a total loss?

Your sum insured matters most in a total loss because it is the amount that may be available to rebuild your home, depending on the terms of your policy.

That is why your house sum insured should reflect what it would cost to rebuild your home to its current size and standard using today’s building costs.

If your sum insured is too low, it may not reflect the real rebuild cost of your home after a major loss. That is why it helps to calculate your sum insured carefully and review it over time.

Can total loss apply to contents insurance too?

Yes. A total loss can also apply to contents insurance if your belongings are damaged or destroyed to the point they need full replacement.

For example, after a major fire or flood, the claim may reach the full contents sum insured if everything inside the home is lost or badly damaged.

If you are reviewing that side of your cover too, we also have a separate calculator for contents cover.

Does a total loss always mean the insurer pays the full amount?

Not necessarily. How a total loss is handled depends on your policy wording, your policy schedule, and the circumstances of the claim. The exact details can vary between policies and insurers.

That is why it is important to read your policy wording carefully and understand what applies to your cover.

Where can you check how total loss applies to your policy?

Your policy wording explains how your cover works, what limits apply, and how claims are assessed. Your policy schedule shows the details specific to your own policy.

Reading both together will give you the clearest picture of how total loss would be handled under your cover.

Why this matters when reviewing your insurance cover

Understanding total loss is important when reviewing any property insurance cover, whether that is house, landlord, holiday home or any other kind of property insurance. A total loss is the kind of event where your cover may be tested most heavily, so it is worth making sure the amount insured still reflects the real cost to rebuild or replace what is covered.

Final thoughts

A total loss in house insurance is when a home is damaged so badly that it needs to be fully rebuilt rather than repaired. It can also apply to contents when belongings need full replacement after a major insured event.

If you are reviewing your house insurance, it is a good time to check whether your sum insured still reflects the real cost to rebuild your home today.

Related articles

- Does your home have unusual features, renovations, or non-standard materials?

- How to read an insurance policy

- Are there limits to how much I can claim for my contents?

- Factors to consider when using a house insurance calculator

FAQ’s about total loss

What is a total loss in house insurance?

A total loss in house insurance usually means the home has been damaged so badly that it needs to be fully rebuilt rather than repaired.

What is a total loss in contents insurance?

A total loss in contents insurance usually means the belongings have been destroyed or damaged to the point they need full replacement.

Is a total loss the same as a write-off?

Often, yes in general conversation. Both usually refer to damage so severe that repair is no longer practical. Generally, “write-off” is the term used when talking about vehicles.

Why does sum insured matter in a total loss?

Because in a total loss, the cost to rebuild or replace may reach the maximum amount available under your policy.

Where can I check how my policy handles total loss?

You should check your policy wording and policy schedule for the details that apply to your cover.

Does my landlord insurance cover a total loss?

Initio’s Landlord Insurance is designed to cover serious damage to the rental itself, including a total loss, on a replacement basis up to the house sum insured you select for the property, rather than just minor or partial damage.

Written by Hannah Gabbie – Initio’s Head of Support

Hannah has been with initio since 2023 and brings more than a decade of experience in fire and general claims. She joined the business as Claims Team Lead and quickly moved into the role of Head of Claims, reflecting her strong expertise and leadership in the claims space. She is a Senior Associate CIP of ANZIIF and holds a Diploma of Loss Adjusting.

Initio wins Deloitte Fast 50 ‘Fastest Growing Services Business’

Initio has been named the Fastest Growing Services Business in the 2025 Deloitte Fast 50 for the Central North Island region.

The Deloitte Fast 50 recognises high-growth New Zealand businesses that are scaling rapidly through innovation, technology, and strong market demand. A few weeks after the regional results, initio was also ranked 28th nationally across all New Zealand companies in the 2025 Deloitte Fast 50.

Quick summary

-

Initio named Fastest Growing Services Business (Central North Island, 2025)

-

Ranked 28th nationally in the Deloitte Fast 50

-

Recognised for strong growth as a New Zealand-only insurance provider

-

Growth driven by digital-first insurance and technology innovation

-

Backed by IAG NZ investment and underwriting support

The Fast 50 celebrates Kiwi businesses that are shaking things up – growing fast, breaking barriers, and doing things differently. So, to be recognised in that crowd means a lot.

