Search results for: {search_term_string}/house-flip-insurance

What you need to know about insuring your investment property.

Recently we were approached by the Auckland Property Investors Association to do a brief Q&A on landlords insurance, and some of the risks that landlords face in the modern market.

You can find some of the common questions and answers here. For more specific questions, you can always head over to our FAQ.

Q: Why do property owners take Landlord’s Insurance?

A: We have found that landlords tend to be quite sensible with their insurance decisions. The main driver for getting insurance is basic protection against the big loss risks such as fire, flooding, earthquake, and other natural disasters.

Sometimes current events will motivate landlords to seek cover for specific risks such as meth, or damage by tenants, but the “average landlord” still looks mainly to get cover for those big loss risks.

Q: What is the biggest risk for landlords and property owners?

A: The single most common cause for claims is leaking water pipes, especially in older homes where maintenance has not been carried out or has fallen behind.

Regarding what is costliest, no surprise that fires caused by wiring/electronics is the most damaging source. One of the most common sources is overloaded multi-plugs and wall sockets, especially where the multi-plugs are older/low quality.

Q: Insurance is one of those peace-of-mind expenses that people want to have but don’t want to claim on. What advice is there for investors to manage their insurance costs?

Depending on the provider and type of claims, it is true that too many claims will push up the premium. At the end of the day, insurance is there to be claimed on.

The best approach is to ask your insurer if they have any form of no-claims bonus or increase if a claim is made. While claiming with Initio will not penalise you in terms of premiums, other insurers may have a different approach. If the claim amount is just over the excess, it is worth considering not lodging.

The best advice to manage your costs is to select as high an excess as you can comfortably afford. This means you are protected against the major events, but due to fewer claims, you will end up spending less overall on your insurance bill.

Q: Are NZ landords adequately insured?

Unfortunately, not always. The Initio philosophy is to provide cover that ticks all the boxes right from the get-go. But insurance is a competitive market and some policies, while cheaper, do not include basic covers such as gradual damage, or even deliberate damage caused by tenants. If you are entirely focused on being a price-chaser than you could become underinsured.

If you have any questions or comments regarding the article, you can contact us to find out more.

We’re proud to share that initio has been recognised as a 5-Star Insurance Innovator in the 2025 Insurance Business New Zealand (IBNZ) awards. This award celebrates the companies that push the industry forward with real innovation, delivering meaningful results for customers.

Why this award matters

For us, innovation isn’t about shiny technology for the sake of it. It’s about using smart digital tools to make insurance simpler, faster, and smarter for homeowners and landlords across New Zealand. That’s why being recognised by IBNZ is special. Their judging looked not just at new ideas but also at proven results – how those ideas genuinely improve outcomes.

In 2024, we rolled out major improvements to our platform:

- Smarter online quoting that allows customers to compare cover and buy a policy in minutes

- A more intuitive dashboard where policyholders can manage their insurance 24/7

- Faster claims processing supported by real-time updates and better data sharing

- Behind-the-scenes risk technology that reduces friction for customers while keeping cover accurate and fair

Each of these developments was designed with one question in mind: how does this make life easier for our customers?

Smart insurance for smart people

Our customers are busy people who want insurance to just work – without the jargon, paperwork, or hold music. That’s why we’ve built a platform that puts control in their hands. The award validates that our approach, removing complexity and giving transparency, is working.

For example, being able to update your policy online, lodge a claim, or instantly access documents via your client dashboard isn’t just a “tech feature.” It means less stress when something goes wrong, quicker answers, and confidence that you’re in control.

What it means for our customers

Recognition from IBNZ is encouragement to keep going. But the real win is for our customers. Because every innovation we introduce is about:

- Saving time – no waiting on hold or posting forms

- Clarity – cover explained in plain language, upfront

- Confidence – knowing you can rely on us at claim time

- Fairness – technology that helps us keep pricing sharper and more accurate

Our customers sit at the front of every decision we make. This award highlights that focusing on them, rather than outdated processes, leads to better outcomes.

Looking ahead

We’re proud of the recognition, but we see it as a milestone rather than a finish line. Innovation never stops, and we’ll continue to improve how we serve New Zealand homeowners and landlords.

Complex insurance, made simple.

Try it for yourself. Start by getting a quote

Related articles

All our house insurance policies include cover for natural disasters up to the replacement sum insured you select on your policy.

From 1 July 2024 new governing legislation, the Natural Hazards Insurance Act 2023 came into effect. This Act modernises and replaces the Earthquake Commission Act 1993, now commonly known as the “NHI” (previously known as EQC).

Under the Act, the NHI will cover up to the first $345,000 including GST towards any insured damage. We (your insurer) then cover the repair costs over $345,000 – up to your replacement sum insured. This is called ‘top-up cover’. The NHI have a standard excess of $500 per insured home.

The NHC Commission also provides limited cover for land and land structures such as retaining walls, bridges and culverts.

If a Natural Disaster only damages your driveway, fence, patio, path, paving, tennis court or another artificial surface (i.e. not the house), this is not covered by the government NHC but may be covered by Initio. An excess of $5,000 applies in these instances.

We have a summary of the cover provided for your home and land by the Natural Hazards Commission here and you can view the full details on the Natural Hazards Commission Toka Tū Ake (NHC) site.

This information applies to the following initio products:

Login to make a claim

Related Articles:

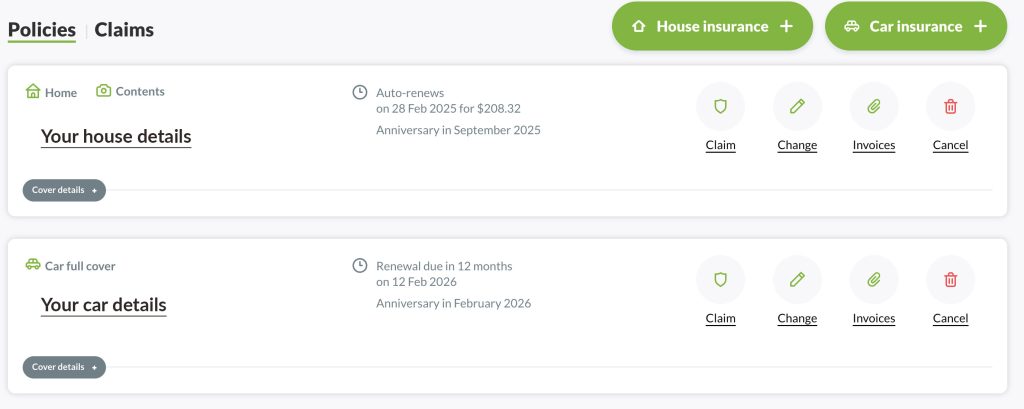

You can change how you pay for your policy. There are two key timings to be aware of when making a change:

- At renewal (your annual anniversary) – the change can be done as part of the renewal transaction.

