Search results for: {search_term_string}

Covering yourself for an unexpected event that leads to damage and financial loss is exactly what insurance is for. For house and contents insurance, you are most likely to think of your typical risks that might include fire, property flooding or theft of contents. However, insurance goes much further the ‘usual’ losses.

At initio we come across our fair share of unusual claims. As part of our ‘2019 in Review’ we go over our top 5 most unexpected claims – with a few honourable mentions. We are calling this the ‘Annual Initio Claims Awards’

Expect the Unexpected?

#1. Runaway Trailer

Sometimes damage can come from something outside of your control and your property. In late 2019, an initio customer in Te Awamutu was taken by surprise by a runaway trailer. Concrete was being laid at the building site next door and one the contractors loaded trailers became unhitched. The trailer was sent rolling down the hill and ended its journey by colliding the corner of our customers house and garage door.

This resulted in significant damage to the interior lining, exterior cladding and the garage door. Lucky for the insured their vehicles were not parked in the garage at the time, however a shelving unit and set of golf clubs were also destroyed. Saturday golf was put on hold unfortunately.

Total claim cost $19,187. In this instance, the concrete layers public liability insurer was pursued for the costs of this claim.

# 2. Colouring-in competition

When a customer rented their holiday home to short term guests they were not counting on their TV taking part in a kids colouring competition. The guest’s toddler thought they would hone their colouring in skills on the large flatscreen TV.

The artistic crayon drawings were cleaned off but the hard crayons left permanent scratches across the screen that could not be removed. A claim was made under their ‘landlord-holiday home contents’ which meant that the homeowner was able to replace their TV.

#3 . The Phantom Bather

An initio client with a multi-unit rental property was expecting it to be unoccupied for eleven days between tenancies. Two days into the property being untenanted, they received a call from their neighbour to say that there was water coming out of the property. It appeared an intruder had entered the property gone up the stairs and decided to run a bath.

Extensive water damage included saturated carpet upstairs that then seeped through the floor to downstairs. The ceiling in the kitchen and dining room downstairs collapsed, and significant water damage and clean-up was required through the property.

While we don’t know what the motives were for running the bath, we know that the landlord was happy to have an initio landlord insurance policy come to the rescue. With further costs still to come in the claim cost of repairs so far exceeds $32,000.

#4 . Rampant Puppies

After a tenancy had ended at an initio rental property early in 2019, an initio client lodged a claim for damage to the underfloor insulation. When repairers investigated the cause of loss, it appeared that the previous tenants family of puppies had found their way under the house, and shredded the flooring insulation from below.

Unlike many domestic insurance policies in New Zealand, the initio landlord insurance policy does not exclude damage caused by pets. After the landlord’s excess, Initio paid out $2,225.16 to repair and reinstate the insulation.

#5. Clumsy Chopping Board

While renting a holiday home, the guests popped down the road only to return to water running out the front door. They certainly didn’t expect to find water everywhere, a swelling to the kitchen, kitchen bench, cupboards, walls and floor.

It turns out that while they were out of the house a bread chopping board fell from its stand and landed on the sink tap. Not only did this turn the tap on, the awkward way it landed meant it also redirected the water away from the sink, running down the bread board and into the kitchen cabinets.

The aftermath damage resulted in water damage to the kitchen structures, damage to electrical components, and loss of rent payments as the sodden kitchen meant the property could no longer be rented. Total repairs amounted to $21,151.38 and are covered as sudden accidental water damage under the customers initio holiday home policy.

2019’s Honourable Vehicle v House Mentions

From AirBnB guests throwing a party to lightning strikes – we have had some interesting ‘honourable mentions’ lodged throughout the year.

Six claims were lodged with initio in 2019 for vehicle damage to properties – where a member of the public lost control of their vehicle and damaged our customers houses.

Three were involved in a police chase, whilst a further two were caused at the hands of drunk drivers.

Drivers who are responsible for damage caused are liable to cover the costs of repair. However in reality it’s difficult to get those responsible to accept liability (especially where it involves a police chase or drunk driving). Regardless of the driver accepting responsibility or being insured themselves (not that they would have insurance if drunk or in a police chase) initio provides cover for the damage caused to the property. We then pursue the driver.

The average claim for vehicle house damage in 2019 was $4,761.

‘Expect the Unexpected’ – You never know what could happen to your property. This is why it’s best to make sure you are covered for such unexpected and unusual events.

For more information on insuring different types see our insurance covers designed specifically for:

Home Insurance – for your own home, and contents.

Holiday Home Insurance – for the bach and for holiday homes that are also rented out (eg Bookabach, AirBnB)

Landlord Insurance – all in one house and landlord insurance, including loss of rents, malicious damage & more.

Christmas is the busiest time of year …. for burglars. House insurance is just one part of managing your house and contents risk. Heres a guide on protecting your property.

It’s coming into that time of year where we like to take a load off – relax for a couple of weeks, put the feet up at the bach, or even head off overseas – but it’s also the time of year when burglars tend to be more active. Leaving houses empty for periods of time can be risky in several ways, and among other factors, result in an uptick of property insurance claims. We’ve all seen Home Alone!

