Search results for: {search_term_string}/house-flip-insurance

What claims cost the most, and what are the most common claims of 2024?

As we approach the end of 2024, we’ve taken a closer look at the trends in claims across the range of insurance policies we offer. The main ones being holiday homes, rental properties, owner-occupied homes and vehicles. Understanding these trends helps us, as your insurance provider, to stay on top of the risks that matter most to you – and also gives a bit of insight into what’s happening out there in the real world. Here’s a summary of what we’ve found.

Please note these figures only cover the most common categories. They are not an all-inclusive list and may not total 100%.

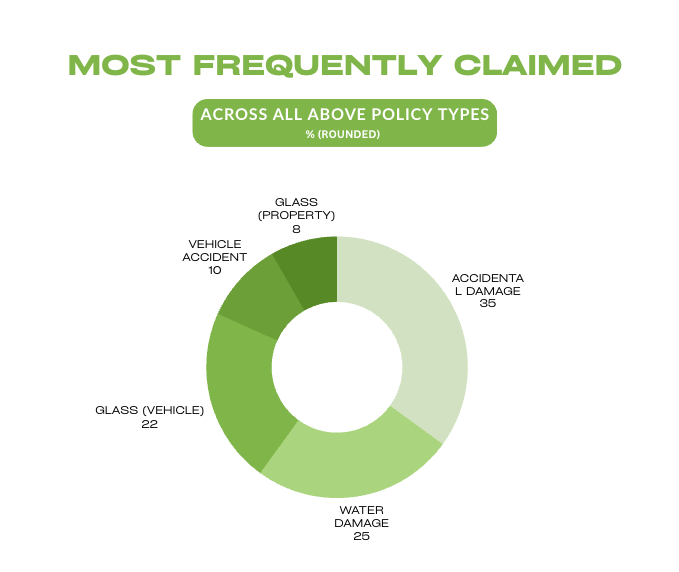

The most common claims this year

Across all policy types discussed in this article – Own Home, Holiday Home, Rental/Landlord, and Vehicle – two trends dominate: accidental damage and water damage.

Accidental damage is one of the most common types of insurance claims because it covers a wide range of unexpected scenarios. Accidents are often unavoidable, even with the best precautions, which is why having comprehensive insurance is so important. It ensures you’re protected from the financial impact of repairs or replacements, helping you get back to normal quickly without unnecessary stress.

Water damage, including hidden water damage, is another significant area of cover. Hidden water damage applies to gradual leaks from internal water pipes or tanks that aren’t visible. Coverage is subject to specific conditions and limits, so it’s worth understanding what’s included in your policy. Sudden water damage, such as from a burst pipe, is generally covered under most policies.

For more details about how we handle water damage, visit our water damage support page – it’s always good to know exactly what’s included.

For more information:

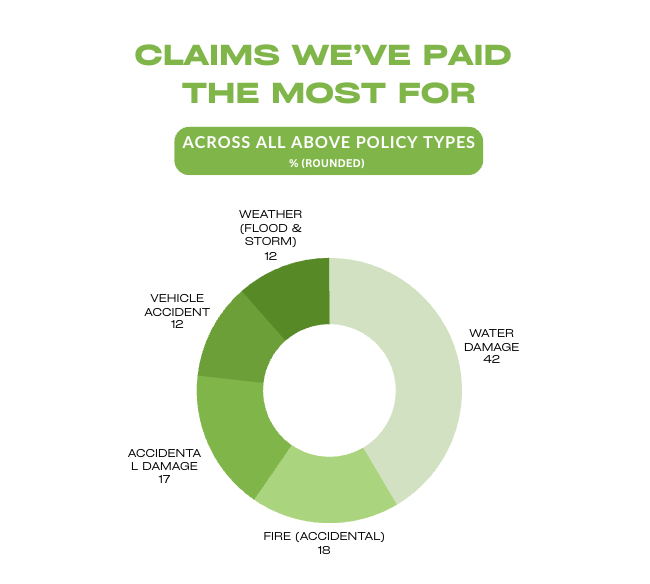

The most expensive claims across all policy types

While frequency tells one side of the story, cost paints a different picture. Here’s a look at the claims that we’ve paid out the most amount of money for this year:

Some key insights stand out when it comes to the costliest claims. Thankfully, weather-related claims have dropped a few spots this year, providing some much-needed relief.

While accidental damage was the most frequent reason for our claims, it accounts for just 10% of the total payouts – indicating many smaller, less costly incidents.

When accidental fires occur, they’re among the most financially costly claims. These events often result in extensive damage, sometimes requiring a complete rebuild of the home.

Prevention is always the best defence against accidental fires. Simple steps like never leaving candles or cooking unattended, regularly testing smoke alarms, and ensuring your electrical systems are safe can greatly reduce the risk. While the financial cost of a fire can be substantial, the threat to human lives is immeasurable.