- Mid-term (during the insurance year) – a new policy is required.

You should also check current premium rates before taking out a new policy. These may have changed since your last rates were set. You can check current premium rates at any time by using the quote options from your dashboard (home insurance + or car insurance +).

Changing from monthly to annual

If you want to change from monthly to annual payments at anytime, you will need to set up a new annual policy. Here’s how:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “Pay annually” option.

- Complete the application form and make the annual payment.

- Once the new annual policy is active, cancel your original monthly policy. Any unused portion of premium will then be automatically calculated and refunded.

Unfortunately, due to the different payment technologies used for monthly and annual payments, we’re unable to simply change an existing policy mid-term.

Changing from annual to monthly

What if I want to switch from annual to monthly payments?

How to achieve this depends upon the timing of your insurance year;

At your annual renewal

If your home policy is due for renewal, you can switch from annual to monthly by selecting the “Pay monthly” option during the renewal process from your customer account/dashboard.

Mid-term (during the insurance year)

If you want to change to monthly payments before or after your renewal date, you’ll need to set up a new monthly policy:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “pay monthly” option.

- Complete the application form and make the first monthly payment. The subsequent monthly payments will fall on the same day of the month that you start this policy from.

- Once the new monthly policy is active, cancel your original annual policy. Any unused portion of premium will then be automatically calculated and refunded.

Payment Options

Can I pay monthly by bank transfer or direct debit?

No, Monthly payments require a valid credit card or visa debit card and cannot be paid for by any other means.

Can I pay fortnightly, weekly or quarterly?

No, we only offer monthly or annual payment frequencies. We do not have alternatives available.

Remember, it’s always important to review your options carefully to make sure you’re selecting the best one for your needs.

Useful links:

Login now

When you think about claims, people generally jump to their own worst fear of their property burning to the ground, and that’s exactly why we all buy insurance. Big marketing hypes insurance products as providing ‘peace of mind’, but what you’re literally purchasing is compensation in the event you submit a claim – and a reasonable expectation that any such claim will be processed and paid to you. What do you need to know about claims when it comes to your property insurance?

Don’t sweat the small stuff

Claims are there for the major events – think fire, earthquake, storm damage – but also the slightly smaller but still very costly incidents such as a leaking pipe that damages flooring that your tenant didn’t notice. Insurance isn’t there for the day-to-day maintenance of a property, so don’t use your policy for repairs, ware and tear, and upkeep, as your insurer may deny those types of claims.

What about damage and the new legislation amendments?

The recent amendments to the Residential Tenancies Act provide that a tenant is liable to pay their landlord’s insurance excess or four weeks’ rent – whichever is lesser – but only for careless or intentional damage. Accidental damage, such as spilling a glass of red wine onto fluffy white carpet, may still be the responsibility of the landlord; further Government guidance and future Tenancy Tribunal decisions will provide more certainty on this.

A snapshot of Initio’s last 12 months of rental property claims shows that unexpected events such as house fires and storms take the lion’s share of the number and value of claims:

|

|

|

| Type of claim |

Number of claims |

Cost of claims |

| Accidental loss (e.g. storm damage, fire, burst pipe) |

55% |

70% |

| Accidental damage caused by tenants |

14% |

5% |

| Careless damage caused by tenants |

7% |

1% |

| Intentional damage caused by tenants (including meth) |

16% |

23% |

| Other/third party claims |

8% |

1% |

What types of claims are the most common?

As the insurance provider to over $2.5 billion of Kiwi property, Initio has its fair share of claims – so based on our experience, we can give you an insider’s view on what to look out for. In the last 12 months to end of August 2019, our 4 most common claims in order:

#1 Sudden water leak (eg burst pipe) – average claim value $5,916

#2 Tennant damage (eg malicious damage) – average claim value $2,960

#3 Weather damage (eg storm, flood) – average claim value $5,732

#4 Hidden gradual water damage (eg slow dripping pipe) – average claim value $1,980

The best insurance of all is the proactive management of the risks faced by the property. For example actively keeping an eye on areas where hidden leaks are most likely to occur (under the kitchen sink and in the bathroom) will reduce the likelihood of damage. But should you get hit with a nasty loss – well, that’s exactly what insurance is for.

Take action

Many customers seem to think that they must leave their water sodden carpet festering away until the insurance assessor turns up or their insurer says it can be taken out. This is definitely not the case. My advice is to act and to start the clean-up process; take photos and get on with things. It is important to note that most insurers want you to take steps to reduce any further loss, and taken action aligns with this. The exception here is fire damage, following a fire you will want to take steps to secure the property (eg. boarding up entry doors) but you should leave the property as is so that fire investigators have the best chance of determining the origin of the fire.

Know the process

The process around submitting and receiving payment for claims can be frustrating if you don’t know how long you’ll be kept waiting, and what is required of you as a claimant. So, when choosing an insurer it’s good to take the time to understand this upfront – so if and when you suffer a loss, you know what to expect and can have confidence in the process.

Get a quick quote online, insure online, lodge and see the progress of your claim online Initio.

Learn more about landlord insurance

Learn more about house insurance

Learn more about how claims work at initio

Insurance premiums can be a complex subject, influenced by a variety of factors. Whether it’s your personal driving record or larger market trends, it’s essential to understand how these elements may affect your cost of insurance, especially in New Zealand’s dynamic environment.

General factors impacting premiums

Weather events

New Zealand’s weather is becoming more erratic, with significant impacts on vehicles. For instance, North Island floods in 2023 led to a high number of vehicles being written off due to water damage.

Advances in technology & materials

Newer cars come with advanced technology like backup cameras and sensors. The materials used, such as aluminium, although beneficial for fuel efficiency and safety, are harder and more costly to repair.

Inflation & economic factors

With New Zealand’s inflation at a 32-year high and increasing labour costs, the overall cost of vehicle repairs is rising.

Claims cost inflation

Driven by the increasing frequency and costs of claims, the average cost for vehicle parts has surged by 8-10% over the past year. Labour costs have also seen an increase, now ranging between $115-$160 per hour.