Holiday homes are particularly vulnerable as they are often left unoccupied for extended periods of time, but even our own homes need to stay secure and damage-free over the silly season.

Burglary prevention is equally important for holiday homeowners, landlords, and people with a single main residence. Importantly, burglary isn’t only about having your contents stolen, but also the fact that thieves can cause significant damage to other possessions and the property itself whilst trying to gain access.

Property insurance cover is designed to protect you if the worst should happen, but as a property owner there are several steps you can take to avoid having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy.

Prevent opportunistic burglars from targeting your property by:

- Keeping all valuables out of sight. Gifts under the tree are tempting for thieves so make sure they, and other valuables, can’t be seen from the outside the home. Also be careful when disposing of any tell-tale packaging

- Checking window joinery, and promptly replacing or repairing any loose latches

- Installing security stays on windows

- Fitting deadlocks or deadbolts to all external doors, especially older doors and ranch sliders which can be more easily broken into

- Installing a burglar alarm and advertising the presence of an alarm

- Installing exterior sensor lights, and checking any existing lights are working correctly

If possible, make it difficult for someone to break into your home. Trim trees and shrubs so there are no places for burglars to hide and move wheelie bins and other large objects away from fences, ledges and drop-offs wherever possible. Lock your shed and put away any tools, to remove the temptation of them being used to aid access.

Something else to consider is not advertising that you are away: keep your lawns mowed, gardens tidy, the mailbox clear and avoid leaving messages on social networking sites and answering machines with dates and other specific details of your absence. Let your neighbours know if you’re going to be away, give them your contact phone number, and have if you a good relationship with your neighbour – ask them to clear your mail, or park in your driveway to keep up the ruse.

Good security makes people feel safe; it also has the added benefit of retaining good and long-term tenants – and for holiday homes, a reputation for a safe and secure property.

This week, law changes to the Residential Tenancies legislation is set to strengthen renter’s rights. It aims to transition a landlord’s rental house into a tenant’s home.

Looking specifically at landlord insurance, the change that will have the most ramifications on landlord insurance is the removal of no-cause evictions. Essentially, it will be more difficult for landlord’s to remove bad tenants and from a risk management perspective this is not a good thing. Other changes to the legislation such as limiting rent increases, and banning rent bidding are unlikely to have a direct impact on landlord insurance.

Landlord insurance provides cover for intentional damage by tenants. If troublesome tenants are harder to remove then landlord insurers will consider that there is a higher risk that the tenant will cause damage to the property. It remains to be seen but this could lead to an increase in the value of deliberate damage insurance claims. Working out how and when the damage occurred could be further protracted when there is a tenant that is unwilling to co-operate and cannot be removed from the property. It has always been about working with the landlord, the tenant, and the property manager (if applicable) and this will not change when it comes to insurance.

While tenant damage could increase under the new rules, the legislation changes could in fact improve risk management and reduce the incidence of damage. Our view is that with bad tenants being hard to evict, it will mean that landlords increase their scrutiny during tenant selection. So, ultimately tenants with a poor record and lack of supporting references may find it harder to get rent a property, which would filter out bad tenants and lead to lower claims payouts for insurers.

The ultimate outcome of the law changes is difficult to predict. It is unlikely that insurers will make any adjustments to premiums or policy conditions as a result of the reforms.

The bulk of the legislative changes are set to be put into practice in early 2021. We expect that it will take at least 12 months before we see any outcomes or trends on claims.

About Initio

Initio is a New Zealand-based online house insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home and contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with built-in cover for loss of rent and damage by the tenant.

Having completed over 35,000 automated insurance transactions, Initio’s market-leading policies can be quoted, bought and amended online – all in an instant.

Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

A candid take on initio’s approach to you and your home

At initio we are ‘all-in’ on customer experience. We ruthlessly pursue customer satisfaction with our technology, support and communications …. But only for a certain type of customer. In short, we are not for everyone.

Yes, we’re audacious enough to say: “Sorry, we can’t be your insurance provider” – at least not if it means compromising the ethos that underpins our brand, or transacting with you in a way that doesn’t celebrate the use of our tech. We provide superior ease of insurance and customer service, but only to a specific kind of customer who appreciates and respects our ‘digital by default’ approach.

Catering to the Modern, Digital-Savvy Customer

Our business model is laser-focused on a modern, self-reliant breed of customers. The digital age has dramatically reshaped the insurance industry, and initio remains at the forefront of this transformation. We are designed for customers who value autonomy, speed, and convenience, rather than the traditional, hands-on approach.

Customers who are comfortable transacting online, managing their property portfolios with digital tools, and who comprehend that competitive premiums and high-touch hand-holding services are often mutually exclusive, are our ideal clientele. For these customers we are digital by default, and human when you need us.