For more information:

General insights by property type

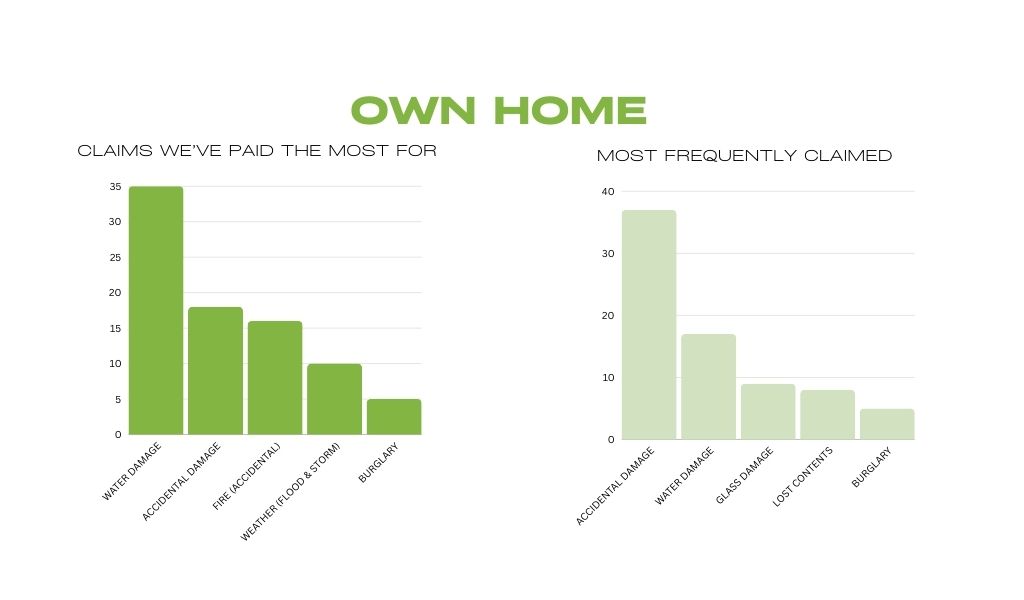

Own Home/Owner-Occupied

Weather has raised its ugly head again this year, but thankfully we’ve been spared the extreme damage experienced in 2023. Historically, summer is a season when storms and flooding can cause significant damage, so it’s a good time to take precautions to protect your property. If you’d like to learn more, check out our support articles for helpful tips and information:

Rental/Landlord

Similar to own home and holiday home insurance, water damage and accidental damage are the most common claims for rental properties. These issues often arise from the higher turnover of tenants or insufficient regular maintenance. What sets rental properties apart, however, is the added risk of loss of rent & malicious damage cover.

Learn more about these topics:

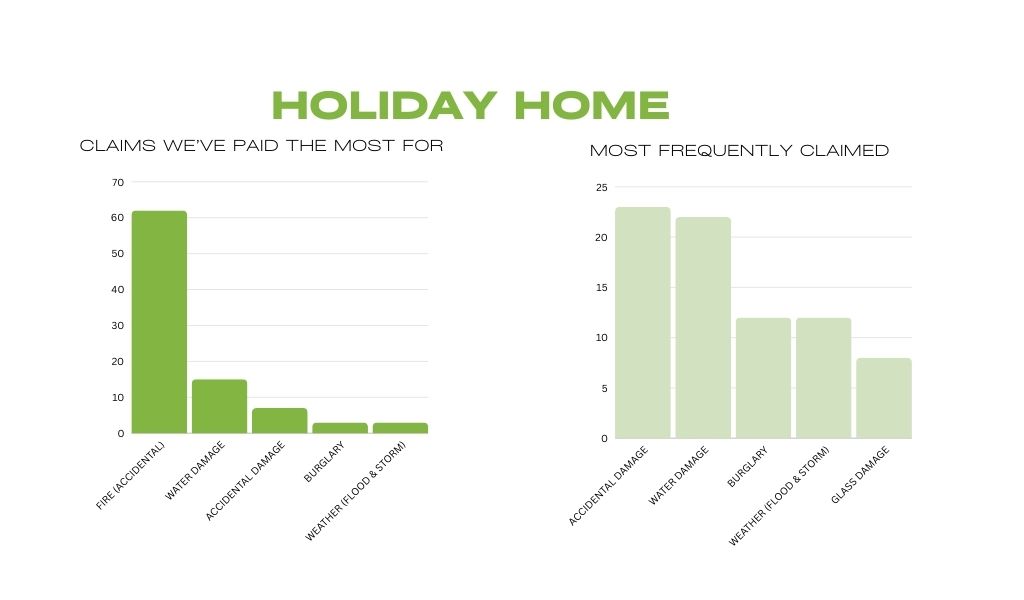

Holiday Home

After the usual suspects of accidental damage & water damage, these properties see a higher risk of burglary and weather-related claims. Being unoccupied for long stretches makes them vulnerable, particularly during storm seasons. Burglary ranks as the third most common issue. Our Holiday Home insurance basics article offers helpful tips on mitigating these risks.

For more information:

Vehicle

One of the main standouts in 2024 is glass damage – it’s the most common claim by far. These claims, while annoying and inconvenient, usually don’t cost much to fix.

When we look at the vehicle claims we’ve paid out the most for, major accident damage tops the list. The good news? The Roadside Assist portal is now available for vehicle customers who’ve added the Roadside Assist feature to their policy. If you haven’t added it yet and want to know more, you can start here.

Another common (and costly) culprit is damage from static collisions – when your car meets an immovable object.

For more information

Roadside Assist for initio vehicle customers

When we look at the vehicle claims we’ve paid out the most for, accident damage tops the list. The good news? Roadside Assist Online is now available for vehicle customers who’ve added the Roadside Assist feature to their policy. If you haven’t added it yet and want to know more, you can start here.