Insurer’s data

Between September 2022 and February 2023, our underwriter, IAG NZ, recorded a rise in claims, especially due to weather events like North Island floods and Cyclone Gabrielle. The Insurance Council New Zealand reported that Cyclone Gabrielle had already resulted in costs of around $1.5 billion*

Personal factors impacting premiums

Location & past claims

Where you live, your past vehicle claims, the sum insured, and the type of car you drive all contribute to your premium rate.

Changes to cover

If you alter the agreed value, excess, main driver, or permit drivers under 25 years to use the vehicle, this will affect the cost.

Driver grades

If the main driver incurs an ‘at-fault’ claim, this changes the driver grade, affecting the premium. Learn more about driver grades here.

Government levies

A segment of your car insurance goes towards the Fire & Emergency NZ (FENZ) levy. This rate will increase to $10.96 (incl GST) per vehicle on 1 July 2024.

Why premiums may change

The cost you pay for insurance needs to mirror what it costs your insurance provider to offer the cover. With the various contributing factors outlined above, it’s understandable that premiums may undergo adjustments. Rates usually change annually, aligned with your policy’s anniversary.

Understanding these factors will better prepare you for any changes to your insurance premiums and equip you with the knowledge to make informed choices.

*Insurance Council New Zealand, September 2023

USEFUL LINKS

Diving into the next part of our series, we’re tackling how to stay one step ahead of Mother Nature’s surprises. As the seasons shift, weather patterns can change rapidly, bringing unexpected conditions right to our doorsteps. Lately, we’ve noticed an uptick in flooding enquiries from our community, highlighting the importance of being alert. We’re all for optimism, but being ready for any weather is just common sense. So, let’s pack our emergency kits and make sure we’re prepared for whatever comes our way. Here’s a quick guide to keeping safe, protecting your property, and getting through any weather challenge.

Make sure you’re ready for Mother Nature’s curveballs

Regardless of the type of natural disaster that might take place, the drill’s pretty much the same. So, let’s tuck this know-how into our mental back pocket – because, let’s face it, it’s always good to have a plan before the weather decides to crash our party. It’s been just over a year since we witnessed the severe impact of the consecutive flooding and storms of early 2023. They were a soggy reminder that while we’d love a year filled with nothing but sunshine and gentle breezes, hoping for the best without preparing for the rest is like wearing socks with sandals – a risky fashion statement in the world of weather.

While we remain hopeful for a calmer year ahead, we wouldn’t be in the insurance game if we didn’t value cautious optimism and thorough preparation for unforeseen events.

Make sure your emergency kit isn’t just a collection of last year’s Halloween candy and a flashlight with dead batteries. The following simple steps can lessen the impact of future major events and help make your recovery just that little bit smoother:

Stay Safe and Informed

- Listen to updates from official channels like Civil Defence and emergency services. Keeping you, your family, and your fur babies out of harm’s way is priority number one.

- Gather essential items like your emergency bag and a lockbox with important documents.

Secure and Document

- If your home is safe, make temporary repairs to secure it. Take photos of any damage for insurance purposes.

- Move valuable items to a safe place if possible. Your insurance might cover the cost of storing these items.

Communicate and Manage

- If your home is damaged but livable, contact your insurance provider for advice on urgent repairs. Keep all documentation and receipts related to the damage and repairs.

- Be aware of repair scams. If the damage is serious or your home is not safe, get in touch with your insurance provider for prioritised support.

Cleanup and Claims

- Begin cleanup for flood damage by removing affected items, and document everything with a list and photos. Keep damaged items for assessment.

- Arrange for emergency repairs to prevent further damage, knowing these costs can be covered by your insurance claim.

This guide ensures you know the steps to take for safety, protecting your property, and efficiently handling insurance claims during emergencies.

OTHER ARTICLES OF INTEREST

EXTERNAL RESOURCES

Smart moves insight VI

In this final chapter of our Smart Moves series, Graeme Fowler reflects on the future of property insurance and what landlords can do now to stay ahead, no matter what the market throws their way.

Do you spend much time thinking about where insurance is heading?

“Not really—but I do make sure I’m ready to adapt when things change. You can’t control the market, but you can make sure your foundations are solid.”

Graeme’s approach is simple: focus on what you can control. That means keeping your policies current, reviewing your cover annually, and ensuring your paperwork is in order—especially as your portfolio grows or changes.

What do you think landlords should be doing to future-proof their portfolios?

“Keep your policies up to date. Review your sum insured. Don’t let cover lapse just because you’ve had a quiet run. Disasters don’t check your calendar.”

Graeme recommends making policy reviews a yearly habit, particularly after renovations or new purchases. He also stresses the importance of maintaining enough cover to reflect today’s rebuild costs—not the prices from five years ago.

Managing this doesn’t have to be hard. With initio, you can renew your policy, adjust your excess, update cover, or add new properties—all in just a few clicks. You can check and update your sum insured anytime using our digital tools and calculators, with helpful articles to guide you through.

Are there trends landlords should be watching?

“The cost of insurance is likely to keep rising. That’s just the reality. So work it into your numbers—don’t treat it like a surprise.”

Graeme points out that premiums, like everything else, are being affected by inflation, labour shortages, and increased risk exposure. And while you can’t change these external forces, you can plan for them.

Any final advice for new or growing landlords?

“Don’t treat insurance like a checkbox. It’s not something you do once and forget about. Make it part of your overall strategy—protect what you’re building.”

That mindset is key. Insurance isn’t just a cost—it’s a tool to protect your investment, preserve your cashflow, and reduce uncertainty. Whether you’re insuring one property or a large portfolio, the goal should be the same: stay covered, stay compliant, and stay in control.

Final thoughts from initio

Managing your insurance is designed to be easy and on your terms. No paperwork, no phone calls, no waiting around. Just fast, flexible, and fully online insurance that fits the way you work.

We’ve built a platform for property investors who value control, speed, and transparency – because we’re investors too, and we know the frustrations of traditional insurance. Whether you’re updating your cover, adding a new property, or making a claim, everything is in your hands, 24/7.

You get real-time quotes that reflect up-to-date risk and levy data, automated policy updates, instant documentation, and built-in tools to help you manage rebuild costs and risk exposure.

Complex insurance, made simple (finally!). That’s the initio way.

Thanks for following the Smart Moves Series.

Want more insights from experienced investors? Keep an eye on our blog for upcoming interviews, case studies, and landlord resources.

