It’s common for your mortgage provider or bank to want confirmation that you can secure insurance on any house you are looking to purchase (before they approve your loan).

This is known as a ‘Letter of Intent’. In simple words, it’s a document that confirms an insurer is able to provide cover on a house. This is usually what you would require if you are yet to purchase the home, but instead you want to make an offer or head to auction. This is different to a “Certificate of Insurance” which you would provide upon purchase of the home and, therefore, the insurance policy.

In summary, in looking to make sure you can get cover on a home, you would obtain a “Letter of Intent” prior to any purchase and a “Certificate of Insurance” upon purchase of the property.

With initio, obtaining a letter of intent is fast and straightforward. After completing a few straightforward steps, you can email a copy to yourself as soon as you’ve filled out the form.

Where can you request a Letter of Intent?

Begin by requesting a quote and completing our online application.

1. Get a quote

Visit our 30 second quote calculator here. You’ll need to enter an effective date, don’t be too concerned with this date (for a letter of intent) as it’s likely you won’t have a confirmed settlement date. At this point, it’s for quoting purposes only, choose a date as close as possible to a potential settlement date.

If you’re happy with the quote, you can continue by scrolling to the bottom and selecting a preferred payment interval (either monthly, or annually). But don’t worry, you won’t have to make a payment if you are only looking for a “letter of intent”.

You’ll then need to fill out our three online application pages. These include information about the property, your details, and completing the disclosure and claims history page.

Fill in these pages as if you will be the successful bidder/purchaser. This means putting your name as the property owner, etc.

3. Submit a referral, or request a Letter of Intent

If we need to review your application, the next option will submit your info for a review. In some cases, a review will require us coming back to you wanting some more information or detail, we aim to do so within one business day.

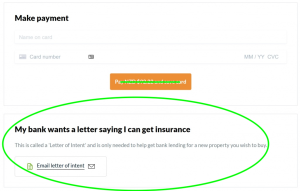

If no review is needed, you’ll go through to a summary page where there is an option below the make payment section to send a ‘Letter of Intent’ to your email. No payment is required to download the ‘Letter of Intent’ option which will give you a pre-approval document for your peace of mind and any finance. Select this option and enter your email address.

A confirmation document will be automatically sent to your email, and that’s it! You can then easily forward this to your bank or mortgage provider to finalise the process. Note that the Letter of Intent is not a Certificate of Insurance so won’t show a start date or confirm cover is in place. What it will show is that you are able to obtain cover with initio, should your purchase be successful.

If you need a Letter of Intent, start by getting a quote:

Digital only matters when it makes things easier at the moments that count.

You’ll often hear us described as a fully digital insurance provider. That’s true. But what does being digital actually mean for the people who insure with us?

For us, digital isn’t about removing people from the process. Removing the friction that gets in the way of something that should be simple is what it’s about.

Because our systems do the heavy lifting. Our support and claims teams avoid manual paperwork. They don’t have to re-enter details. They also don’t have to chase forms. Claims don’t need to be lodged through multiple phone calls. You don’t need to stitch insurance policies together by hand.

That time shifts to what truly matters when you feel overwhelmed, under pressure, or just want a clear answer.

It means we pick up the phone when you call or respond to you online in an instant.

Technology that gives time back to people

We use technology to make things faster and clearer. Things like online quotes, a customer dashboard, and a chatbot that can answer common questions at any time of day.

But here’s the key part: if our chatbot can’t give you the answer you need, it doesn’t trap you in a loop. It puts you through to a real person, straight away.

Digital tools should never be a barrier. They should be a shortcut.

That’s why we design everything we build on the technical side to give our team more time to help, not less.

People first, always

Have a look at our reviews, and you’ll see a common theme. People talk about being able to get hold of someone. About feeling listened to. About their insurance claims being handled with care.

Insurance claimscan be stressful for customers, and sometimes emotions run high; not every situation is simple. But when things are stressful, the last thing you need is to be playing phone tag with your insurance provider.

Digital insurance on its own isn’t enough. Digital only works if it makes human support easier to access when you need it most.

Why this matters when things go wrong

I saw this first-hand over Christmas when a family member was involved in a car accident. Thankfully, no one was seriously hurt.

In the middle of it all there were police, ambulances, fire trucks, people from the other vehicles, and broken glass mixed with Christmas pavlova scattered throughout the car, alongside tow trucks that needed organising. It was already stressful. Trying to get hold of someone, anyone, about the insurance only made it worse.

We couldn’t find details about their insurance policy details online, and their login didn’t show anything useful. There was no clear next step, just waiting and uncertainty at a time when answers mattered.

All I could think was how different this would have been if they’d been with initio. A claim could have been lodged immediately online; the system would have provided clear instructions on what to do next and what to expect from your insurance provider. All policy details and cover information would have been sitting there in one place.

Simple, transparent, and there when it counts

That’s one of the things we’re most proud of. With initio, your insurance policy, documentation, and details are available online through your dashboard. No digging through emails. No wondering what you’re covered for. No guessing who to call.

Insurance is stressful enough without added complexity.

Being a digital insurance provider isn’t about doing less for our customers. It’s about doing better. Using technology to remove the noise, so when you really need us, we’re available, responsive, and human.

Because at the end of the day, we’re not just digital. We’re people first.

Written by Megan Fisher, Head of Marketing at initio.

Megan has been with initio since 2022 and has over 20 years’ experience in marketing and product strategy. She works closely with initio’s claims and customer experience teams, giving her a first-hand view of how insurance works when customers need it most.

If you insure your home with initio, part of what you pay includes a compulsory levy for Natural Hazards Insurance. This levy gives you access to cover provided by the Natural Hazards Commission Toka Tū Ake (NHC), previously known as the Earthquake Commission (EQC). It sits underneath your initio policy and covers specific parts of your land and home when they are damaged by natural disasters.

NHC cover is a type of government-provided insurance that operates under the Natural Hazards Insurance Act 2023 to help with the cost of repairing or replacing your residential home and specific parts of your land that are damaged by:

Earthquake

Tsunami

Landslip

Volcanic eruption

Hydrothermal activity

Storm or flood (land only)

You receive the NHC cover automatically when you purchase a house insurance policy. If a natural disaster damages your home, NHC will help to pay for the cost and your home insurer, such as initio, will pay the rest up to your selected sum insured (within the terms of your policy).

What Natural Hazards cover is provided by NHC for your home?

Cover for your home or holiday home, plus related outbuildings such as a shed, garage or pergola.

Essential services connected to your home (for example water, drainage, sewerage, gas, electricity or telecommunications) up to 60 metres from the home.

The maximum amount the NHC will pay towards repairing or rebuilding a home for a covered event is $300,000 plus GST for events on or after the 1 October 2022. If the damage relates to an event prior, the cap may be lower. The limit is per insured dwelling unit.

Anything above that cap is covered by your private insurer through your home policy.

Although your initio policy pays for the top up cover on your home, it’s important to know that initio cannot top up or extend any land cover beyond what the NHC provides. The amount paid by the NHC is the full entitlement for land under the Natural Hazards Insurance Act, and insurers are not able to offer additional land cover above this cap.

This means that if the cost to repair or stabilise the land is higher than the NHC settlement, initio is unable to pay the difference. Your initio policy will continue to respond to damage to your home and other insured buildings, but any extra cost relating purely to land sits outside the policy and cannot be covered.

What Natural Hazards cover is provided by NHC for your land?

Under the NHC, you are insured for the land that is inside your legal property boundaries AND;

under your home and some related outbuildings

within 8 metres of your home and select outbuildings

under or supporting your main accessway for up to 60 metres (for example, the land under your driveway)

New Zealand is one of the only countries where homeowners have access to residential land cover. But it’s important to understand that this cover is limited and does not extend to all parts of your section.

Your land cover is based on a land cover cap, made up of:

the market value of your insured, damaged land

the value of insured retaining walls, bridges and culverts (to a limit)

If it costs more to repair the land than it is worth, the NHC will cash settle based on the land’s market value at the time of damage.

This means Natural Hazards Insurance usually contributes toward repairs rather than fully covering them.

What if my property has a Section 72 or Section 51 Notice?

Section notices are warnings placed on a property’s title that inform current and future owners, insurers and lenders about known or newly identified natural hazard risks. They affect how claims under the NHC’s natural hazards cover are assessed. There are two main types:

Section 72 notices (under the Building Act 2004).

A Section 72 notice may be placed when a building consent is granted for land that has a known hazard (erosion, slippage, inundation etc).