The Interplay of Technology and Affordability

“Why can’t you just start the policy for me over the phone”

“Why don’t you call me every year when my policy renews so we can have a chat about it”

“Why can’t you just send me your bank account and I’ll transfer the premium funds”

“Send me a quote”

It’s a ‘no’ on all fronts. The truth is, high-touch insurance services involve considerable operational costs – think travel, long-winded phone calls, time, and administration. We’ve spent over 10 years building a digital platform that substitutes for these things; its frictionless insurance, that’s quote in one click, cover in 2 minutes, claim in an instant. By utilising technology to automate many aspects of our services, we increase efficiency and are able to offer competitive pricing.

Our system has been designed to suit a certain type of customer, and it’s not for everyone.

This doesn’t mean we shirk our responsibility to our customers that embrace our technology. Quite the contrary – we provide comprehensive digital and phone support, and abundant online resources to help.

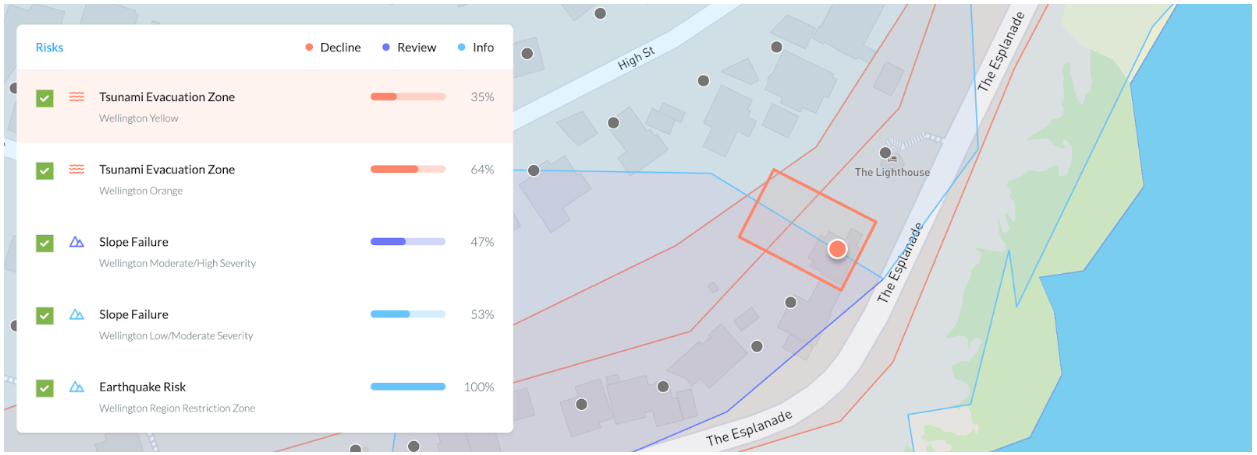

Why we decline to insure some houses

Sometimes we have to say no to insuring your house. It’s not you, or your house, it’s simply the way we want to run our business and the rules we, and our insurer, have had to create to be able to offer our services long-term.

It’s digital too: The primary decision making on whether or not to insure your property is done by a smart tool we built called ‘Locatio’. When you type in your address with initio, Locatio makes decisions about whether initio can provide cover by using things like council property data, flood maps, earthquake and land risk.

In order to remain a sustainable and successful insurance provider we choose to focus on certain types of houses, and this means that there are some locations where we can’t provide cover, and certain risk exposures such as flood or land instability that are just not our bag.

We are constantly updating our business and underwriting rules, so just because we say no today, doesn’t mean that it’s a no forever.

You also need to know that we cannot sell you something that isn’t right for your situation either. So if your property does not fit our product we’ll decline to provide cover, and we don’t mean any offence by this.

The cost is the cost

A number of factors go into calculating the total cost of your home insurance, including location, age of the property, and other things like government-imposed levies. Our award-winning insurance technology computes the insurance cost, and we rely on that to run our business. The premiums need to be set at a level that allows the insurer the margins to continue to pay claims and reinsurance costs. In short, the cost is the cost.

Learn more about how the insurance risk component of your insurance cost is calculated

It’s 100% your choice whether or not to accept the insurance cost we offer. You can ring or email and challenge a cost but ultimately it’s out of our hands as the system has spoken. You need to know though that we work incredibly hard to maintain competitive premiums for our customers. We do this by continually investing in our technology for efficient processes, negotiations with our insurer, constantly refining the rules that determine how risky our portfolio of houses is (ultimately the more aggregated risk we take on, the bigger our premium pool needs to be).