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Related support articles:

Christmas is the busiest time of year …. for burglars. House insurance is just one part of managing your house and contents risk. Heres a guide on protecting your property.

It’s coming into that time of year where we like to take a load off – relax for a couple of weeks, put the feet up at the bach, or even head off overseas – but it’s also the time of year when burglars tend to be more active. Leaving houses empty for periods of time can be risky in several ways, and among other factors, result in an uptick of property insurance claims. We’ve all seen Home Alone!

Holiday homes are particularly vulnerable as they are often left unoccupied for extended periods of time, but even our own homes need to stay secure and damage-free over the silly season.

Burglary prevention is equally important for holiday homeowners, landlords, and people with a single main residence. Importantly, burglary isn’t only about having your contents stolen, but also the fact that thieves can cause significant damage to other possessions and the property itself whilst trying to gain access.

Property insurance cover is designed to protect you if the worst should happen, but as a property owner there are several steps you can take to avoid having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy.

Prevent opportunistic burglars from targeting your property by:

- Keeping all valuables out of sight. Gifts under the tree are tempting for thieves so make sure they, and other valuables, can’t be seen from the outside the home. Also be careful when disposing of any tell-tale packaging

- Checking window joinery, and promptly replacing or repairing any loose latches

- Installing security stays on windows

- Fitting deadlocks or deadbolts to all external doors, especially older doors and ranch sliders which can be more easily broken into

- Installing a burglar alarm and advertising the presence of an alarm

- Installing exterior sensor lights, and checking any existing lights are working correctly

If possible, make it difficult for someone to break into your home. Trim trees and shrubs so there are no places for burglars to hide and move wheelie bins and other large objects away from fences, ledges and drop-offs wherever possible. Lock your shed and put away any tools, to remove the temptation of them being used to aid access.

Something else to consider is not advertising that you are away: keep your lawns mowed, gardens tidy, the mailbox clear and avoid leaving messages on social networking sites and answering machines with dates and other specific details of your absence. Let your neighbours know if you’re going to be away, give them your contact phone number, and have if you a good relationship with your neighbour – ask them to clear your mail, or park in your driveway to keep up the ruse.

Good security makes people feel safe; it also has the added benefit of retaining good and long-term tenants – and for holiday homes, a reputation for a safe and secure property.

Loss of rent insurance helps protect your rental income if your property cannot be lived in or your tenant stops paying rent. Under initio’s landlord insurance, loss of rent cover is included automatically. This guide explains when it applies, how much cover you get, and what is not covered. This can also be included in our holiday home cover if you also rent your bach to guests.

Quick summary

-

Loss of rent is automatically included with landlord insurance.

-

Standard cover is $20,000, with options to increase to $40,000 or $80,000.

-

Cover applies if damage makes the property uninhabitable.

-

Cover may also apply after tenant eviction or abandonment.

-

Overdue rent before eviction is not covered.

-

Holiday homes have cover for cancelled guest bookings due to damage.

What is loss of rent insurance?

Loss of rent cover replaces rental income when you cannot collect rent due to certain insured events. This usually happens when:

-

Damage makes your property unliveable, or

-

A tenant is evicted for non-payment, or

-

A tenant leaves without notice.

It helps reduce financial pressure while you repair the property or secure a new tenant.

How much loss of rent cover do I get?

Landlord insurance includes $20,000 of loss of rent cover as standard.

You can increase this to:

For property damage claims, payments stop when:

-

Repairs are complete and the property can be rented again, or

-

You reach your selected cover limit, or

-

12 months of rent has been paid,

whichever happens first.

When does loss of rent cover apply?

Property damage that makes the home uninhabitable

If claimable damage means your tenants must move out, loss of rent cover replaces the rental income during repairs.

Example: A flood damages carpets and internal walls. Your tenants move out while repairs are completed. Loss of rent cover replaces the rent you would have received during that period.

Cover is paid until the property is liveable again, up to your selected limit or 12 months.

Tenant eviction for non-payment of rent

If a tenant is more than 21 days behind in rent, you may apply to the Tenancy Tribunal for eviction.

Once the tenant is evicted, landlord protection under your policy can pay up to 6 weeks of rent, or until you find a new tenant, whichever comes first.

-

Overdue rent (arrears) before eviction is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations under the policy.

Tenant leaves without notice

If a tenant vacates the property unexpectedly and stops paying rent without giving the required notice, the policy can pay up to 6 weeks of lost rent, or until a new tenant is secured, whichever comes first.

-

Normal vacancy between tenancies is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations.

Does loss of rent apply to holiday homes?

Yes. If you rent out your holiday home to paying guests, loss of rent protection is included.

Holiday home damage and cancelled bookings

If claimable damage makes the property uninhabitable, we will cover lost rental income from cancelled guest bookings.

You automatically receive:

Payments may consider:

-

Confirmed bookings that must be cancelled.

-

Expected future bookings, using previous rental income history where appropriate.

The maximum payment is your selected limit or 12 months, whichever comes first.

What does not apply to holiday homes?

The 6-week tenant eviction or abandonment benefit does not apply to holiday homes, as short-term guests do not have formal tenancy agreements.

What is not covered?

Loss of rent cover does not include:

-

Rent arrears before eviction.

-

Normal vacancy between tenants.

-

Guest cancellations unrelated to claimable damage.

-

Eviction benefits for holiday homes.

Always ensure you are meeting your landlord obligations under the policy.

Frequently asked questions

Does landlord insurance cover unpaid rent?

It may cover rent after eviction or abandonment, but it does not cover overdue rent before eviction.

How long is loss of rent paid for?

For property damage, up to 12 months or your selected limit. For eviction or abandonment, up to 6 weeks.

Do I need to add loss of rent cover separately?

No. It is automatically included in landlord insurance and holiday home cover (if rented).

Related Articles:

Insurance premiums don’t increase simply so the insurer can make more money – they increase so the insurer can afford to pay claims and stay in business. These are just some of the reasons why initio has seen premium increases in recent years.

WHERE DOES MY PREMIUM GO?

In this example we have used a typical house insurance premium of $997.28 inc GST to depict the actual levies and taxes paid, and the approximate distribution of the remainder of the premium.

METHAMPHETAMINE

IAG pays out $14 million in methamphetamine claims on residential properties each year. IAG receives up to 80 new Methamphetamine claims each month. The average decontamination claims costs $25,000. With detailed testing ranging from $3,000 to $10,000, and house decontamination costing between $2,000 and $50,000.

