Search results for: {search_term_string}/page/get-quote

House & Contents

Home & Paying Guests

Renting out part of your home short-term?

Such as a bedroom or a self-contained unit/area?

If you have a part of your property that you sometimes rent out short-term whilst you are not using it yourself, renting out part of your home means you need the right insurance to protect your entire property, rental income, and liability to any guests.

What counts as short-term renting, for insurance?

Short-term renting is lets of up to 90 days per guest stay. This could be via platforms like Airbnb or other short-term rental arrangements. When the space isn’t being rented, you or your friends and family use it. If a guest books in for a stay longer than 90 days, it is classed as long term and the property should then be insured under our Landlord Insurance product.

Does this match your situation?

- The area (unit/bedroom) is used for short-term lets between your own use.

- This could be an occasional Airbnb, but;

- You must use the area yourself (or friends and family do) between paying guests

What insurance do you need?

For this setup, you’ll only need one insurance policy that covers your home and the short-term rental use. This is called an own home, partially rented policy, and it provides cover for both your personal use and rental activities.

Own Home, Partially Rented insurance

What does this policy cover?

Having the right policy means you’re covered for:

- Your home – Protection for your home including the area sometimes let.

- Short-term rental risks – Cover for things like accidental damage caused by guests, loss of rents and your liability to guests

- Loss of rent – If a guest cancels or you’re unable to rent the space due to an insured event, you’ll be covered for lost income.

Get covered today

With initio, you can get a quick quote and buy insurance online in minutes, making it easy to ensure your property is fully protected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

Own Home, Partially Rented insurance

Why is this policy important?

Standard home insurance might not cover short-term renting, leaving you exposed to potential financial risks. A policy designed for partial rental use ensures you’re protected, whether you’re welcoming guests or enjoying the space yourself.

Need help? If you’re unsure about what policies are right for your situation, contact us to make sure you’re fully protected.

Get covered today with initio – Quick quotes, easy online cover.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

Landlord Insurance

Landlord insurance built for landlords. We make it easy with all-in-one rental property and landlord insurance.

Initio provides an all-in-one landlord insurance policy for the rental property itself and the extra risks you take on as a landlord, such as a tenant deliberately damaging your property. The only real value you see from your landlord insurance policy is at claim time, and that’s why we make it easy.

Have a rental property with multiple units? Check out our multi-unit rental cover.

[initio_review_rating_total property_type=”rental” get_quote_button=”Get online quote” get_quote_button_classes=”cta-button cta-button–orange”]

Here are some of the great features of the Initio landlord insurance policy:

| Description of Cover | Limit of Cover | Excess |

|---|---|---|

| Full replacement Dwelling Cover up to Sum Insured | Your Sum Insured | Your Choice of $400 / $650 / $1,150 / $2,000 |

| Major Malicious Damage by Tenant (Fire & Explosion) | Your Sum Insured | Greater of $500 or Your Chosen Excess |

| Deliberate Damage by Tenant | $25,000 | Greater of $500 or Your Chosen Excess |

| Methamphetamine Contamination – manufacture | Your Sum Insured | Your Chosen Excess |

| Methamphetamine Contamination – consumption | $30,000 | $2,500 |

| Loss of Rents Cover (following property damage) | $20,000 – $80,000 | Nil |

| Landlords Contents | $20,000 – $40,000 | Your Chosen Excess |

| Hidden Gradual Damage Cover | $3,000 | Your Chosen Excess |

| Landlords Legal Liability Cover | $2,000,000 | Your Chosen Excess |

| Full Earthquake Cover | Your Sum Insured | $5,000 |

IMPORTANT This is a summary of the landlord insurance policy only. Please refer to the policy wording for full details of cover

Here are some of the many landlord insurance claims we’ve paid:

- A tenants dog was left locked in the property. The doors, walls and carpets didn’t win the dog fight, but Initio came to the rescue.

- Leaking tap connection in the bathroom wrecked the vanity and particle board floor. The tenant worked this out when his foot went through it. Gradual damage claim.

- Fire in the laundry caused by an overloaded electrical multiplug. Fire service attended. Repair costs and loss of rents covered while the property couldn’t be tenanted.

- Meth lab in attached garage. Police raided causing more damage. Initio picked up the tab.

- House foundations severely damaged by Canterbury Earthquake. EQC and Initio put things back in order.

And, here are some of the landlord losses we don’t pay:

- Tenant decides not to pay the rent. We consider this a payment risk best managed by you or your professional property manager.

- Shower tray leaks over time and the tenant doesn’t let anyone know that the floor is squishy. Gradual damage has to be from a water pipe.

- Wooden window sill rots and needs to be replaced. Wear and tear is not covered. This is a maintenance cost not an insurable risk.

- Tenants move out and leave the house untidy, including a large amount of rubbish to be disposed off. Unfortunately there is no damage so no cover, the Initio policy is designed to cover damage.

- Upon the property becoming vacant the odd mark is found on the carpet, and a few marks on the walls where the tenant has hung pictures. Unless you can point to a sudden event that caused damage we consider this to be wear and tear, and the policy does not provide cover.

This is not an exhaustive list and the list does not imply that all losses the types described are covered or not covered. Landlord insurance claims are like butterflies, each very unique with its own set of facts that we need to apply to the policy.

Initio provides landlord insurance to NZ’s top property investors. Buy landlord insurance online with Initio. Quick quote, quick claims, initio

[initio_quote_calculator title=”Instant free quote & buy online” pre_selected_cover=”rental”]

[initio_review_list property_type=”rental”]

Holiday Homes; rented to short-term guests

Hosting short-term guests introduces unique risks. Most insurance companies are cautious about rented holiday homes so before letting out your home or listing your property on platforms like Airbnb or Bachcare, it’s important that you confirm your policy covers holiday bookings.

Effects on insurance costs

If you host paying guests, and you tell your insurer, they will likely adjust your coverage. Be sure to inform your insurer about your hosting activities and understand the implications for your policy. Many insurers, including initio, may increase premiums or excesses due to the additional guest-related risk. Some insurers may exclude coverage for guests entirely, leaving you at risk of being uninsured. It’s best to review your policy or contact your insurer if you’re unsure. Make sure your insurer is aware that you rent out your holiday home.

What qualifies as a holiday home, for insurance purposes?

To qualify as a holiday home, the owner must;

- Use the property themselves as a holiday home, and;

- Have the right to occupy the property at will, and;

- Store personal belongings at the home.

A holiday home can be used by:

- The owner, at any time.

- Friends and family.

- Tenants on a periodic basis, including short-term paying guests (stays with durations of less than 90 days).

These criteria ensure the property remains under your control and qualifies as a holiday home with your insurance provider and meets the requirements for cover provided by the Natural Hazards Commission (NHC, previously EQC).

How property management can affect your insurance

Using a property management company under a full management contract can impact your insurance. If the property manager has full control, you may lose the right to occupy the property, which can disqualify it from being considered a holiday home, and makes it ineligible for Natural Hazards Commission (NHC) coverage. You must check your agreement with your property management provider as it may mean that you have assigned control cover to the manager and you no longer have the ability to occupy it when you wish.

An insurer cannot provide domestic house insurance cover for a holiday home that does not meet the conditions of cover for the NHC.

Understanding NHC cover: The Natural Hazards Commission (NHC) provides special insurance protection for the home against natural disasters like earthquakes and floods, and unlike your house insurance policy, it also extends to cover land damage. To qualify, your property must meet specific criteria, including being under your control as a holiday home. For detailed information, refer to the NHC guidelines.

What if your property does not qualify as a holiday home under the NHC legislation?

If your home does not meet the NHC definition of a holiday home, to obtain cover you will likely need a commercial property insurance provider to structure insurance that covers the building, loss of income and liability risk.

Does landlord insurance cover short-term rentals like Airbnb?

No, our landlord insurance is designed for standard long-term residential tenancies only. It doesn’t cover properties used for short-term rental activity such as Airbnb or Bookabach.

If you rent out your own home (where you live) occasionally on Airbnb, you may be eligible for cover under our Own Home, Sometimes Rented policy. Similarly, if you have a family bach or holiday home that you occasionally let to paying guests, it may be suitable for our Holiday Home insurance – sometimes rented – just make sure to select the option for short-stay rentals when quoting.

Short-term rental properties that operate like a business typically require commercial insurance, which isn’t available through initio. Learn more about the things we don’t cover at initio.

Doesn’t Airbnb’s ‘Host Guarantee’ cover me?

If you manage your property using Airbnb, you’re likely familiar with their Host Guarantee.

It’s important to understand that this guarantee isn’t a substitute for proper insurance. The Host Guarantee comes with limitations and might not cover everything you anticipate. It’s not equivalent to regular insurance and some hosts have discovered it doesn’t provide comparable protection. To ensure your property is fully covered against any damages or issues, having your own insurance policy is essential.

Airbnb’s Host Guarantee is not a traditional insurance policy but a conditional promise. It’s not regulated like insurance. Key requirements include:

- Report damage and file a claim within 14 days.

- Provide proof of ownership and, in some cases, a certified police report.

House Guarantee conditions can include:

- Only covers damage during the booking period.

- Coverage is limited to listed areas in your profile.

- Exclusions include damage from excessive utility use, animals, or pets.

- Rent loss cover only applies to confirmed bookings cancelled due to damage.

Given these limitations, Airbnb themselves recommends having a specialist insurance policy in addition to the Host Guarantee.

Everything’s in order, how do I get the right cover?

If you manage your holiday home yourself and meet the necessary NHC criteria, initio offers specialised cover for your holiday home that is also used for short-term rentals. As the first in New Zealand to provide a house insurance policy specifically designed for holiday homes, Initio offers a hybrid house, contents, and guest insurance policy tailored for short-term rentals, without the strict conditions of a Host Guarantee.

Initio’s holiday home (with the additional short stay option) policy covers:

- The home itself for damage from things like flood, fire and storm (whether rented or not)

- Accidental damage to the home by guests.

- Intentional damage by guests, up to $25,000 (e.g., if guests decide to damage walls deliberately) .

- Loss of rent for confirmed bookings cancelled due to the home becoming uninhabitable following insured damage, and also for loss of rent from unconfirmed bookings based on seasonal, area or your previous year’s use data)

- Meth contamination from manufacturing, ie. contamination damage caused by an accidental incident in connection with the manufacture, distribution or storage (but only where the storage is in connection with supply or distribution) of methamphetamine at the home.

- Your legal liability to your guests for accidental damage and bodily injury.

These are the sort of protections you need when renting your home out to short-term guests.

Key takeaways

- Check your insurance: Ensure your policy covers holiday rentals before using platforms like Airbnb.

- Higher costs: Be prepared for higher premiums or excesses if your insurance covers guests.

- Host guarantee limits: Airbnb’s Host Guarantee has strict rules and limited coverage.

- Property Management impact: A property manager’s control might disqualify your home from holiday home insurance, check your agreement with the property manager and that you still comply with the NHC definition of a holiday home.

- Holiday Home rules: You must retain occupancy rights and keep belongings there to maintain holiday home status.

- Get the right insurance: Choose insurance designed for short-term rentals for better protection.

- Comprehensive coverage: Seek policies that cover guest damage, lost rent, meth contamination, and liability.

By managing your property with these factors in mind, you can better protect your holiday home and maintain your insurance coverage.

