Search results for: {search_term_string}/house-flip-insurance/house-insurance

Float Mortgages

Vega

New Zealand Pathfinder

Online Insurance at its best

Transacting your insurance online does not get much better than with initio. We just want to make it as easy as possible; no unnecessary forms to fill out or paper wasting documentation to clutter your house. Judging by the number of policies the website is transacting it certainly looks like people are enjoying our approach.

You will notice that one of the major benefits of this online approach is that we can provide our exceptional cover at very very competitive prices. Online rental property insurance is just the beginning; we hope to bring you domestic house insurance and contents insurance soon. And all online as they should be.

Technology you can trust

Instant, reliable quotes you can count on

They say AI might take over the world someday, but for now, we’ve put it to work making your life easier – one insurance quote at a time. At initio, we’ve spent countless hours perfecting our technology so you can get a home insurance quote faster than you can say, “robot overlords.”

Simply type in your address, and our advanced system gets to work, drawing on resources like flood mapping tools, council records, and the latest data to deliver a reliable, competitive quote instantly. We can quote most New Zealand properties on the spot, there’s just the occasional scenario where the property might get referred. For more information, you might like to check out our support articles: insuring old houses and five tips to insuring in a flood zone.

Other insurance providers might claim they can give you a fast quote, but none are as quick or accurate as initio. After extensive research, we’re confident no other provider matches the speed and precision of our platform, but that’s just our opinion, feel free to try it for yourself.

No tricks or gimmicks

With initio, what you see is what you get. When you use our platform, the price displayed is the price you’ll pay – no surprises. Whether you’re insuring a house, rental property, or holiday home, our quotes are consistent and accurate.

While some providers might adjust their pricing based on how you contact them or bundle other policies, initio does things differently. We focus on transparency and simplicity so you can trust that the quote you’re receiving is fair and final.

How does our technology work?

Our system leverages multiple reliable data sources to assess your property’s risks and deliver a personalised quote within seconds. From flood zones to natural hazards, our advanced platform ensures you’re getting a quote that reflects the latest information.

Even if your property requires a referral for further review, we’ll ensure it’s assessed promptly. This guarantees your policy is built on a thorough, expert evaluation—giving you the confidence to move forward with certainty.

Why initio doesn’t offer multi-policy discounts

We’re often asked if bundling insurance can save you money. The answer is simple: initio doesn’t do multi-policy discounts because we offer you the best price for every policy right from the start. We provide a fair and straightforward process where every quote is designed to be competitive and accurate.

A fast, modern insurance experience

Initio isn’t just about speed; it’s about trust. Our platform ensures you can quote, compare and get cover in minutes – backed by a system designed to simplify your experience. No upselling, no misleading information – just an honest, reliable service powered by the best technology in the industry.

If you have questions, our team is here to help. But when it comes to finding a better deal, you won’t need to look anywhere else. With initio, you’re already getting the fastest, most accurate quote possible.

Hear from the team behind the tech

Take a look under the hood to see the tech that drives our insurance and how it’s evolved into what it is today.

Other articles of interest

- Awards we’ve won

- How do I buy my first policy?

- Essential guide to house insurance

- Understanding landlord insurance

- Explore our video library

- How to switch from your current insurance provider to initio

Try it for yourself

Landlord insurance for multiple rentals

Help with adding more than one property to your cover

If you own more than one rental property, you might be wondering how landlord insurance for multiple rentals works. With initio, it’s simple – you can manage all your insured rentals under one dashboard, add new properties when you’re ready, and keep your cover consistent across your portfolio.

If I want to add more than one property, do I need separate quotes and invoices?

You can buy your first policy online, then add more properties from your initio dashboard by selecting the “House insurance +” button. Here’s a step-by-step guide to navigating the initio dashboard.

Each property usually needs its own quote, so the right details and cover apply to that address. If you own a block of connected flats or units (up to 8 units) on standard residential leases, you could look at our Multi-Unit Rental policy, which covers the whole block under one policy.

Can I pay with a different account for each of my rental policies?

If you’re paying monthly, initio can only hold one card per account to cover all monthly policy payments. To use a different card for a specific monthly policy, you’d need to set up a separate initio account under a different email.

If you’re paying annually, you can choose a different card for each policy at the time you buy it.

Learn more here: Common Queries and How monthly insurance works.

“When managing landlord insurance with multiple rentals, it’s a good idea to review each property’s cover once a year. Different homes can have different risks – like flood zones, tenant types, or rebuild values – so checking that your sum insured and excess still make sense helps ensure you’re not under- or over-insured. Keeping your details up to date also means any claims can be processed faster and without surprises.”

If you get stuck while adding another property or managing multiple rental insurance, help is only a click away. You can chat with Chad, our friendly digital assistant, directly on the initio website for quick answers and step-by-step guidance. Just click on the ‘help’ button at the bottom of the screen to get started. If you’d prefer to talk to a real person, our support team is always happy to help – just head to our contact us page to get in touch.

Related articles

- Help when your quote isn’t straightforward

- What can be insured under our Multi Unit Rental Policy?

- How property use affects your cover

- Are you thinking about becoming a Landlord and renting your home?

The Unpredictable World of Home Insurance

From Seagulls to Scribbles

Life can be full of surprises. This year, our clients’ experiences range from the utterly unexpected to the charmingly chaotic. We understand the need for comprehensive property insurance that covers these unforeseen events.

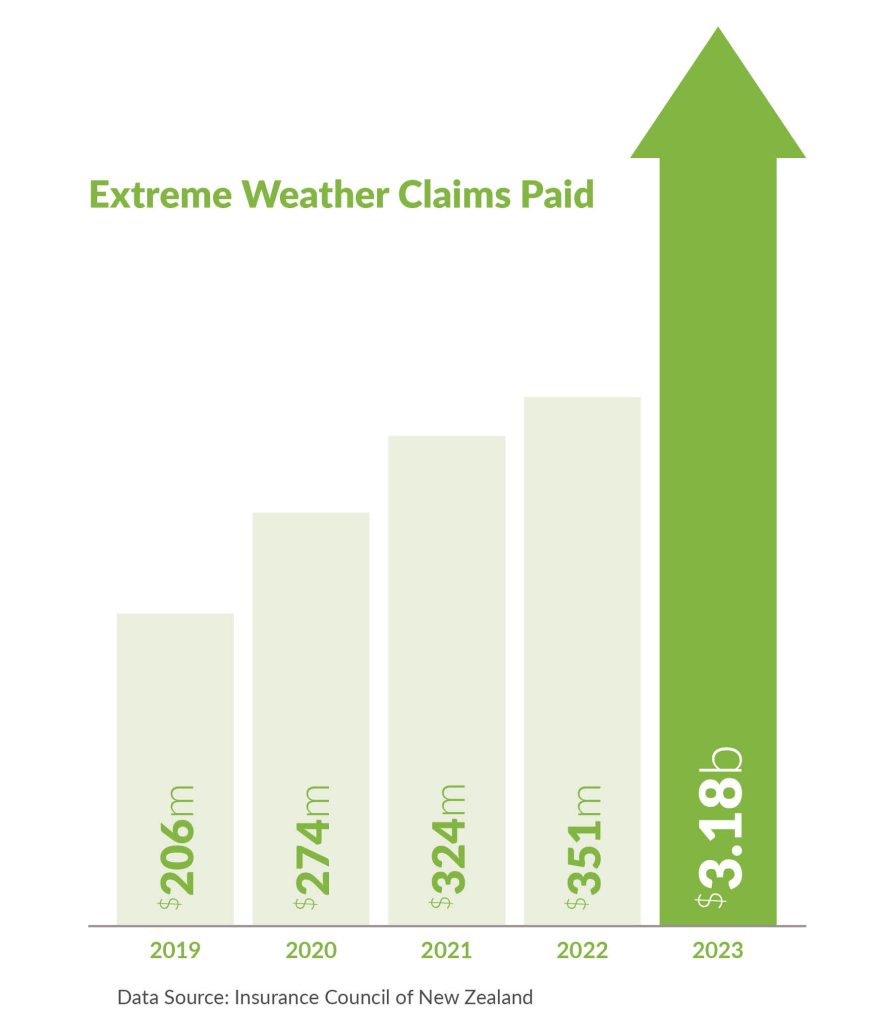

This year, initio has processed a record number of claims, almost doubling from last year. Our payouts have increased significantly by over 230%, a substantial rise compared to the 45% increase from 2021. The major storms and flooding we saw at the beginning of the year (along with other significant events) meant more people needed help from their insurance provider, which in turn pushed up the cost of insurance premiums. The intensity and frequency of these events have been steadily increasing, with 2023 being off the chart, as shown in the graph below:

It’s worth noting that the above figures are across all New Zealand insurers and were calculated in August 2023, these numbers will be even higher now.