NATURAL DISASTERS AND WEATHER EVENTS

2 Days of wild weather in March 2016 cost insurers $30 million, with 687 House and Contents Claims, costing over $2 million.

2 Days of wild weather in March 2016 cost insurers $30 million, with 687 House and Contents Claims, costing over $2 million.

12 months later in March 2017 a months’ worth of rain fell in 24 hours that costing insurers another $42 million. This time the effect was greater on homes with 5824 House and Contents Claims that costing $24.5 million.

GOVERNMENT LEVIES

Government imposed Fire Service Levies increased from 1 July. If you are renewing cover after this date the additional cost to you is $41.40. The annual cost of Fire Service Levies is $146.28.

Government imposed Earthquake Commission Levies are increasing from 1 November. If you are starting your cover on or after this date the cost of you insurance will increase by $69. The annual cost of Earthquake Commission Levies is $276.00.

EARTHQUAKES AND REINSURANCE

Before the Canterbury 2011 earthquakes, reinsurance costs made up about 7% of total cost of house insurance, now that amount has tripled to about 20%. The risks associated with natural hazards were grossly underestimated before the 2011 quakes.

The Natural Disaster Fund has paid out $9.5 Billion so far in claims to people affected by the Canterbury Earthquakes. It is expected another $550 Million will be paid out for claims relating to the 2016 Kaikoura Earthquake.

INCREASED CLAIM COSTS

The Health and Safety at Work Act 2015 has meant increased compliance costs for all building repairs and more on site safety requirements. For example, a single tradesperson is no longer able to access a roof via a ladder; now there must be two tradespeople on every job, and they must use a scaffold.

In April 2016, the Asbestos Regulations came into force, as a result, the cost of removing Asbestos Containing Material has increased significantly. For example, a straightforward textured ceiling removal that may have cost $1,000 in 2015 would now cost over $5,000 to remove.

INCREASES IN BUILDING COSTS

Strong demand and not enough supply has seen the average cost of building a new home in New Zealand’s four largest cities rise by 21.09 percent since the previous peak, (and last building boom), in 2007.

Strong demand and not enough supply has seen the average cost of building a new home in New Zealand’s four largest cities rise by 21.09 percent since the previous peak, (and last building boom), in 2007.

There is more to building cost inflation than simply labour and material cost escalation. Other significant cost increases can be found in health and safety compliance and higher levels of specifications being imposed such as higher seismic loads.

USEFUL ARTICLES

How are house insurance premiums calculated?

Why has my premium changed?

Why does the global insurance pool impact my premium?

My Mortgage & Initio have teamed up to provide clients with house and contents insurance, and dedicated claims management when you need it. You can get a quick quote below, and cover can be started online.

Working out the right sum insured can be harder when your home is not standard. Renovations, custom features, and specialist materials can all affect what it may cost to rebuild, and those details are easy to overlook.

Online calculators can be a helpful place to start. They are designed to give you an estimate based on typical building replacement costs, using the information entered along with available property and construction data.

Online calculators do not provide advice, and they may not capture every detail that could affect the rebuild cost of your home. If you would like a more tailored assessment for your specific property, a quantity surveyor or insurance valuation service may be the best option.

Key takeaways in this article

- Renovations can increase rebuild costs

- Unusual homes may cost more to rebuild

- Non-standard materials can affect your sum insured

- Custom features are easy to overlook

- A calculator is a useful starting point

- It’s worth checking whether the estimate feels right for your home

Why this matters for insurance

Your house insurance should reflect what it may cost to rebuild your home to a similar size and standard using today’s building costs.

For many homes, an online calculator can provide a useful estimate. But if your home has unique features, premium finishes, or non-standard construction, the cost to rebuild may be less straightforward. That is why it is worth taking a closer look before relying on the result.

What counts as an unusual feature?

An unusual feature is anything that could make your home more expensive or more complicated to rebuild than a typical home of a similar size. This might include:

- architectural design features

- high or vaulted ceilings

- custom kitchens or bathrooms

- bespoke joinery

- imported fittings or finishes

- unusual rooflines

- heritage details

- specialist glazing

- detached studios or sleepouts

- retaining walls or complex outdoor structures

These types of features can all add cost and may not always be fully reflected in a standard estimate.

How renovations can affect rebuild cost

Renovations can improve the layout, finish, or quality of a home, but they can also increase what it would cost to rebuild. For example, rebuild costs may be higher if you have added:

- an extension

- a new kitchen or bathroom

- premium flooring

- double glazing

- custom cabinetry

- upgraded cladding or roofing

- decks or attached outdoor living spaces

Even if the work was done years ago, it can still affect what your home would cost to rebuild today.

Why non-standard materials matter

Some homes are built with materials or methods that are less common. This can make rebuilding more expensive, especially if the materials are harder to source or require specialist trades. Examples can include:

- specialist cladding

- imported tiles or finishes

- plaster systems

- unusual timber treatments

- stone or decorative masonry

- architectural glass

- custom metalwork

If your home includes materials like these, it is worth making sure your sum insured reflects that.

Older homes can have hidden complexity

Older homes can also be more complex to rebuild than people expect. They may include features such as native timber, ornate detailing, decorative ceilings, original fittings, or older construction methods. Even if you would not replace every detail in exactly the same way, older homes can still involve more labour and higher rebuild costs.

Before relying on the estimate

If your home has been renovated or includes unusual features, it is worth asking yourself:

- Have I upgraded parts of the home since I last reviewed my cover?

- Does my home have high-spec or custom finishes?

- Are there any specialist materials that may cost more to replace?

- Is my home harder to rebuild than a standard house of similar size?

- Would site access make demolition or rebuilding more expensive?

These questions can help you decide whether the estimate feels realistic for your home.

Why a calculator is still useful

An online calculator is still a helpful starting point. It can do a lot of the heavy lifting and help you get close to a realistic figure without having to work it all out from scratch.

Initio uses the Cotality Sum Insured calculator to help estimate what it could cost to rebuild your home. It uses the details you enter, or confirm, and compares them with construction industry data to generate an estimated rebuild cost for the improvements on your property. The main thing to remember is that it provides an estimate, not a tailored assessment. If your home has features that make it different from a more standard property, it is worth taking the time to sense-check the result.

Final thoughts

If your home has unusual features, renovations, or non-standard materials, it is worth giving your sum insured a bit more attention. These details can all affect rebuild cost, and they are easy to underestimate.