Holiday Home Insurance

Holiday Home vs Own Home

Related articles

Renting out two dwellings on your property long-term

If you own a property with two dwellings and rent them both out long-term (90 days or more per tenant), it’s important to have the right insurance to protect your investment. Whether the dwellings are separate or physically connected will determine the type of insurance you need.

What type of rental arrangement is this?

- Two homes, same site

- Both rented on long-term residential leases

What insurance do you need?

The right insurance depends on whether the dwellings are physically connected or separate:

If the dwellings are NOT physically connected (e.g., separate buildings on the same section):

- You’ll need two landlord insurance policies, one for each self-contained dwelling. Each policy will cover the specific rental risks of that property, including tenant-related damage, liability, and loss of rent.

Start by buying one landlord insurance policy, then add a second through your dashboard (instructions below)

If the dwellings ARE physically connected (e.g., one upstairs and one downstairs, or connected by a wall, roof, or garage):

- You can use our Multi-Unit Rental policy, which provides coverage for both units under a single policy. you’ll need to state the number of self-contained dwellings at the address. This helps ensure you get the right level of cover for your property setup.

How to add a policy for a second dwelling on the same title:

-

Login to your dashboard and click on the ‘house insurance +’ button

-

Search for your home address & ‘see full quote’

-

On the full quote screen, click ‘back’ to edit the second dwelling’s details if needed.

-

If both properties are the same size or the details are already correct, no changes needed.

-

-

Once you go back, edit the property details, then click ‘continue’

- This will adjust the quote to reflect the correct figures for the property.

Finish the quoting process from here per the usual process – Easy!

You can get a quick quote and buy insurance online in just a few minutes with initio. Make sure you choose the right policy based on whether your dwellings are separate or connected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

What if my quote isn’t straightforward?

Most of the time, getting a quote with initio is fast and simple. But every now and then, something pops up that needs a closer look – whether it’s a map that doesn’t match your house, a question about flood zones, or a message saying your quote needs review. This guide covers the common situations that can make things a bit less straightforward, and what to do next if that happens.

Can’t find your address in the quote tool?

If your address doesn’t come up with the details you have entered, please use the blue option below the address box that then comes up showing as “I can’t find my address”. Clicking on that option will let you enter both the house number and street manually.

If your property is a new build in a particularly new street, potentially our database may not be able to locate the street, if so, please give our team a call to obtain a quote.

Your website says my home is in an RMS flood zone. I called the council and they said I’m not?

It’s quite common for there to be differences between the flood risk assessments provided by initio (using RMS data) and those from your local council. RMS (Risk Management Solutions) uses advanced modelling techniques, recent data, and a national standardised approach, while councils may focus on specific local concerns and use different methodologies or older data. This means that RMS might identify risks not yet reflected in council maps, or vice versa. If you have concerns about these discrepancies, we encourage you to get in touch with our team for further clarification. You can reach the initio team through our contact page — it’s the best way to connect with the right person quickly.

I don’t need flood cover, I live on a hill

Initio’s home insurance policies automatically include flood cover as part of the standard protection, and it cannot be removed or excluded, even if you live on a hill or believe your property is not at risk. This is because the policy is designed to provide comprehensive cover for all insured events, including those that may be unexpected.

Can you do risk-based pricing for my property specifically?

Initio uses risk-based pricing for its property insurance policies, which means your premium is calculated based on specific factors related to your property, such as location, construction type, and exposure to risks like flood or earthquake. However, the risk assessment is determined by initio’s underwriting and data models, and individual requests for manual risk adjustments or exclusions are not available. If you believe there is a significant error in how your property’s risk has been assessed, you can contact the initio team to discuss your situation further.

Why does the water supply matter?

The water supply matters because it affects the risk of significant damage in the event of a fire. Properties that are closer to a fire station and have better access to water are less likely to suffer extensive fire damage, which can result in lower insurance premiums. For example, a house next to a fire station will generally have a lower premium than one that is far from town and relies solely on rainwater tanks. This is one of several factors used by initio to calculate your house insurance premium. Learn more about how premiums are calculated

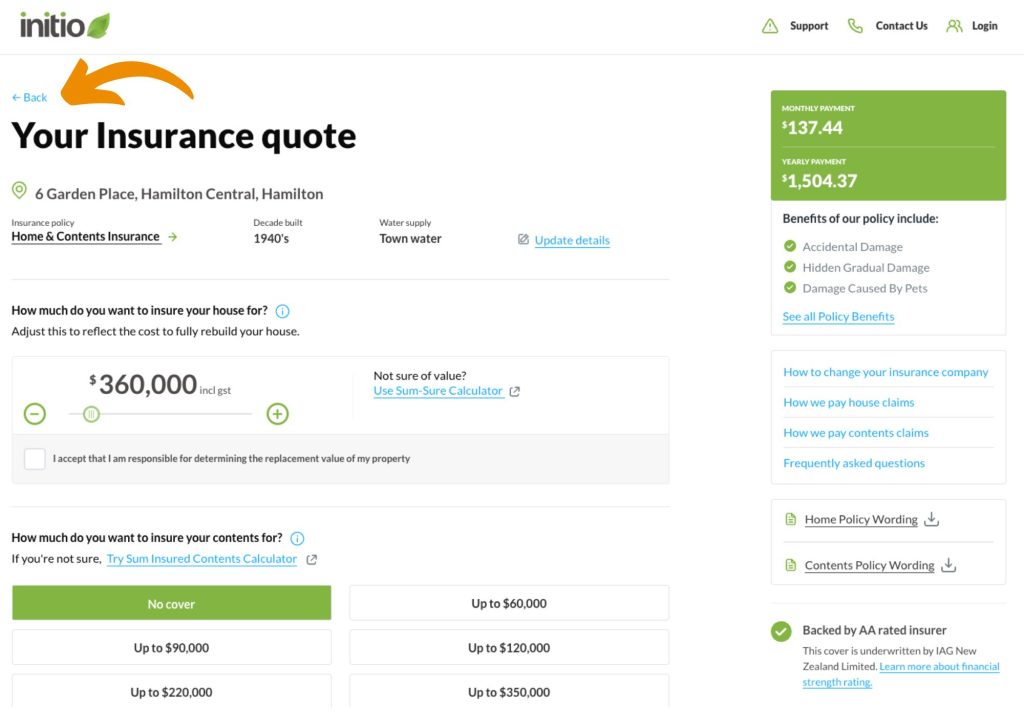

The map image above the quote is not my house

The map image shown above your quote on the initio website is generated automatically based on the address information you provide, and sometimes it may not display the exact property, especially for new builds or properties in recently developed areas. This image is for reference only and does not affect your insurance cover or the details of your policy. If you have concerns about your address or need to ensure your property is correctly identified, please get in touch with the initio team through our contact page

Your website gave me a quote. Now it says you need to review it before you can provide cover. What do I do now?

If your quote shows that a review is required, it means our team needs to check some details about your property or situation before we can offer terms. This can happen for a few reasons, such as unique property features, location, or other risk factors.

To proceed:

-

From your quote, select either the annual or monthly option

-

Complete the online application form and submit it

Once submitted, a member of the initio team will review your application and contact you directly. There’s no obligation to purchase once the review is complete.

If you’d like to follow up or have any questions while you wait, get in touch with the Initio team through our contact page .

If you’re insuring more than one property with initio, please wait until the first application has been reviewed and the policy purchased before submitting the next. Once that’s done, you’ll be able to submit your next property directly from your new initio account, which keeps your portfolio together in one place.

Start a new quote or check your address

If you’re unsure about the details in your original quote, or just want to double-check your address and start fresh, it’s easy to get a new quote online. Our quote tool is quick, and you’ll be guided through the process in just a few steps.

Related articles

- How to buy your first policy

- How to navigate your initio dashboard

- How to claim with initio

- How to get a quote with initio

- Insuring old homes

Hey there partner!

Car Insurance

Two dwellings on the same title

Autumn Home Expo

How do I buy my first policy?

Wondering how to get your first policy with initio started? This guide outlines the entire process from getting a quote to paying for your policy.

It takes you through the basic steps of quoting, customising and changing your cover, disclosing other information and making payment.

Once you have purchased your first policy with initio, you get access to a personal dashboard where you can modify and manage all your policies online.