Another common (and costly) culprit is damage from static collisions – when your car meets an immovable object. And we hate to break it to you, but that pole you reversed into didn’t sneak up behind you.

For more information

What does this mean for you?

These trends highlight the importance of staying proactive with maintenance, securing your property, and ensuring your insurance is comprehensive enough to cover frequent and high-cost risks. As your insurance provider, we’re here to help – whether it’s providing advice on minimising risks or ensuring your cover matches your needs.

Did you find this interesting? You might also enjoy our article on the weird and wonderful claims from this past year.

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2024 (1 Dec 2023 – 27 Nov 2024), spanning our entire claims portfolio. Please note that all figures are approximate percentages, calculated to offer a representative overview of claim trends during this period. These figures only cover the most common categories. They are not an all-inclusive list and may not total 100%.

Switching your house insurance to initio is quick and easy, but timing is important to make sure you stay covered every step of the way. Here’s what to do and in what order.

1. Get your initio policy lined up first

Before you cancel your current policy, start a quote with initio. You can do this online in minutes. Once you’re happy with the cover and price, set the start date for your new policy.

- If you want your cover to roll over seamlessly, choose the day after your current policy ends.

- If your old policy ends at midnight, set your new one to start the next day, you don’t want a gap in cover.

2. Make sure the dates line up

Your current policy should stay active until your new one begins. Even a short gap could leave you without cover if something unexpected happens.

- Example: If your old policy ends on 14 June, set your initio policy to start on 15 June.

3. Sign up with initio

Once you’ve confirmed the start date, complete the sign-up online. You’ll get instant confirmation of cover and policy documents sent straight to your inbox.

4. Cancel your old insurance

When your initio policy is locked in, contact your old insurance provider to cancel your policy from the day your new cover starts. Most providers will refund the unused portion of your premium if you’ve paid in advance.

- Be prepared for them to ask for proof of your new cover (you can email them your initio confirmation).

5. Double-check everything

Before your initio policy starts, check that:

- Your start date is correct

- You’ve got confirmation that your old policy is ending on the right date

- You’ve downloaded and saved your initio policy documents

Tip: If you’re unsure about dates, start your new policy a couple of days before your old one ends — a small overlap is better than no cover.

Get a quote

Useful Links

3 News Article

http://www.3news.co.nz/Increase-in-insurance-claims-for-P-Lab-dwellings/tabid/309/articleID/198177/Default.aspx

Initio Comments:

These are certainly some alarming statistics. I agree that it is good to be proactive in identifying when your rental property may become the victim of drug manufacture; MethMinder certainly seems to be the best approach. It is important to note that not all dwelling insurance policies provide cover for drug related / illegal activities (ie P Labs). In light of this it is crucial that the landlord understands the extent of their existing insurance cover. Initio Rental Property Insurance provides comprehensive cover for this risk and it can all be done (and managed) online. Have a look for yourself.

Its been almost a year since our rental property insurance and holiday home insurance policies started converting from an open ended cover based on size to a specified replacement sum insured. A year on we continue to stress the importance of insuring rental properties and holiday homes correctly.

In the event of a major loss it is crucial that your sum insured is an accurate reflection of the actual cost to replace your property.

Just a reminder; the replacement sum insured is the amount it would cost to replace your property with modern equivalent construction materials, and should include the costs of demolition, professional fees, inflation and site improvements such as fencing, swimming pools, landscaping, retaining walls and driveways. As one could imagine this is a very difficult figure to calculate without a knowledge of materials costs and building techniques. This is why we encourage rental property insurance holders to get professional advice from a valuer or at the very least use an online replacement calculator such as Cordel: Online replacement calculator

Having fielded many queries from landlords, rental property insurance and holiday home insurance holders we have some myths to bust:

1. The government valuation (GV) has nothing to do with the replacement value of the dwelling

2. The market value or purchase price of your property has NO bearing on the replacement value.

3. Demolition and removal of debris is very expensive.

4. Building techniques and compliance are NOT the same as when your dwelling was first constructed. Local authorities may not allow you to build ‘what you had’.

Always feel free to contact us if you have any further queries. Initio online insurance is a specialist rental property insurance, landlord insurance and holiday home insurance provider.

2016 in review:

With 2016 gone and everyone returning from the beach, it is a good opportunity to reflect on the events of the past 12 months and provide an update on changes to the insurance market for 2017.

2016 saw a large rise in the prevalence of meth contamination claims and costs. This has had impacts across the entire market, and seen a lot of media attention.

The Kaikoura earthquake of 14 November also had an impact on the insurance market. Repairs are expected to cost hundreds of millions in repairs, says the Insurance Council’s Tim Grafton (read more here).

This means that insurance premiums across the board are likely to increase further as more costs to the Kaikoura earthquake are realised. Areas affected by the quake are also seeing stricter rules for cover, especially properties in the Wellington/Nelson area.

Positive changes:

While there have been some challenges, there are some positive results as well.

An agreement was reached between EQC and many private insurers (including Initio) that claims for damage caused by the Kaikoura earthquake can now be handled directly. This means that claims no longer need to go through EQC, and makes the process quicker and easier.

Further good news is that the old guidelines for meth contamination and remediation have been reviewed. The government has indicated that they will be adopting the new guidelines which have higher limits in place (MoH Summary). Ultimately, this should reduce the cost and exposure to property owners.