An online calculator can help you get started, but the final figure should still feel right for your home. If you are unsure, getting a more tailored assessment from a quantity surveyor or insurance valuation service may give you more confidence in the amount you choose.

Related articles

FAQ’s about non-standard houses

Can renovations affect my sum insured?

Yes. Renovations can increase the cost to rebuild your home, especially if they involve extensions, upgraded finishes, or custom features.

What are non-standard materials in insurance terms?

These are materials or construction features that are less common and may cost more to source, replace, or rebuild.

Can a standard calculator still work for an unusual home?

Yes, it can still be a useful starting point. But if your home is more complex than average, you should review the result carefully.

Why would an architecturally designed home cost more to rebuild?

Architectural homes often include more complex design features, specialist materials, and higher-end finishes, which can increase rebuild cost.

Can site access affect the cost to rebuild?

Yes. Steep, narrow, or difficult-to-access sites can increase demolition and rebuilding costs.

Written by Toby Pudney – Initio’s Support Team Lead

Toby has been with initio since 2023 and is the Support Team Lead. He brings more than six years of experience in the insurance industry, giving him strong knowledge of general insurance. He has studied with ANZIIF and holds a qualification in New Zealand Compliance for Advisers (General Insurance Broking).

DECLARATION

To be completed by the insured(s) shown and also on behalf of any other person to be covered by this insurance.

I declare that:

1. All information contained in this proposal and on any attachment is complete and correct;

2. I have disclosed all material facts to Initio;

3. I agree that this proposal shall be the basis of the contract between me and Initio and I am willing to accept the terms, conditions and exclusions of this insurance;

4. I am authorised to complete this proposal on behalf of all people to be covered by this insurance and they give the same declarations.

By signing I authorise the insurer to:

Check our details on the Insurance Claims Register and place our claims information on the Insurance Claims Register which other insurers can access;

Disclose our personal information about this insurance to other members of the insurance industry and/or parties who have a financial interest in the subject matter of this insurance;

Obtain our personal information held by any other party regarding my/our existing and previous insurances.

YOUR DUTY OF DISCLOSURE

You must tell us everything you know (or could be reasonably expected to know) that a prudent insurer would want to take into account in deciding:

a. Whether to agree to insure you

b. if so, on what terms

Examples of what you must tell us include:

a. anything that increases the risk of a claim

b. any criminal offending or convictions

c. any previous insurance claims

d. any refusal by another insurer to insure you on standard terms.

You must also tell us this every time this policy renews and when you make any changes to it. If you fail to do this, we may void the policy retrospectively. You will have no insurance at all. When in doubt, disclose. We treat all information confidentially

CHANGE IN CIRCUMSTANCES

You must tell us about any material changes in your circumstances after the policy starts and during the policy period

PRIVACY

The personal information you provide in this proposal will be held by Initio and IAG.

Our collection of this information is part of your duty of disclosure at law to us, and is compulsory

If you fail to provide it, we may choose not to insure you.

You have rights of access to the personal information, and correction of it, under the Privacy Act 1993.

REPLACEMENT SUM INSURED

The ‘replacement sum insured’ above represents the total replacement value of your dwelling and improvements (eg driveways, swimming pools, fencing etc). Initio & IAG do not accept any responsibility for the accuracy of this value. You are responsible for determining and accepting this value. An insurance valuation or using an online replacement value calculator will provide you with a more accurate replacement value.

Non Disclosures

Disclosure vs. Declaration

Where do I disclose additional information?

Please include all relevant details in your online application form. If there’s anything not covered in a specific question, you can disclose it in the final question: “Is there any further information likely to affect the acceptance of this insurance?” Select Yes and a text box will appear where you can record your disclosures.

Smart moves, part V

In this edition of the Smart Moves series, we tackle a question some seasoned investors eventually ask: should I self-insure? Graeme Fowler shares why, even with decades of experience, it’s not a gamble he’d take.

Have you ever seriously considered not insuring?

“Not once. Even if I owned 500 houses outright, I wouldn’t do it. The risk is just too big.”

Graeme says the idea of not insuring, or ‘self-insuring’ – where you skip traditional insurance and rely on your own reserves to cover any potential loss – might sound appealing to confident investors. But in reality, it’s a dangerous bet.

From initio: Some landlords toy with self-insurance after years of no claims. But it only takes one event – a fire, a major flood, an earthquake – to wipe out years of progress. Comprehensive cover isn’t just peace of mind, it’s smart protection for your property and future income.

Why do you think some landlords consider it?

“Usually because they haven’t had a big claim yet. It gives a false sense of security. You think, ‘I’ve never had to claim – why am I still paying?’ But the day you need it, you’ll be glad you did.”

Graeme compares it to health insurance – you don’t buy it hoping to use it, but you definitely want it when things go wrong.

What kinds of events make insurance non-negotiable?

“Fires are the big ones for me. I’ve had a few over the years, and they’re expensive – repairs, temporary accommodation, loss of rent. Without insurance, I would’ve taken a massive hit.”

He also points out that natural disasters like floods and earthquakes are unpredictable and can affect multiple properties at once – something no reserve fund can reliably cover.

From initio: Our policies cover comprehensive replacement for accidental fire, storm, flood, and more. And with loss of rent included when a claim makes the home uninhabitable, your income is protected too.

But it’s more than that, insurance is what steps in when the stakes are highest. A fire or natural disaster doesn’t just damage property – it disrupts lives. You might need to relocate tenants, pause income, and navigate months of rebuilds or repairs. That’s not something most landlords can self-fund, especially if multiple properties are impacted at once.

That’s where we come in. The purpose of insurance is to absorb those risks on your behalf. You pay a premium so that when the worst happens, you’re not left scrambling. You’re backed by a provider that’s prepared to step in with cover, support, and real financial backing when you need it most.

And because disasters don’t give you notice, our policies are designed to respond fast. Claims can be lodged online in minutes, and we’ve built a digital-first platform to speed things up – so you’re not stuck waiting around when time matters most.

What would you say to investors who feel overinsured?

“You’re not. You’re covered. That’s a good thing.”

Graeme says insurance isn’t about trying to beat the system – it’s about protecting what you’ve built. “I’d rather have cover and never use it than need it and not have it.”

From initio: With the right cover in place, you’re not throwing money away – you’re protecting your investments from the risks you can’t predict or prevent.

Coming up next in the Smart Moves Series:

Looking ahead: what does the future of insurance for landlords really look like?