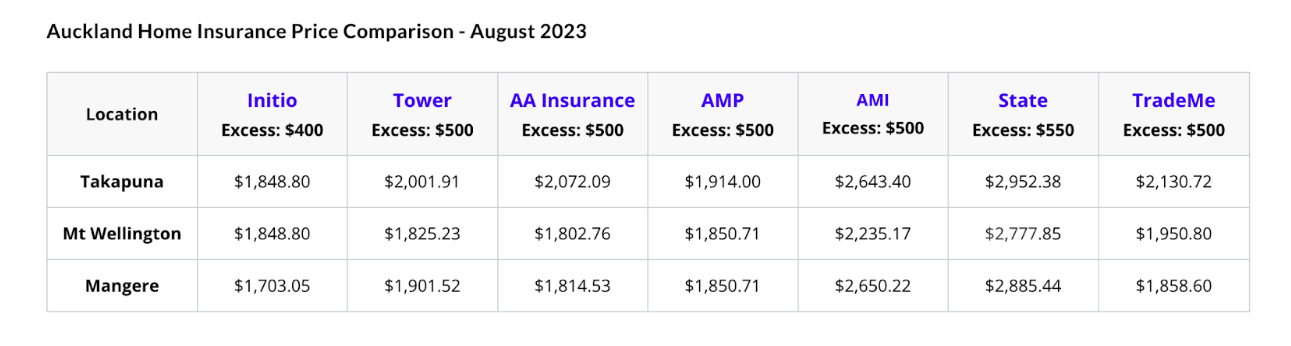

Our efforts to keep premiums competitive have been confirmed by feedback from our customers and also by financial resource websites like Moneyhub.

Source: Moneyhub

It’s simply not possible to be the most competitive all of the time, and we implore our customers to take a long and holistic view of their insurance that takes account of things like support (can you get you easily get ahold of your insurer), claims responsiveness, ease of use, technology and overall confidence in your provider.

It’s worth bearing in mind that not all policies are built the same, so just comparing price vs price doesn’t quite cover it. We highly recommend using our comparison tool if you want to see how we stack up when you also take the policies into consideration.

An Unapologetic Philosophy

Our philosophy is blunt but honest: “We are not for everyone”. Our model isn’t all things to all people, and that’s intentional. We’re looking for customers who align with our ethos – those who want a superior digital service.

While we understand some may expect more traditional customer service methods, we respectfully suggest they may be happier elsewhere. This is not a dismissal, but a candid admission that our service model may not suit everyone’s expectations.

In sum up, initio is unyieldingly committed to delivering our unique brand of customer experience, one that is unabashedly shaped by the needs of modern, digital-savvy customers. While our approach may not resonate with everyone, we are firm in our refusal to compromise on the affordability and efficiency that our model provides.

To our customers who find value in what we offer, we welcome you wholeheartedly. To those who don’t, we don’t hesitate to say: “We are not for you” And that’s how we maintain the balance that allows us to continue delivering what we believe is the optimal blend of service and affordability in today’s market… all driven by our technology.

Loss of rent insurance helps protect your rental income if your property cannot be lived in or your tenant stops paying rent. Under initio’s landlord insurance, loss of rent cover is included automatically. This guide explains when it applies, how much cover you get, and what is not covered. This can also be included in our holiday home cover if you also rent your bach to guests.

Quick summary

-

Loss of rent is automatically included with landlord insurance.

-

Standard cover is $20,000, with options to increase to $40,000 or $80,000.

-

Cover applies if damage makes the property uninhabitable.

-

Cover may also apply after tenant eviction or abandonment.

-

Overdue rent before eviction is not covered.

-

Holiday homes have cover for cancelled guest bookings due to damage.

What is loss of rent insurance?

Loss of rent cover replaces rental income when you cannot collect rent due to certain insured events. This usually happens when:

-

Damage makes your property unliveable, or

-

A tenant is evicted for non-payment, or

-

A tenant leaves without notice.

It helps reduce financial pressure while you repair the property or secure a new tenant.

How much loss of rent cover do I get?

Landlord insurance includes $20,000 of loss of rent cover as standard.

You can increase this to:

For property damage claims, payments stop when:

-

Repairs are complete and the property can be rented again, or

-

You reach your selected cover limit, or

-

12 months of rent has been paid,

whichever happens first.

When does loss of rent cover apply?

Property damage that makes the home uninhabitable

If claimable damage means your tenants must move out, loss of rent cover replaces the rental income during repairs.

Example: A flood damages carpets and internal walls. Your tenants move out while repairs are completed. Loss of rent cover replaces the rent you would have received during that period.

Cover is paid until the property is liveable again, up to your selected limit or 12 months.

Tenant eviction for non-payment of rent

If a tenant is more than 21 days behind in rent, you may apply to the Tenancy Tribunal for eviction.

Once the tenant is evicted, landlord protection under your policy can pay up to 6 weeks of rent, or until you find a new tenant, whichever comes first.

-

Overdue rent (arrears) before eviction is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations under the policy.

Tenant leaves without notice

If a tenant vacates the property unexpectedly and stops paying rent without giving the required notice, the policy can pay up to 6 weeks of lost rent, or until a new tenant is secured, whichever comes first.

-

Normal vacancy between tenancies is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations.

Does loss of rent apply to holiday homes?

Yes. If you rent out your holiday home to paying guests, loss of rent protection is included.

Holiday home damage and cancelled bookings

If claimable damage makes the property uninhabitable, we will cover lost rental income from cancelled guest bookings.

You automatically receive:

Payments may consider:

-

Confirmed bookings that must be cancelled.

-

Expected future bookings, using previous rental income history where appropriate.

The maximum payment is your selected limit or 12 months, whichever comes first.

What does not apply to holiday homes?

The 6-week tenant eviction or abandonment benefit does not apply to holiday homes, as short-term guests do not have formal tenancy agreements.