The growing number of Kiwi homeowners choosing initio has also influenced these increased numbers. We’re delighted that many have selected us as their insurance provider, indicating our ongoing growth and success. A heartfelt thank you to those who have recently joined us and to our loyal customers who have continued with us this year.

As we wrap up the year, let’s explore the lighter side of insurance with a look at some of the most unique claim trends we’ve encountered in 2023:

Nature is wild

Nature can be unpredictable, and it certainly was for a few of our clients this year. In one instance, a drone was unexpectedly taken out by a seagull, while in another, a bird decided to make a home in a client’s chimney, causing a mess and eventually meeting an untimely end. Nature’s surprises can sometimes be costly! Domesticated pets also caused their fair share of claims this year, the majority of which were caused by them not making it outside in time to use the bathroom. These types of claims alone caused thousands of dollars worth of damage.

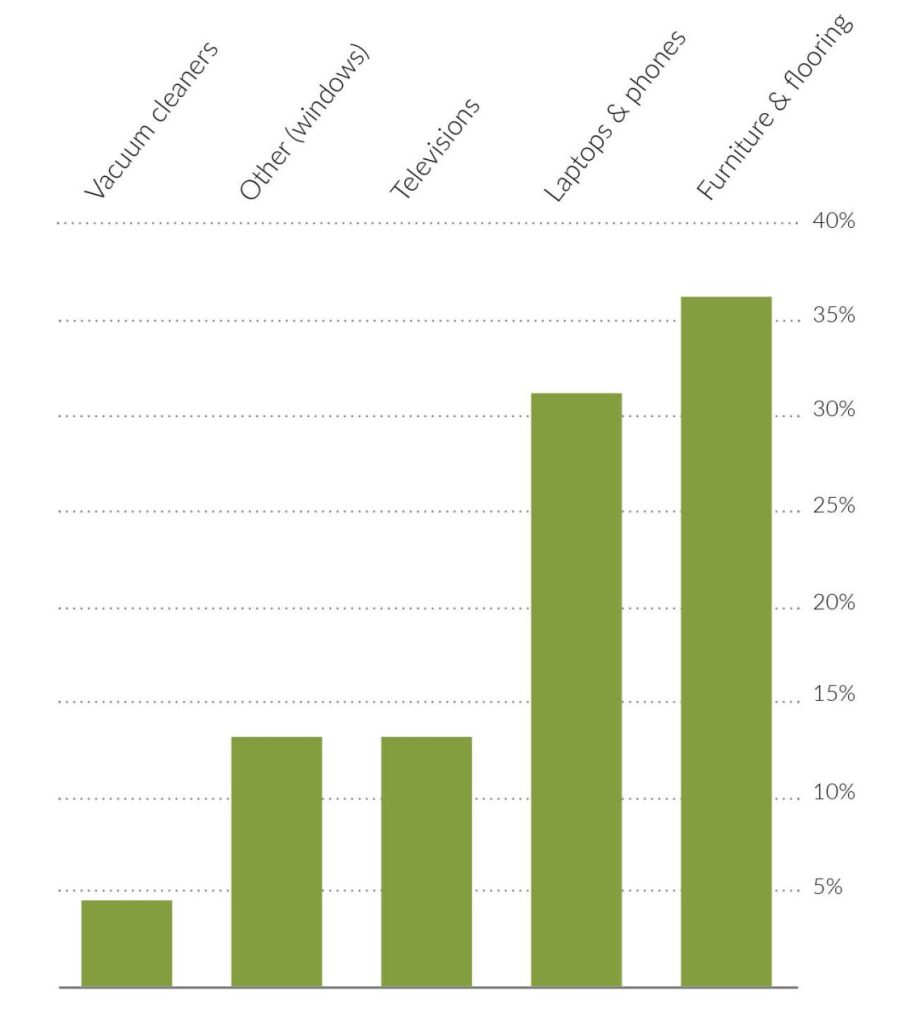

The artistic and the audacious: Children at play

Children bring joy and, occasionally, a bit of chaos. From a child’s artistic scribblings using foundation makeup that unfortunately left lasting marks on furniture and décor, to the regrettable incident where a backpack met its fate under the blades of a lawnmower, and those inventive yet ill-fated attempts at cleaning up spills with a vacuum cleaner, the innocence and spontaneity of children can sometimes come at a cost. Not to mention the numerous TV and tech accidents involving toy hammers, building blocks and balls, all leading to thousands of dollars of damage.

Another client unexpectedly went into labour while at home, an experience filled with surprise and natural wonder. But when her water broke, it soaked the carpet in the process.

CHILDREN VS HOUSEHOLD ITEMS 2023:

Tesla tales: The perils of parking

This year, our Tesla owners have navigated various challenges, notably a rise in claims for windscreen damage and parking incidents. Even the most advanced vehicles aren’t immune to the quirks of daily life. One advantage of owning a Tesla is the reduced petrol costs, coupled with comprehensive camera coverage. This feature ensures most incidents are recorded, providing valuable evidence. It’s important to remember if you accidentally collide with a parked Tesla, chances are, it’s on camera.

Candles and pianos don’t mix

Coincidently we saw two cases of candle wax melting onto pianos this year, making them unplayable. These two incidents alone cost thousands of dollars of damage (pianos are expensive!). While they might create a beautiful ambience, the takeaway lesson would be perhaps don’t have lit candles on top of your piano.

At initio, we’ve seen it all, from feathered fiascos to technology tragedies. These stories showcase the unpredictable nature of life and the essential role of comprehensive property insurance. Whether it’s a mischievous child or a parked Tesla, we’re here to ensure that when life happens, you’re covered. Discover the ease of getting a quote and the simplicity of insuring with initio for yourself.

Percentages in this article have been rounded.

Understanding flood risk and zones – a guide for property owners

Flood risk is becoming an increasingly significant issue for property owners in New Zealand due to the growing frequency and severity of weather events. This risk often translates into financial hardship due to the damage caused and the potential for increased insurance premiums. Certain areas, like Edgecumbe and Westport, for example, face heightened challenges, with insurance becoming harder to secure.

To help you navigate these challenges, this guide combines insights on flood risk assessment and the implications of living in flood zones, using advanced tools like Risk Management Solutions (RMS) and council-provided data.

Measuring flood risk

Flood risk is determined by two key factors:

- Frequency: How often floods are likely to occur.

- Severity: The potential impact and damage caused by those floods.

Initio is committed to providing transparent and accurate information to help you protect your property.

At initio, we use Risk Management Solutions (RMS) data to assess properties’ flood risk. RMS is a global leader in risk modelling and analytics. They use advanced technologies, scientific data, and sophisticated modelling techniques to assess natural disaster risks, including flooding. RMS determines flood layers by analysing:

- Historical flood data

- Topographical information (land elevation and shapes)

- River systems and water flow patterns

- Rainfall data and climate patterns

- Soil types and ground absorption rates

- Man-made structures like dams and levees

When you get a quote, and the property you’re quoting is in a flood risk zone according to the RMS modeling, we will show you a message detailing what risk has been found. These are as follows:

- “Flood Risk – RMS Flood 50 Year Return”: There’s a 1 in 50 chance of a significant flood in any year, or a 2% chance of a flood occurring in any year.