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Related support articles:

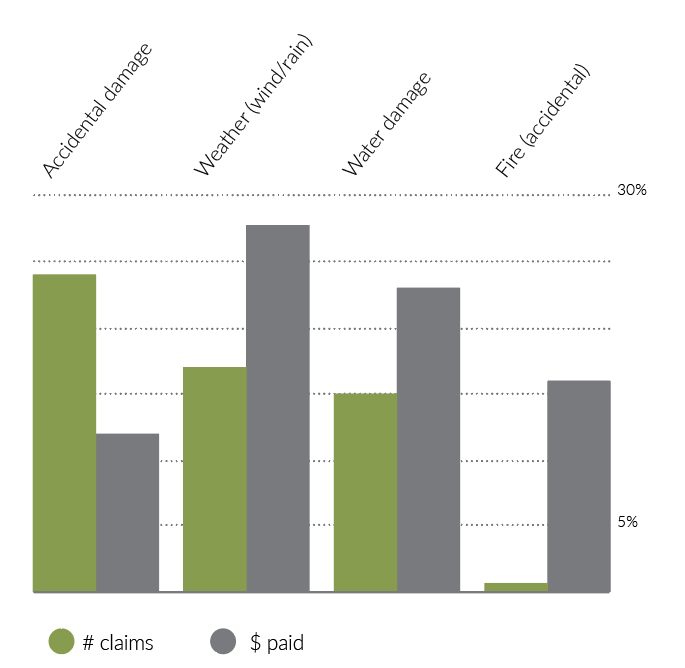

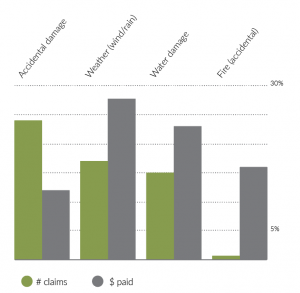

Another year has come and (nearly) gone so here’s a review of the year that was. This year, initio processed nearly 45% more claims when compared to 2021. We think you’ll agree, it’s a big increase and is indicative of both of greater rate of weather-related claims, and the significant support from kiwi homeowners (more policies, means more claims)

In relation to the house & contents claims we saw this year, accidental damage was claimed most frequently at 24% but only cost 12% of all payouts. On the flip side of this, pesky weather-related events (storms, flooding, wind, rain) were the cause of 17% of our claims but responsible for nearly 28% of our payments.

They were closely followed by various types of claims citing water damage as the cause (not including weather-related flood damage) costing 23% and (accidental) fire claims 16% of all payouts. It’s also worth noting here that less than 1% of all claims cited accidental fire as the reason. This means that while it might not be a common reason to claim insurance, it sure is costly.

Insurance is there to cover you for the unexpected, but sometimes the unexpected is also a little unusual. Our team have come up with the following claims that deviate from the usual reasons:

Dog + Robot Vacuum = Big mess

While modern technology is usually supposed to make life easier, sometimes it can go horribly wrong. This year we saw a claim involving someone looking after their parents’ dog. This person had to take a zoom meeting and during that time, the dog, unfortunately, had a code brown on a rug. This also coincided with their robot vacuum doing its rounds which tried its very best to help but ultimately made the situation much, much worse.

Both the vacuum and the rug needed to be replaced (but they kept the dog).

This year we saw 11 pet damage-related claims in total (1% of total claims). Our four-legged friends caused nearly $18,000 worth of damage this year – which doesn’t include one motor vehicle accident caused by swerving to avoid a cat. Dogs proved to be the most troublesome with the finger being pointed at them twice as often as cats.

Speaking of family members, children have also caused their fair share of damage this year. Although worth pointing out, the two-legged family members haven’t caused as much damage as pets.. We’ve only seen 6 claims involving children. These included:

- Drew on lounge carpet with a marker (for two different claims)

- Damaged fridge

- Scratched television

- Damaged walls

- A toy was thrown at the TV – breaking the screen.

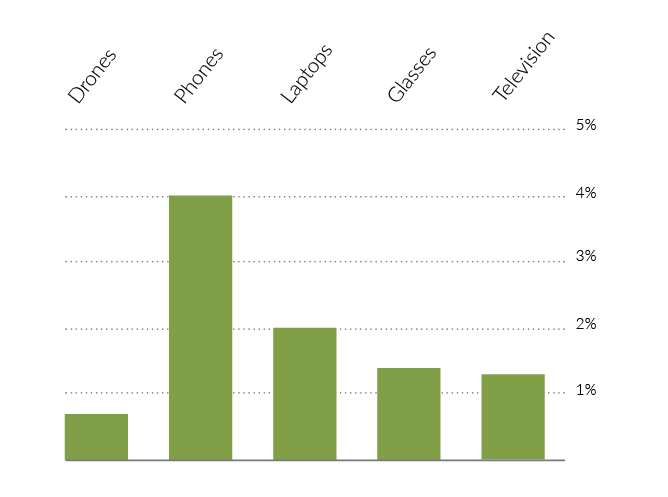

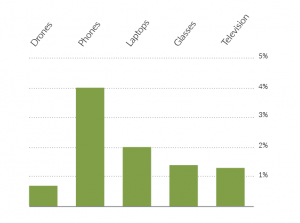

Technology has also been in the wars this year. We’ve seen 7 claims involving drones, which a couple of years ago wouldn’t have even been a blip on our radar. Phones are still the most commonly claimed gadget, but who knows what the future looks like?

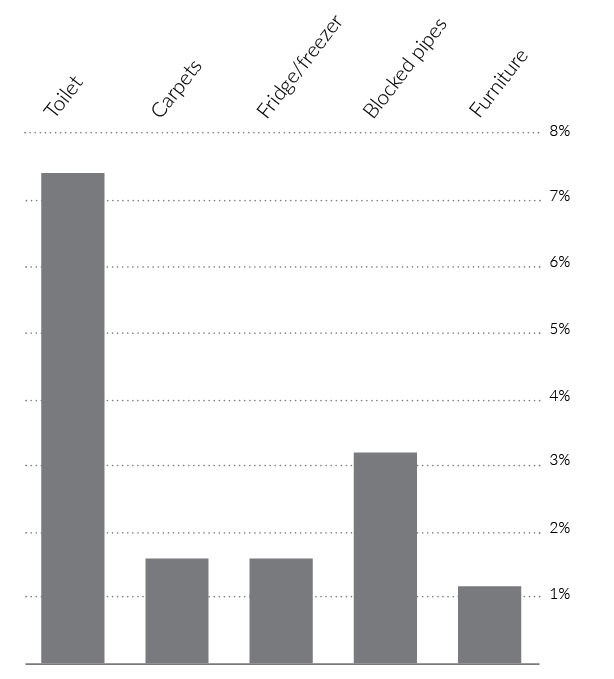

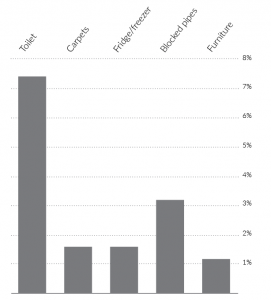

In terms of household items, toilets have been the most troublesome (including x2 phones dropped into the toilet) with blocked pipes coming in second.