What is not covered?

Loss of rent cover does not include:

-

Rent arrears before eviction.

-

Normal vacancy between tenants.

-

Guest cancellations unrelated to claimable damage.

-

Eviction benefits for holiday homes.

Always ensure you are meeting your landlord obligations under the policy.

Frequently asked questions

Does landlord insurance cover unpaid rent?

It may cover rent after eviction or abandonment, but it does not cover overdue rent before eviction.

How long is loss of rent paid for?

For property damage, up to 12 months or your selected limit. For eviction or abandonment, up to 6 weeks.

Do I need to add loss of rent cover separately?

No. It is automatically included in landlord insurance and holiday home cover (if rented).

Related Articles:

For any new tenancy agreement signed after 01 July 2021 your property will legally have to comply with all five Healthy Homes Standards within the first 90 days.

To keep on top of things here’s a reminder of what the changes mean, and what’s required.

The changes

Any new or renewed tenancy (whether it’s fixed term or periodic) in effect after 01 July 2021 has just 90 days to be fully compliant with Healthy Homes. For example, if new tenants move in on 01 July, you’ll have until 01 October to make the necessary changes.

Does your rental meet the five standards?

Heating Standard

At least one built-in heater capable of heating the main living room to 18°C or more.

- Some types of heaters that are unhealthy, too energy inefficient or unaffordable to run won’t meet the requirements.

Insulation Standard

Meet minimum requirements for insulation levels in ceilings and under-floors. Levels required depend on what part of the country the property is in (zone 1, 2 or 3).

- Insulation installed before 01 July 2016 acceptable under 2008 standards, and

- Insulation installed after 01 July 2016 acceptable under current, post 2016 thickness levels.

Learn more about the different levels for the three zones here.

Ventilation Standard

An extractor fan that vents to the outside (not another room), in all kitchens & bathrooms. They also need to meet some performance and size levels.

Open-able ventilation (like windows) to the outside in all liveable parts of the house. Size of windows is more than 5% compared to the size of the room they are in.

Drainage and Moisture Standard

Able to manage and drain normal rainfall levels. This includes working gutters, downpipes and drains for water flow.

- Houses with a closed off sub-floor (area beneath flooring) need a barricade to stop water flowing in, where feasible.

Draught Standard (air-type)

Air tight with no gaps that cause noticeable airflow into the house.

- Unused fireplaces are airtight, unless there’s an agreement with tenants otherwise.

What’s the penalty?

If you haven’t already, now is a great time to make a start. If you don’t comply and there’s tenants living in the property, you’re at risk of getting a penalty of up to $4,000 (per property). Anyone can claim a breach, including your tenants. If you haven’t already, the time’s now to make the changes to avoid future problems with your tenants.

Please Note: This is simply a summary of the five standards. To get the full details and piece of mind, we recommend going to the official Tenancy Services’ Guide.

Key takeaways in this article

-

A self-contained dwelling must have facilities to cook, sleep, live, wash, and use the toilet.

-

These facilities do not have to be in one building, but they must be for the exclusive use of that home.

-

Shared facilities usually mean the property is not self-contained.

-

Most home or landlord policies cover one self-contained dwelling only.

-

If your property has more than one self-contained living area, you may need separate policies.

Is your property considered self-contained?

To be self-contained a premises must contain the facilities necessary for day-to-day living on an indefinite basis. There must be somewhere:

• to cook;

• to sleep;

• to live;

• to wash; and

• to carry out ablutions.

The facilities needed to live in a self-contained manner do not have to be in one building, but must be for the exclusive use of the dwelling.

For example, a property may have an external ablutions building in the grounds. As the whole property has the facilities to enable the people using the house to live in a self-contained manner, and the facilities are not shared with other homes, this property will be self-contained for NHC (Formally EQC) cover purposes. NHC is the Natural Hazards Commission.

How this affects your insurance cover

A typical home or landlord policy is designed to cover one self-contained unit being used as a dwelling either by the owner or a long term tenant (over 90 days). If you have a second self contained area at the property also used as a home, you may need a second policy, please check out our support page here to assist with determining the correct cover for you.

Related articles:

Our house flip cover is designed for short-term cosmetic renovations. If you’ve got a do-up project that’s liveable, in reasonable condition, and just needs a refresh to get it market-ready, this policy is ideal.

We can cover homes that:

We cover cosmetic renovations — things like painting, new carpet, or replacing fixtures.

We don’t cover structural alterations — so it’s important to know the difference before purchasing this policy.

If you’re planning work that involves changing the structure of the home, you’ll need a separate contract works policy.

Is your project suitable for initio’s Flip Policy?

Works covered by a House flip policy

Cosmetic Renovations

If you’re doing cosmetic renovations to your house (with no structural alterations) you can place cover under a House flip policy.

What’s considered ‘Cosmetic Renovations’?