- “Flood Risk – RMS Flood 30 Year Return”: This indicates a 1 in 30 chance of significant flooding each year, or a 3.3% chance of a flood occurring in any year.

These year values represent the probability for the scale of flooding that needs to occur for the water to reach this property. So when you hear about “one in a hundred year flood”, or “one in 50 year floods”, that is what those flood risks mean; if a “one in 30 year flood” occurs, water is likely to reach properties that fall in the RMS 30 Year flood model.

The risk information don’t mean that a flood will only happen once in 100, 50, or 30 years. As we saw with the Auckland flood events from 2023, multiple flood events can occur in quick succession.Ultimately these are modeled risks, and real world outcomes may vary, but they are a way to better predict flood risks and keep insurance accessible for New Zealand.

However, it’s crucial to understand that frequency doesn’t always correlate directly with severity. Flood severity refers to how damaging a flood might be, regardless of frequency. For instance, a less frequent flood might cause significant damage if it is severe, while a more frequent flood might have a lower impact.

When you get a quote online, if there is a flood risk associated with the address you have provided we will display the risk found on the RMS dataset based on the location of the property.

This information helps determine whether we can offer immediate insurance cover or if further review is needed. However, it’s important to note that these are probabilistic models and real-world outcomes may differ.

Understanding flood severity

While frequency tells us how often flooding might occur, severity helps us understand the potential impact on your specific property. We assess severity by looking at several key factors that combine to create a complete picture of risk:

-

Predicted flood water depths (ranging from shallow surface flooding to depths of over 3 meters)

-

The percentage of land potentially affected

-

Your building’s position on the property

-

Natural drainage patterns

-

Existing flood protection measures

-

The building’s design and construction

The interaction between these factors can significantly influence the actual risk to your property. Here are some examples:

-

A property might be in a 30-year flood zone with a predicted 2.5-meter water depth, but if this only affects a small corner of the section where no buildings stand, the practical risk might be manageable.

-

Conversely, a property in a 50-year zone with a lower 0.5-meter predicted depth could present higher risks if the water would cover most of the land and directly impact the building.

-

A property with moderate flood frequency but high predicted water depths (3+ meters) covering significant building areas would typically represent a more serious risk which may be outside of our capacity to insure.

Our website continually evolves as data and modeling capabilities improve. The rules we use to evaluate properties are regularly updated to reflect the latest RMS data and our growing understanding of flood risks in New Zealand. This means that assessments can change over time as we refine our approach and incorporate new information about flood risks and their potential impacts.

At Initio, we use this comprehensive understanding of both frequency and severity to make balanced insurance decisions. Our approach is designed to be practical – we can typically provide coverage even when some flood risk is present, however not all properties are able to be insured by Initio, depending on the risks involved.

Understanding Flood Zones and Mapping Tools

In addition to RMS data, tools like the Searise website, local council hazard maps, the property’s history and your own LIM report provide valuable insights into flood risks. These tools help both insurers and property owners understand sea-level rise, vertical land movement, and local flood hazards. With these resources, you can view your property’s flood risk, explore hazards like river overflow and storm surges, and prepare accordingly.

Searise example

Auckland Council flood mapping example

Local councils also play a crucial role in managing flood risk by improving infrastructure, such as drainage systems, which are increasingly under pressure. Ensuring that these systems are up to standard is essential in reducing flood risks for homeowners.

Why might my council’s flood risk assessment differ from RMS data?

It’s possible that your local council’s flood risk assessment may differ from the RMS data we use. This can happen for several reasons:

- Updated information: RMS may have access to more recent data or use more advanced modeling techniques.

- Different focus: Council assessments might focus on specific local concerns, while RMS provides a standardized national assessment.

- Varying methodologies: The methods used to assess flood risk can differ between organizations.

- Broader considerations: RMS data may take into account factors beyond what local councils typically consider.

If you have concerns about discrepancies between council and RMS assessments, we encourage you to contact us for further clarification.

How Does Flood Risk Impact Insurance?

Suppose your property falls within a high-risk flood zone. In that case, initio uses all information available to help decide whether immediate insurance cover can be offered or if custom terms would be required.

While insurance can help protect against flood-related damage, it’s important to manage the risks proactively. This might involve flood-proofing your property, improving drainage, or making structural changes to better withstand flood events.

Flood risk can vary across properties depending on:

- Specific property location within a flood zone.

- Local topography and elevation.

- Drainage systems and recent land developments.

What If I’ve Reduced My Flood Risk?

If you’ve taken steps to reduce your property’s flood risk, such as installing barriers or improving drainage, let us know. These improvements would be considered when assessing your property’s flood risk for insurance purposes.

Summary

With the growing threat of severe weather events, understanding flood risk and using available resources is essential for property owners in New Zealand. By leveraging data from tools like RMS and local flood maps, you can make informed decisions, better protect your property, and ensure you are adequately insured.

For more information or help understanding your property’s flood risk, reach out to our support team at initio. We’re here to provide the transparency and guidance you need to manage these risks effectively.

Remember, understanding your flood risk is the first step in protecting your property. Stay informed and prepared!

Related articles & useful links

- Five tips to insuring in a flood zone

- Risk Management Solutions RMS

- Searise

- Auckland Council’s flood zone maps

- What is an alluvial fan – and why does it matter for property owners?

IMPORTANT – RMS Moody’s disclaimer

This report, and the analyses, catastrophe modelling results and predictions contained herein (“Information”), are based on data provided by Initio Limited, and compiled using proprietary computer risk assessment technology of Moody’s Analytics, Inc. and its affiliates (“Moody’s”). This Information is a single copy, copyright protected work of Moody’s that contains confidential and proprietary information of Moody’s. As with any model of physical systems, particularly those with low frequencies of occurrence and potentially high severity outcomes, the actual losses from catastrophic events may differ from the results of simulation analyses. Furthermore, the accuracy of predictions depends largely on the accuracy and quality of the data used by Initio Limited. The Information is owned by Client or provided under license to Initio Limited and is either Client’s or Moody’s’ proprietary and confidential information and may not be shared with any third party without the prior written consent of both Initio Limited and Moody’s. Furthermore, this Information may only be used by the recipient in connection with, as applicable, (i) Initio Limited’s imminent placement of insurance or reinsurance; or (ii) the recipient’s 3 regulatory activities in relation to Initio Limited; and always for internal purposes only and for no other purpose, and may not be used under any circumstances in the development or calibration of any product or service offering that competes with Moody’s. You are not authorized to use, copy, modify, disclose, and/or distribute this Information in whole or in part in any form, except as expressly and specifically permitted under a written agreement signed by Moody’s. Any unauthorized use, copying, modification, disclosure, or distribution of this Information will constitute an infringement of Moody’s intellectual property and your agreement to pay list price for the use of the product or application associated with this Information, in addition to any applicable penalties or damages or other remedies available under applicable law. The recipient of this Information is further advised that Moody’s is not engaged in the insurance, reinsurance, or related industries, and that the Information provided is not intended to constitute professional advice. Moody’s including its parent, subsidiary and other affiliated companies are all beneficiaries of this disclaimer. MOODY’S (AND ITS PARENT, SUBSIDIARY AND OTHER AFFILIATED COMPANIES) SPECIFICALLY DISCLAIMS ANY AND ALL RESPONSIBILITIES, OBLIGATIONS AND LIABILITY WITH RESPECT TO ANY DECISIONS OR ADVICE MADE OR GIVEN AS A RESULT OF THE INFORMATION OR USE THEREOF, INCLUDING ALL WARRANTIES, WHETHER EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO, WARRANTIES OF NON-INFRINGEMENT, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE. IN NO EVENT SHALL MOODY’S (OR ITS PARENT, SUBSIDIARY, OR OTHER AFFILIATED COMPANIES) BE LIABLE FOR DIRECT, INDIRECT, SPECIAL, INCIDENTAL, EXEMPLARY, OR CONSEQUENTIAL DAMAGES WITH RESPECT TO ANY DECISIONS OR ADVICE MADE OR GIVEN AS A RESULT OF THE CONTENTS OF THIS INFORMATION OR USE THEREOF.