If you later make a claim for damage caused by the hazard listed in that notice, the NHC may fully or partly decline your claim.

If the damage is caused by a different hazard than the one specified in the notice, the normal natural hazards claims process applies.

Section 28 or 51 notices (which limit or cancel cover after a claim settlement)

These notices apply when the NHC limits or cancels natural hazards cover after a previous claim, for example if repairs haven’t been made or the hazard risk remains unaddressed.

Once a notice is placed, cover is limited or cancelled from the date of notification — and stays on the title until the homeowner provides sufficient proof of repair or risk mitigation.

If the cover is cancelled, future natural hazards claims may not be accepted for that property.

Section notices are important because they can affect your insurance cover under NHC policies and influence how your private insurer treats your claim. For homeowners, it means full disclosure of any known hazards or title notices is vital — failure to do so may lead to claim difficulties. Repairing or mitigating hazard risks after a claim is critical to avoid a Section 28/51 notice limiting future cover.

How much does the levy cost me?

It depends on your sum insured but for the vast majority of homeowners, the annual cost is $552 incl gst ($46 per month).

If you have a home or unit with lower sum insured the levy increase will not be as much, and you may even see a reduction in NHC levy.

Does the NHC levy change by region?

No, it’s a flat charge regardless of where your home is. So Auckland homeowners pay the same as Wellington homeowners. The cover and the levy does not take account of regional natural disaster risk.

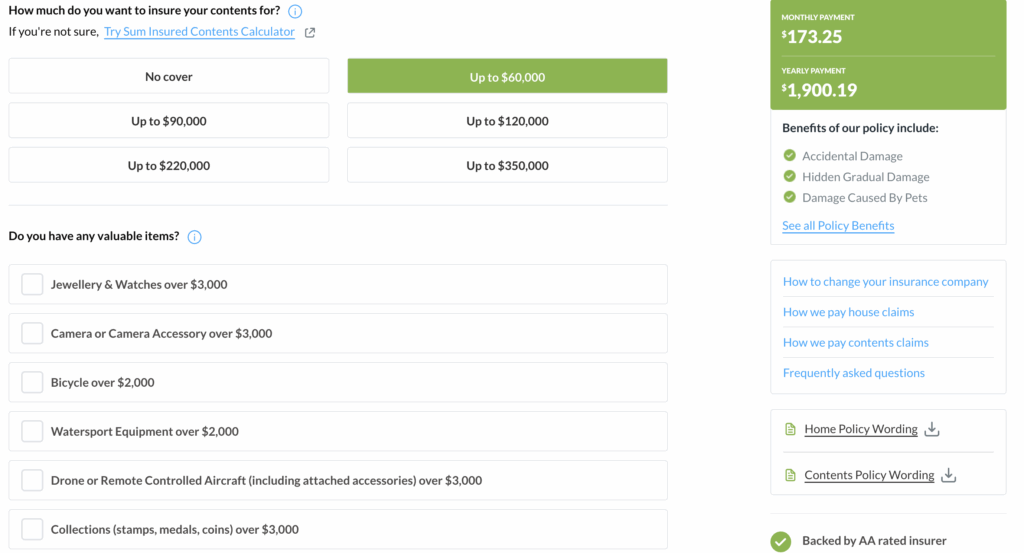

Yes, while your contents insurance covers most of your belongings up to the sum insured shown in your policy schedule, there are some limits that apply to certain types of items and situations. Knowing these limits can help you decide if you need to specify an item on your house insurance policy to ensure full cover.

If you’re not sure what everything in your insurance policy means, our guide on how to read an insurance policy walks you through in a simple, easy-to-follow way.

General policy limit

For any single event, the most we’ll pay for all your contents combined is your sum insured (listed on your policy schedule).

Item-specific limits (unless the item is specified on your policy)

Jewellery, watches, earrings, collections, cameras – $3,000 per item

Surfboards, windsurfers, paddleboards, kite surfers, surf skis, dinghies, kayaks, canoes – $2,000 each (including parts/accessories in or attached to them)

Remotely piloted aircraft (drones) – $3,000 each (including parts/accessories in or attached to them)

Bicycles – $2,000 each

Money, bullion, unset precious stones, credit/debit cards, and stamps (not part of a collection) – $1,000 total

Parts and accessories for watercraft, motor vehicles, trailers, caravans, or aircraft (if not in or attached) – $2,500 total

Combined jewellery and watch limit

If you lose multiple unspecified jewellery/watches in one event, the total is capped at $15,000 unless your policy schedule shows a higher amount.

Special benefits with separate limits

Home office equipment – $10,000 at home, $1,500 while away

Alternative accommodation – $20,000 per event (up to 12 months)

Children living away from home – $500 per item, $5,000 total

Hidden gradual damage – $2,000 per year

Credit/debit card fraud – $500 per year

Overseas travel cover – $5,000 per trip (up to 3 weeks)

Keys and locks – $1,000 per year

Stress payment – $2,000 once per total loss claim

When to specify an item

If you own high-value items (like an engagement ring, top-end bike, or premium surfboard) that are worth more than these limits, you can list them as specified items on your policy for full replacement cover.

If you’re still unsure, you can reach out to us directly – or even use an AI chat tool to quickly search your policy for specific details – just remember to always double-check the results!

A candid take on initio’s approach to you and your home

At initio we are ‘all-in’ on customer experience. We ruthlessly pursue customer satisfaction with our technology, support and communications …. But only for a certain type of customer. In short, we are not for everyone.

Yes, we’re audacious enough to say: “Sorry, we can’t be your insurance provider” – at least not if it means compromising the ethos that underpins our brand, or transacting with you in a way that doesn’t celebrate the use of our tech. We provide superior ease of insurance and customer service, but only to a specific kind of customer who appreciates and respects our ‘digital by default’ approach.

Catering to the Modern, Digital-Savvy Customer

Our business model is laser-focused on a modern, self-reliant breed of customers. The digital age has dramatically reshaped the insurance industry, and initio remains at the forefront of this transformation. We are designed for customers who value autonomy, speed, and convenience, rather than the traditional, hands-on approach.

Customers who are comfortable transacting online, managing their property portfolios with digital tools, and who comprehend that competitive premiums and high-touch hand-holding services are often mutually exclusive, are our ideal clientele. For these customers we are digital by default, and human when you need us.

The Interplay of Technology and Affordability

“Why can’t you just start the policy for me over the phone”

“Why don’t you call me every year when my policy renews so we can have a chat about it”

“Why can’t you just send me your bank account and I’ll transfer the premium funds”

“Send me a quote”

It’s a ‘no’ on all fronts. The truth is, high-touch insurance services involve considerable operational costs – think travel, long-winded phone calls, time, and administration. We’ve spent over 10 years building a digital platform that substitutes for these things; its frictionless insurance, that’s quote in one click, cover in 2 minutes, claim in an instant. By utilising technology to automate many aspects of our services, we increase efficiency and are able to offer competitive pricing.

Our system has been designed to suit a certain type of customer, and it’s not for everyone.

This doesn’t mean we shirk our responsibility to our customers that embrace our technology. Quite the contrary – we provide comprehensive digital and phone support, and abundant online resources to help.

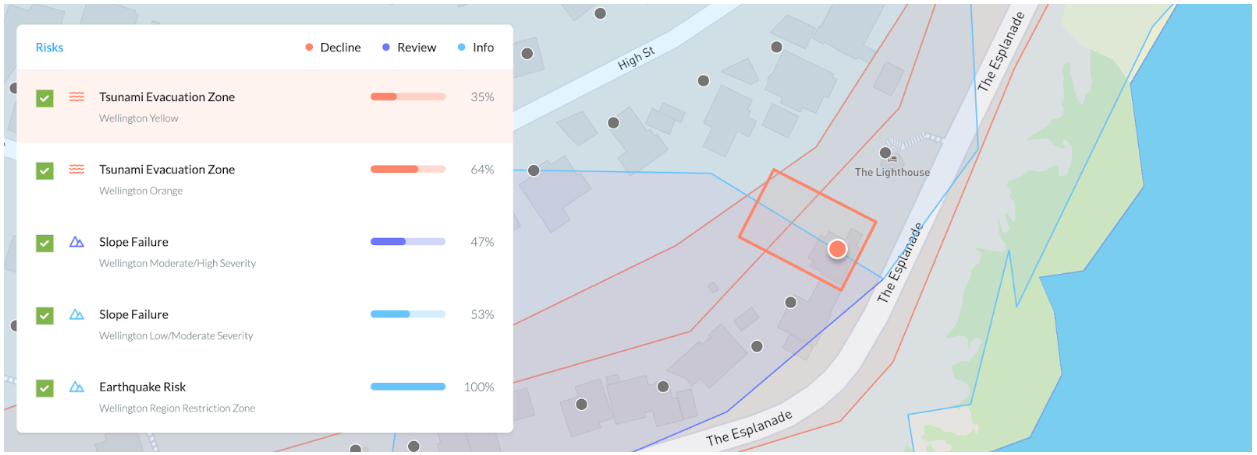

Why we decline to insure some houses

Sometimes we have to say no to insuring your house. It’s not you, or your house, it’s simply the way we want to run our business and the rules we, and our insurer, have had to create to be able to offer our services long-term.