The government is also considering ways to deal with the Holler v Osaki issue, which saw tenants exonerated from accidental damage caused to properties. Housing Minister Nick Smith announced plans to change the law so that tenants would be liable to some extent, which should provide some relief to property owners.

With continuing changes in the property market, 2017 promises to be an interesting year.

Landlord, or Rental Property Insurance is an insurance policy that specifically covers the property owner (Landlord) for their Rental Home and some of the risks associated with being a landlord.

Owning and insuring a rental property is a bit different from owning and insuring your own home. That’s why it’s so important to get the right insurance cover in place. Initio want to be able to take care of the unknowns and the what ifs for you.

So what are the insurable risks?

To find out check out our latest article.

What is Landlord Insurance?

From 1 January 2019 the initio Homeowners insurance policy is changing. We’ve added some extra benefits, enhanced and simplified some of the existing covers, and put some restrictions on some areas. This is a summary of the good, the improvements, and the not so good.

THE GOOD:

New Benefits:

Breakage Extension

If you are only claiming for the accidental breakage of glass (windows and doors) or sanitary fixtures (such as sinks and baths) a reduced excess of $250 applies.

Electronic Programs

If your electronic equipment suffers loss or damage covered under the home section of this policy, you’re also covered for the reasonable cost of restoring, re-setting or re-programming programs, software and other coded instructions necessary to operate that equipment. There’s no cover for any data that may be stored on that equipment.

Keys and locks

The maximum amount payable during an annual period for your home’s keys and locks is $1,000. No excess applies. This limit applies across all keys and locks cover you may have under this or any other policy with NZI.

New building work

Up to $10,000 of cover is available per annual period for a new structure valued at $10,000 or less being built at the home, including any associated materials that are to be included in the new structure. Covers loss or damage caused by specified events only. Please contact us if you need separate cover for building work that falls outside of the above criteria.

Post-event inflation protection

Under the home section of this policy, up to 10% of the relevant policy limit or sum insured is available as additional cover if building costs increase due to widespread damage following a natural disaster, storm or flood.

Stress payment

If we pay a total loss claim for the home, we’ll also pay you $2,000 for stress caused by the loss. This limit applies across all stress payment cover you may have under this or any other policy with NZI.

Sustainability Upgrade

If your home is a total loss, we will pay up to $15,000 to upgrade your home with sustainable products. Examples of sustainable products include solar water heating, rainwater collection tank, and environmentally friendly paint.

Water or sewage pipe blockage

Up to $500 of cover is available per annual period towards unblocking water or sewerage pipes at the home. No excess applies.

Improvements to Existing Cover:

Carpets

Loose floor coverings (such as rugs) are defined as contents under the policy. Fitted floor coverings, including glued, smooth edge or tacked carpet and floating floors are defined as part of the home under the policy – previously only glued floor coverings were included. You may wish to check the sums insured of your home and contents are adequate, taking this change into account.

Clarification to existing cover:

Reduction and reinstatement of sums insured

Following damage to your home for which a claim is payable under the home section of this policy or by the Earthquake Commission, the sums insured are reduced from the time of the loss by the amount required to repair the loss. When payments are applied to the repair of the home, the sums insured are reinstated.

Alternative Accommodation

If your home can not be lived in due to a loss to the home, which is covered by this insurance policy or by EQC; we will pay for you and your domestic pets to stay in alternative accommodation, up to $20,000.

GST

All amounts shown are inclusive of Goods and Services Tax (GST).

Outbuildings

Cover for outbuildings used for domestic purposes now extends to outbuildings that may have limited rural lifestyle use, i.e. for the storage of tools, animal feed, uninstalled equipment or machinery and vehicles only. The outbuildings must be within the residential boundaries of the insured property.

Legal liability

Your legal liability cover has reduced to $1,000,000 for damage to another person’s property, but has been extended to cover liability for another person’s accidental death or bodily injury in connection with your home or its grounds. The limit is GST inclusive. Defence costs you incur with our prior approval are now covered on top of this. Clarification that there’s no cover for liability in connection with seepage, pollution or contamination, unless it occurs during the period of cover and is caused by a sudden and accidental event that occurs during the period of cover.

THE NOT SO GOOD:

Vacant homes

Where the home will be vacant for more than 60 days you will need to let us know or we will only pay for a loss that is caused by fire, explosion, lightning or natural disaster.

Tree disposal

Your policy no longer covers the disposal of tree debris following damage to your home or contents caused by a falling tree or part of a tree.

Landscaping

The maximum amount payable to restore your garden or lawn has reduced from $3,000 to $2,500. This payment is now in addition to any other payment under this policy. Now, cover applies only where a claim is payable for damage to the home, and the damage to the garden or lawn occurred either in the same event or during the subsequent repair of the home.

Recreational features and retaining walls

There is now a sub-limit of $45,000 for all recreational features and a sub-limit of $25,000 for all retaining walls, unless these items are specified with a higher limit as shown in the schedule. Learn more about recreational features and retaining walls.

Bridges, wells and private utility plants

The following items are covered provided they are primarily for domestic use, although they may have limited rural lifestyle use:

- Bridges, culverts, permanent fords or dams with a replacement cost of $15,000 or less

- Wells or bore holes including their pump, lining or casing with a replacement cost of $10,000 or less

- Private utility plants and associated equipment with a replacement cost of $10,000 or less.