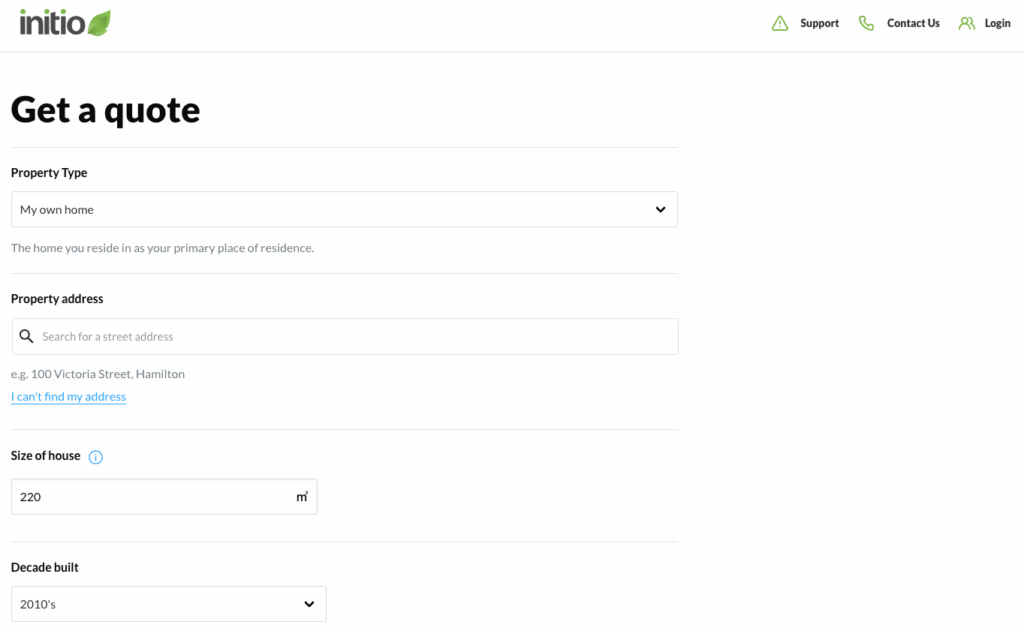

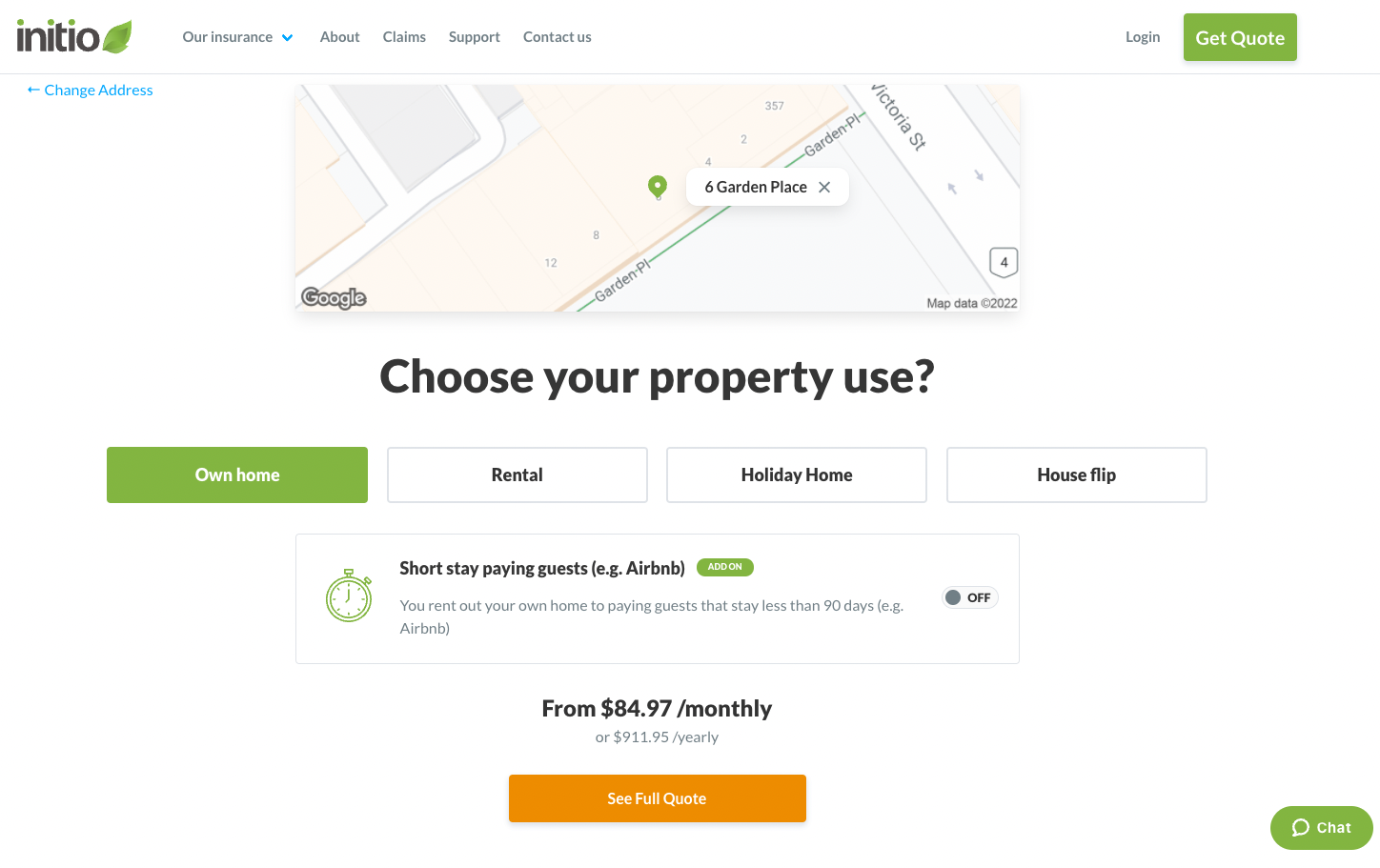

Get an instant quote – enter property address

If your address doesn’t come up with the details you have entered, please use the blue option below the address box that then comes up showing as “I can’t find my address”. Clicking on that option will let you enter both the house number and street manually.

If your home is a new build in a particularly new street, potentially our database may not be able to locate the street, if so, please give our team a call to obtain a quote.

Select property use

If you’re uncertain about the type of property insurance that best suits your needs, visit our ‘Choosing Your Insurance‘ support page. There, you’ll find detailed information and guidance to help you make an informed decision tailored to your unique circumstances.

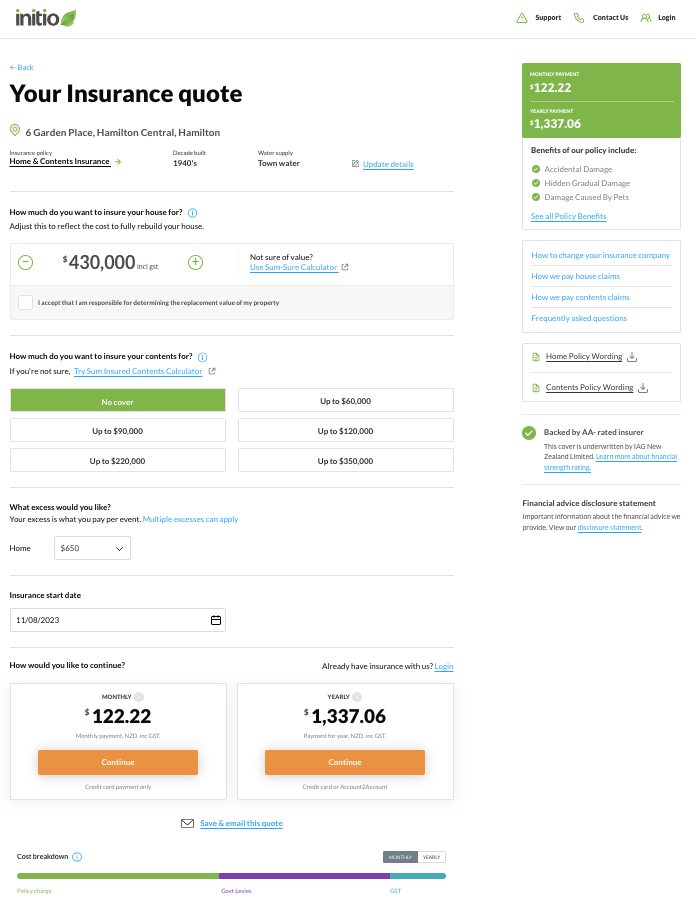

Customise quote

From here you can edit the details of the quote and customise as required. This can also be done from a home quote you have previously emailed yourself using the “restore” button.

Uncertain about the proper amount to insure your property for? We’ve designed a support page that walks you through the essential factors you need to consider regarding the sum insured.

Choosing the right amount of insurance for rebuilding your home is important. This amount should be what it costs to build your home again, not what your home is worth on the market. Don’t forget to include things like fences and swimming pools, and remember that building costs might go up over time. For example, if two neighbors with the same houses insure for too little or too much, they could lose money if their houses are destroyed. The right amount saves worry and money. Tools like the Cordel Sum Sure Calculator can help you figure out how much it might cost to rebuild your house.

If you’re wondering about how much excess you should have on your insurance policy, this support page covers some of the basics. Many property owners choose to cover minor losses themselves, avoiding insurance claims for low-value damages. If this applies to you, consider raising your excess to $1,000 or $2,000 to save on premiums. Think about what you’re comfortable claiming for and your financial risk tolerance when selecting house insurance. Under initio’s landlord insurance, tenants only cover the excess on careless damage, so assess your comfort level with potential out-of-pocket expenses, and set your excess to match your ability to absorb those costs.

Insurance Start Date? Enter the date that you would like the cover to start from should you proceed with purchasing. If it’s a new home, that should represent the sale’s settlement date. If you’re changing from another insurer, use your existing expiry date. Please note that we are only able to provide confirmed quotes for policies with effective dates of up to 30 days in advance. If the effective date you need is more than 30 days ahead, please wait till you are closer to that time to quote/apply.

Once you are happy with your customised quote, you can either;

- Email yourself a copy to save a copy of the quote

- Proceed to purchase the policy by selecting either the “annual” or “monthly” payment option at the bottom of the quote. Then follow the steps below.

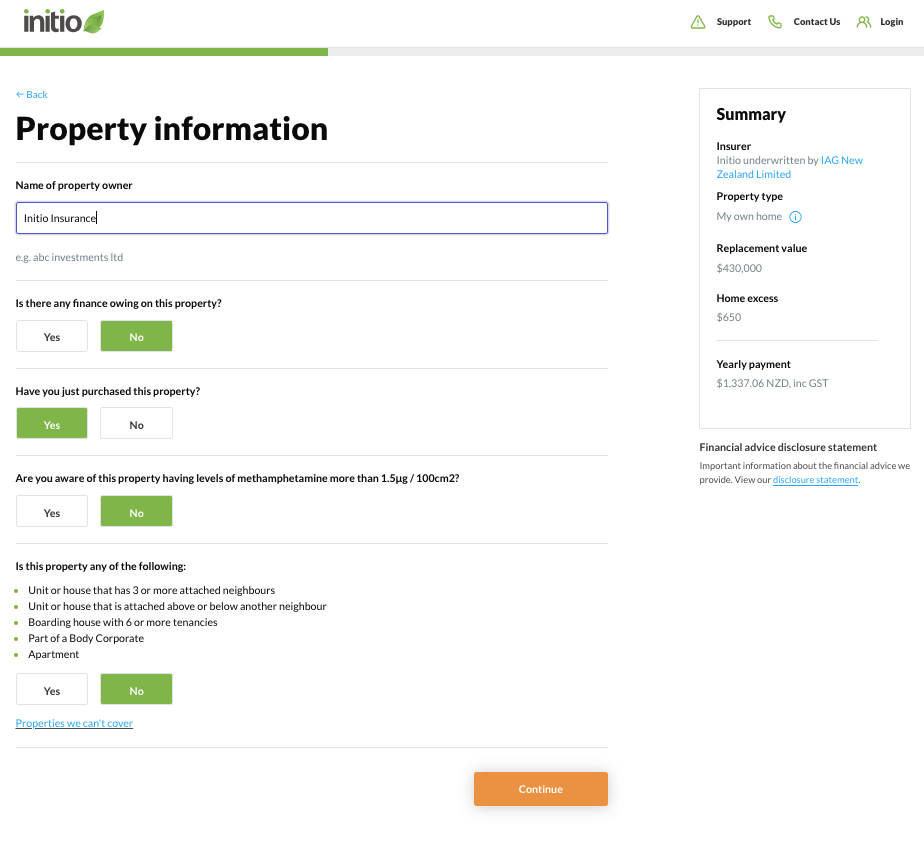

Enter property details

A note about selecting start date of cover; ensure its the same date as the expiry/renewal date of your current policy to ensure cover continuity (or the settlement date if purchasing a new house)