What is a Multi-Unit rental property for the purpose of insuring under our Multi-Unit Rental policy?

What can be insured under our Multi Unit Rental Policy?

At initio we have a multi-unit rental policy which was designed to insure a block of flats owned by a single landlord. For the purposes of this policy, a Multi-Unit Rental Property is defined as;

- two or more units, townhouses or flats that are combined under one building, so connected under the same roof or are physically connected in some other way (e.g. car-port or deck) and

- with each unit being self contained and

- having the same owner and

- on a standard long-term residential lease

Some examples of multi-units that we can insure under this policy are;

- a two story house where each level has a separate tenancy

- a block of flats owned by one person/entity – up to 8 units

- cross lease units, connected by a carport

- duplex townhouses

- rental house with physically attached self contained studio / granny flat – also rented out

There are some limitations as to what the multi unit properties we can insure.

- We cannot insure more than 8 units.

- We cannot insure properties that are more than 3 stories.

- The tenancies must not be short term or holiday lets.

- The property must be residential use only.

- We cannot insure individual or multiple units that form part of a body corporate.

- We cannot insure more than one rental unit at different addresses under this policy.

Related Articles:

How to: Methamphetamine Contamination Claim

Methamphetamine contamination in a rental property can be an alarming and confusing time for property owners. There are conflicting theories on what levels are acceptable and what needs to be done to get the house livable again. Initio keeps it simple and adheres to the Ministry of Health Guidelines which state that any house reading more than 1.5mg of methamphetamine per 100 cm2 needs to be decontaminated.

If your short or long term rental property has tested positive for the presence of methamphetamine and you have house insurance with Initio, here’s what you need to do:

- If you haven’t already, you need to get a detailed room-by-room test completed. This will show you which specific areas of the house are contaminated.

- Log into your dashboard on the initio website and click on the make a claim button.

- Fill in the form and attach your test results.

- We’ll email or call you within one business day.

FAQ’s:

- Does my initio landlord insurance policy cover methamphetamine contamination?

Yes; however, the cover is specific and limited to $30,000:

Where the contamination damage occurs in connection with any tenancy or occupancy of:

- More than 90 days, there is no cover unless you, or the person who manages the tenancy on your behalf, have fully met the ‘landlord’s obligations’ under the ‘Policy conditions’; or

- 90 days or less, there is no cover unless the contamination damage was caused by an accidental incident in connection with the manufacture, distribution or storage (but only where the storage is in connection with supply or distribution) of methamphetamine at the home.

- What is the excess?

All methamphetamine contamination claims have a specific excess of $2,500.

- Can I start cleaning the house?

Not yet, please follow steps 1-3 above and then we’ll work together on getting the house livable again.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

Methamphetamine is not a discriminatory drug … anyone could be using or manufacturing methamphetamine in your rental property … even your tenants!

Methamphetamine is not a discriminatory drug … anyone could be using or manufacturing methamphetamine in your rental property … even your tenants!

Can I insure a boarding house?

In a boarding house, each tenant rents a room rather than the whole house. They then share facilities such as the kitchen with the other tenants, and in many cases each tenant has their own bathroom.

We can insure boarding house’s with five or less rooms (tenants). If your boarding house has five or less rooms you can get a insurance quote here.

If there are more than six rooms we consider this to be a commercial building risk and we are unable to provide cover.

Contents

Can I insure a house bought in a mortgagee sale?

In most cases insurers won’t provide cover for houses that were sold under a mortgagee sale. This is because of the increased and known risk associated with this type of property sale. However, we know that all mortgagee sales are different so can consider cover on a case by case basis if some requirements are met. We can only consider cover from the settlement date of the property, not from the fall of the hammer/purchase date.

Mortgagee Sales are typically purchased on an “as is where is” condition, and often purchased without being inspected. The property is either left unoccupied which can add to the overall risk of the property, or the defaulting owner is still living in the property, which adds another level of complexity.

A major issue with the insurance of mortgagee sales houses is that the buyer can be required to insure the property before they are the legal owner. A condition is often applied to the sales agreement requiring insurance of the property from the “fall of the hammer”, i.e the date you agree to purchase the dwelling and not from the settlement date. It can be very difficult to get insurance cover from “fall of hammer”. Fall of the hammer cover, if you can get it, is normally for a short period only (up to 3 months), is provided by a offshore insurer, and will cost at least $3,000. The cover will also be limited to loss from weather damage, natural disaster, water damage and will not include cover for malicious damage.

Minimum requirements for insurers to consider cover

Insurance providers like Initio will generally only consider mortgagee sale cover for existing clients, and will provide cover from the settlement date not fall of the hammer. You will need to provide information on the following:

- Purchase date

- Settlement date

- Are you required to insure the home prior to the settlement date?

- Overall condition of the home

- Whether the current or previous owner lives in the house, if it is a rental, or empty

- Your intentions after settlement (e.g. moving in immediately, or putting tenants in after renovations etc.)

- Have the locks been changed? If not, when will they be changed?

Send your details to [email protected] and our team will get back to you.

Apple Mortgage

Frank Risk

Reduce your insurance costs by insuring online, and know that Frank has got your back with support and claims management.

Get a quick quote and start your cover

Why have my property insurance premiums increased?

There are a number of reasons why your premiums may have seen a recent rise. Some of those reasons are associated with passing on costs such as recent claims and securing reinsurance, but the most recent hike will be due to increases in government levies.

Levies are charges that are applied to insurance premiums and then paid to the government by insurers. They help cover the cost of services that benefit all New Zealanders, such as the Earthquake Commission and Fire and Emergency New Zealand. Sometimes these levies can make up half of the cost of house insurance . Effective from 1 July 2019 the Government Earthquake Levy (EQC Levy) increased by between $69 and $115 per house. Learn more about the EQC levy change here

In addition to this, many insurers (including initio) have now changed to a risk-based pricing model, which has affected how they calculate premiums. Instead of being spread across different areas, if you buy a risky home or a property in an area prone to disaster, for example, this risk will be reflected in a higher premium specifically for you.

Due to the increasing prevalence of extreme weather events, reinsurers are also re-examining New Zealand’s risk exposure to natural disasters. As a result, may insurance companies have begun pricing for seismic risk, flood risk and the effects of climate change.

Initio named MoneyHub’s favourite home insurance quote platform

We’re proud to share that initio has been recognised by MoneyHub as their Favourite Home Insurance Quote Platform. It’s an honour to be featured by one of New Zealand’s most trusted consumer platforms, known for cutting through the noise and helping Kiwis make confident financial decisions.

In a market where “best” is rarely clear-cut, MoneyHub doesn’t hand out praise lightly. Their awards focus on innovation, value, and customer benefit, not just big marketing budgets. That’s why we’re especially proud they’ve recognised initio for what truly sets us apart: our technology and market-leading customer service.

Real quotes, really fast

According to MoneyHub, initio’s platform delivers “a high-quality insurability assessment and property premium in under six seconds.” That means when someone’s looking to insure their home, they don’t get vague pricing or hoops to jump through – they get a tailored result, instantly.

And this isn’t by accident. Our quoting engine is the result of years of dedicated development. We’ve built the tech in-house, from the ground up, to be the fastest, smartest and most accurate in the industry. Every part of it is designed with the customer in mind, whether it’s pulling property data, calculating risks, or accounting for tricky scenarios like flood zones or multi-dwelling sites.