What is the Deloitte Fast 50?

The Deloitte Fast 50 is an annual programme that celebrates the fastest growing companies in New Zealand, measured by revenue growth over a three-year period.

It highlights businesses that are:

-

Scaling quickly

-

Innovating within their industries

-

Building sustainable growth models

-

Contributing to New Zealand’s economic landscape

Being recognised in the Deloitte Fast 50 signals strong demand, operational strength, and market confidence.

Standing out as a New Zealand-only insurance provider

What makes this recognition particularly significant is that initio operates solely within New Zealand.

Unlike many companies in the Fast 50 that have international markets or offshore expansion strategies, initio focuses entirely on Kiwi homes and properties. Growth has been driven by serving the local market with a digital-first insurance experience built specifically for New Zealand conditions.

This shows there is strong demand for:

-

Simple online insurance

-

Real-time quoting

-

Fully digital policy management

-

Technology-led underwriting

Ranked 28th nationally

Following the regional announcement, Deloitte released the national rankings. initio was placed 28th across all New Zealand businesses in the 2025 Fast 50.

Ranking nationally reinforces that this growth is not just regional momentum, but part of a broader shift toward smarter, technology-driven services.

Growth powered by digital insurance innovation

initio’s growth has not been about speed for its own sake. It has focused on removing friction from insurance.

That includes:

-

Instant address-based quoting

-

Automated underwriting

-

Online policy management through the dashboard

-

Digital claims processes

-

AI-powered support tools

The result is insurance that works quickly behind the scenes, so customers do not have to wait on hold, fill in long forms, or deal with paperwork.

Technology backed by people

Strong technology alone does not drive sustainable growth.

The real momentum comes from the team building and improving the platform every day. From software development to claims support, the focus remains on making insurance simpler, clearer, and easier to manage.

Recognition from Deloitte confirms that a technology-led, customer-focused model can scale successfully in New Zealand.

IAG NZ partnership supports future growth

initio’s partnership with IAG NZ strengthens the foundation for continued growth.

With IAG NZ’s underwriting support and investment, initio can:

-

Expand product offerings

-

Continue enhancing its digital platform

-

Introduce new features and tools

-

Maintain high service standards while scaling

The partnership supports long-term growth while preserving the digital-first experience customers expect.

What this means for customers

Awards are encouraging, but the real outcome is improved service.

Growth enables:

-

Faster platform improvements

-

Broader product options

-

Stronger underwriting support

-

Continued investment in technology

The focus remains on protecting Kiwi homes and properties with simple, modern insurance.

Thank you to our customers and partners

This recognition reflects the trust of customers, the support of partners, and the dedication of the initio team.

Growth is not an end point. It is momentum.

Related articles

Landlord insurance and tenants – how property use affects your cover

This guide answers common questions about landlord insurance, tenants, and property use — including how family arrangements or business activities can change your cover.

Do I need to notify you when my tenants change?

You don’t need to notify us every time a new tenant moves in. But to stay covered under your landlord insurance, you must meet the landlord obligations:

- Choose tenants carefully

- Keep records of pre-tenancy checks

- Complete inspections at least every 3 months, and at every change of tenants (with written records and photos kept on file)

You can review these in more detail on our landlord obligations guide.

“Tools like myRent can help with tenant checks, tenancy agreements, and ongoing property management — it’s a handy way to stay organised and meet your landlord obligations.”

If the change involves a different type of tenancy – for example, switching to short-term guests or another arrangement that could affect your cover – please let us know so we can check you’re on the right policy wording. You can also compare our options on the ‘help me choose’ page

My family member ‘rents’ the house – what kind of policy do I need?

If a family member lives in the home and pays rent under a tenancy agreement, you’ll usually need landlord insurance. This gives you cover for things like loss of rent or intentional damage by tenants. Read more on our landlord insurance page.

If it’s a second dwelling on your property that a family member lives in permanently and you don’t want/need specific landlord benefits such as loss of rents , this usually requires a separate own home policy for each dwelling. More details are here: second dwelling – family lives in it.

Examples:

- Your brother pays rent and you want to cover that rent income → landlord insurance

- Your parents live in a granny flat rent-free → own home insurance

What if my tenant wants to run a business from my rental?