It’s digital too: The primary decision making on whether or not to insure your property is done by a smart tool we built called ‘Locatio’. When you type in your address with initio, Locatio makes decisions about whether initio can provide cover by using things like council property data, flood maps, earthquake and land risk.

In order to remain a sustainable and successful insurance provider we choose to focus on certain types of houses, and this means that there are some locations where we can’t provide cover, and certain risk exposures such as flood or land instability that are just not our bag.

We are constantly updating our business and underwriting rules, so just because we say no today, doesn’t mean that it’s a no forever.

You also need to know that we cannot sell you something that isn’t right for your situation either. So if your property does not fit our product we’ll decline to provide cover, and we don’t mean any offence by this.

The cost is the cost

A number of factors go into calculating the total cost of your home insurance, including location, age of the property, and other things like government-imposed levies. Our award-winning insurance technology computes the insurance cost, and we rely on that to run our business. The premiums need to be set at a level that allows the insurer the margins to continue to pay claims and reinsurance costs. In short, the cost is the cost.

Learn more about how the insurance risk component of your insurance cost is calculated

It’s 100% your choice whether or not to accept the insurance cost we offer. You can ring or email and challenge a cost but ultimately it’s out of our hands as the system has spoken. You need to know though that we work incredibly hard to maintain competitive premiums for our customers. We do this by continually investing in our technology for efficient processes, negotiations with our insurer, constantly refining the rules that determine how risky our portfolio of houses is (ultimately the more aggregated risk we take on, the bigger our premium pool needs to be).

Our efforts to keep premiums competitive have been confirmed by feedback from our customers and also by financial resource websites like Moneyhub.

Source: Moneyhub

It’s simply not possible to be the most competitive all of the time, and we implore our customers to take a long and holistic view of their insurance that takes account of things like support (can you get you easily get ahold of your insurer), claims responsiveness, ease of use, technology and overall confidence in your provider.

It’s worth bearing in mind that not all policies are built the same, so just comparing price vs price doesn’t quite cover it. We highly recommend using our comparison tool if you want to see how we stack up when you also take the policies into consideration.

An Unapologetic Philosophy

Our philosophy is blunt but honest: “We are not for everyone”. Our model isn’t all things to all people, and that’s intentional. We’re looking for customers who align with our ethos – those who want a superior digital service.

While we understand some may expect more traditional customer service methods, we respectfully suggest they may be happier elsewhere. This is not a dismissal, but a candid admission that our service model may not suit everyone’s expectations.

In sum up, initio is unyieldingly committed to delivering our unique brand of customer experience, one that is unabashedly shaped by the needs of modern, digital-savvy customers. While our approach may not resonate with everyone, we are firm in our refusal to compromise on the affordability and efficiency that our model provides.

To our customers who find value in what we offer, we welcome you wholeheartedly. To those who don’t, we don’t hesitate to say: “We are not for you” And that’s how we maintain the balance that allows us to continue delivering what we believe is the optimal blend of service and affordability in today’s market… all driven by our technology.

Every year, our claims team sees the serious stuff that reminds you why house insurance and landlord insurance matter: storms, leaks, break ins, big events.

But in between the big moments, there is another side to the story. Tiny humans, runaway trampolines, drones with a death wish, and phones that seem determined to meet every body of water in New Zealand.

This is a light look at some of the more unusual patterns from our 2025 claims data, based on what we saw in the initio book.

House and contents

Tiny humans breaking things

Kids just love to push limits

Children do not show up in most claims, but when they do, the stories are very easy to picture.

Looking across our 2025 claims:

Around 1 percent of all claims mention a child somewhere in the story

For contents claims, that jumps to roughly 7 percent

In some towns, around 3 in every 100 claims mention children in the description

On our books, you are most likely to find tiny humans breaking things in:

Cambridge

Nelson

Gisborne

Palmerston North

Queenstown

What are they breaking?

Screens and devices

Glass doors and windows

Soft furnishings and carpets

The odd high value item that probably should not be within arm’s reach

Common themes in child related claims are:

Accidental damage makes up more than 40 percent of the kid stories

Followed by water damage from spills and overflows

And glass breakage, usually with balls, scooters, toys or bikes hitting windows and doors

So while the bulk of our book is still storms, leaks and more traditional events, there is a clear pattern of small people and big repair bills.

Claim spotlight: the mobility scooter vs the glass door

One claim that deserves its own call out: a child driving a mobility scooter into a glass door.

It reads like a scene from a comedy, but it is a real claim with real broken glass and a real clean up.

It is a good reminder that accidents do not always look like the classic storm or burglary. Sometimes they look like kids having a bit too much fun practising to be the next big grand prix driver.

Runaway trampolines

If you own a trampoline, you probably already know it tries to rebrand into an aircraft in any kind of decent wind.

From our 2025 claims:

Trampolines make up only a tiny slice of all claims, but

They are roughly 3 percent of all wind and storm claims

Most storm claims are still for roofs, fences and leaks, but about one in thirty wind claims involves a trampoline trying to escape the backyard and live its best life out on the road.

A few of the real descriptions include:

A trampoline that simply blew away and was never found

A small tornado lifting a trampoline onto a roof

Trampolines taking out fences on the way past

For home and contents insurance, it is a useful reminder that the risk in a storm is not just trees and roofing iron. It is anything light enough to take off, so tie things down before the next big blow.

Drones go rogue and fishing gear with a death wish

Ten years ago, it was rare to see drones or motorised kontikis in claims. Now they turn up often enough to be a pattern, even if they are still a small slice of the overall numbers.

A lot of the drones we see are used for fishing, taking lines out past the breakers, which is why they sit neatly alongside kontikis in our claims. Others are doing land based duty, filming the backyard or the farm, and getting into trouble there instead.

In 2025 we saw plenty of examples of drones and kontikis going AWOL, including:

Drones hit by waves, sinking into the ocean or just lost at sea, never to be seen again

Drones colliding with power lines or crashing on land

Kontikis colliding with rocks or other solid objects and coming back broken

Kontikis filling with water or just sinking and never making it back to shore

Put simply, some of the gadgets people use to fish seem very keen to join the fish.

These claims are still only a small fraction of what we see overall, but they are modern, very Kiwi, and show how quickly new tech turns into new kinds of risk.

New tech, new kinds of trouble

Phones, laptops, tablets and smart devices feature more and more in our claims.

Across our 2025 data:

Roughly 1 in every 80 claims involves a mobile phone

Around 1 in every couple of hundred claims involves a laptop

Tablets and iPads sit a little behind that, but still show up as a clear group

Robot helpers like robot lawn mowers and robot vacuums appear in a handful of cases

From an insurance point of view, it shows how much value is now sitting in small, fragile devices. For landlords, it is a reminder that tenants are bringing all this tech into your property too.

Landlord and rental property

The everyday chaos

When people think about rental property claims, they often imagine the big scary stuff: major meth damage, fires, floods, or tenants doing a runner.

Those things do happen. But a lot of landlord insurance claims are far more everyday. Think stained carpet, bumped garage doors, lost keys and a few over enthusiastic pets.

Looking across our landlord type claims for 2025 (where the description clearly involves tenants or rentals), most of what we see is surprisingly normal:

Around four in ten landlord claims on our book are simple accidental damage

Roughly a quarter are loss of rent only

The rest is a mix of impact (things hitting the house), malicious tenant damage, and keys and locks

So most of the time, it is everyday life going wrong in small but expensive ways.

Why we care about this stuff

This is a playful look at our 2025 claims, but there is a serious purpose behind it.

Every time:

A trampoline takes off in a storm

A child drives a mobility scooter into a glass door

A drone vanishes into the ocean

Tenants backing into the garage door

A phone or laptop ends up in water…

…it tells us something about how people actually live in their homes and rentals.