There’s no cover for any of the above items with a higher replacement cost, unless they’re specified with a higher limit as shown in the schedule.

CONTENTS INSURANCE

Also have homeowners contents insurance?

About the changes to your contents insurance.

IMPORTANT: This is not an exhaustive or comprehensive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio home policy NZ1811

Probably not! If you have left your property uninsured and decide to insure because your property is in the path of an incoming cyclone, it’s not likely that you will be able to take out cover with the storm on it’s way.

Why you can’t just get insurance when trouble is about to happen

Think of insurance like a safety net for your property. If everyone only got this safety net when they saw trouble coming, like a big storm, it wouldn’t be fair. This is because insurance works by spreading out the cost among lots of people, over time. If some people only pay in when they think they’ll need help soon, it puts more pressure on everyone else. We figure out what to charge for insurance based on how likely it is something might go wrong. If people could only get insurance when there’s a high chance of trouble, it would change how much we’d have to charge, affecting everyone.

Why keeping your insurance going is important

We know insurance costs can go up, and there are many reasons for this, like more expensive repairs or more people needing help. This can understandably influence you into letting your cover lapse. We don’t recommend this approach as we want to be there for you in the event of a major disaster or loss. We’re working hard to make sure you still get good value and support from us and have cover when you need it.

Clearing up myths about claims

Some people think they won’t get paid when they need to make a claim, but that’s not true. We’re here to support you and have paid out a lot of claims this year. If you are unsure of what’s covered or you need any specific advice around an area of concern please check your policy documents for details and reach out to our team for assistance if needed.

To wrap up, it’s really important to keep your insurance going without breaks. It ensures your peace of mind and provides support for you and others, especially when facing significant events. If you have questions or need help with your insurance, feel free to get in touch with us at initio.