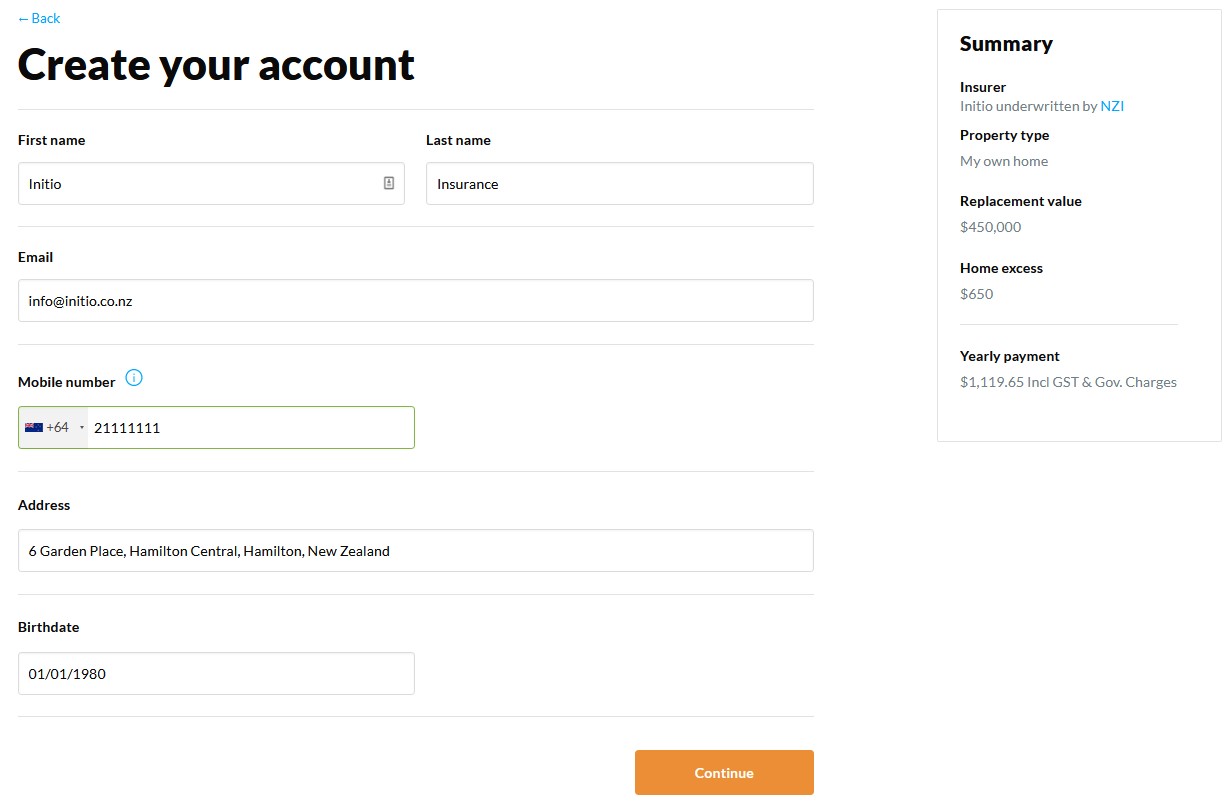

Confirm your details

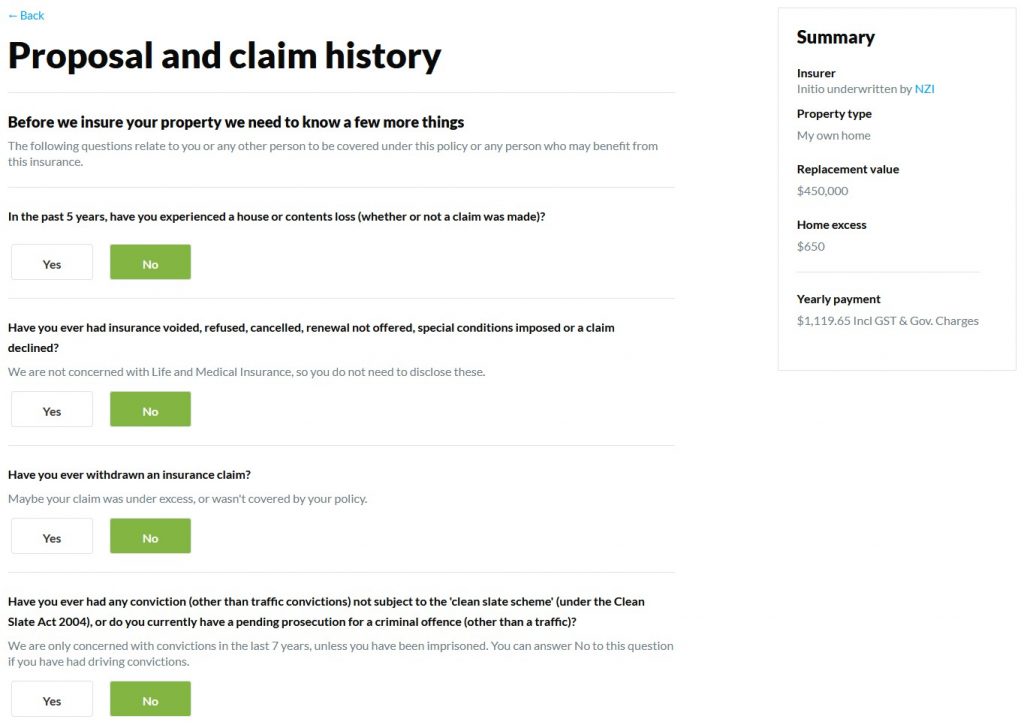

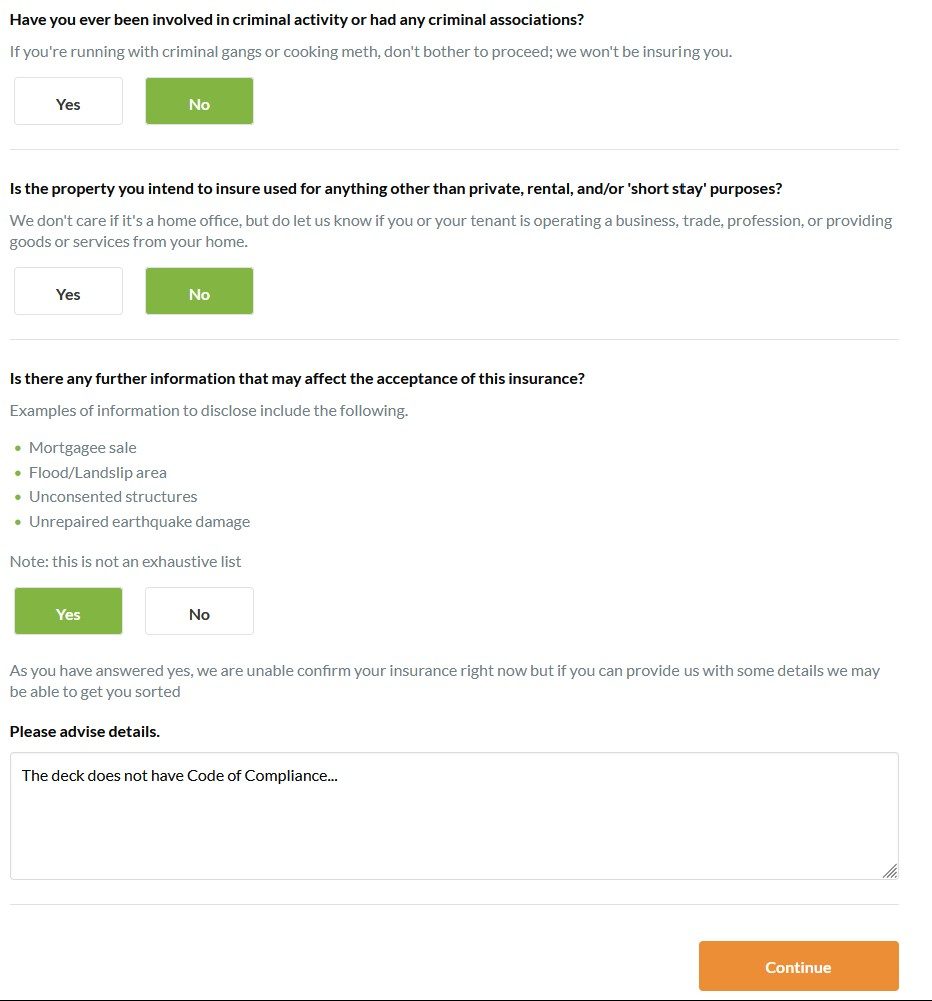

Complete online proposal form

Unsure if something may affect your cover? Disclose it

How to sign your application form

Use the device keyboard to type your name in full (as the person completing the form) in the space provided.

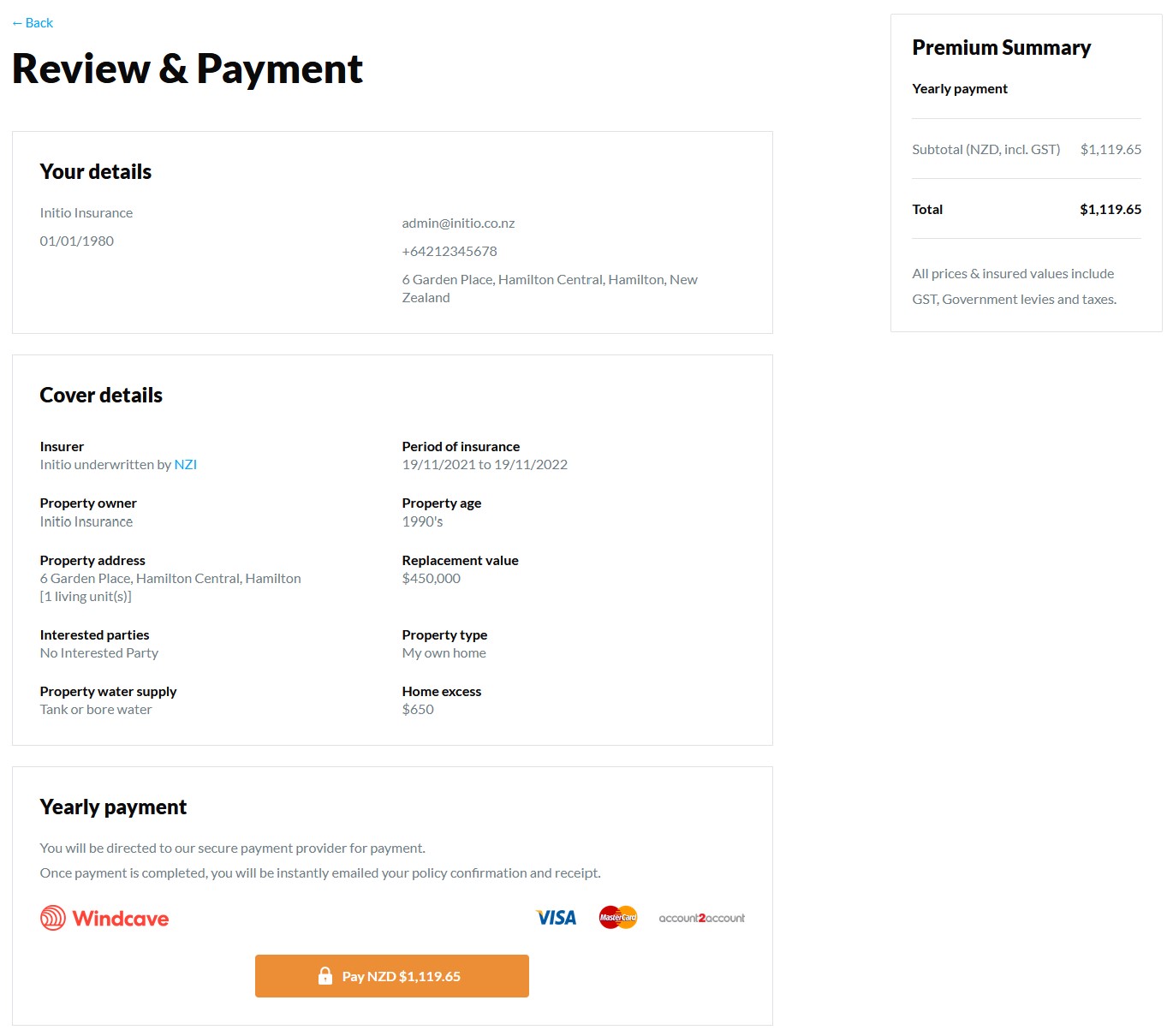

Review and make payment OR Application requires a review?

If the payment option isn’t offered it’s because a human will need to review the application for you. Please continue to submit the application for review and we will aim to come back to you within one business day to let you know the status of the request.

Otherwise, if the payment option is available, you can either

- proceed to purchase the policy OR

- if you’re not ready to commit or haven’t yet bought the property, you can choose to download a “letter of intent” on this page. The letter of intent simply outlines that based on the information provided we are able to insure the property when you’re ready.