The gold standard in quoting

While some providers give a rough estimate or send your details to a call centre, initio delivers a real quote in real-time. No salespeople, no follow-up calls – just clarity and speed. It’s why landlords and homeowners alike rate our quoting platform as the most seamless and transparent in the market.

As MoneyHub puts it:

“The cyclone and flood devastation in early 2023 highlights the need for insurers to prioritise technology for claims and risk-pricing… Initio is future-focused and propelling the industry forward.”

We couldn’t have said it better ourselves. Because great insurance starts with great tech – and at initio, we’ve made that our mission.

Try our award winning quick quote out for yourself:

Quick House Insurance Quote

Related articles:

Landlord Insurance – initio features in NZ property investor magazine

Initio recently featured in the New Zealand Property investor magazine. Our policy and pricing was compared to all the mainstream insurance providers…. the result …. Initio provides some of the best landlord insurance cover in New Zealand. The initio policy extensions provide our clients with robust landlord insurance cover.

As well as providing extensive cover, the NZ property investor magazine proved that our premiums are the most competitive (at time of publishing).

Landlord insurance for your rental property online with initio insurance.

What could go wrong at my rental?

A closer look at property damage for New Zealand Landlords

Rental properties, for all their promise of steady income and long-term value can, if not managed correctly, become ground zero for an array of unforeseen problems and potential hazards.

The reality is that damages, an often neglected aspect of rentals, pose a considerable risk to your investment. These risks are as varied as they are prevalent, raising a pertinent question in the minds of property owners: “What damage is most likely to occur at my rental property?”

Safeguarding your investments and mitigating potential losses, and understanding these risks is essential to success as a landlord.

A thorough examination of our 2022 loss data provides a detailed analysis of the challenges faced by New Zealand property owners. Last year, claims related to rented properties — including traditional rental properties, own homes partially rented, and properties with multiple rentals, made up 35% of all the claims we received. When focusing on these rental-specific claims, we identified a broad spectrum of loss types, which we’ve classified below in terms of number of claims:

Water-related damage: At 21.6%, this was the most common type of damage. These losses typically involved scenarios including suddenly bursting pipes and rodent damage, while blocked pipes accounted for 6.4%.

Accidental damage: This category, representing 18.1% of the claims, includes an array of unexpected incidents, from minor mishaps to substantial accidents, illustrating the diverse risks property owners encounter. The losses range from outdoor misadventures, such as balls shattering windows or trees falling onto the property (while being pruned), to indoor accidents like stains on carpets and damaged rugs, often due to spills or pet-related incidents. There were also multiple kitchen bench damage incidents – caused by hot pots.

Weather-related damage: Severe weather events substantially contributed to the claims we received, with flood-related incidents constituting 11.2% and wind-induced damage representing 9.9% of the total claims. These statistics do not include the severe flooding and storms experienced earlier this year. Weather damage events are hard for property owners to mitigate.

Other incidents: Some more specific types of damages also occurred, albeit less frequently. These included

- Malicious damage by tenants (4.6%),

- Fire – accidental or unknown reasons (1.1%),

- Meth contamination (1.5%),

- Issues with keys and locks (3.5%),

- Impact damage, typically involving a vehicle (5.5%) eg car versus house

Loss of rent: There were several circumstances that led to a loss of rental income, resulting in insurance claims. Property damage rendering the property uninhabitable was one such factor and is the most common.

However, issues such as tenant abandonment, non-payment of rent, and eviction also significantly contributed. These loss-of-rent-only situations accounted for 3.3% of the total claims made.

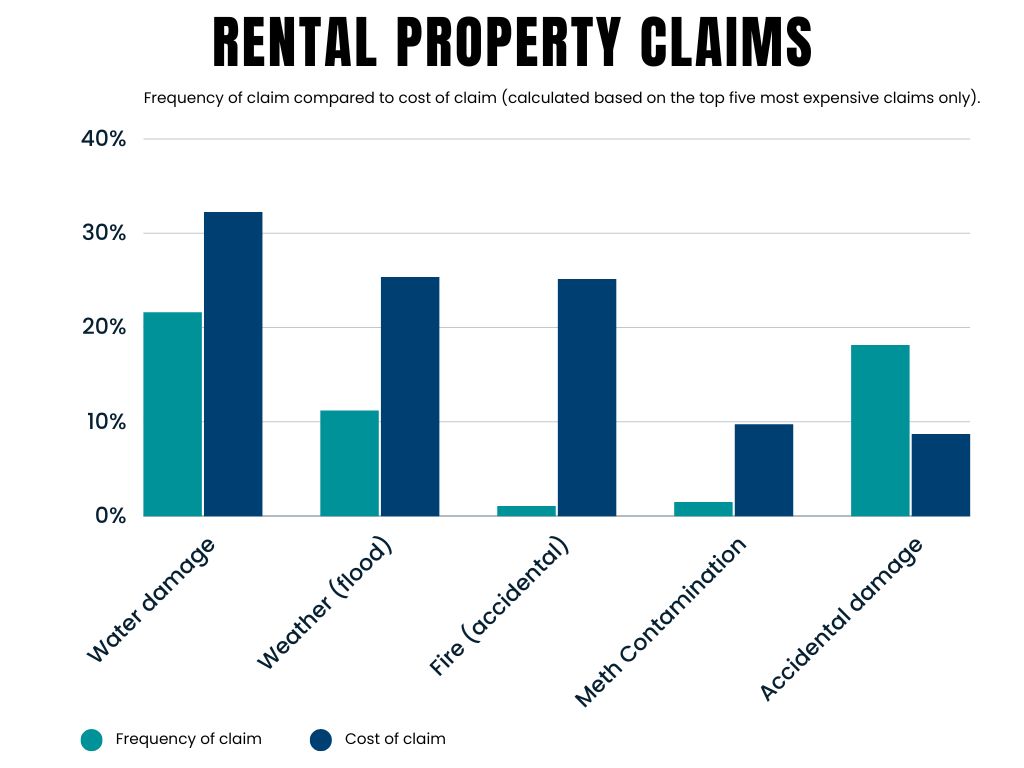

Frequency of claim vs. cost

The above numbers are based on frequency (i.e number of claims made). We also analysed the payout values for rental property claims. The graph below shows the top five losses by value. This data is presented alongside the frequency of each of these claims. It illustrates that losses like fire are uncommon but are high in value.

Fire-related claims constituted a mere 1.1% of the overall number of rental property claims, but made up 25% of the total value of claims paid. This underscores the potential devastation that fires can cause to rental properties. The significance of this cannot be overlooked, highlighting the importance of equipping your rental properties with smoke alarms, and fire extinguishers. By taking these simple proactive measures, you can significantly reduce the risks associated with fires and safeguard your valuable assets and your tenants.

Final word

Understanding the potential risks involved in rental property ownership can help landlords to better prepare for and protect their investments.

Proactive and pragmatic management of landlord risk is a form of insurance in its own right. In our experience, with the losses we see on a daily basis, a landlord that focuses on tenant selection, tenant vetting, regular property inspections, fire extinguishers in kitchens, regular maintenance including plumbing and electrical checks will outperform and not contribute to the statistics in this article.

Choosing an insurance provider that knows landlord insurance and who provides an insurance policy that is dedicated to the diverse needs of rental property owners is the icing on the cake for a well-rounded risk mitigation approach to landlording.

Learn more about initio’s Landlord insurance cover

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2022, spanning our entire claims portfolio. Please note that all figures are approximate and have been calculated to provide a representative view of the claim trends during this period.

Autumn Home Expo

How to calculate your sum insured

Your rebuild sum insured is one of the most important parts of your house insurance policy. It determines the maximum amount payable if your home needs to be rebuilt after major damage.