Other articles of interest

Other resources

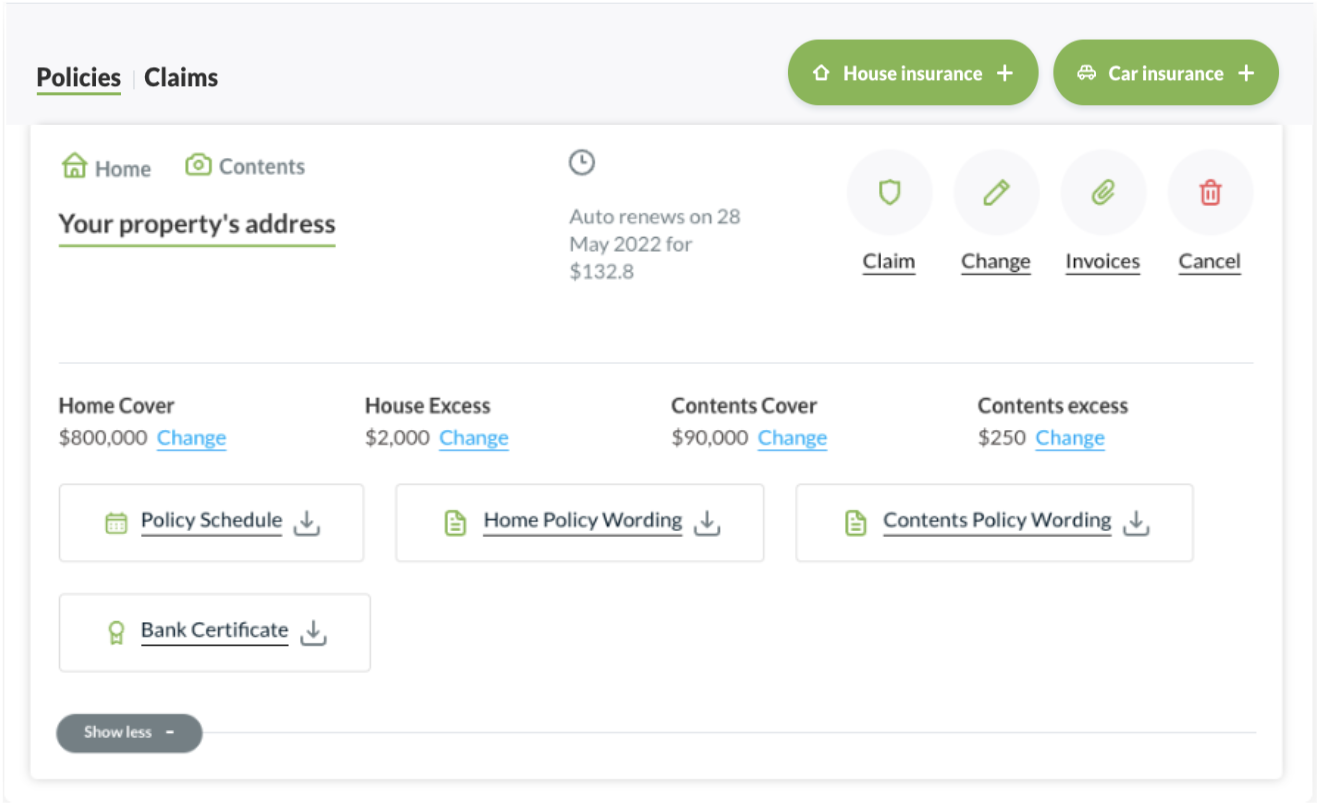

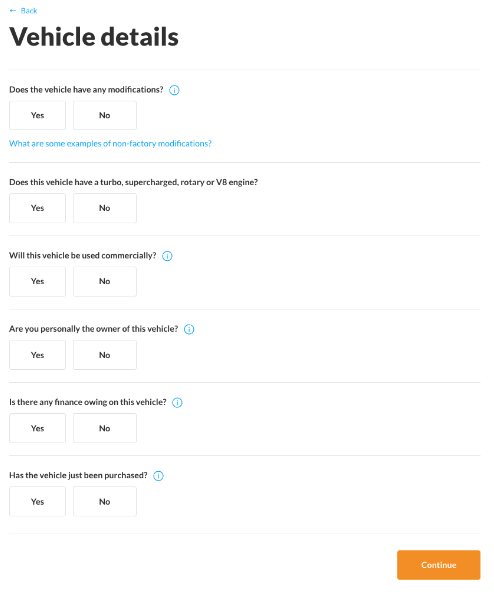

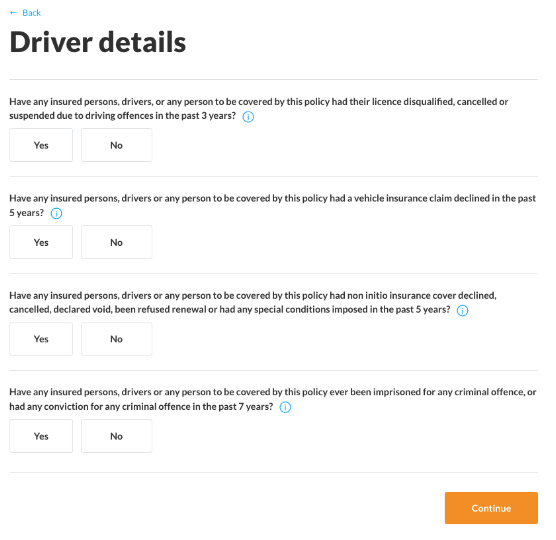

So you have just insured your property with us. Awesome! But you are wondering how to add insurance for your vehicle? This guide will walk you through the essential steps: getting a quote, customising your cover, disclosing necessary information, and making your payment.

1. Get an instant quote

When you purchased your insurance policy for your property, you would’ve been introduced to your initio dashboard. Within a few moments of your home product purchase, we would have provided you with login information for your initio dashboard. You will need to login to your dashboard to begin the process of getting vehicle insurance. This is because we only offer vehicle insurance to customers who have a property insured with initio.

Simply click on the green “Car Insurance +” button, which takes you to a page asking for your vehicle registration number.

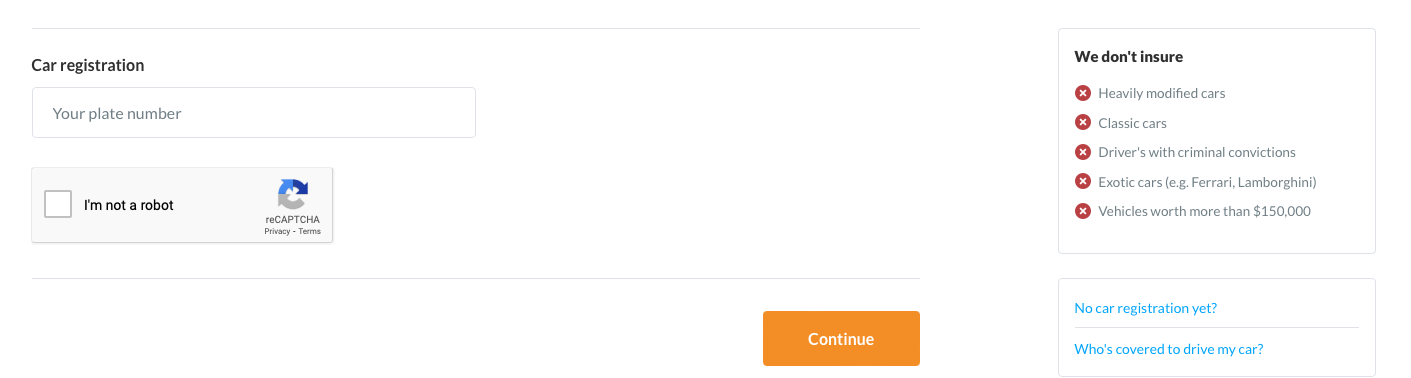

2. Get a quote

Enter your vehicle’s registration number to continue. If you have a brand new vehicle that has not been registered yet; email our team, they can assist you further.