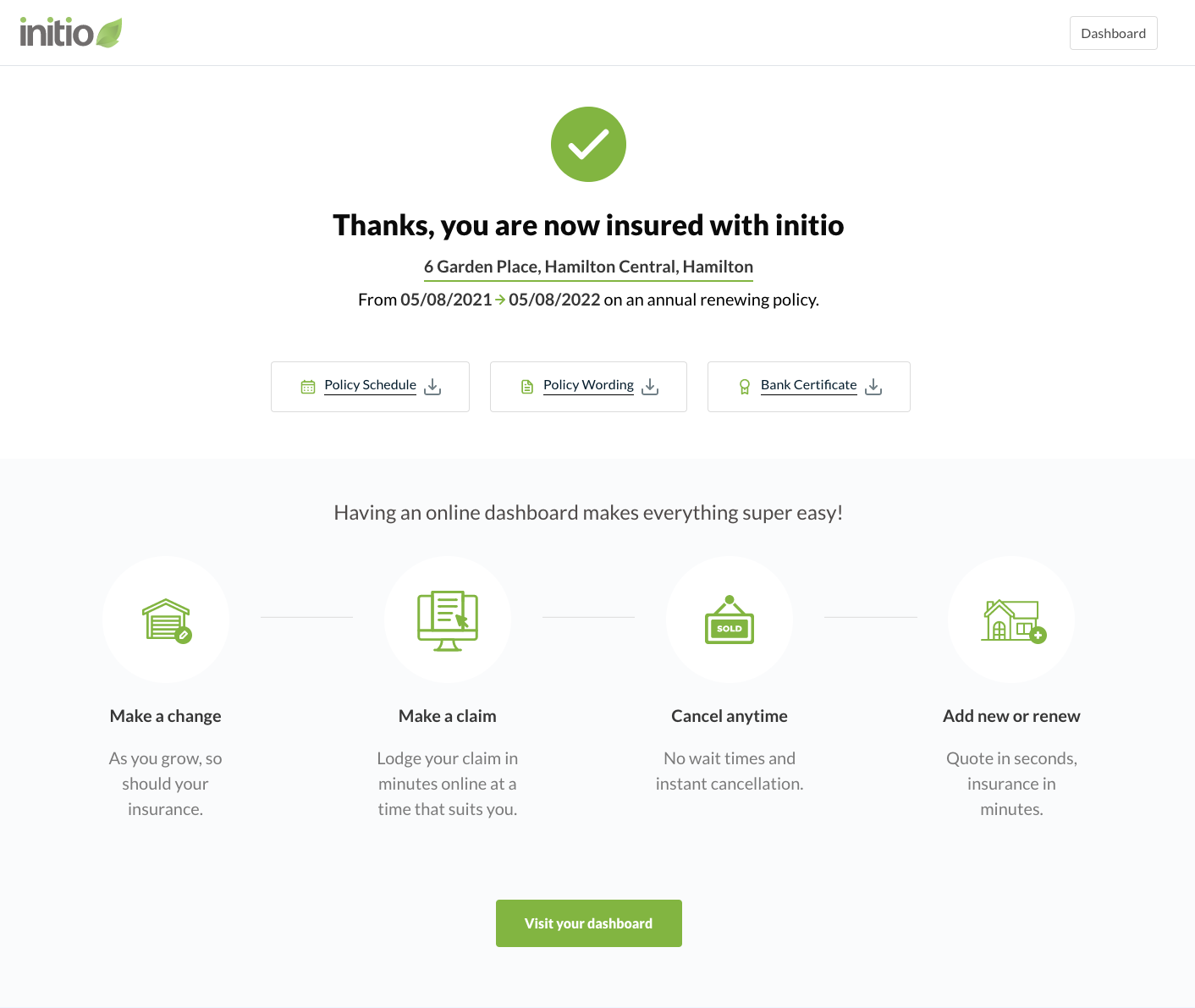

ALL DONE! We will instantly email you confirmation documents

Want to add another property? Click “Add insurance”

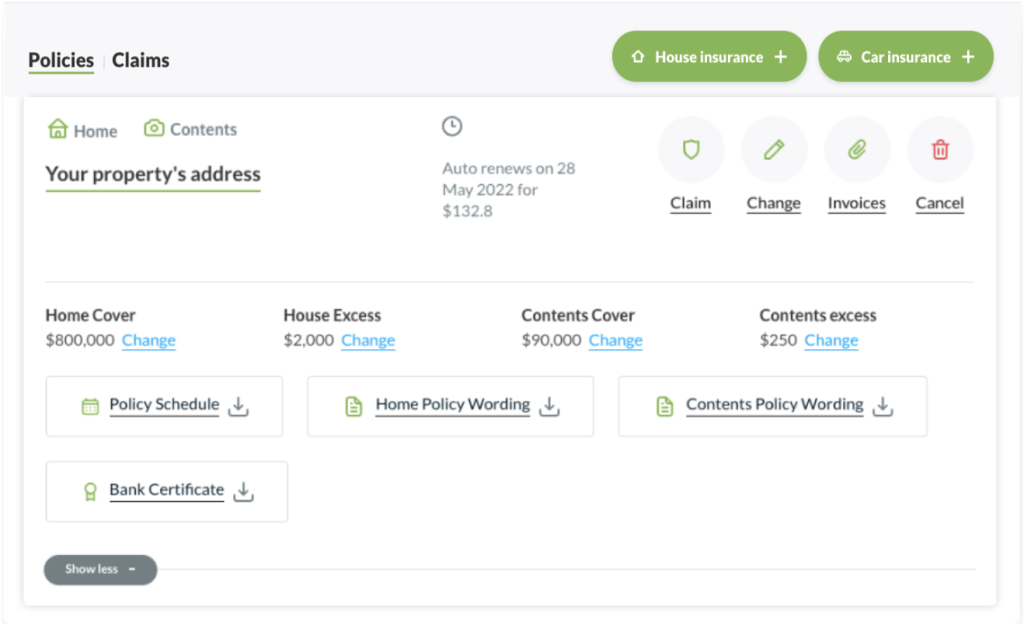

Need to make a change to your policy?

Refer to our guide here. Our website is informative and the go to for accessing your account. No need for an app, our site is available in a user friendly format on all your devices.

Looking for more information? Our top five mistakes to avoid when insuring property article might help.

If you would like to see how initio compares to other popular New Zealand insurance companies, start here.

Adding or changing your policy

Looking to buy a Motor Vehicle Policy?

Our vehicle insurance is exclusive to our home policy holders. Once you become a home policy holder with initio you can easily add car insurance from your initio dashboard using the “vehicle insurance +” option.

Ready to begin your journey with initio?

Useful articles

Your Owner Occupied Home, that’s also rented Occasionally for Short Periods

Short term tenants and insurance

If you plan on renting out a room or your house to short term tenants, there are some things you need to consider. One of the most important is how it will affect your insurance cover.

Non-Disclosure

Failing to tell your insurance company about the change in occupancy could result in non-disclosure; which in turn could result in non-payment of a claim. Make sure you let your insurer know if you intend to rent a room or home to short term tenants or guests. A house, rental or landlord insurance policy designed for long term tenants is unlikely to cover you.

Getting the right cover

Just because you’ve got insurance, and you have disclosed the occupancy, it doesn’t mean that you are covered. You will need to specifically ask your insurer about policy coverage whilst short term tenants / guests are staying in your home. Some of the key questions to ask are:

- Any cover for damage/theft by short term holiday rental guests?

- Is there a cover for lost rental income following a damage to the property?

- Will there be cover if guests contaminate the home with methamphetamine?

Simply continuing to insure the home isn’t always enough. You want to make sure that you have the right insurance cover for the increased risk exposure. If your existing insurer cannot provide this cover check out initio.co.nz who specialises in rental and holiday home insurance.

If your home or unit is used solely for short term tenants it is unlikely to meet the EQC (Earthquake Commission) definition of a home. This is because it is viewed as more like a motel, and will require a commercial insurance policy.

Don’t rely on Airbnb Host Guarantee

The Host Guarantee is not an insurance policy, and should not be relied on as such. The extensive terms and conditions including time limitations can make receiving a payment from Airbnb difficult. There are no guarantees of payment with this guarantee. The security deposit paid by guests is also controlled by Airbnb so unless Airbnb and the guest agree, you cannot retain any security deposits to cover your damage.

How to stay safe

If you do decide to list your home (or room) online with sites such as Airbnb or Bookabach there are some simple ways to stay safe.

- Screen guests by checking online reviews and looking at online profiles such as Facebook and LinkedIn. Don’t be afraid to ask for references, and remember you can decline a booking if you are not comfortable.

- Don’t go off the platform, and complete the transaction offline, this will void any ‘guarantees’ offered by Airbnb. Always be wary of guests wanting to pay with prezzy cards or cash.

- Question guests intentions if they are wanting to stay for extended periods at short notice; especially if it is off season and your home is in a remote location.

- Always refund cancellations to the credit card used to make the payment to avoid assisting money launderers.

- Don’t leave valuable or sentimental items lying around for guests to use or damage.

- Consider installing a meth alarm.

- Keep your keys safe by not always leaving them in the same place.

- Build relationships with your neighbours so they can keep an eye on the home and report any suspicious behaviour.

How do I quote and insure a house, not already with initio?

Scenario:

- An existing client of yours is up for renewal on their House & Contents, Landlord or Holiday Home and needs cover.

- An existing client of yours has purchased a new/additional house and needs cover.

- A new customer has approached you for House & Contents, Landlord or Holiday Home insurance.

Getting your client online is easy with initio

- Use your initio landing page to quote your customer’s house

- Choose the relevant property type (own home, rental, holiday home)

- See instant quote on screen. From the quote screen email yourself the quote

- Select the expected start date of insurance.

- Set the sum insured to the amount discussed with your client, their current sum insured, or leave it as the default sum insured.

- Click ‘Save & email this quote’.

- Enter your client’s name and then your email address.

- Separately email your client the price (and high-level details of the cover) and include the ‘restore quote’ link you received in the email from initio. (copy the link/url)

- If your client would like to proceed with the cover they can click the restore quote link, which will give them the ability to dynamically things like excess, sum insured, contents etc., In this email, you may also like to compare us with other insurance companies.

Please note:

- Initio does not onboard these customers. For compliance reasons, the customer must complete the signup online themselves in order to answer the proposal questions.

- Prices can change so please select the correct expected start date.

- If the property is pre 1935, or in a certain risk zone this may trigger a referral to the initio team. They will need to review the cover, and potentially obtain further info before deciding on whether or not to offer cover.

- Alternatively, simply send your broker landing page link to the customer.

- If your client already has a property insured with initio, then simply refer to login to their own initio dash, click the ‘House Insurance +’ button, and enter the property address.

- Monthly payment is limited to credit cards or Visa/MC debit cards. Annual is a credit card or account2account (real-time bank transfer).

Helpful link:

What does the customer do once they have the restore quote link?

- Click the ‘restore quote’ link or they can re-quote from your broker landing page

- Review and make changes to the quote, eg adjust the sum insured, excess

- Confirm the start date of the cover

- Select the preferred payment option monthly or yearly

- Answer property information questions (e.g insured name, interested party)

- Fill in account details (e.g customer name, contact details)

- Answer proposal and claim history questions (e.g previous claims, convictions)

- Policy may refer at this point, initio will handle and advise.

- Make the payment online for instant cover

Please note:

- Monthly payment is limited to credit cards or Visa/MC debit cards. Annual is a credit card or account2account (real-time bank transfer).