Cosmetic renovations are work that doesn’t involve structural alterations or changes to the house. Some examples that are covered by the House flip cover are:

- Painting (outside and inside)

- Installing new carpets

- Replacing a toilet

- Removing a non-load bearing wall

Works that won’t be covered by a House flip policy

Structural Renovations

The House flip cover is not designed to cover work that involves changes to the house’s structural make-up. This kind of work should be covered by a separate contract works policy on the house.

What’s considered ‘Structural Renovations’?

Some examples of structural work are:

- Re-roofing

- Building a new extension to the house

- Removing a load-bearing wall

- Re-cladding the house’s exterior

Note that this isn’t an exhaustive list. If you’re still unsure if the work you’re doing is structural, please get in touch.

Doing Structural Work and need contract works cover?

For a specialist online contract works solution we’re partnered with BuiltIn Insurance. BuiltIn are New Zealand’s trade insurance experts and have an online Contract Works insurance offering where you can get a quote for your works online, and purchase online too.

Like initio, BuiltIn are underwritten by IAG so this means that you will have the same ultimate underwriter for the house and contract works risk, which is important.

Looking for more information?

When you have had claims you may have to pay more premium on your insurance. Don’t be offended, insurance companies are just trying to automatically place a price on the risk of the driver. In insurance driving this is called ‘pricing risk’.

Car insurance is a bit different to house insurance in that when you claim on your house insurance the vast majority of the time it is something outside of your control, like a storm blowing your roof off or a burst water pipe.

However, the typical car insurance claim does have something to do with the driver of the car. While it’s not always the case, the driver (and policyholder) can be at fault if they lost control of the car and crashed.

Naturally, some drivers are more likely to have accidents. For example, young inexperienced drivers are more likely to crash than a middle aged driver in say their 40s. Insurance companies will price this difference into their base premium rate calculation.

Even within these groups (i.e. under 25 year old drivers) there are subgroups of drivers that are more prone to accidents.

In general insurance companies try to balance long term claims payment trends between good and bad drivers. If someone uses their policy more and is paid out 1 more insurance is it fair that they pay the same premium as someone that has never made a claim?

The way insurance companies try to gauge this is by assigning a Driver Grade to the person applying for the cover.

This is what they are trying to do when they ask you to disclose how many car insurance claims you have had in the last five years.

Why do we only care about claims in the last five years?

Don’t worry, we (and most insurance companies in general) know and expect that the average driver is going to have a car insurance claim in their lifetime.

People’s driving habits change over time so how you drove 20 years ago is not likely to be reflective of how you drive today. Insurance companies realise it’s unrealistic too look too far back into the past. Someone that had three accidents all over 10 years ago does not reflect their driving today.

Therefore you will only be asked about claims in the last five years. If someone has had 3 accidents or claims in the last five years there is a good chance the driver is more dangerous than the average.

Do I pay an excess when I am not at fault?

If you are at fault for an accident, or admit liability you will need to pay your policy excess on your insurance payout.

If you are not at fault, and you have the details of another party who caused the crash and who admits liability its unlikely you will have to pay an excess.

Some particular items of your policy may not have an excess that applies to the cover. Examples include theft, or windscreen damage. You should check your policy for these.

In all other cases it’s most likely that you will have to pay your excess even if you’re not at fault. If you have a crash with another driver, but you are unable to get their details there’s no definitive proof of who was at fault, and you will generally have to pay the excess on your policy.

How do Insurance companies apply the Driver Grade?

Some insurance companies will ask you to only disclose claims where you were ‘at fault’. We ask you to disclose any claims where you were either at fault, or paid the excess on the policy. We are not saying that every claim where you have paid the excess is one that is your fault, but we are trying to offset and balance premiums between those that have used their policy for payouts, and those that have not. It’s only fair.

Login in to make a claim

Related Articles:

We currently offer Landlord insurance, Landlord insurance for multiple attached units, Own home and contents insurance, House flip insurance, Car insurance, Holiday home insurance and we also have an add-on for Short term paying guests insurance (e.g. Airbnb) for your home or holiday home.

All our policies are underwritten by IAG New Zealand Limited (IAG). IAG has received a financial strength rating of AA from Standard & Poor’s (Australia) Pty Ltd, an approved rating agency. Learn more about financial strength rating.

We’re constantly working on new and exciting products and features that are designed to improve our customers experiences. We would love to hear your feedback.

Get a quote

Related Articles:

Navigating the intricacies of insuring a home with an attached flat in New Zealand, especially one that is rented out part-time, can be overwhelming for landlords and property investors. At Initio, we are dedicated to helping you make sense of these complexities, equipping you with the tools needed to make the right insurance choices for your unique situation. This article is specifically designed to assist you in understanding the process for homes with attached flats rented out occasionally.

Guidelines on Insuring Your Home and Attached Flat in NZ

If you happen to own a home with an attached flat rented out occasionally, you may find yourself unsure about how to secure the right insurance coverage. This situation differs from one where both units are exclusively used as long-term rentals (which are catered for by our multi-unit policy). Insuring a property where you live and have an attached flat rented out part-time necessitates a more nuanced approach.

Here’s what you need to know:

- Own Home policy: This policy has been crafted to cover the portion of the property that you inhabit.