Your tenant is responsible for arranging their own commercial insurance to cover their business activities. This is separate from your landlord insurance and not something we provide. See our guide: When do I need commercial insurance?

If the business changes the way the property is used (for example, a salon, office, or childcare), it could affect whether we can provide cover. Get in touch with us if you’re unsure – we’ll be happy to review your situation with you.

Ready to make the switch to initio? Start with a quote

Related articles

- When do you need commercial insurance?

- Landlord obligations

- Have a second dwelling that your family lives in?

- Help me choose the right insurance

- Landlord insurance for multiple rentals

Preparing your home for winter

As winter approaches in New Zealand, ensuring your home is ready to handle the colder months is crucial.

Not only can a well-prepared home offer more comfort, but it can also help you avoid common winter hazards, reduce your energy bills, and prevent potential damage. Here’s a practical checklist for homeowners to get their homes winter-ready.

1. Maximising home insulation and warmth

Enhancing your home’s insulation is key to staying warm and efficient during winter. Here are crucial updates to consider:

- Quality curtains: Choose thermal or lined curtains to significantly reduce heat loss through windows, a common escape point for warmth.

- Flooring insulation: Add rugs or carpets over hardwood or tile floors for extra warmth. Consider investing in underfloor insulation for long-term benefits.

- Roof insulation: Ensure your roof insulation is sufficient and in good condition to prevent heat from escaping upwards, thereby maintaining a warmer home environment.

- Draft excluders and door stops: Use draft excluders or door stops to seal gaps under doors, particularly external doors or those leading to infrequently used rooms.

- Keeping doors closed: Keep doors shut to unused rooms to help contain heat in occupied areas, making heating more efficient.

- Additional sealing and weatherstripping: Seal any cracks or gaps around windows and doors with weatherstripping or caulking to further prevent heat loss.

2. Fireplace safety

If you have a fireplace, ensuring it is safe and ready for use is essential:

- Chimney cleaning & inspections: Have your chimney inspected and cleaned to prevent chimney fires and carbon monoxide buildup.

- Keep your wood dry: Store wood in a dry, covered area to avoid moisture, which can lead to more smoke and less efficient burning.

- Use a wood moisture meter: To ensure your firewood burns efficiently and safely, use a wood moisture meter. Firewood should ideally have a moisture content of less than 20%. Properly prepared wood reduces the risk of chimney fires, thereby preventing potential damage and insurance claims.

3. Smoke alarms and CO2 monitors

Smoke alarms and carbon monoxide detectors are vital year-round, but especially during winter when the use of fireplaces and heaters increases:

- Test and replace batteries in all smoke alarms and carbon monoxide detectors.

- Install carbon monoxide detectors near any fuel-burning appliances.

Ensure that there’s at least one smoke alarm on each level of your home, including the basement and near sleeping areas. Regularly testing and maintaining these devices can be a lifesaver, preventing catastrophic events and the associated costs and claims from fire or gas-related incidents.

4. Managing slippery decks and concrete

Slippery decks and walkways can be a hazard as frost and moisture accumulate. Here are some tips to prevent slips and falls:

- Apply anti-slip coatings to decks.

- Use sand or salt to improve traction on concrete paths and steps.

- Regularly clear away leaves and debris, which can become slippery when wet.

These measures not only ensure safety but also help prevent accidental damage to the property, reducing the need for repairs.

5. Maintain a healthy indoor temperature

Keeping your home at a healthy temperature during winter is essential for comfort and health. The World Health Organization recommends a minimum of 18°C in living areas, with higher temperatures advisable for homes with elderly residents, children, or anyone with health issues. Consider the following to maintain a healthy indoor temperature:

- Use timers on heaters to warm the house before you get up or before you return home.

- Seal gaps and drafts in windows and doors to keep warm air inside.

- Consider using a programmable thermostat for better temperature control.

Maintaining a proper temperature helps prevent issues like burst pipes and the structural damage caused by freezing and thawing, which are common winter insurance claims.

Additional tips

- Inspect your roof: Check for any damages or leaks and repair them to prevent water damage.

- Gutter cleaning: Clear your gutters and downspouts to ensure water can freely flow away from your home, preventing icicles and ice dams.

- Prepare an emergency kit: Winter storms can come unexpectedly. Have an emergency kit with essentials like flashlights, batteries, water, and non-perishable food.