That feeds back into how we think about house insurance and landlord insurance. It helps us make sure common accidents are covered clearly, that our wording matches real life, and that we can give better tips on how to avoid some of these mishaps in the first place.

Behind every percentage and every claim code, there is usually a very human, very Kiwi story.

Initio Insurance knows New Zealand houses and landlord insurance – it’s all we do. Whether it’s a rental property, holiday home or your main residence, we’ve got the perfect insurance cover for you.

We provide everything you need online – instant quotes, easy cover, and efficient claims. We know your time is valuable, so we get straight to the point.

Why choose initio?

We’re specialists

We’re different because we only provide cover for houses. This means that we understand what matters to you, and you have the important cover you need as a property owner or a landlord. Find out more about the coverage options, including landlord insurance here.

We save you money

We run the entire insurance process online – including quotes, payments, and claims. This means our business costs are lower; savings which we can then pass on to you.

We love being online, but you can always contact us by phone or email. Even better, we don’t send your call to a faceless claim centre; your call will be taken by one of our highly experienced team.

We’re secure

Initio is underwritten by Lumley, a business division of IAG New Zealand Limited, which means if the unthinkable happens and disaster strikes, we’ll always have you covered. Read more about IAG’s financial strength here.

We keep you updated

When you submit a claim, we will confirm the details and keep you informed of its progress. The only real value you see from your insurance cover is at claim time, and that’s why we make it easy.

We send you email reminders when your policy is due for renewal, so you have plenty of time to login to your dashboard and renew your policy before it expires. At any time you can contact the initio team about coverage, a change in circumstances or any other queries.

What do our customers have to say?

Don’t just take our word for it; click the below link to see what our customers think of initio and whether they would recommend initio to their own friends and family.

If you’re new to the rental property game, you’re probably searching the internet, asking yourself, what does landlord insurance cover? It’s important to find the right policy that covers you if things go wrong – whether it’s tenant-related damage, loss of rent, or unexpected repairs. The last thing you want is to be caught short with the wrong type of policy from an insurance provider that doesn’t specialise in landlord insurance.

That’s where initio comes in. We live and breathe landlord insurance, making sure your rental property is in the hands of a provider that understands the challenges landlords face.

Owning a rental property can be a great investment, but it’s not without risks. That’s why having the right landlord insurance is essential – it helps safeguard your investment from unexpected costs, such as tenant damage, legal claims, and loss of rental income.

What landlord insurance with initio typically covers:

Loss of rent – Cover for lost rental income if your property becomes uninhabitable due to damage or if tenants leave unexpectedly

Deliberate damage – Protection against intentional damage or theft caused by tenants.

Meth contamination – Cover for decontamination costs and additional rent loss during cleanup.

Landlord contents – Coverage for furniture, appliances, and other items you provide in the rental.

Replacement cover – Full rebuild protection up to your insured sum.

Legal liability – Protection against legal costs if your property causes damage or injury.

Excess-free blocked pipe cover – Coverage to unblock underground pipes without paying an excess.

Hidden gradual damage – Cover for gradual water damage caused by hidden water pipe/tank leaks.

Excess-free keys and locks – Replacement of lost or stolen keys and locks with no excess to pay.

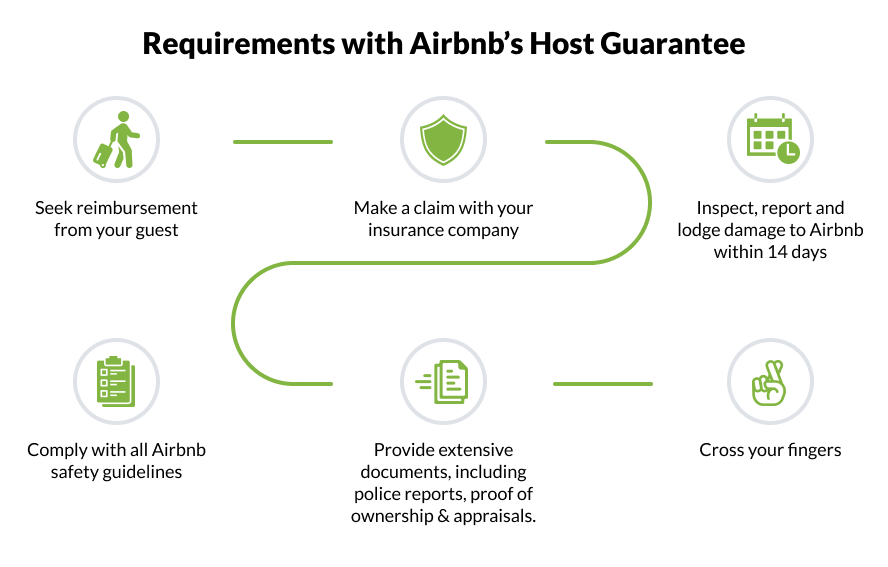

Many hosts rely on Airbnb’s well-advertised $1USD million of free Host Guarantee cover. But be warned, this can lull you into a false sense of security leaving many disappointed when they make a claim but find they don’t tick the boxes.

The rules are specific, which can make it hard to claim especially when innocent hosts unknowingly violate the conditions.

What does it cover?

The Airbnb Host Guarantee isn’t a formal insurance policy, but rather a strongly-worded promise to rectify guest damage providing your situation meets certain conditions.

It isn’t regulated by the New Zealand Financial Markets Authority, so you would struggle to take them to court locally if things really turn sour.

Last Resort for Recovery

In Airbnb’s own words they say the Host Guarantee is not an insurance policy, and shouldn’t be considered a replacement.

Firstly, the guarantee can only be claimed on after trying to recover compensation from the guest, and then your own insurance (if you have this). Already the Host Guarantee is a last resort.

For a chance of recovery from the guarantee, you’re going to have to prove you persistently chased up that festival-goer to get $800 back for a living room wall repair.

There are many examples of people angry about their payout from the guarantee. Usually it’s because they aren’t aware of the conditions.

A main stump is that damage needs to be inspected, reported and lodged to Airbnb within 14 days, or else you’re out of luck.

By the time you’ve checked in your next guest it could already be too late. This could be enough to kill any claim through the Guarantee if you live away from your Airbnb.

Remember that you need to seek recover from the guest, and then your insurance before you lodge a claim in the 14 day window. The requirements almost seem like a trap to get you to exceed the strict 14-day deadline.

Watch out for Exclusions

Only damage that happens during the booking period is covered. If an unwelcome guest overstays their welcome and causes damage, there won’t be cover.

Cover only applies to part of the house that’s in your listing. If you rent a room, but your guest uses another bathroom and causes damage, you’ll need to foot the plumber’s bill yourself.

It’s full of various exclusions; like damage from excessive water utility use (a sink overflow won’t be covered), and any damage by animals or pets (are you sure your guests won’t bring their dog?).

Be prepared for stacks of bureaucracy when you make a claim. Airbnb require extensive police reports, proof of ownership and request form documents for damage.

The list of exclusions goes on. To read the full terms, conditions and exclusions see here.

No Liability Insurance

Finally, the Host Guarantee doesn’t help when it comes to legal liability. If your guest suffers an injury and they sue you, the Host Guarantee will fall seriously short.

The idea of someone stubbing their toe on the coffee table and suing might seem ridiculous, but legal liability also extends to things like sickness (if an illness is caused by the condition of your house) or freak accidents.

Is it worth the Risk?

One-in-seven Kiwi Airbnb hosts report damage. That’s about a 15% chance you’ll suffer damage one-day.

While most reports are minor and hosts voluntarily pay to avoid the lengthy resolution process, we’ve heard some shocking stories ranging from vomit-covered walls to 100-person guest parties.

Hosts should ask themselves if relying on the Guarantee is worth the risk? After all, Airbnb themselves recommend having robust insurance in place in the first instance.

Initio Insurance are the pioneers of online house insurance in New Zealand, with cover specifically designed for own homes and holiday homes also rented on Airbnb.

Is it only used as extra space for your household?

If you have two dwellings on your property and the second one is used only by you or your family—without being rented out—it’s important to have the right insurance to cover both spaces.

What counts as an extension to your own home?

If the second unit/home is;

Used like a sleepout for members of your immediate family, such as teenagers or elder family members.

And you all predominantly share meals and/or facilities OR

Used as a hobby room such as an art or music room OR

Used as a home office space, then

It’s considered as an extension to your home and counts towards the one home unit/dwelling.