Helpful link:

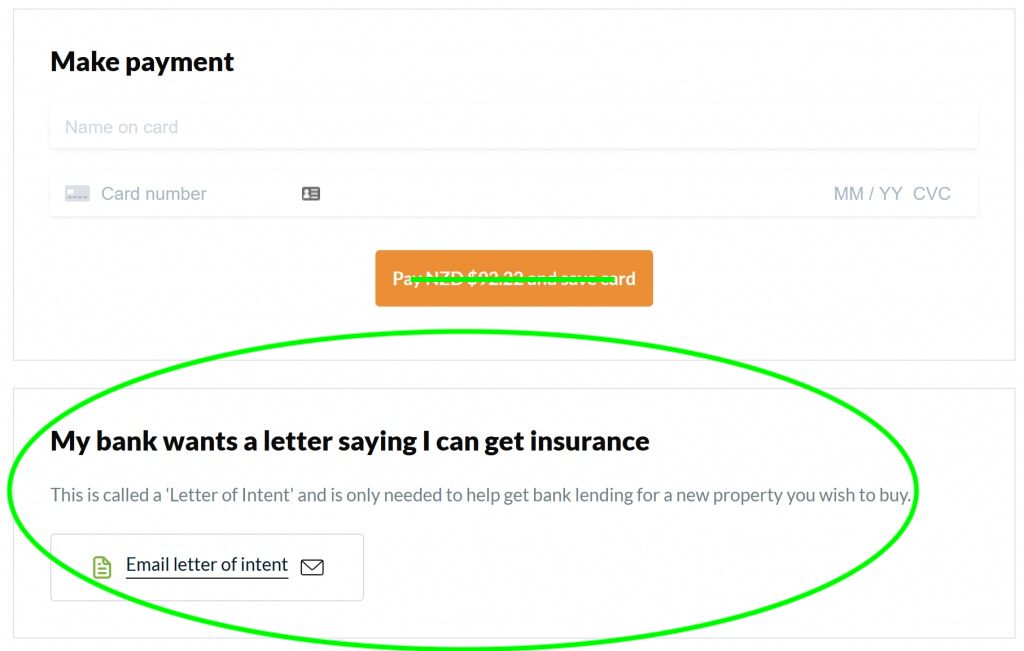

Need to confirm you can obtain insurance on a property before making an offer? Get ‘pre-approval’ for insurance!

It’s common for your mortgage provider or bank to want confirmation that you can secure insurance on any house you are looking to purchase (before they approve your loan).

This is known as a ‘Letter of Intent’. In simple words, it’s a document that confirms an insurer is able to provide cover on a house. This is usually what you would require if you are yet to purchase the home, but instead you want to make an offer or head to auction. This is different to a “Certificate of Insurance” which you would provide upon purchase of the home and, therefore, the insurance policy.

In summary, in looking to make sure you can get cover on a home, you would obtain a “Letter of Intent” prior to any purchase and a “Certificate of Insurance” upon purchase of the property.

With initio, obtaining a letter of intent is fast and straightforward. After completing a few straightforward steps, you can email a copy to yourself as soon as you’ve filled out the form.

Where can you request a Letter of Intent?

Begin by requesting a quote and completing our online application.

1. Get a quote

Visit our 30 second quote calculator here. You’ll need to enter an effective date, don’t be too concerned with this date (for a letter of intent) as it’s likely you won’t have a confirmed settlement date. At this point, it’s for quoting purposes only, choose a date as close as possible to a potential settlement date.

2. Complete an application

If you’re happy with the quote, you can continue by scrolling to the bottom and selecting a preferred payment interval (either monthly, or annually). But don’t worry, you won’t have to make a payment if you are only looking for a “letter of intent”.

You’ll then need to fill out our three online application pages. These include information about the property, your details, and completing the disclosure and claims history page.

Fill in these pages as if you will be the successful bidder/purchaser. This means putting your name as the property owner, etc.

3. Submit a referral, or request a Letter of Intent

If we need to review your application, the next option will submit your info for a review. In some cases, a review will require us coming back to you wanting some more information or detail, we aim to do so within one business day.

If no review is needed, you’ll go through to a summary page where there is an option below the make payment section to send a ‘Letter of Intent’ to your email. No payment is required to download the ‘Letter of Intent’ option which will give you a pre-approval document for your peace of mind and any finance. Select this option and enter your email address.

A confirmation document will be automatically sent to your email, and that’s it! You can then easily forward this to your bank or mortgage provider to finalise the process. Note that the Letter of Intent is not a Certificate of Insurance so won’t show a start date or confirm cover is in place. What it will show is that you are able to obtain cover with initio, should your purchase be successful.

If you need a Letter of Intent, start by getting a quote:

Other articles of interest

Initio’s House Insurance Calculator

Making sure your property has an accurate Sum Insured, or replacement value, is the single most important thing when insuring a house. Insurance is designed to protect homeowners from financial ruin, so its crucial that such a major asset, like a house, is insured for what it would actually cost to rebuild it.

So let’s start from the beginning:

What is replacement value?

The replacement value of a house is the amount it would cost to

What does ‘sum insured’ mean?

The sum insured of a house is the maximum amount that will be paid out during a ‘total loss’ event, such as the house burning to the ground or destroyed in an earthquake.

So it’s logical that the sum insured is the same as the replacement value, but depending on how the homeowner calculates the replacement value the two can be vastly different.

What costs should be calculated?

- Labour

- Demolition and removal of debris

- Building materials

- Interiors

- Foundations

- Compliance costs

- Gates, fences, walls, swimming / spa pools, tennis courts

- Other permanent structures on the property

How do I calculate these costs?

Use the free Cordell Sum Sure Calculator

Cordell Sum Sure Calculator tool

Note – every house is different, the Cordell Sum Sure calculator is just an estimate.

Or else you may want to engage a qualified Quantity Surveyor or Valuer to get a professional estimate.

How often should I check my sum insured value?

We recommend you check your Sum Insured value each year, to make sure you are adequately covered based on current market building and labour costs and inflation.

Helpful resources for calculating your house insurance

Understanding the Sum Insured insurance approach

Learn more about rebuild costs

- http://need2know.org.nz/what-you-need-to-do/estimate-your-rebuilding-cost/

- https://sorted.org.nz/guides/protecting-wealth/insuring-our-homes/

Need to increase your Sum Insured?

If you’re insured with initio it couldn’t be easier.

You can make changes to your policy online by logging in to your initio dashboard and selecting the “Make a Change” button from the right-hand side action menu. Click on the “Cover” button, and you will now be able to update the sum insured. You will be able to see the effect on the premium, and make the payment if additional premium is due. Once your alteration has been completed your policy will be updated immediately and a current schedule of insurance will be emailed to you.

When you take out a house insurance policy in New Zealand, you are typically asked to provide a replacement sum insured for the property. This is the amount you choose will be required to completely rebuild the home and its improvements (eg driveways, fences etc ) in the event of a total loss.

However, many properties end up being insured for much less than the cost it would actually cost to rebuild them (known as under-insurance). If a major loss was to occur the sum insured chosen by the customer is not adequate to fully replace the home and the customer is left with a shortfall.

A 2016 Treasury report stated that up to 85% of dwellings in New Zealand could be underinsured by an average of 28%. Underinsurance of homes across the country was estimated to be worth $84 billion.

Previously, it was the norm for house insurance policies in New Zealand to have no sum insured, and were simply insured for replacement of the dwelling to its pre-damage size. However, following the Christchurch Earthquakes, insurers in New Zealand were left with inflated house repair costs and many changed to “sum insured” replacement policies – where the insured and insurer agree on a maximum amount to be covered. This allowed insurers to have more of a handle on their total house insurance exposure, eg so many billions of dollars of houses insured.

So, why do people get the rebuild cost of their home wrong?

There are various reasons as to why people end up underinsured (and on occasion over-insured). The main reason is that people are not experts on building costs so its very difficult to get it right.

Another significant reason for widespread under-insurance is that costs included in the replacement sum insured are often not considered. The replacement sum insured includes all the direct costs of rebuilding a home, as well as compliance costs, professional and other fees and demolition/removal costs. When such costs are ignored by insured parties, it contributes to the underinsured shortfall for fully replacing the home.

Other than a lack of knowledge on costs, some people may purposely choose to under insure their home to save premium. This is approach is very dangerous and not recommended as in the event of a major loss it may leave the home owner without adequate funds to rebuild. The premium saved only likely to only be a modest sum. If the premium is a motivator the homeowner is best to select a high excess (eg $2,000 or even $5,000) – this results in a decent premium reduction but means the little things are not covered and the big things are. Insurance is about worst-case scenario so making sure the big things (fire, flood, storm etc) are insured is key.

How do I calculate the rebuild cost (sum insured) of my home?

Knowing how to calculate and what to insure your property for can be hard. Thankfully, there are various tools that can help you with your responsibility of selecting your sum insured.

We strongly recommend taking the time to utilise resources on accurately estimating your sum insured value. Getting a quantity surveyor, calculator is an excellent option that uses council and government records on New Zealand properties to estimate the cost to rebuild your home. You can easily get an estimate by visiting the following site:

www.cordell.clickhere

The initio property insurance quote calculator will default to $2,000 per square meter replacement value. This is simply a base estimate for the rebuild cost and is not a sum insured calculator. Your sum insured can be easily be amended by adjusting the value on the initio quote screen.

Calculating the right Sum Insured – Under-Insurance in New Zealand

When you take out a house insurance policy with initio – or most insurers in New Zealand – you are asked to provide a replacement sum insured for your home. This is the figure you calculate for what you think it would cost to rebuild your house if it suffered a total loss and represents the maximum sum the insurer will pay out. Because of this estimate many houses in New Zealand end up being under insured, where the sum insured chosen by the home owner is not enough to fully replace their house and they are left with a shortfall that is often in the tens of thousands of dollars come claim time for a major loss.

While New Zealand has some of the best rates of home insurance in the world, Kiwis don’t seem to value their houses highly enough. A 2016 Government Treasury report reported that up to 85% of dwellings in New Zealand could be under-insured by an average of up to 28%. The shortfall between sums insured and the actual cost to replace housing across the country was estimated to be worth a staggering $84 billion of under insurance.

Sum Insured vs. Replacement Policy:

In the past it was the norm for house insurance policies in New Zealand to have no sum insured, and homes were simply insured for replacement of the dwelling up to its pre-damage size – with no maximum cap on the payout. This was very effective in removing the risks of homes not having adequate insurance. However, following the major Christchurch Earthquakes of 2010 and 2011, insurers in New Zealand were left struggling with unexpected and inflated house repair costs as it was difficult to estimate their total potential payouts with uncapped replacement policies. Following the troubles arising from the Christchurch earthquakes, the majority of insurers in New Zealand changed to “sum insured” replacement policies – where the insured and insurer agree on a maximum amount to be covered.

Why Are People Under Insuring?

There are various reasons as to why people end up with under-insured homes. Often, people are un-educated on building costs and do not take enough time to consider the potential costs. A common mentality for home owners is that they might think; “The chances of my house having a total loss is very small” and so they don’t fully consider or review their house’s sum insured when purchasing or renewing a policy.