These proactive steps not only make your winter more comfortable but also protect your home from potential damage, reducing the likelihood of having to file an insurance claim.

Useful links

What we don’t cover at initio

At initio, we’re all about providing clear and simple insurance solutions that fit your needs. However, there are a few types of insurance we don’t handle. Here’s a quick rundown of what we don’t currently cover, so you know exactly where we stand.

Stand-alone contents

We understand that protecting your belongings is crucial. However, initio currently does not offer stand-alone contents insurance. Contents insurance is only available as an add-on to a home insurance policy for the same address as the insured property. If you are renting and only need to insure your contents, initio does not have an option for you at this time. If you would like a quote for contents cover for your existing home insured with us, please view the add-on option/quote by logging into your initio dashboard and using the ‘change’ options.

Life products such as Life Insurance, Income Protection and Mortgagee Protection

We do not offer life or income protection insurance. Life insurance ensures your loved ones are financially supported in the event of your passing, covering expenses like funeral costs and living expenses. Income protection insurance provides a regular income if you can’t work due to illness or injury, helping cover essential living costs. For these needs, we recommend consulting with specialised providers to get the comprehensive cover and peace of mind you deserve.

Travel

Planning a trip can be exciting, but it also comes with its own set of risks. Unfortunately, initio does not offer travel insurance. This means we do not cover trip cancellations, lost luggage, or travel-related disruptions. For these specific needs, we recommend looking into specialised travel insurance providers who can offer you the necessary peace of mind for your journeys.

Medical

Health and well-being are paramount, but initio does not provide medical insurance. Whether you need coverage for regular check-ups, emergency medical care, or long-term health treatments, you will need to find a dedicated health insurance provider. Our focus remains on property and vehicle insurance, ensuring that your primary assets are well protected.

Homes in transit

Moving homes can be a stressful experience, and ensuring your belongings are covered during the move is important. Unfortunately, initio does not offer insurance specifically for homes in transit. This means we do not cover any damage or loss that might occur while your belongings are being moved from one property to another. For coverage during your move, you will need to explore options with specialised moving insurance providers or seek transit cover from a broader insurance policy that includes this specific protection.

Contract works

We don’t have a product at into for contract works. If you’re renovating and making any structural alterations to your property, a standard house insurance policy won’t cover construction-related losses. For this, you need a Contract Works policy. This specialised insurance covers both the work being done and your home against construction-related losses. This can include issues like water damage from exposed cladding or structural damage caused by the renovations.

To make this easy for you, we’ve partnered with Builtin to offer the perfect Contract Works insurance solution. With Builtin, you can ensure that your renovation project is fully protected.

Body corporates

We cannot insure properties that are owned under a Body Corporate. Our cover is designed for domestic residential houses that have a single owner. Under a Body Corporate, there is a manager that collectively is responsible for insuring all the units on behalf of each owner. This is common where there’s a large number of living units, such as an apartment block.

Commercial/Business

We don’t provide commercial insurance at this time. Our primary focus is on landlords and homeowners, ensuring your residential properties are covered with the best possible policies. Commercial or business insurance is designed to protect businesses from a variety of risks. This type of insurance typically includes coverage for property damage, liability, and employee-related risks. It can protect against losses from events such as fires, theft, and lawsuits, and can also include specialised coverage like business interruption insurance, which helps cover lost income if your business is temporarily unable to operate. For business insurance needs, we recommend seeking specialised providers to get the tailored coverage your business requires.

Vacant Lots/Land or Lots/Land with only an Outbuilding

We only insure homes you can actually live in — so if it’s just a patch of grass, a shed (or a future dream build), we can’t provide cover until there’s a house on it.

Pet Health Insurance

While we love pets as much as you do, we don’t offer pet insurance. We recommend checking with providers who specialise in this area to find the best cover for your furry friends. We do, however, cover damage caused to your property by pets.

Motorcycles, caravans, tractors and classic cars

Generally speaking, motor vehicles (including quad bikes, motorbikes, and tractors) aren’t covered under your initio contents insurance. The only exception is for small, domestic-use vehicles listed in the policy definition of contents, such as electric wheelchairs, mobility scooters, golf carts, or children’s motorbikes under 50cc that are used only off-road. If you want cover for larger or road-legal vehicles like quad bikes, motorbikes, or tractors, you’ll need to arrange a separate motor vehicle insurance policy with a specialist provider, as this isn’t something initio offers.