- Landlord/Rental policy: This policy needs to be put in place to provide coverage for the attached flat when it’s rented out. Even if the rental isn’t full-time, coverage for the times when the flat is tenanted is ensured by the landlord/rental policy.

Should a significant claim arise, both policies would be engaged, with the combined sum insured being applicable to the whole property.

Why do I need Two Policies?

Each policy is designed specifically to cover one self-contained home/unit only and for the risks associated with the type of occupancy. The Own Home policy provides coverage for the main house/unit where you live, while the Landlord/Rental policy covers your rental home/unit including the legal liabilities and other specific risks associated with renting.

Conclusion

The process of insuring a home with an attached flat, rented out on occasion, needn’t be a difficult one. With an understanding of how Initio’s insurance products can be strategically combined, comprehensive protection of your property is ensured. Additional information on this topic, as well as other insurance solutions offered by Initio, can be found here.

Get a quote

Useful links

A closer look at property damage for New Zealand Landlords

Rental properties, for all their promise of steady income and long-term value can, if not managed correctly, become ground zero for an array of unforeseen problems and potential hazards.

The reality is that damages, an often neglected aspect of rentals, pose a considerable risk to your investment. These risks are as varied as they are prevalent, raising a pertinent question in the minds of property owners: “What damage is most likely to occur at my rental property?”

Safeguarding your investments and mitigating potential losses, and understanding these risks is essential to success as a landlord.

A thorough examination of our 2022 loss data provides a detailed analysis of the challenges faced by New Zealand property owners. Last year, claims related to rented properties — including traditional rental properties, own homes partially rented, and properties with multiple rentals, made up 35% of all the claims we received. When focusing on these rental-specific claims, we identified a broad spectrum of loss types, which we’ve classified below in terms of number of claims:

Water-related damage: At 21.6%, this was the most common type of damage. These losses typically involved scenarios including suddenly bursting pipes and rodent damage, while blocked pipes accounted for 6.4%.

Accidental damage: This category, representing 18.1% of the claims, includes an array of unexpected incidents, from minor mishaps to substantial accidents, illustrating the diverse risks property owners encounter. The losses range from outdoor misadventures, such as balls shattering windows or trees falling onto the property (while being pruned), to indoor accidents like stains on carpets and damaged rugs, often due to spills or pet-related incidents. There were also multiple kitchen bench damage incidents – caused by hot pots.

Weather-related damage: Severe weather events substantially contributed to the claims we received, with flood-related incidents constituting 11.2% and wind-induced damage representing 9.9% of the total claims. These statistics do not include the severe flooding and storms experienced earlier this year. Weather damage events are hard for property owners to mitigate.

Other incidents: Some more specific types of damages also occurred, albeit less frequently. These included

- Malicious damage by tenants (4.6%),

- Fire – accidental or unknown reasons (1.1%),

- Meth contamination (1.5%),

- Issues with keys and locks (3.5%),

- Impact damage, typically involving a vehicle (5.5%) eg car versus house

Loss of rent: There were several circumstances that led to a loss of rental income, resulting in insurance claims. Property damage rendering the property uninhabitable was one such factor and is the most common.

However, issues such as tenant abandonment, non-payment of rent, and eviction also significantly contributed. These loss-of-rent-only situations accounted for 3.3% of the total claims made.