Another large reason for widespread under-insurance is that particular costs included in the replacement sum insured are often not considered by people, or simply not known to them. The replacement sum insured includes all the direct costs of rebuilding a home, as well as compliance costs, professional, other fees and demolition/removal costs. Homeowners oftentimes will only regard the direct rebuild costs and exclude these additional elements. When such costs are ignored by insured parties, it contributes to the under-insured shortfall for fully replacing the home.

Other than a lack of building cost knowledge and cost exclusions, some people may purposely choose to under insure their home to save on their insurance premium. At initio, we do not recommend doing this as you can be left widely uninsured to the tune of thousands of dollars in the event of a major loss, while the premium saved is likely to only be a modest reduction. Selecting a higher excess is the most cost effective way of reducing your premium whilst still remaining adequately insured in the event of a major loss.

Making Sure You Are Not Under-Insured

Knowing what to insure your property for can be hard. Thankfully, there are various tools that can help you with your responsibility of selecting your sum insured.

We strongly recommend taking the time to utilise resources on accurately estimating your sum insured value.The Cordell Sum Sure calculator is an excellent option that uses council and government records on New Zealand properties to estimate the cost to rebuild your home. You can easily get an estimate by visiting the following site:

www.cordell.clickhere

The initio property insurance quote calculator will default to $2,000 per square meter replacement value. This is simply a base estimate for the rebuild cost and is not a sum insured calculator. Your sum insured can be easily be amended by adjusting the value on the initio quote screen.

Get insurance

Holiday Home Insurance

Owning a Holiday Home means you’re a little different. That’s why you need an insurance policy that provides good cover when you’re not there or when someone else is using it.

At Initio we understand that your holiday home could be advertised online, and that on occasion you may have paying guests staying. Or perhaps your holiday home is only used by your friends and family. When you insure with Initio we give you the choice, so you get the right cover for the right price.

Holiday homes are often left vacant for extended periods, we know this and we make sure that the cover continues regardless of when the property was last occupied. We also know that your holiday home is furnished and that some of your personal items may remain at the property, and this is why we provide you with a range of contents insurance options.

[initio_review_rating_total property_type=”holiday-home” get_quote_button=”Get Quote” get_quote_button_classes=”cta-button cta-button–orange”]

Here are some of the great features of the cover:

| Description of Cover | Limit of Cover | Excess |

|---|---|---|

| Full replacement Holiday Home Cover up to Sum Insured | Your Sum Insured | Your Choice of $400 / $650 / $1,150 / $2,000 |

| Major Malicious Damage by Guest (Fire & Explosion) | Your Sum Insured | Greater of $500 or Your Chosen Excess |

| Deliberate Damage by Guest | $25,000 | Greater of $500 or Your Chosen Excess |

| Loss of Rents Cover (following property damage) | $20,000 – $80,000 | Nil |

| Owners / Landlords Contents Options for present day & replacement value cover |

$20,000 – $220,000 | Your Chosen Excess |

| Hidden Gradual Damage Cover | $3,000 | Your Chosen Excess |

| Owners Legal Liability Cover | $2,000,000 | Your Chosen Excess |

| Unoccupancy exceeding 60 days | Your sum insured | $5,000 or $2,000 with intruder alarm** |

| Full Earthquake Cover | Your sum insured | $5,000 |

** Where your property is a Holiday Home or Bach your chosen excess will apply if the property is kept in a tidy condition, all external doors and windows are securely locked, all papers and mail are collected regularly, and the home is under regular supervision.

IMPORTANT This is a summary of the policy only. Please refer to the policy wording for full details of cover.

Initio allows you to buy insurance online and enjoy some of the best policy coverage and claims service available for Holiday Home owners.

[initio_quote_calculator title=”Instant free Holiday Home quote & buy online”]

[initio_review_list property_type=”holiday-home”]

Do you have a second dwelling on your property that your family lives in?

If you have two dwellings/units on your property and the second one is permanently occupied by a family member or friend who lives separately to you, it’s important to have the right insurance in place to cover both homes properly.

What counts as permanent family use?

If your second dwelling—such as a granny flat, unit, or cottage—is lived in independently by a family member or a friend, then it’s considered a separate household. Even though they are part of your extended family or close circle, the fact that they live there permanently and independently means the second home/unit needs to be insured separately as another home/unit.

What insurance do you need?

For this setup, you’ll need two separate home (Own Home) insurance policies, one for each dwelling. This ensures that:

- Each home/unit is covered.

Begin by getting a home insurance policy for your first property and then proceed to obtain another quote for the second home/unit.

If you rely on rent from your family member for the second home/unit, we would recommend considering the Landlord policy for the second home/unit.

Own Home, Partially Rented insurance

To ensure both dwellings are protected with the right level of insurance you’ll need to set up one policy first, then start a new quote for the other. The good news? Getting covered online only takes a few minutes, so setting up two policies is quick and easy. If you already have house insurance with us and need to add a second policy, login to your dashboard and click on the + add house policy to begin the process. While getting a quote and buying insurance online with us might be easy, our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

How to add a policy for a second dwelling on the same title:

-

Login to your dashboard and click on the ‘house insurance +’ button

-

Search for your home address & ‘see full quote’

-

On the full quote screen, click ‘back’ to edit the second dwelling’s details if needed.

.

-

If both properties are the same size or the details are already correct, no changes are needed.

-

-

Once you go back, edit the property details, then click ‘continue’

-

- This will adjust the quote to reflect the correct figures for the property.

Finish the quoting process from here per the usual process – Easy!

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

The pitfalls of Airbnb Insurance

There’s a lot of talk about the ‘pitfalls‘ of renting your home out on airbnb or bookabach. Local councils are cracking down on short-term rental property owners, with the result being that your profitability suffers. Like any business, increases in costs can be managed and in many cases have to be passed on. There are also anecdotal claims that the risks associated with rental your home to guests short term are uninsurable. Some risks, and expenses, can be managed by choosing the right insurer and the right insurance policy.

What’s the problem with insurance?

Most insurers will tell you that your domestic house and contents policy isn’t suitable for home sharing situations. Or that inviting strangers into your home for money could invalidate your insurance. Others might tell you that you are insured, but come claim time, you’ll discover there was no cover. For example your standard home contents policy, won’t cover you for items stolen by individuals allowed in the home. And your standard home policy, won’t cover you for intentional damage caused by guests. That means that you’re not covered if anyone who has a key (or their guest) steals, or damages your stuff – including your home.

A landlord insurance policy will usually provide cover for the above, but generally these come with a bunch of landlord obligations. Landlord obligations include things like reference checks, credit checks and written inspections between tenancies. Without upholding your obligations; which are generally impossible for holiday rentals, the insurer could deny your claim.

What’s the solution?

To circumnavigate these issues, most short term holiday accommodation providers recommend a commercial insurance policy. But these can cost thousands of dollars, and are not always necessary. What you probably don’t realise is that there is an insurance policy designed specifically for holiday homes that are rented out. The initio insurance policy for landlord and holiday home owners.

In addition to providing cover for your holiday home and its contents, the policy extends to cover intentional damage and theft by paying guests. Unlike other insurers, when the home is occupied by guests as a holiday home, the landlord obligations do not apply. Loss of rents is also covered, with the policy allowing for the lost income to be calculated using a combination of factors. These include confirmed future bookings, and rent received in the 12 months preceding the loss or contamination damage. As for meth contamination, it is covered in connection with the manufacture or distribution of methamphetamine at the home.

In the past, there has been confusion on whether your holiday rental will be covered for Earthquakes and Natural Disaster. To clarify, provided that it is your intention to live in, or holiday, at the home, then you will be covered under the EQC Act (of which you pay an EQC levy as part of your insurance). If the home is purely a commercial enterprise that is not used personally by you or your family, you will need a commercial insurance policy (which will cost a lot more).

What about liability?

Health and safety legislation applies to short-term rental properties in the same way that it applies to other landlords. You have a duty to make sure your property is safe and healthy. This includes installing smoke alarms and providing protective gear for any equipment that might be used by guests, such as lifejackets for kayaks. It also means that you, as a landlord, could be deemed liable for an injury or accident suffered by a guest suffers at the property.

Some home sharing services will provide property owners with a limited amount of liability cover. However if you are renting your property you should make sure you have adequate public liability insurance in place. The initio policy provides $2 million of cover including bodily injury and defence costs.

What about the provided insurance / guarantee?

The Airbnb Host Guarantee is not an insurance policy. If you do a quick search in google, you will soon see that claiming is not very easy or straightforward.

Bookabach Owner Protection provides an actual backup insurance policy, which is locally supported. The policy covers owner’s liability and property damage protection and is underwritten by NZI (IAG New Zealand Ltd). However, for cover to apply, the guest booking must be booked and paid online through Bookabach. A current house insurance policy also needs to be in place for the Bookabach backup policy to apply.

It’s always best to have a proper holiday home insurance policy in place in the first instance. Find out more about the initio insurance policy for landlords and holiday home owners, including an instant quote,

Technology you can trust

Instant, reliable quotes you can count on

They say AI might take over the world someday, but for now, we’ve put it to work making your life easier – one insurance quote at a time. At initio, we’ve spent countless hours perfecting our technology so you can get a home insurance quote faster than you can say, “robot overlords.”

Simply type in your address, and our advanced system gets to work, drawing on resources like flood mapping tools, council records, and the latest data to deliver a reliable, competitive quote instantly. We can quote most New Zealand properties on the spot, there’s just the occasional scenario where the property might get referred. For more information, you might like to check out our support articles: insuring old houses and five tips to insuring in a flood zone.

Other insurance providers might claim they can give you a fast quote, but none are as quick or accurate as initio. After extensive research, we’re confident no other provider matches the speed and precision of our platform, but that’s just our opinion, feel free to try it for yourself.

No tricks or gimmicks

With initio, what you see is what you get. When you use our platform, the price displayed is the price you’ll pay – no surprises. Whether you’re insuring a house, rental property, or holiday home, our quotes are consistent and accurate.

While some providers might adjust their pricing based on how you contact them or bundle other policies, initio does things differently. We focus on transparency and simplicity so you can trust that the quote you’re receiving is fair and final.

How does our technology work?

Our system leverages multiple reliable data sources to assess your property’s risks and deliver a personalised quote within seconds. From flood zones to natural hazards, our advanced platform ensures you’re getting a quote that reflects the latest information.

Even if your property requires a referral for further review, we’ll ensure it’s assessed promptly. This guarantees your policy is built on a thorough, expert evaluation—giving you the confidence to move forward with certainty.

Why initio doesn’t offer multi-policy discounts

We’re often asked if bundling insurance can save you money. The answer is simple: initio doesn’t do multi-policy discounts because we offer you the best price for every policy right from the start. We provide a fair and straightforward process where every quote is designed to be competitive and accurate.

A fast, modern insurance experience

Initio isn’t just about speed; it’s about trust. Our platform ensures you can quote, compare and get cover in minutes – backed by a system designed to simplify your experience. No upselling, no misleading information – just an honest, reliable service powered by the best technology in the industry.

If you have questions, our team is here to help. But when it comes to finding a better deal, you won’t need to look anywhere else. With initio, you’re already getting the fastest, most accurate quote possible.

Hear from the team behind the tech

Take a look under the hood to see the tech that drives our insurance and how it’s evolved into what it is today.

Other articles of interest

- Awards we’ve won

- How do I buy my first policy?

- Essential guide to house insurance

- Understanding landlord insurance

- Explore our video library

- How to switch from your current insurance provider to initio

Try it for yourself

Do you rent out a second dwelling solely for short-term stays?