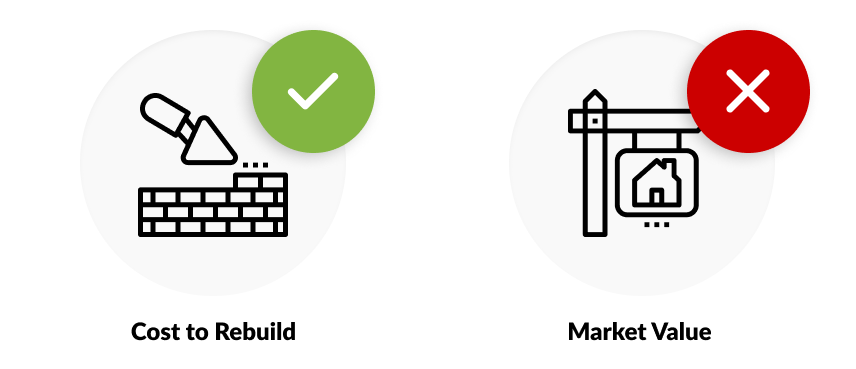

This guide explains what sum insured means, how to calculate it correctly, and why market value is not the right number to use.

Quick summary

-

Your sum insured should reflect rebuild cost, not market value.

-

Include demolition, fences, pools and other structures.

-

Add a buffer for rising building costs.

-

Minimum and maximum limits are based on your floor area.

-

All sums insured include GST.

-

You are responsible for selecting the correct amount.

What is sum insured?

Sum insured is the amount it would cost to fully rebuild your home to its current size and standard, using today’s building costs. It is not:

-

The market value of your home

-

What you paid for the property

-

The land value

It should reflect rebuild cost only.

Rebuild cost vs market value

Market value includes land and location demand. Rebuild cost only covers construction.

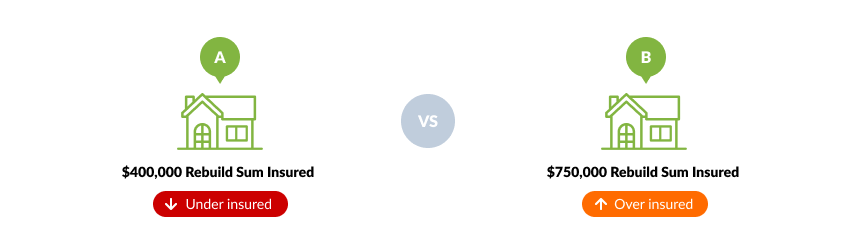

Example: Under-insured vs over-insured

Imagine two neighbours with identical homes that would cost $500,000 to rebuild.

-

Neighbour A insures for $400,000 using a rough estimate of $2,000 per square metre.

-

Neighbour B insures for $750,000, thinking market value is the right number.

After an earthquake:

-

Neighbour A receives $400,000 and is $100,000 short.

-

Neighbour B receives $500,000 (the rebuild cost), but has paid higher premiums than necessary.

Getting it right avoids both financial shortfall and overpaying.

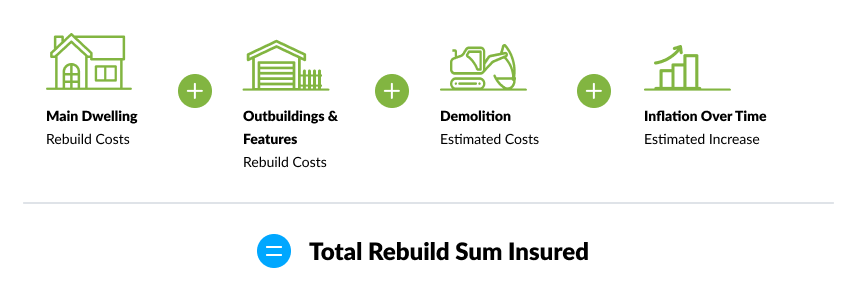

What should be included in your rebuild sum insured?

When calculating your sum insured, include:

-

The house itself

-

Fences

-

Swimming pools

-

Retaining walls

-

Other permanent structures

You should also factor in:

-

Demolition and debris removal

-

Professional fees

-

Inflation and rising building costs

Adding a reasonable buffer can help protect against cost increases over time.

Why is there a minimum and maximum sum insured?

When selecting your sum insured, you will see a minimum and maximum value range.

These are calculated based on:

-

The floor area of your home

-

Any declared outbuildings

Minimum sum insured

This reflects the lowest realistic rebuild cost per square metre for a basic home. It helps prevent serious underinsurance.

Maximum sum insured

This reflects the upper realistic rebuild cost based on floor area.

Selecting a figure above this will not increase your payout. It may only increase your premium.

If your situation genuinely requires a higher amount, contact our support team to discuss your circumstances.

💡 Building costs vary depending on materials, design and location, but most homes fall within the provided range.

Does my sum insured include GST?

Yes. Any nominated sum insured on an initio policy includes GST.

Before confirming your GST preference, ensure your selected amount includes the GST component.

How can I estimate my rebuild cost?

If you are unsure where to start, you can use the Cordell Sum Sure Calculator.

It uses council data, floor area, and building details to estimate rebuild costs. You can compare this estimate with your own assessment.

You may also wish to consult:

-

A registered builder

-

An architect

-

A quantity surveyor

Cordell Rebuild Calculator

Who is responsible for setting the sum insured?

While we can provide guidance on how our products work, we are not qualified to value homes.

You are responsible for determining the correct rebuild sum insured for your property.

If your calculated amount falls outside the available range, please contact our support team.

Frequently asked questions

Should I insure for market value?

No. Your sum insured should reflect rebuild cost, not market value.

What happens if I under-insure?

Your maximum payout will be your selected sum insured, even if rebuild costs are higher.

What happens if I over-insure?

Your payout is capped at the actual rebuild cost. You may pay higher premiums without receiving additional benefit.

Do I need to include demolition costs?

Yes. Rebuilding after major damage includes demolition and debris removal.

Related Articles

New policy for Holiday Homes

From 1 January 2019 the initio Holiday Home insurance policy is changing. We’ve added some extra benefits, enhanced and simplified some of the existing covers, and put some restrictions on some areas. This is a summary of the good, the improvements, and the not so good.

THE GOOD:

New cover benefits

New building work

Up to $10,000 of cover is available per annual period for a new structure valued at $10,000 or less being built at the home, including any associated materials that are to be included in the new structure. Covers loss or damage caused by specified events only. Please contact us if you need separate cover for building work that falls outside of the above criteria.

Post-event inflation protection

Under the home section of this policy, up to 10% of the relevant policy limit or sum insured is available as additional cover if building costs increase due to widespread damage following a natural disaster, storm or flood.

Stress payment

If we pay a total loss claim for the home, we’ll also pay you $1,000 for stress caused by the loss.

Water or sewage pipe blockage

Up to $1,000 of cover is available per annual period towards unblocking water or sewerage pipes at the home. No excess applies.

Electronic Programs

If your electronic equipment suffers loss or damage covered under the home section of this policy, you’re also covered for the reasonable cost of restoring, re-setting or re-programming programs, software and other coded instructions necessary to operate that equipment. There’s no cover for any data that may be stored on that equipment.

Keys and locks

The maximum amount payable during an annual period for your home’s keys and locks is $1,000. No excess applies.

Improvements to existing cover:

Vacant homes

Where the home has been vacant for more than 60 consecutive days we continue to provide insurance cover but with a higher than standard excess ($5,000). If you have an active, professionally-installed alarm, the excess reduces from $5,000 to $1,000. Under the old policy the alarm excess was $2,500.

Landlord’s protection

Additional Benefits for landlords (in addition to existing benefits for malicious damage):

- Loss of rent due to non-payment of rent because of prevention of access or failure of public facilities, up to 6 weeks’ rent

- Loss of rent due to the tenant vacating the property without notice, up to 6 weeks’ rent

- Loss of rent due to eviction for non-payment of rent, up to 6 weeks’ rent.

The excess has changed from minimum $500 to the standard policy excess.