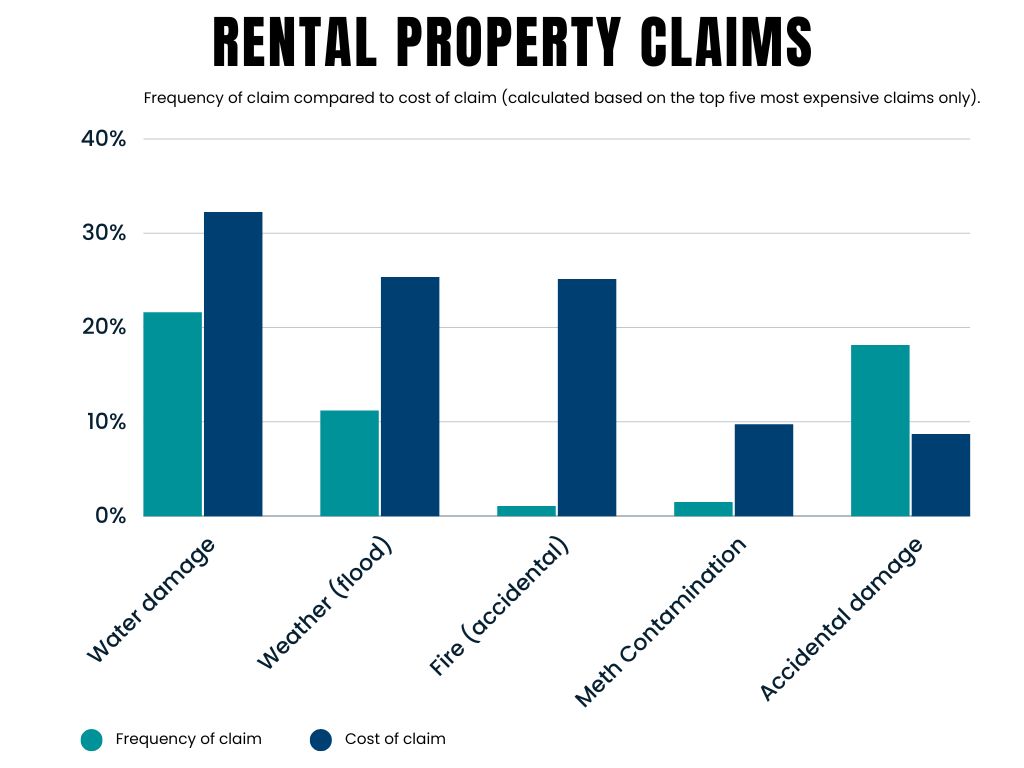

Frequency of claim vs. cost

The above numbers are based on frequency (i.e number of claims made). We also analysed the payout values for rental property claims. The graph below shows the top five losses by value. This data is presented alongside the frequency of each of these claims. It illustrates that losses like fire are uncommon but are high in value.

Fire-related claims constituted a mere 1.1% of the overall number of rental property claims, but made up 25% of the total value of claims paid. This underscores the potential devastation that fires can cause to rental properties. The significance of this cannot be overlooked, highlighting the importance of equipping your rental properties with smoke alarms, and fire extinguishers. By taking these simple proactive measures, you can significantly reduce the risks associated with fires and safeguard your valuable assets and your tenants.

Final word

Understanding the potential risks involved in rental property ownership can help landlords to better prepare for and protect their investments.

Proactive and pragmatic management of landlord risk is a form of insurance in its own right. In our experience, with the losses we see on a daily basis, a landlord that focuses on tenant selection, tenant vetting, regular property inspections, fire extinguishers in kitchens, regular maintenance including plumbing and electrical checks will outperform and not contribute to the statistics in this article.

Choosing an insurance provider that knows landlord insurance and who provides an insurance policy that is dedicated to the diverse needs of rental property owners is the icing on the cake for a well-rounded risk mitigation approach to landlording.

Learn more about initio’s Landlord insurance cover

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2022, spanning our entire claims portfolio. Please note that all figures are approximate and have been calculated to provide a representative view of the claim trends during this period.

Can I insure my boat with initio?

No, we do not provide boat and/or marine insurance products.

Can I insure my motorcycle with initio?

No, we do not provide motorcycle insurance.

Can I change my payments from monthly to annual at renewal?

If you wish to change from monthly to annual (yearly), please take out a new annual policy from your initio dashboard and then cancel the original monthly policy. The system will also automatically arrange a refund for any unused portion of the monthly policy.

If I’m going to rent out one of the rooms in the house I live, do I need to get a landlord insurance policy?

If the boarder/tenant will be sharing facilities with you, such as kitchen and/or bathroom, then you will not need a separate policy. Our “Own Home, that’s also rented” will suit that purpose.

If the area they will be living in is self-contained (either attached to or separate from the main dwelling) with it’s own facilities, to the extent that they don’t share rooms/areas with you, then you will need to take out an additional landlord policy for that part of the property. That policy would be in addition to your Own Home policy for the portion of the home that you occupy. Together, both policies should make up the total sum insured required over the whole property.

Can I pay for one or some of my policies using a different credit card?

If you are purchasing annual insurance, you can use a different card for each and every purchase. If you are purchasing monthly insurance, we are only currently able to facilitate one card for any monthly payments under your account. If you wish to use a different card for a monthly policy, you will need to set up a new initio account using an alternative email address for any policy to be paid via the new card.

How do I login?

If you are a current policy holder already with initio you will have an initio dashboard where you can manage your insurances. You will have been emailed your login details following your first purchase with initio. Please login to your initio account here.

Your email is the first login credential required, followed by your password. If you can’t recall the email you used when you purchased your policy, please contact initio staff.

If you’ve forgotten your password, click the “Forgot my password” option to reset it. Simply follow the instructions to complete the process.

Please note that logins are only provided upon purchase of a home policy with initio.

Where do I find my renewal invoice to pay?

We don’t send invoices for the upcoming year in the traditional sense, if you are looking for the cost to renew your annual policy for the upcoming year, you can find that information by using the “review & confirm” button on the relevant policy. More information regarding that can be found here.

Once the renewal has been completed and paid, the paid invoice information is immediately emailed to you and is thereafter available on your initio dashboard for viewing. All of your historical Invoices/Receipts will remain available via your initio dashboard.

How do I determine the amount of replacement cover to take for my home? Does the amount of replacement cover includes demolition costs?

Please refer to our support page here for your home and here for your contents.

Which cover should I choose to insure my rental?

To insure a rental property set up as one self contained dwelling that you lease to tenants on a long term residential lease, please use our Landlord policy. We also have a multi-unit landlord cover for small blocks of flats or if you own more than one connected rental unit.

If I hire a car, does my vehicle policy insure the hired car?

No, your initio policy does not cover the hire vehicle, we recommend arranging cover with the hire company.