If you have two dwellings on your property and one is used exclusively for short-term stays – such as an Airbnb or similar short-term rental arrangement – it’s important to understand your insurance options.

What insurance do you need?

Homes used this way are no longer classified as residential, as they are considered to function more like motels. Because of this you will require a commercial product to insure the home/unit.

What are your options?

Unfortunately, initio does not currently offer an insurance product that fits this type of use. Please contact a provider who offers commercial solutions, such as a broker.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

- Renting out part of your home short-term

- Do you have a second dwelling on your property that you rent out?

- Insurance for a non-rented second home on your property

- Second dwelling on your property that your family lives in

- Renting out two dwellings on your property

Get started with initio

How do I get a quote with initio?

Getting a house insurance quote with initio is quick and simple. Just pop your property address into our quick quote tool and we’ll do the heavy lifting for you. You’ll see your premium instantly and can customise your cover to suit your needs.

When you’re ready, choose either annual or monthly payments and follow the prompts to buy online – no paperwork, no waiting.

For more details, check out our step-by-step guide to buying your first house insurance policy.

What information do I need to get a house insurance quote?

Most of the time, all you need is your property address, and our quick quote tool will pull in the important details. You might just need to answer a few simple questions, including:

- Approximate house size (no exact measurements needed)

- Estimated rebuild cost (your “sum insured”)

- Age of the home

- The date you want cover to start

Not sure about your rebuild cost? Our quote tool links to the Cordell SumSure Calculator, which helps you estimate it. You can also read our guide to choosing your sum insured for more details.

How fast can you really get a quote?

This short demo puts our quote tool through its paces to show how fast and easy it is to use.

How do I log in?

If you already have a policy with initio, you’ll have access to your dashboard to manage your insurance. Login details are emailed to you when you buy your policy. Login here

To log in:

- Enter the email address you used when purchasing your policy.

- Enter your password.

- If you’ve forgotten your password, click Forgot my password and follow the steps.

If you’re not sure which email you used, contact our team, we can help.

Logins are only provided once you’ve purchased a home policy with initio.

Related articles

Is my house covered if I also rent to guests?

Here’s what you need to know to insure your main home if it’s also rented to short-term guests.

What can be covered? A shared primary residence

If the house is your primary residence, we can cover your own home that’s also rented with our Own Home Rented product. However, it’s required that you share the use of the property with guests.

The two most common scenarios for renting your own home are:

- You rent out part of your home to short stay guests while you still live in the property (e.g. a room or downstairs).

- You rent out you whole house to short stay guests when you’re not living there (e.g. you go overseas or stay in your holiday home).

If your house is not your primary residence, it may be able to be insured as a Holiday Home also Rented. Learn more about insuring holiday home rentals here.

Essentially, our guest rental cover only applies to properties that have shared use (at-least occasionally) by the owner. We’ll explain why next.

What can’t be covered? A dedicated short-stay accommodation

We can’t insure a dedicated short-stay living unit that’s only used for guest accommodation. When a unit is used solely for guests it becomes a commercial property – similar to a motel.

The EQC’s $150,000 of natural disaster cover will not apply to a ‘dedicated short stay’ as they are considered commercial risks. Our domestic house insurance policy assumes part of the natural disaster risk is covered by the EQC. A dedicated short stay rental therefore needs to be covered under a commercial material damage policy, where the insurer covers 100% of the natural disaster risk.

Please note the definition of a dedicated short stay property is any living unit that is set up purely as a commercial enterprise and the owners don’t use it or intend to use it for their own purposes (or for somebody else to use it as their home).

Is a secondary unit at my house covered under my house insurance policy?

Yes, as long as it’s not a dedicated short stay unit – and it’s used by yourself (at least occasionally) as part of your own home.

It’s common for people to have an additional self contained living units at their houses. It’s common to have a separate unit at the back of the house, or a downstairs living unit with its own access. Often these are rented to short term guests (via Airbnb or BookaBach), or longer term boarders for additional income.

If you don’t use this unit yourself (at least occasionally) then we can’t insure it together with the main house.

If the unit is used purely for short terms guests a commercial policy is required. If the unit is simply rented to tenants you’ll need a separate landlord insurance policy for it.

Short Stay Airbnb Unit Example

If the additional unit is used by both the owner and short-term guests we can provide cover under our own home rented.

If the additional unit’s use is shared by the owner (themselves or family) as well as short-stay guests, it can be covered under our Own Home Rented product.

When the living unit is solely rented to guests and not utilised by the owner, it is deemed a dedicated short stay. EQC cover does not apply, and we can’t provide cover.

An example of this is where the unit is used for children when they return home from university and other times the unit is rented to short stay guests. This can be insured under a Own Home Rented policy on the main house.

Renters or Boarders Unit Example

If the rental unit (for example downstairs unit) is only used for a longer term tenants (i.e. more than 90 days) or boarders and not utilised by the owner themselves – this can’t be insured under a single Own Home Rented policy. In this instance, a separate Landlord Insurance policy is required to cover the self-contained rental unit.

If you need help working out which insurance or combination of insurance is best for you, see our home & income insurance page.

What is Covered?

Our Own Home Rented product takes all of the standard owner occupied policy features, and includes extra cover for the risks of renting. You can also choose to add personal household contents cover. You can get the peace of mind that your property and contents itself is covered, while the risks associated with renting your house to guests is insured.

Generally a standard house insurance policy won’t cover guest risks, so it’s important for owners to get the right cover. The extras included in the own home rented cover includes:

- Accidental or intentional damage by guests

- Theft by guests

- Loss of rent following damage

- Owners liability cover

Learn more about what the Own Home Rented policy covers.

What happens if my house is too damaged and can’t be lived in?

If your house is too damaged to be lived in (like a fire or flood) there is cover (up to $20,000) to go towards moving into a temporary house while repairs are completed. If you also get regular rental income from guests there is cover for your lost rents you would otherwise have got if your house wasn’t damaged.

We provide $20,000 of loss of rents cover for free, with options to increase to $40,000 or $80,000. Both loss of rents and alternative accommodation have a payout period of 12 months.

The Loss of Rent calculation will take account of future actual guest bookings that are cancelled, and expected bookings based on the same period in the previous year. If you are new to the home and income game then we will use short-stay occupancy rates in that particular region to estimate the loss. If you have a boarder or tenant with a fixed weekly rent then that amount will be used.

The policy aims to put the owner in the same financial position they were in before the loss, by paying for the repair costs and lost rental income – all while paying for the owners temporary accommodation costs.

Privacy Policy

This is the website of Initio Limited (initio). The administration of the website is performed by initio. The arranging of insurance contracts on this website, as well as policy and claims management is the responsibility of initio. ‘We’, ‘us’, and ‘initio’ refers to Initio Limited.

The postal address for initio is:

PO Box 319, Hamilton 3204

The physical address for initio is:

Level 1, 6 Garden Place, Hamilton Central, Hamilton, New Zealand

All email correspondence can be directed to [email protected]

Our telephone contact number is + 64 7 929 4126.

Our web server automatically recognises a user’s domain name.

We collect:

- Email addresses of those users that communicate with us via email.

- Email addresses of those who make postings via online chat.

- Email addresses (and other personal information as supplied by the customer) of customers who chose to transact with us, including users who email themselves a quote from our website.

- Aggregate information, data, and record of pages unidentified users access or visit, and how they interact with those pages.

- User-specific information, data and record of pages a customer accesses, completes, or visits, and how they interact with those pages.

- Information volunteered by the customer/user during the quote, sign-up and claims process.

- Specific personal contact and other information as supplied by the customer/user during the insurance signup and claims process.

- Risk data about properties or vehicles that we may quote on or insure. We may use third parties in order to collect this data.

- Personal contact information (including but not limited to email address, property location, and phone number) and risk information supplied to us by our partners, affiliates, and resellers through referral programs and other methods.

We Store:

The above information on our secure servers and related software and database applications.

The information we collect is:

- Shared with insurers (and their agents) who assist in providing support for the insurance placement, our internal operations, and underwriting of risk.

- Shared with an association, club, buying group or other business that are partners of initio and that our customer is a member or customer of. This information is limited to the customers name, the address of the insured property or vehicle year/made/model, effective date of cover, expiry date of cover, insurer premium, type of transactions (eg renewal), and payment type and interval

- Shared with broker partners who have advised their customer to insure with initio, and that cover has been placed through that broker’s dedicated gateway or page.

- Used by us to contact consumers by phone, email, or text message for marketing, follow-up or feedback purposes.

- Disclosed when legally required to do so, at the request of governmental authorities conducting an investigation and audit.

- Used to verify or enforce compliance with the policies governing our website and applicable laws or to protect against misuse or unauthorised use of our website.

- Disclosed to any successor entity in connection with a corporate merger, consolidation, sale of assets or other corporate change.

- Used to underwrite and bind insurance policies.

- Used to submit claims to insurers.

- Shared with associated suppliers, current or prospective insurance capacity providers,and service providers for claims processing and management.

- Used for all other purposes relating to the placement and management of a customer’s insurance.

- Shared with storage providers (including “cloud storage”) within New Zealand and overseas. We use reasonable endeavours to ensure people we disclose your personal information to outside New Zealand are required to protect it in a way that provides comparable safeguards to those set out under New Zealand privacy law

We Share:

With referrers/affiliates: where you have been introduced to initio by a Referrer or Affiliate we will share with that Referrer your name, your initio client number, and when you transacted with us.

If the Referrer is the market comparison website Quashed, as per your arrangement with them, we will share additional information including the address of the insured property and provide to them a copy of the initio policy schedule.

With partners: Where you have been introduced to initio by a Partner organisation (such as the New Zealand Property Investors Association or a Mortgage Advisor), of which you are a customer or member, we will share with that Partner the location of the risk (eg address of house insured), the period of insurance cover, the premium, the type of transaction (eg renewal, or new), the payment type and interval (eg annually or monthly), and if applicable the particular business, branch, office or region you are associated with.

With insurance brokers: Where your insurance placement has been facilitated through a broker, we will share with that broker the information we collect (as defined above). The way we do this is through reporting, and by providing your broker with copies of all communications and documents. For example, any email a customer receives from us will also be copied to that customer’s broker. This includes sharing with the broker the information about and correspondence we have with you, relating to any claims you make with us. We may also share information with the customer’s broker on specific request from the broker, and this may include but is not limited to claims records, claims status, policy insured values, excesses and the like.

With insurers: Initio is underwritten by a registered Insurer. We will share the collected information with this insurer either automatically or on request from the insurer. The insurer holds the ultimate risk for the customer’s insurance, and the information we collect is relevant for that insurer’s underwriting of the risk and assessment of claims.

With advertising providers: We may share certain information with advertising platforms to deliver and improve our marketing campaigns. This includes identifiers, website interaction data, and transaction information necessary for campaign measurement and optimisation.

You have the right to:

1. Request all information that is held about you by us.

2. Request that information held about you is corrected.

Cookies:

Cookies are small data files that a website host computer sends to, or installs on, a user’s computer to help it remember information you enter, by passing a unique ID between your computer and the initio website that identifies you.

We use ‘first party’ and ‘third party’ (including, but not limited to, Google Analytics, Google Signals and Hotjar) cookies on our website. The information recorded and tracked includes:

- Information that users/consumers input when obtaining quotes or filing in the online forms.

- User-specific information on pages users access, visit, complete.

- Past activity on our site in order to provide better service when visitors return to our site.