We try to remove roadblocks in our claims process – there’s enough stress dealing with the event that you’re claiming for in the first place. We make an effort to alleviate some of that stress by processing claims as quickly and efficiently as possible.

Hopefully, you’ll never need to find out for yourself how good we are, but it’s nice to know we’re there for you when you need it

Percentages in this article have been rounded.

The hot recent housing market has seen Kiwis buying and selling houses at some of the highest rates ever.

The hot recent housing market has seen Kiwis buying and selling houses at some of the highest rates ever.

While the effects of FOMO (fear of missing out) may make it tempting to dive into the market, we’re here to remind potential home-owners the importance of due diligence before buying, particularly dealing with meth contamination.

We’re seeing signs of complacency creeping in, as people look to ‘hurry up’ the process, or start reaching for houses that aren’t in the best nick.

If you’re buying a rental property it’s essential you consider that it could be contaminated with meth.

The seller must disclose to potential buyers if there is contamination over 15 micrograms (μg) per 100 square centimetres of meth contamination. This is considered a material property defect.

However, the seller only needs to disclose contamination below 15μg per 100cm2 if they are specifically asked by the prospective buyer (or where the buyer has shown a clear interest in meth contamination).

Your first takeaway should be that if nothing is provided, simply ask the seller about meth contamination at the very least. This is an easy win.

No meth information provided by the seller?

Disclosure is only required if the seller knows about the contamination. In reality, people often don’t know their property is contaminated as there’s no legal requirement to keep testing your rental. Meth often flies under the radar, especially at lower levels.

Therefore you should always have some form of confirmation it isn’t contaminated. See first if anything is disclosed on the real estate listing (ask the agent!). If not, ask the seller if they suspect there could be any contamination (preferably in writing).

If neither can provide any confirmation, you should arrange a test yourself. You can easily do a composite test with a self-testing kit for less than $50. This won’t tell you the level of contamination – it’s simply to tell you whether meth is present or not. It will only put a small dent in your budget, and point out if a more expensive professional composite test is required to find the exact levels.

A swab test is well worth the money.

What if you buy a contaminated house unknowingly?

In short, you could be in for a cleaning bill in the tens of thousands. We paid out an average of $22,000 per meth claim in 2020.

Unfortunately we’ve seen more examples of people buying new houses, and quickly finding contamination. They then enquire about lodging a meth contamination claim.

It’s a painful conversation we never want to have, as in most cases it won’t be covered.

If there’s no record of the house being clean when purchased, insurance companies generally won’t pay for meth discovered within 90 days of your policy beginning. This is because they don’t know the culprit who is responsible, and chances are the contamination happend before the period of cover.

So please take a moment to enquire, ask, and test for meth where necessary before buying. It could save you thousands!

Initio are the pioneers of online house insurance in New Zealand.

Learn more about us

It can be common to claim for fallen trees and branches after a severe weather event, for the damage caused to houses and guttering, fences, cars and neighbouring properties.

In general, a home insurance policy doesn’t cover trees themselves; but you may be covered if a fallen tree has damaged your insured structures (cars, buildings, fences, special/recreational features) within the boundaries of your home. In these situations, we’ll cover the costs to remove the sections of the tree required to enable safe repairs – and you’ll need to arrange the tree’s disposal.

Some common examples;

1. A tree has fallen and damaged your car or living room

If the fallen tree has damaged your insured property, we’ll cover the cost of repairing the damage as part of your claim, including removing specific sections of the tree required to enable safe repairs. The insured is responsible for arranging and paying for the tree’s disposal.

2. A tree has fallen over on the lawn or driveway

If the tree has not caused damage, cover for the cost of cutting up or disposing of the tree does not apply.

3. A tree has partly fallen against my house, but it hasn’t caused any damage – am I covered?

If there is no damage to the house, then the cost of removing the tree is not covered. You should take reasonable steps to remove the tree to protect your property and prevent future damage. If you discover damage after removing the tree, then please let us know.

4. My tree has fallen onto my neighbour’s property – am I liable?

A homeowner will generally not be held liable for damage that their trees cause to other people’s property in a severe weather event. However, if it can be proven that they were negligent in not removing rotten trees or had ignored requests for removal, then they may be held liable.

5. Tree roots have grown and caused the underground pipes to block – is the removal of tree roots covered?

Our automatic additional benefit ‘water or sewage pipe blockage’, will pay a limited annual amount toward unblocking pipes. But, the cost to remove the tree roots is not covered.

Tips for tree maintenance

Got a tree or two around your property? Taking care of them is one way to reduce the risks of damage when bad weather strikes. Here’s the lowdown on how you can keep them in tip-top shape:

- Give ’em a good look: Assess the trees around your place before and after severe weather. Spot anything weakened or damaged? They might need a trim or even removal.

- Chat with the Council: Check with your local council about the rules for chopping, pruning, or trimming a tree on your, your neighbour’s, or council land. And don’t forget to see if the tree has any special protection.

- Spotted something? Speak up! If you notice a problem with a tree on council property, don’t be shy. Report it to your council pronto.

- Know your limits: Trimming a branch is one thing; taking on a big project that could damage a house or hurt someone is another. For the bigger stuff, it might be best to bring in a professional arborist.

- Think before you plant: Before you get that tree in the ground, think about how it’ll grow. Steer clear of planting large-growing trees too close to your house or other property. Know how your trees will grow above and below the ground before you plant them, and avoid placing ones that will grow large and too close to your house and other property.

For more information, please refer to your full policy

MORE ON THIS TOPIC

With First Lane you can insure your rental property, house or holiday home insurance online. Enter your property details to get an instant quote, if you like what you see you can start cover online with payment by credit card or bank transfer.