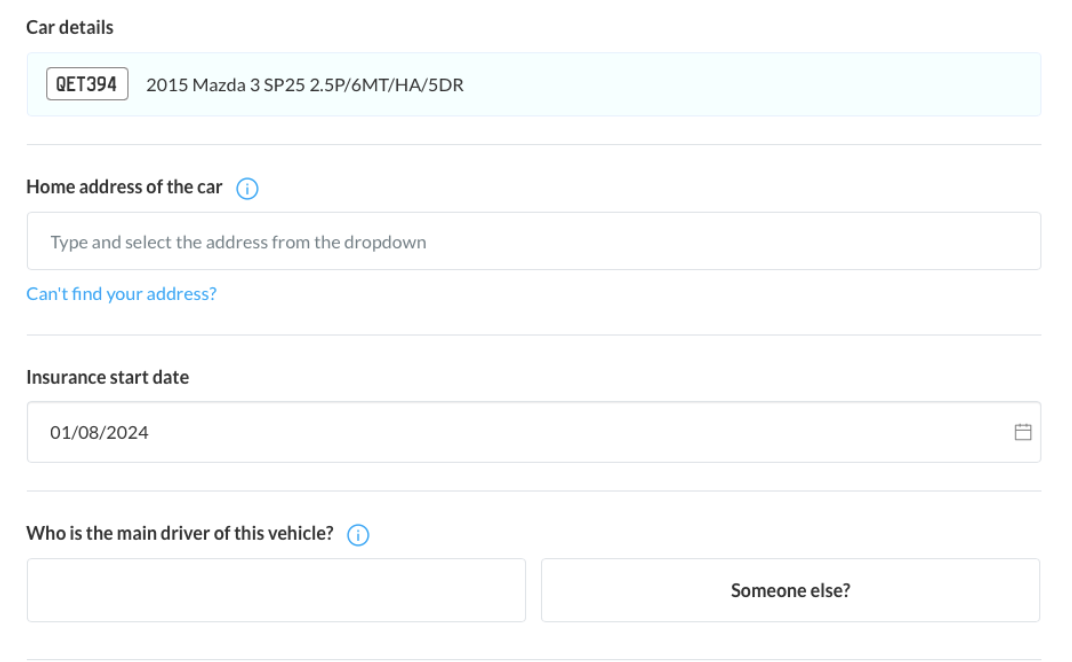

3. Enter your details

Enter the details above to proceed to the next step. This information helps us understand where the car will be parked overnight and during the day, who the main driver is, and when you’d like the insurance to start.

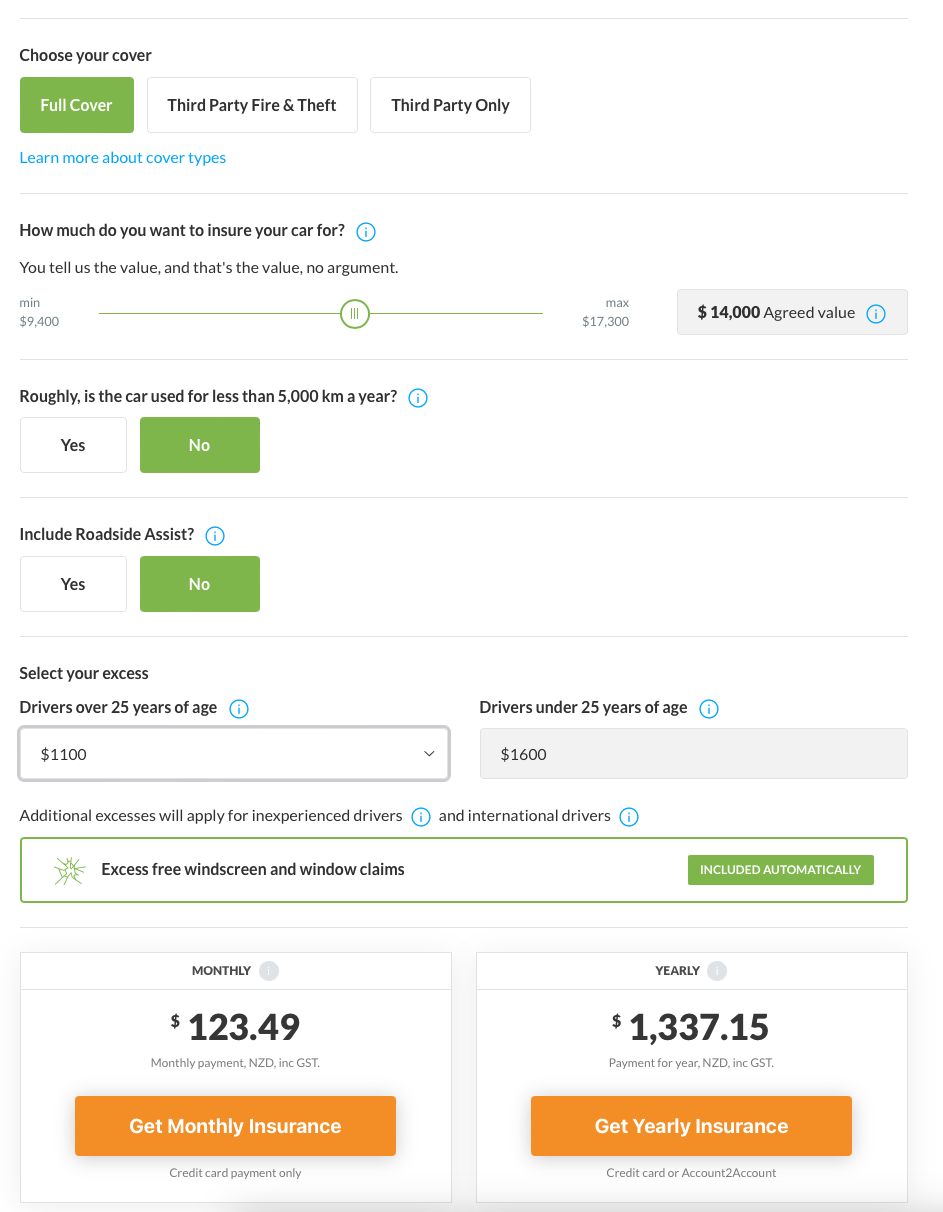

4. Select vehicle cover, customise quote & select payment option

For our vehicle insurance, we offer the following which include different policy extensions and exclusions:

- Comprehensive Full Cover

- Third Party – Fire & Theft

- Third Party Only

5. Enter vehicle details

6. Complete driver details

7. Sign the application form

To sign the application form, use your device keyboard to type your name in full (as the person completing the form) in the space provided.