Boats, jet skis, and other watercraft

Our cover doesn’t extend to boats, jet skis, or other types of powered watercraft. These fall outside the definition of household contents and need their own specialist cover. If you own watercraft, you’ll need to arrange a separate policy designed for marine risks, as they aren’t included under your home, landlord, or holiday home contents insurance.

Why these limitations?

Our goal is to offer you the most effective and straightforward insurance solutions. By focusing on specific areas, we ensure that our policies are comprehensive, easy to understand, and tailored to your needs. We believe that doing a few things exceptionally well is better than spreading ourselves too thin.

What we DO cover

For pretty much everything else, we’ve got you covered! We provide a wide range of insurance options to keep you protected. If you’re not sure which is the best cover for your situation, we recommend you visit our ‘help me choose’ page. Here’s a simple breakdown of our current insurance options:

- Home and contents

- Landlord

- Holiday homes

- Multi-unit rentals

- Own home, sometimes rented out

- Two dwellings on the same property

- House flip

- Vehicle insurance (only available to current policy-holders)

What we do best

We pride ourselves on providing excellent cover for your property. Our policies are designed to be simple, effective, and hassle-free. We’re always here to help you find the best solution for your insurance needs.

If you have any questions or need further clarification about what we cover, feel free to reach out. We’re here to help!

Final thoughts

While we do cover a whole heap of things, here are a few others we also don’t cover, just in case you were wondering:

- Pet dragons – Sorry, your fire-breathing friend is a bit too hot to handle.

- Alien abductions – We haven’t quite figured out how to insure intergalactic incidents yet.

- Time travel mishaps – If your time machine breaks down in 2050, you’re on your own!

- Unicorn stables – Magical creature houses aren’t covered, but we admire your imagination.

If none of this applies to you…

Great! You’re probably exactly the kind of property owner we can cover. Getting a quote takes just a minute, and there’s no paperwork or waiting.

Get insurance

Smart strategies for premiums, excess and payment timing:

Smart moves, part II

In the second part of our interview with experienced investor Graeme Fowler, we unpack how insurance decisions can impact your bottom line, especially when it comes to excess, premiums, and payment timing.

How do you decide on the right excess?

“I always choose the highest excess available, usually around $2,000. That helps lower my annual premiums quite a bit. But if you’ve only got a couple of properties, a lower excess might make more sense.”

Graeme treats excess like any other business decision: it comes down to scale and risk tolerance. For those with larger portfolios, absorbing the occasional small cost can be a smarter long-term play.

From initio: When quoting with initio, you can select an excess from as low as $400 up to $2,000. The premium updates instantly as you adjust the excess. A higher excess = lower premium, but the right choice depends on how often you expect to claim and what you can comfortably afford to self-fund. Learn more about insurance excess: Demystifying Insurance Excess

What’s your take on how to pay for insurance?

“I always pay annually. Monthly payments might feel easier, but they usually end up costing more. Over a year, you could save quite a bit by paying in one go.”

For Graeme, annual payment isn’t just about cost – it’s also about efficiency. One payment, done and dusted.

From initio: Our quick quoting tool shows the full cost upfront, with a clear breakdown of monthly vs annual payments. Monthly might feel easier, but it comes with a life admin fee – plus, annual is usually better value. And honestly, how much is your time worth? Adjust your excess or add contents and the quote updates instantly. It’s fast, clear, and makes insurance simple.

How do you view insurance as part of your overall investment strategy?

“It’s one of those things that, if you get it right, saves you money quietly in the background. If you get it wrong – or ignore it – you’ll know about it quickly.”

Graeme treats insurance like any other portfolio tool: it should be optimised, not just set and forgotten. Managing excess, timing payments smartly, and locking in renewal rates all contribute to a more efficient portfolio.

From initio: With our digital platform, you can manage all your policies in one place – tweak cover levels, update payment settings, and renew when it suits you. We also send early renewal reminders and show any pricing changes upfront, so you can stay ahead of known levy increases.

Coming up next in the Smart Moves Series:

Common landlord insurance mistakes – and how to avoid them.

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Related support articles:

When do you need commercial insurance?