What insurance do you need?

For this setup, you only need one home insurance policy, which will cover both your main home and the second dwelling under the same policy. This ensures protection for:

Your home and any structures used as part of your home for residential purposes on the property

Get covered today

With initio, you can get a quick quote and buy insurance online in minutes, making it easy to ensure your home and second dwelling are fully protected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

An existing client of yours is up for renewal on their House & Contents, Landlord or Holiday Home and needs cover.

An existing client of yours has purchased a new/additional house and needs cover.

A new customer has approached you for House & Contents, Landlord or Holiday Home insurance.

Getting your client online is easy with initio

Use your initio landing page to quote your customer’s house

Choose the relevant property type (own home, rental, holiday home)

See instant quote on screen. From the quote screen email yourself the quote

Select the expected start date of insurance.

Set the sum insured to the amount discussed with your client, their current sum insured, or leave it as the default sum insured.

Click ‘Save & email this quote’.

Enter your client’s name and then your email address.

Separately email your client the price (and high-level details of the cover) and include the ‘restore quote’ link you received in the email from initio. (copy the link/url)

If your client would like to proceed with the cover they can click the restore quote link, which will give them the ability to dynamically things like excess, sum insured, contents etc., In this email, you may also like to compare us with other insurance companies.

Please note:

Initio does not onboard these customers. For compliance reasons, the customer must complete the signup online themselves in order to answer the proposal questions.

Prices can change so please select the correct expected start date.

If the property is pre 1935, or in a certain risk zone this may trigger a referral to the initio team. They will need to review the cover, and potentially obtain further info before deciding on whether or not to offer cover.

Alternatively, simply send your broker landing page link to the customer.

If your client already has a property insured with initio, then simply refer to login to their own initio dash, click the ‘House Insurance +’ button, and enter the property address.

Monthly payment is limited to credit cards or Visa/MC debit cards. Annual is a credit card or account2account (real-time bank transfer).

Monthly insurance cover means that it is renewed and paid for each month. It’s a month-to-month policy that automatically renews and is charged to your credit card on the same day each month.

How can I pay monthly?

You can choose to either pay monthly or annually when you first purchase a policy. Our monthly payment is only available with a visa debit or credit card payment. We don’t offer a monthly direct debit from your bank account.

For details on switching between monthly and annual payments, check out our article on ‘Switching Payment Frequency‘.

Will you tell me if my monthly insurance payment changes?

Yes, we’ll let you know in advance if your monthly payment is going to change thirty days prior to any payment.

Your total insurance cost will typically change on the anniversary of your policy (i.e the day and month you first started the cover). This means that your monthly payment will remain the same for the year. The exception being that if there is a government levy change (for example Fire & Emergency New Zealand levy rate change) that is mandated to be applied from the effective date of your next monthly renewal.

Each month we will send you an email confirming the renewal of your policy. In that email, if the next month’s payment is going to be different (i.e its the anniversary renewal) we’ll let you know.

Your initio dashboard will also show you the date and amount of your current and next months payment.

When will my card be charged?

When you first purchase your policy the first payment will be withdrawn from your card on that day. All following monthly payments will be withdrawn from your card the day your policy renews (your chosen renewal date).

For example, if you buy a new policy on the 1st of January and the start date of the policy is the 5th of January, you’ll initially be charged for the first month on the purchase date, ie 1st Jan. All future monthly payments starting from the February renewal will then be withdrawn on the 5th of each month.

What if I need to change my card details?

You can change the card that’s used for the payments at anytime. To do so, please login to your initio dashboard and choose “credit card” from the “account” menu in the top right corner of your dashboard. Here you can enter the new card information and any future payments will automatically default to the new card. You can also see what card is currently registered for your payments on this screen.

What if my monthly payment fails to go through?

We’ll make four attempts in total to process the payment, you’ll receive an email notification each time — whether the payment succeeds or fails. We’ll include when the next transaction attempt will be on our email correspondence, so you can ensure funds are available at the right time.

Prior to the fourth and final Attempt:

You can contact us prior to the final fourth attempt to request the payment to go through at an earlier preferred time. You can also trigger an earlier payment re-try by updating your credit card details kept in your initio dashboard — updating this field (even with the same card info) will automatically trigger an immediate re-try of any outstanding monthly payment.

Get in touch with your bank if the payment has missed despite the funds being available, in some cases your bank may have put a hold on transactions for security reasons.

Cover remains in place pending the successful payment within this time.

After the fourth and final Attempt:

If the premium remains unpaid after the final fourth attempt, the policy will lapse. Cover then ceases back to the date of the initial missed payment.

We are unable to re-activate the original policy once it has lapsed. To re-instate the cover at this time, please do so by beginning a new policy from your initio account (dashboard) using the ‘+’ options.

What if I want to use a different card for each policy?

If you are purchasing annual insurance, you can use a different card for each and every purchase. If you are purchasing monthly insurance, we are only currently able to facilitate one card for any monthly payments under your account. If you wish to use a different card for a monthly policy, you will need to set up a new initio account using an alternative email address for any policy to be paid via the new card.

What if I want all my monthly policy payments to be aligned on the same day of the month?

The monthly due date automatically aligns with the original inception date of the policy. Should you wish to change a policy’s monthly due date you would need to replace it with a new policy, effective on the preferred date. Once the new policy is in place, you can then cancel the original policy, any unused portion of that policy will be automatically refunded.

Why does the cost of insurance change?

There are a number of reasons why your house or car insurance premiums can change each year. Some of the more common reasons are:

Change in the costs of materials and labour, which makes repairs to houses and cars more expensive (Covid supply chain issues put pressure on materials costs)

Increased in the frequency and severity of weather events (Auckland Floods 2023, Nelson Floods 2022, Napier floods 2023 & 2021, Auckland tornado 2021 to name a few)

Government earthquake levy changes

Fire Service levy changes

Increased re-insurance costs due to the way international insurers view New Zealand’s natural disaster risk (NZ is one of the highest risks in the world unfortunately)

For cars, the main driver may have had birthday or an accident which changes the risk and in turn changes the premium (up or down) at the next policy anniversary renewal.

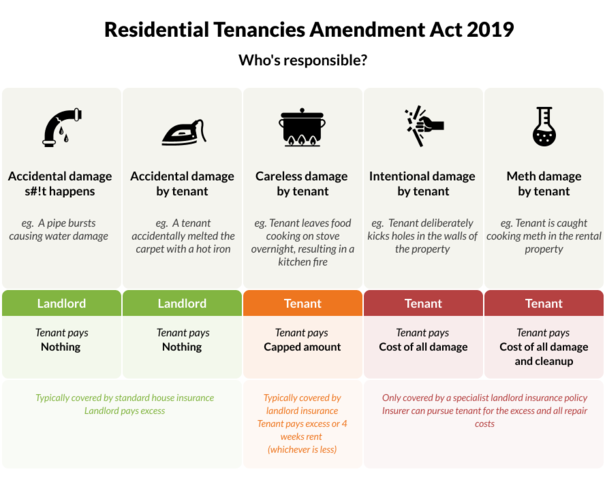

1. A tenant can be held fully responsible for intentional damage

A tenant who intentionally causes damage can be held liable, and the landlord can ask them to pay for the damage. This seems like common sense.

If the landlord has insurance cover for deliberate damage, they can lodge a claim with their insurance company. The insurer will pay for repairs, and try to recover the costs from the tenant later down the track (if it’s possible).

2. A tenant can be held partially responsible for careless damage

If a tenant has ‘carelessly’ caused damage they can be held responsible, but only up to a maximum of the landlord’s insurance excess, or four weeks of rent (whichever is less).

But what is considered careless? We’ll get to that shortly.

In this case, the tenant can share in with the benefits of the landlord’s insurance cover.

3. A tenant cannot be held responsible for accidental damage

If a tenant accidentally causes damage the act considers that sometimes; these things just happen, and the damage is the landlord’s responsibility.

However, this falls into the same problem. It’s often not crystal-clear whether damage is ‘careless’ or ‘accidental’, nor is it something the landlord and tenant may easily agree on.

Many things that would ‘sensibly’ be considered careless, have been ruled by the Tenancy Tribunal as accidental – such as knocking over and leaving a hot iron to melt into the carpet.

So it’s a good idea to read through some recent Tribunal decisions – this may be helpful for future tenant discussions.

A case of melted carpet

The 2019 changes to the act are still relatively fresh and we could still see its interpretation change. This 2020 example gives an indication of the Tribunal’s approach to the difference between careless and accidental damage.