Learn more about landlords protection here

Simplified cover for contents

The following items are covered for present value only:

- watercraft and their parts and accessories (there’s no cover under this policy for watercraft with a present value of over $2,500)

- bicycles

- linen

- items that you choose not to repair or replace.

For all other items we’ll either pay:

- to replace the item if it’s under 5 years of age, or

- the present value of the item if it’s 5 years of age or over, or

- to repair the item as close as possible to the condition it was in before the loss or damage.

There is no cover for personal effects, and cover only applies at the home or whilst you are transiting items from your permanent residence or its place of purchase.

Legal liability

Your legal liability cover of up to $2,000,000 for damage to another person’s property is extended to cover liability for another person’s accidental death or bodily injury in connection with your home or its grounds. The limit is now GST inclusive. Defence costs you incur with our prior approval are now covered on top of this. Clarification that there’s no cover for liability in connection with seepage, pollution or contamination, unless it occurs during the period of cover and is caused by a sudden and accidental event that occurs during the period of cover.

Carpets

Fitted floor coverings, including glued, smooth edge or tacked carpet and floating floors are defined as part of the home under the policy and now covered for replacement (new for old).

Clarification to existing cover:

Reduction and reinstatement of sums insured

Following damage to your home for which a claim is payable under the home section of this policy or by the Earthquake Commission, the sums insured are reduced from the time of the loss by the amount required to repair the loss. When payments are applied to the repair of the home, the sums insured are reinstated.

GST

All amounts shown are inclusive of Goods and Services Tax (GST).

Outbuildings

Cover for outbuildings used for domestic purposes now extends to outbuildings that may have limited rural lifestyle use, i.e. for the storage of tools, animal feed, uninstalled equipment or machinery and vehicles only.

THE NOT SO GOOD:

Tree disposal

Your policy no longer covers the disposal of tree debris following damage to your home or contents caused by a falling tree or part of a tree.

Landscaping

The maximum amount payable to restore your garden or lawn has reduced from $3,000 to $2,500. Cover applies only where a claim is payable for damage to the home and the landscaping damage occurred during the same event.

Recreational features and retaining walls

There is now a sub-limit of $45,000 for all recreational features (tennis courts, pools etc) and a sub-limit of $25,000 for all retaining walls, unless these items are specified with a higher limit as shown in your schedule. More details here

Methamphetamine contamination

We continue to provide cover for meth however the maximum amount payable for cleaning or repairing the house and its contents damaged by methamphetamine contamination (manufacture and consumption) has reduced from the house sum insured to the amount shown in the schedule, currently $30,000. An excess of $2,500 applies to each claim. There are additional conditions and limitations for tenancies or occupancies of 90 days or less. Learn more about meth here

Landlord’s obligations

This section outlines the increased standard of care that is now required of landlords. To make a valid claim on a tenanted property, you’ll need to have fulfilled these obligations.

The inspection and monitoring requirements must be met from when your policy renews. The updated tenant-vetting requirements will only apply to new tenancies that commence after your policy renews, not to your existing tenants.

You’ll also need to test for methamphetamine contamination before and after each tenancy, in order to be covered for methamphetamine contamination-related liability as a landlord. Learn more about landlord obligations here

This is not an exhaustive or comprehensive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio landlord and holiday home policy NZ1811

Letter of intent

Is my water damage Sudden or Hidden Gradual damage?

Gradual water damage claims are not always straightforward.

Home insurance protects you from sudden damage like a burst water pipe. But gradual damage over time generally isn’t covered. There’s an exception to this. Most house insurance policies in New Zealand have a extension for Hidden Gradual Water Damage.

However, there’s certain conditions that need to be met to make a claim for this cover.

When can I make a Gradual Water Damage Claim?

Damage needs to be hidden, and caused by an internal water pipe or tank.

Essentially the water damage or leak needs to be hidden from the naked eye. If the leak isn’t hidden there won’t be cover as the damage could have been prevented.

Cover is specific. The source of the water damage needs to come from a tank, hot water cylinder or water/waste pipe.

Examples of Hidden Gradual Damage Claims:

- Sink waste pipe behind kitchen bench top was leaking which damaged and moulded below cabinets.

- Shower’s pressure pipe behind wall was leaking and slowly rotted wall lining and floorboards.

- Broken valve on hot water cylinder leaks water down the inside wall and swells the wooden flooring.

How much cover do I get?

Most house insurance policies have cover for this but with a limit. The limit can range from $1,000 to $5,000 and your excess is taken from the limit.

Our home insurance includes $3,000 of cover.

What will not be a Gradual Water Damage Claim?

The conditions are narrow. Any damage from a leak you can see, or one that doesn’t come from a pipe or tank is unlikely to be covered.

Examples that won’t meet the conditions for a Hidden Gradual Damage Claim:

- Leaking window frame causes rain to leak onto the window sill and rot.

- Water leaking onto the floor from a faulty washing machine (unless the leak was from a hidden pipe).

- Damage to the carpet caused by moisture from a potted plant.

What if I’m not sure what type of damage it is?

It’s hard to know exactly how the damage has occurred or where it’s coming from. If you’re not sure we recommend getting a repair quote from a tradesperson ask them to include their opinion on how the damage happened.

Is the leaking pipe itself covered?

Your insurance cover will protect you for the damage that results from the leak.

The cost to fix the leaking pipe itself; or the actual cause of damage won’t be covered. Insurance will pay to repair the resultant damage, but fixing the faulty pipe or equipment will be your responsibility as a homeowner. In most cases this cost is a small part of the total repair costs.

Learn more about the cause of damage here.

Hidden Gradual Damage Claim Example

A tenant discovers the kitchen floor is spongy under the lino where the water pipe for the cold tap had been slowly dripping. Over time the kitchen cabinet swelled causing the particleboard to deteriorate. The landlord gets a builder to quote the cabinet repairs and a plumber to fix the leaking pipe.

| Item | Amount | Claimable? |

| Sink Cabinet Panels | $866 | Yes |

| Fixing, Screws, Glues | $63 | Yes |

| Particle Board Sheet | $110 | Yes |

| Builder’s Labour | $590 | Yes |

| Relaying of Lino | $783 | Yes |

| Piping Replacement | $25 | Not included in cover |

| Plumber’s Labour | $100 | Not included in cover |

| Total Repair Costs | $2,500 | |

| Less costs not claimable | $125 | |

| Total Claimable Costs | $2,375 |

Your standard policy excess will then be taken out of your payout.

Related Topics:

broker-example

Chadbot Chad, not just an ordinary chatbot…

…a chatbot-extraordinaire!

At initio, we focus on simplicity, efficiency, and adding a touch of fun. That’s why we’re excited to introduce you to Chatbot Chad, our cutting-edge insurance chatbot that’s here to make your life easier. But why is Chatbot Chad better than all the other generic chatbots out there? Let’s dive in!

The heart of everything we do

Chatbot Chad is more than just a chatbot; he reflects our commitment to excellent customer service and innovation. With his ability to provide quick, accurate answers, access to human support, and continuous learning, Chad is truly a cut above the rest.

Even with powerful AI, the human element is still crucial. At initio, we always put people – our customers – first, no matter how advanced our technology becomes. All our innovations, from our smart claims platform and 5-second quote process to Chatbot Chad, are developed with a people-first philosophy. This commitment also extends to how we nurture our staff culture, ensuring we prioritise human connections in every aspect of our business.

At initio, we’re all about combining the best of technology with irreplaceable human value, making sure you always feel supported and valued.

Expertly trained and constantly updated

Before launching Chatbot Chad, our team spent countless hours training him to ensure he could handle a wide range of queries. But we didn’t stop there. We check Chad’s answers daily to ensure they’re accurate and up-to-date, providing you with the best advice possible. This continuous improvement process means Chad is always learning and getting better.

Decades of expertise at your service

We’ve spent the last decade dedicating time and resources to developing our online support materials. These articles are the backbone of Chad’s responses. When you ask Chad a question, he’s mining through years of expertise and knowledge to find the best answer for you. This wealth of information ensures you’re getting reliable and comprehensive support.