Braziers v Guttman 2020

A landlord (Braziers) took their tenant (Guttmann) to the Tenancy Tribunal to recover damage.

The landlord alleged a patch of carpet was melted, and claimed the cost of carpet replacement from the tenant for $772. The tenant admitted the carpet was melted when they accidentally knocked over a hot clothes iron.

To avoid any liability the tenant needed to prove that they didn’t carelessly or intentionally cause the damage, and that it was a reasonable accident.

The tribunal decided the carpet damage was accidental in nature, and did not have enough ‘careless’ elements to render otherwise. There was no liability against the tenant for repair costs or excess, and the landlord would need to pay for the repairs themselves, or through their insurance (and pay the excess).

Accidental Tenant Damage vs Careless Tenant Damage

As we’ve mentioned, the Act’s definition of the difference between accidental and careless damage could be better, and we are now seeing the results of this coming through the Tenancy Tribunal process. Here’s our overview:

Accidental damage is something caused by the tenant, but outside their control (for example, tripping and putting a knee through a wall).

Careless damage is caused through lack of attention or concern for the consequences (for example, leaving a stove on while you go to do something else).

But ultimately these guidelines will be up for subjective judgement. We expect to see more disagreements between tenants and landlords over who’s liable for damage. If you’re a landlord that’s applying to the Tenancy Tribunal to see what they think, you should be prepared to prove that damage was caused intentionally – or at least carelessly to avoid paying an excess.

What’s our position on all this?

We believe a clearer division between what is accidental and careless tenant damage is needed. If no clear interpretation can be made then ideally all tenant damage – whether careless or accidental – should be treated as the responsibility of the tenant (up to the smaller of the excess or four weeks rent).

This will save a lot of time and arguments. However, based on recent cases the Tenancy Tribunal doesn’t quite see it the same way.

Why can’t the tenant use their own insurance to pay for the damage?

That’s a good question.

In the past tenants were considered completely responsible. If the tenant had their own contents insurance the landlord could rely on this to pay for damage by the tenant. Almost all contents insurance policies will include the tenant’s liability to at least $1 million for accidental damage.

For many landlords, confirmation of contents cover became a condition of tenancy; if the tenant accidentally burnt the house down, the landlord’s insurance company could get the money back from the tenant’s insurance company.

Then a couple of big things happened.

1) Court of Appeal decision on Holla v Osaki

This landmark ruling established that landlords and their insurance companies could no longer recover the costs of damage from tenants. In this case, it was $216,000 worth of damage caused by the careless action of the tenant leaving an unattended pot cooking on the stove.

2) Residential Tenancies Act 2019

This act reversed the effects of the Holla vs Osaki decision and brought back some responsibility for tenants who cause careless damage. Responsibility, however, was limited to the lesser of the landlord’s insurance excess or four weeks rent.

It established that the tenant is fully responsible for intentional damage and that the tenant cannot rely on the landlord insurance policy for this. Remember that; as you would expect, a tenant’s contents insurance won’t provide cover for damage that’s intentionally caused.

To Offer Unique Insurance Product for Holiday Homeowners

New Zealand insurance provider, initio, is excited to announce an alliance with Bachcare, the country’s leading holiday home management company. This unique partnership will provide an innovative insurance product meticulously tailored for holiday homeowners.

Initio, in conjunction with Bachcare, will provide instant online coverage for holiday homes, including those that are also partially rented out. The extensive coverage includes not only holiday homes, but also primary residences, contents, vehicles, and rental properties. With initio’s customer-friendly online platform, obtaining comprehensive insurance coverage for your holiday home is quick and easy.

Initio stands out from competitors due to its forward-thinking approach and unwavering focus on customer satisfaction and simplicity. With initio, you can get a quote in 5 seconds by simply entering the property address. Once insured, customers can also update their insurance cover on the fly with the live policy dashboard.

Smart Claims enhance the experience

To provide an even better customer experience, initio recently upgraded its innovative Smart Claims platform. Having proved its worth in handling claims during severe weather events earlier in the year, this platform brings a new level of efficiency and transparency to the claims process. With features like tailored questionnaires for different types of loss and real-time claims tracking, this technology provides a more streamlined and personalised claims experience. The recent upgrade enhances the comprehensive insurance coverage initio provides, making the process of filing and tracking claims for holiday homes even easier and more convenient.

Specialised Holiday Home cover

Initio developed their specific holiday home insurance product around a decade ago, realising that there were no dedicated holiday home insurance products available from competitors. Rather, competitors simply offered a regular house and contents policy that would often not meet the requirements of the holiday homeowner. Initio understands the unique insurance requirements of holiday homeowners and has meticulously designed their policies to cater to these needs. Whether homeowners use the holiday home for personal enjoyment, or as a rental, initio provides the necessary insurance coverage to protect their investment. With their unique feature of instant online cover in either of these scenarios, holiday home owners can get unparalleled peace of mind.

“We are thrilled to be collaborating with Bachcare, providing an exceptional insurance product that has been designed for holiday homeowners,” said Rene Swindley, CEO at initio. “Our innovative approach and commitment to excellence align perfectly with Bachcare’s mission of providing customers with the best possible experience”.

More about initio & Bachcare

Initio is a pioneering insurance provider based in New Zealand, committed to revolutionising the insurance industry. They offer comprehensive coverage to meet the unique needs of homeowners, covering holiday homes, primary residences, contents, vehicles, and rental properties.

Bachcare is New Zealand’s leading holiday home management company, offering an array of holiday homes throughout the country, focusing on exceptional service and enabling homeowners to maximise returns on their holiday home investment.

Knowing just how far the cover goes is one of the most important things to consider with insurance. Knowing what can and can’t be covered means you can better prepare and plan for the unforeseen.

In general, insurance is there to protect you from the unforeseeable events beyond your control. While you can carefully select your site, carefully plan and build your property, and carefully select tenants, there are other things like storms, disasters, or simply the unexpected that can go wrong.

What follows is a breakdown of need-to-knows when considering insurance and risk in general.

What Insurance Is:

Most insurance policies follow the same form – cover is provided for “sudden and accidental” events causing loss, or something very close.

Sudden in this context means something not gradual. A tree falling on the shed is a sudden impact, while sunlight fading a carpet is a slow gradual process.

Accidental means an unintended result. In using a sledgehammer to break down a wall during renovations, you intended to cause damage to the wall. The neighbor’s car coming through the wall on a Tuesday afternoon? Less expected, and certainly not intended.

A pattern begins to emerge on what is and is not insurable. Insurance is protection against those sudden, unforeseen events which pose a risk to your investment.

What insurance isn’t:

Insurance is not designed to be a maintenance plan. Neither is it designed to remove the responsibility of looking after your property.

All properties suffer some kind of damage over time. Furniture fades, paint gets worn down, and carpets turn lackluster after so many years. These all have to be fixed and maintained, but it is a predictable, gradual process that causes the damage.

Not taking care of the property also means that there will be more damage. For example, not fixing a broken roof means that it is expected and predictable that rain will cause water damage.

What now?

When you understand what insurance does and does not cover, you can better manage your investment.

This is just the summary of how insurance is intended to work, and for more details you can see our cover page and policy wording.

Some important changes will affect what you pay for home and landlord insurance.

The two changes are:

Earthquake Commission cover (EQC)

Insurer premium

We explain these changes below:

Changes to Earthquake Commission cover

From 1 October, all New Zealand homeowners will be affected by the Government’s Earthquake Commission (EQC) changes, which are intended to keep insurance affordable in high seismic regions:

EQC cover increase The natural disaster cover you receive from the government is doubling from a cap of $172,500 to $345,000 per dwelling. Your insurer pays for the repair or rebuild costs when the natural disaster damage exceeds this cap.

EQC levy increase For most homes, the levy is increasing from $345 per year to $552. Some homes will not see the full levy increase due to their lower insured value. Your home insurance spend includes this EQC levy, which we collect on behalf of EQC.

EQC changes affect everyone All insurers have to implement this change. Homeowners throughout New Zealand (regardless of their insurer) will be affected by this change when they start or renew a home insurance policy from October 2022.

This means that the new levy will be applied when your home or landlord insurance policy next renews (either annually or monthly). This is an increase of up to $207 per year or $46 per month.

* all figures referred to in this email include GST

Your insurance spend is made up of both government levies (EQC, Fire & Emergency NZ) and insurer premium. The insurer premium is what we use to pay claims.