Speak to a human anytime

When you need advice on house insurance in New Zealand, we’re here to help. At any point in your conversation, you can choose to speak to a human. While AI is impressive these days, sometimes you need personalised advice or just need to talk to a person and we’re always ready to provide it.

Your personal research assistant

Think of Chatbot Chad as your very own initio-specific Google. Ask him a question, and he will dive deep into our extensive support articles to find the answer for you. It’s like having a personal research assistant at your fingertips 24/7. Chad’s ability to quickly sift through our resources means you get the information fast. When it comes to house insurance in New Zealand, Chatbot Chad is your go-to expert. Whether you’re looking for information on home insurance policies, understanding coverage options, or help with common terms and processes. Chad has got you covered. He can guide you through the the ‘how to’s of insuring your home on our initio site.

What Chad can do

-

Help with general questions about our products and services

-

Point you to relevant pages, FAQs, and support articles

-

Help explain common terms and processes

Chad is designed to support your experience, not replace our team.

What Chad Can’t do

- Does not provide personalised insurance advice

- Does not make decisions about cover, pricing, underwriting, or claims

- May not always have the most up-to-date or complete information

- Provide updates on your claims

- Access your personal records

For anything important or specific to your situation, you should speak with one of our team or refer to your policy documents.

Fun, friendly, and professional

While Chad is highly efficient and professional, we’ve also made sure he’s fun to interact with. At initio, we believe in keeping things light and approachable, even when dealing with serious topics like insurance. Chad embodies this spirit, making your interactions with him enjoyable and helpful.

Accuracy and Reliance

While we aim for Chad’s responses to be helpful and accurate, AI-generated information can sometimes be incomplete or incorrect. You should not rely solely on Chad when making decisions about insurance cover or claims.

If there is any difference between information provided by Chad and your policy wording, the policy wording will always apply.

Privacy and Use of Information

When you interact with Chad, the information you enter may be collected and processed to:

-

Respond to your enquiry

-

Improve our services and support experience

-

Monitor quality and performance

Chat conversations may be stored and reviewed for these purposes. Any personal information is handled in line with our Privacy Policy and the Privacy Act 2020. Please avoid sharing sensitive information such as passwords, full payment details, or other information you would not normally share online.

Need help? Chat with Chad anytime, 24/7, by clicking the ‘Help’ bubble on our website

Learn more about Chad

Related pages

How do I get a Certificate of Insurance?

The Certificate of Insurance is a document that proves your cover is in place once you’ve purchased a policy. It’s also known as a Certificate of Currency. Banks and finance companies often ask for one when you apply for a mortgage or loan or when you are wanting to draw on the loan.

If you are yet to purchase the home or only looking to make an offer, you would alternatively obtain a “Letter of Intent” rather than a Certificate of Insurance.

Get your Certificate

Certificates are available at anytime once you have purchased cover through initio. You can download your certificate directly from your dashboard login. Click the Bank Certificate option on the relevant policy details. A certificate will open which you can save.

If you haven’t yet purchased your policy, please find more information here on how to get started.

Need to change the bank noted on your Certificate?

If you need to change the Interested Party (bank/loan provider) or the Insured Name on the policy, select the “Change” option on the right side-menu of the relevant policy. You can then update the policy and we’ll automatically send you an updated Certificate to your email.

Need to change the dates?

We are unable to alter the inception (effective) date of a policy once it’s been purchased. You can, however, cancel that policy from your dashboard back to the original inception date and re-purchase the policy (from your dashboard) with the correct date. A new certificate will be forwarded within minutes. Our system will also automatically provide you with a full refund for the original policy.

Please find more information regarding changes to a purchased policy on our site here.

Useful Links

When do I need house insurance?

Navigating your dashboard

Confirmation of cover

Property inspections – 3 things landlords need to know

The requirement for 3 monthly property inspections forms part of most landlord insurance policies.

A rental property that is inspected regularly is less likely to be ill treated by its tenants, and if the property does suffer some damage it is easier to establish what and when it happened.

There is widespread debate among landlords, tenants, property managers and insurers as to whether 3 monthly inspections are too frequent and disruptive to tenants.

What is not well understood by landlords is that superior landlord insurance policies (like initio) provide insurance irrespective of whether property inspections are being completed or not.

So, here’s three things you need to know:

1. You are still insured if you don’t do property inspections

From an insurer’s perspective the landlord obligations are NOT a requirement to make ANY claim acceptable. At claim time, property inspection information will only requested when the claim is for a tenant related loss such as meth or malicious damage.

So if you are making a claim for intentional damage caused by the tenant or meth contamination – your insurer may ask to see copies of your property inspections. However, if your claim is for damage not related to the tenancy such as a burst water pipe, a storm blowing the roof off, an earthquake, or total loss house fire (to name just a few) the insurer will not be interested in your property inspections as they are not relevant.

2. 6 monthly inspections used to be the norm, until …. Meth.

It is only recently that insurers have moved to 3 monthly inspections. This is a direct consequence of the rising cost of methamphetamine contamination claims.

To put this in perspective, at its height Initio was receiving a new meth claim per day, and that cost a lot of money. We noticed that a large number of meth claims could have been avoided or at least mitigated by better risk management, namely more regular property inspections. So instead of pushing prices up further to offset this risk (or excluding meth cover all together) we decided that if landlords wanted ongoing meth cover they would need to take an active role in managing the risk through, among other things, property inspections.

Good insurers (like initio) will not use the landlord obligations as a way to avoid claims, but as a way to fast track claims for landlords with good risk management.

3. New Zealand Property Investors Federation members – 4 monthly inspections periods.

We are proud to be the insurance partner to the New Zealand Property Investors Federation (NZPIF). The NZPIF take an active role in professionalising property investing in New Zealand with knowledge, leadership and resources for members.

Our data shows that property investor members have approximately 50% lower incidence of meth and malicious damage claims, compared to non members.

Members of the NZPIF who insure with Initio receive the benefit of 4 monthly inspection periods. Visit NZPIF to find out more about organisation, including how to become a member of a local property investors association. Associate membership starts from just $25 per year.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

Duty of disclosure – law changes ahead

The current situation – Duty of full disclosure

Duty is on you to disclose anything that may affect the insurance company’s decision to cover you.

When you apply for insurance you are asked declaration questions by the insurance company. You are expected to answer these to the best of your knowledge.

With current legislation, a final question is then asked to “disclose any information that may be relevant to the insurer’s decision to insure you”. This is a catch all question which does not relate to any specific question asked by the insurer.

Relevant information is deemed as anything that can affect the decision to insure the risk, and for what premium and excess.

The current full disclosure approach has drawn criticism for expecting too much from you. It’s very difficult for you to know everything that might change the premium or excess of your insurance policy.

The future – Duty to take reasonable care

Duty is on the insurance company to ask questions that help their decision to cover you. Your duty is simply to take reasonable care and not misrepresent this information when answering them.

There is currently an Insurance Contract Law Review taking place in New Zealand. Proposals for the government’s Options Paper want to change the requirements around disclosure. More responsibility is being placed on insurers to get information, instead of asking you to declare anything they might think is relevant.

You will likely see a shift from a ‘Duty of Full Disclosure’, to a ‘Duty to Take Reasonable Care’, and to not make a misrepresentation.

What this means for you

When you apply for cover the insurance company will ask more specific questions. You will no longer be asked the catch-all question to declare any other information that might be relevant.

For example, the insurer might specifically ask if your house is in a flood zone, rather than expecting you to declare this yourself without being asked directly.

We support the proposed changes and look forward to seeing what improvements are put forward. Removing the general declaration question will be an important step towards more equal expectations between you and the insurer.

For the full issues paper on the Insurance Contract Law Review click here

Learn more from leading law firm Minter Ellison, with a useful summary of the review.