We insure thousands of houses in every region of New Zealand. Due to an increase in risk posed by natural disasters and weather events, we have needed to raise the insurer premium.

This means that at your next policy anniversary, after 1 October 2022, your home or landlord insurance cost will change.

Together, as homeowners we buy insurance to get comfort and protection should something go wrong – it’s that simple.

Protection does, however, come at a cost. We’ve spent the last 12 years using our technology to keep premiums down, and we are not letting up.

We are homeowners too and when it comes to insurance, getting responsive cover for the right price is the most important thing. That’s exactly why we exist.

We’ve always been on a mission to provide easy, value for money insurance with exceptional claims service – and that’s what we will continue to do.

The Deloitte Fast 50 recognises high-growth New Zealand businesses that are scaling rapidly through innovation, technology, and strong market demand. A few weeks after the regional results, initio was also ranked 28th nationally across all New Zealand companies in the 2025 Deloitte Fast 50.

Quick summary

Initio named Fastest Growing Services Business (Central North Island, 2025)

Ranked 28th nationally in the Deloitte Fast 50

Recognised for strong growth as a New Zealand-only insurance provider

Growth driven by digital-first insurance and technology innovation

Backed by IAG NZ investment and underwriting support

The Fast 50 celebrates Kiwi businesses that are shaking things up – growing fast, breaking barriers, and doing things differently. So, to be recognised in that crowd means a lot.

What is the Deloitte Fast 50?

The Deloitte Fast 50 is an annual programme that celebrates the fastest growing companies in New Zealand, measured by revenue growth over a three-year period.

It highlights businesses that are:

Scaling quickly

Innovating within their industries

Building sustainable growth models

Contributing to New Zealand’s economic landscape

Being recognised in the Deloitte Fast 50 signals strong demand, operational strength, and market confidence.

Standing out as a New Zealand-only insurance provider

What makes this recognition particularly significant is that initio operates solely within New Zealand.

Unlike many companies in the Fast 50 that have international markets or offshore expansion strategies, initio focuses entirely on Kiwi homes and properties. Growth has been driven by serving the local market with a digital-first insurance experience built specifically for New Zealand conditions.

This shows there is strong demand for:

Simple online insurance

Real-time quoting

Fully digital policy management

Technology-led underwriting

Ranked 28th nationally

Following the regional announcement, Deloitte released the national rankings. initio was placed 28th across all New Zealand businesses in the 2025 Fast 50.

Ranking nationally reinforces that this growth is not just regional momentum, but part of a broader shift toward smarter, technology-driven services.

Growth powered by digital insurance innovation

initio’s growth has not been about speed for its own sake. It has focused on removing friction from insurance.

That includes:

Instant address-based quoting

Automated underwriting

Online policy management through the dashboard

Digital claims processes

AI-powered support tools

The result is insurance that works quickly behind the scenes, so customers do not have to wait on hold, fill in long forms, or deal with paperwork.

Technology backed by people

Strong technology alone does not drive sustainable growth.

The real momentum comes from the team building and improving the platform every day. From software development to claims support, the focus remains on making insurance simpler, clearer, and easier to manage.

Recognition from Deloitte confirms that a technology-led, customer-focused model can scale successfully in New Zealand.

IAG NZ partnership supports future growth

initio’s partnership with IAG NZ strengthens the foundation for continued growth.

With IAG NZ’s underwriting support and investment, initio can:

Expand product offerings

Continue enhancing its digital platform

Introduce new features and tools

Maintain high service standards while scaling

The partnership supports long-term growth while preserving the digital-first experience customers expect.

What this means for customers

Awards are encouraging, but the real outcome is improved service.

Growth enables:

Faster platform improvements

Broader product options

Stronger underwriting support

Continued investment in technology

The focus remains on protecting Kiwi homes and properties with simple, modern insurance.

Thank you to our customers and partners

This recognition reflects the trust of customers, the support of partners, and the dedication of the initio team.

In the second part of our interview with experienced investor Graeme Fowler, we unpack how insurance decisions can impact your bottom line, especially when it comes to excess, premiums, and payment timing.

How do you decide on the right excess?

“I always choose the highest excess available, usually around $2,000. That helps lower my annual premiums quite a bit. But if you’ve only got a couple of properties, a lower excess might make more sense.”

Graeme treats excess like any other business decision: it comes down to scale and risk tolerance. For those with larger portfolios, absorbing the occasional small cost can be a smarter long-term play.

From initio: When quoting with initio, you can select an excess from as low as $400 up to $2,000. The premium updates instantly as you adjust the excess. A higher excess = lower premium, but the right choice depends on how often you expect to claim and what you can comfortably afford to self-fund. Learn more about insurance excess: Demystifying Insurance Excess

What’s your take on how to pay for insurance?

“I always pay annually. Monthly payments might feel easier, but they usually end up costing more. Over a year, you could save quite a bit by paying in one go.”

For Graeme, annual payment isn’t just about cost – it’s also about efficiency. One payment, done and dusted.

From initio: Our quick quoting tool shows the full cost upfront, with a clear breakdown of monthly vs annual payments. Monthly might feel easier, but it comes with a life admin fee – plus, annual is usually better value. And honestly, how much is your time worth? Adjust your excess or add contents and the quote updates instantly. It’s fast, clear, and makes insurance simple.

How do you view insurance as part of your overall investment strategy?

“It’s one of those things that, if you get it right, saves you money quietly in the background. If you get it wrong – or ignore it – you’ll know about it quickly.”

Graeme treats insurance like any other portfolio tool: it should be optimised, not just set and forgotten. Managing excess, timing payments smartly, and locking in renewal rates all contribute to a more efficient portfolio.

From initio: With our digital platform, you can manage all your policies in one place – tweak cover levels, update payment settings, and renew when it suits you. We also send early renewal reminders and show any pricing changes upfront, so you can stay ahead of known levy increases.

Coming up next in the Smart Moves Series:

Common landlord insurance mistakes – and how to avoid them.

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

You’ve purchased insurance from us for exactly this type of situation. Most importantly, make sure you and your family are safe and dry. We are here to get your house, vehicles and belongings back up and running. Here’s some important information and tips on how to best handle things:

Your response

Follow advice: Listen to official information channels and follow the directive of Civil Defence and emergency services

Ensure safety: Make sure you, your family, and pets are safe. If someone is missing, contact emergency services immediately.

Grab essentials: Take your emergency bag and a lockbox containing important and financial documents.

Address health needs: Look after any physical injuries and emotional distress.

Secure your home: If your home is damaged but standing, secure it. This might include temporary repairs.

Document damage: Take photos of any damage for insurance purposes.

Safeguard valuables: If possible, move valuable items to a secure location, like a friend’s house or a storage unit. Your insurance might cover storage costs.

Contact your insurance provider: If your home needs urgent repairs and is still habitable, contact your insurance provider. Remember to document everything and keep all repair receipts. Be cautious of repair scams.

We will prioritise claims with serious damage and uninhabitablehouses. If this is your situation and you require additional support after lodging your claim you can get a hold of us through [email protected] or by phone 0800 763 929

If you have ‘black water’, i.e. rising flood damage, and you want to get on with cleaning up you can lift the carpet and underlay and move it outside.

For damaged contents, start to make a list and take photos. Retain as many items as you can as an Assessor may want to see them.

If emergency temporary repairs are needed to mitigate further loss/damage to the property, engage a tradesperson and send us the costs to add to the claim. For example, securing lose roofing.

Vehicle damage?

If your vehicle has been in deep water (over the tyres) do not attempt to drive the vehicle due to the potential risk of electrical damage and contamination.

Use a permanent marker to mark on the vehicle where you think the water level got to.

Lodge a claim online through your dashboard when you get a chance.

For abandoned vehicles we will arrange for the vehicles to be towed when roads are open and tow trucks have availability. Please let us know during the claim lodgement if the vehicle has been abandoned away from your usual residence.

Where possible and only if it is safe, remove personal belongings from the vehicle.

If you have had to leave your home

If you’ve moved into temporary accommodation, lodge your claim as soon as you can and include the cost of your stay so it can be prioritised as part of your claim.

Owner-occupied homes: Do I have cover for alternative accommodation, a place to stay?

Yes, all initio own-home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you are required to evacuate your residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR if your home is at risk from an insured event such as a flood. Keep receipts and note the dates of your stay — these costs will be included in your claim.

Rental properties: Do my tenants have cover for alternative accommodation?

If you are a landlord and your rental property is unable to be lived in because of the damage you are not responsible for finding your tenant’s alternative accommodation. This is something they are responsible for and their renters insurance would usually cover. However, with initio’s landlord policy, you do have cover for loss of rent if your rental property is uninhabitable.

Lodging a claim

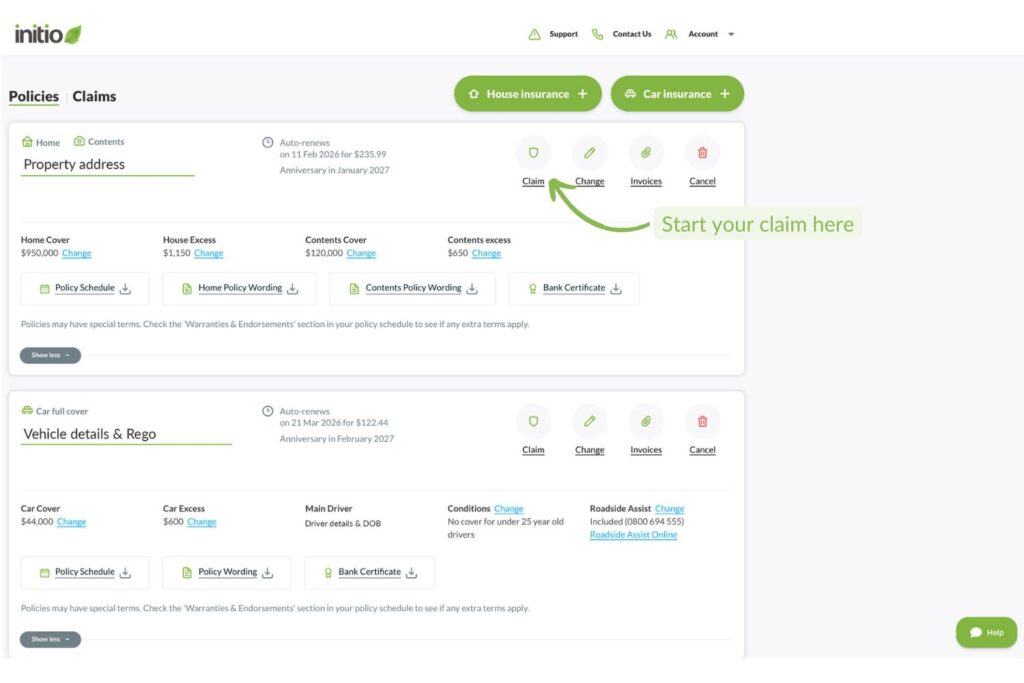

With initio, lodging a claim is easy. Just loginto your customer dash and click on the ‘claim’ icon to the right of your personal information.

Our easy-to-use questionnaire will step you through lodging your claim. We don’t expect you to understand your policy thoroughly, so we explain things along the way. Once your claim is lodged you will get a confirmation email and you can also see the claim’s progress on your dashboard.

To learn more, this guide walks you through how to claim with initio.

Provide as much detail as possible When you make a claim, include clear and detailed information. This helps initio assess how urgent your claim is and what support you need. The smart claims platform can adjust its questions during large events, making it easier to understand your situation and prioritise help where it’s most needed.

Upload photos of the damage Photos are key to understanding the extent of the loss. Upload them when lodging your claim — or later, if needed. Include shots of anything relevant, like flood levels, structural damage, or affected areas. The more visual evidence you provide, the faster and more accurately your claim can be handled.

Timing after a major event Your safety comes first. Once it’s safe and you have internet access, submit your claim as soon as you can. If you’re unable to do this right away, that’s okay — just lodge it promptly when possible. If you need immediate advice, you can always call for help.

Following any natural disaster, we usually receive a significant number of claims. Our team will work on prioritising and acknowledging your claims. Our focus will be to ensure people are safe and that homes are secure following damage.

If you receive a quote from a contractor please send it to us as we take a pragmatic approach to repairs. We prioritise claims for those vulnerable, most in need, emergency accommodation, and serious damage.

Other tips

Never wade through flood water and avoid using vehicles or electrical appliances that might have water damage.

Wear gloves, masks, and protective gear so you don’t come into contact with anything dangerous.

Turn off the power at the mains if flood water has entered the home.

If you are a landlord, check in with your tenants

Learn more about staying safe on the Civil Defence website

NHC (previously EQC) Claims

Claims from a significant event may include areas of damage which NHC covers and also areas which NHC does not cover. All claims need to be lodged with us in the first instance, and then any NHC aspects are referred to NHC internally. This means that you only have to deal with initio (rather than also with NHC), but in the case of significant events, NHC claims can take a while to be processed. NHC claims are assessed in line with the Natural Hazards Insurance Act 2023 (NHI Act), we are bound to the due process that has to be followed.

FAQ’s

Can I start cleaning up?

Yes, but take photos and keep a schedule of damaged contents/items you remove from the house

When will an Assessor come and see me?

We are currently appointing assessors and priority will be given to those with serious damage and to those homes that are accessible.

Do I need to find accommodation for my tenants?

No, you can if you like but this is not your responsibility. Your tenant(s) will have to sort this on their own and they will incur costs to do this, however, if the house is not habitable they will be entitled to stop paying you rent. You can claim this loss of rental income through your landlord policy.

My house needs drying, how do I do that? We use the services of Jaes for drying and extracting water. We will be working with them on the most serious losses, but it could take many days before they can get to you. If you have your own ability to source pumping or drying equipment you can add this to the cost of your claim.

Do I have cover for alternative accommodation, a place to stay? Yes, all initio Own Home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you the homeowner is required to evacuate the residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR because the property is at risk of damage, from an event that would be covered by the policy. Flood damage is automatically covered for initio policyholders. Keep copies of accommodation receipts and record timing/dates and we will include these costs as part of the claim.

Am I covered for damage to my land? The Natural Hazards Commission (previously EQC) provides certain cover for land damage; the NHC provides more than just cover from earthquake damage. Your insurance policy with initio includes NHC cover, and if your land is damaged by storm or flood, you’re eligible to make an NHC claim. To make the claim process simpler, you no longer have to claim through the NHC, we/our underwriter (IAG) will handle your NHC claim on behalf of the NHC. To understand more about how NHC land cover works see this NHC Landcover Guide

Initio recently became a winning 5 star award provider in the 2022 IBNZ (Insurance Business New Zealand) insurance awards and we couldn’t be more proud.

How did we win?

Our winning formula is our smart claims platform, which empowers customer self-service for home, contents, and car insurance. It does this by:

reducing the number of people involved in domestic insurance transactions

providing an extra level of customer control with our online dashboard

every feature, site update, and logic change is made with our customers in mind

never losing sight of how the end user interacts with our technology

creating the easiest and most frictionless insurance experience in New Zealand.

Where others have failed, we’ve been able to provide integration and tools that enable partners to get house insurance quotes instantly. We do this by providing customers with their premium and insurability profile of a property in less than six seconds. What’s more, the technology is scalable. This means our customers have the flexibility to adjust the quote based on their unique needs. Currently, initio generates more than 40,000 automated domestic insurance quotes per day.

How were winners determined?

Technology providers nominated their solution. They explained why it stands out and what makes it the best in the market.

IBNZ then reached out to brokers. Asked them to rate their overall satisfaction with the insurance technology providers they dealt with.

The top-scoring technology and software providers were then named 5-Star Award winners.

We’re incredibly proud to come away with this recognition from the industry. Discover just how impressive our software is for yourself by generating your own instant quote today and starting your own journey with initio. You won’t be disappointed.

At Initio we’ve worked hard to have some of best rates in the market for rental property and holiday home insurance. As well as offering competitive pricing, the cover is tailored to tenanted properties so that you can be sure to have the correct amount of cover.

There have been some who asked how we are able to provide the same cover as other providers but at a lower cost? We’ve put together a number of ways that we’ve been able to keep costs down, and some tips on how you can apply this to save on your own insurance.

Use technology to save time:

By using technology to do a lot of the legwork, admin overheads can be greatly reduced. You can save both time and money by using online services to arrange for bookings and services, including insurance.

Being an online insurance provider, we rely on technology to make it as easy and efficient as possible, and we can provide better savings because of it.

Pay your premiums annually:

Whenever it comes to paying for the insurance, you will have the option of paying monthly, or for the full year in advance. What may not be clear is that monthly payments generally use a loan company in the middle to pay for the full annual total, and then collect back the loan with interest.