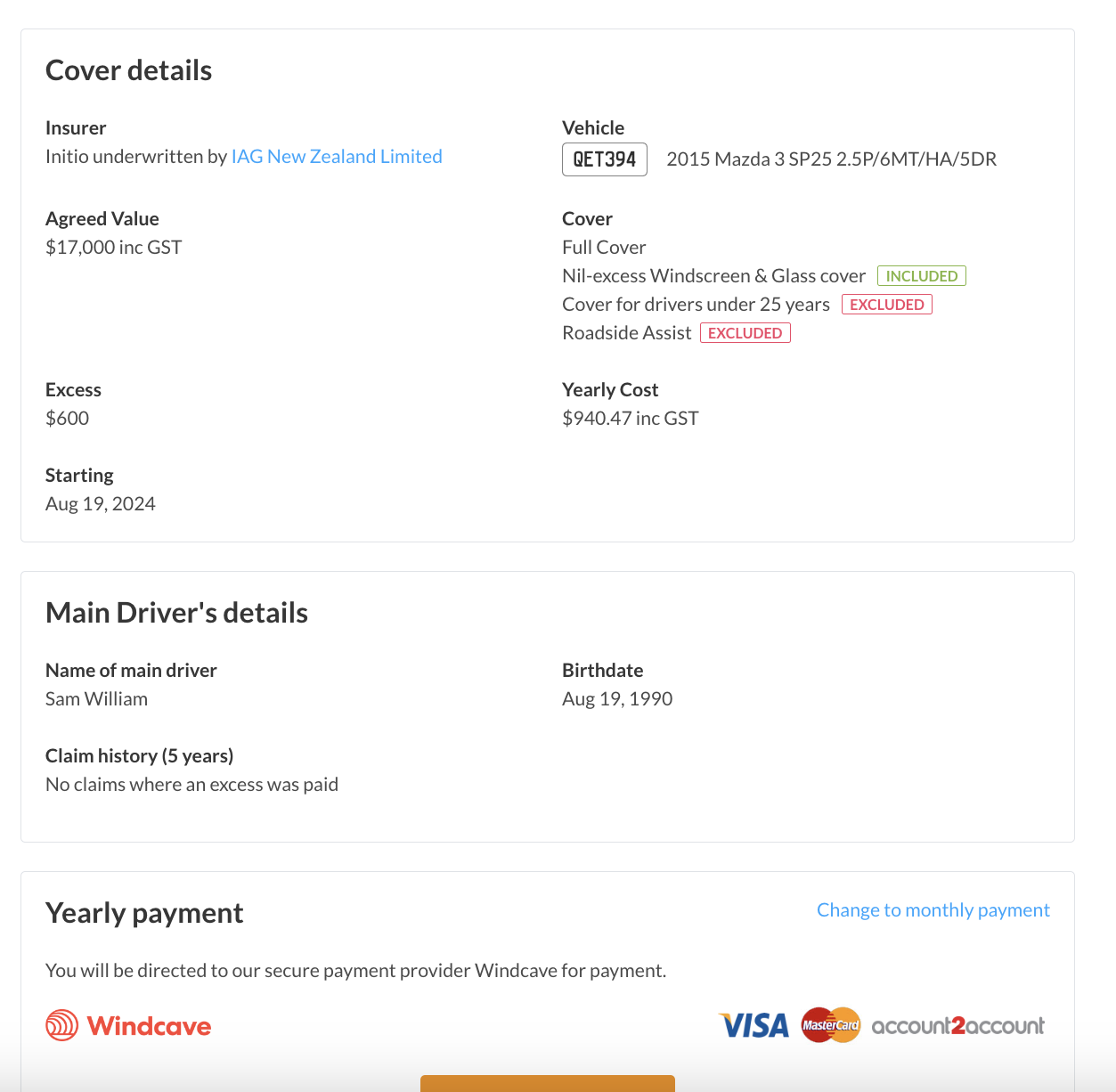

8. Review and make payment

Once you have customised your insurance policy, you will need to select a payment option. For more information regarding our payment options, please refer to our support page, here.

There you have it! We will instantly email your confirmation documents.

Useful links

(just ask our team)

We’re stoked to share that initio has been named one of the Top Insurance Employers of 2025 in Australia and New Zealand. This recognition is awarded by Insurance Business to the best insurance providers to work for, and we made the cut in the “less than 100 employees” category.

It’s a bit of a big deal. Mostly because it’s based on what our people think, not just what we say in job ads or onboarding packs.

So, how do you win?

It wasn’t just about who has the best snacks (although, shout out to our endless supply of choccy biscuits). The process involved our team anonymously rating initio across things like:

- Company culture

- Flexibility and autonomy

- Personal and professional development

- Genuine inclusion and wellbeing

- Whether people feel heard (and whether it actually leads to change)

Long story short: if you don’t walk the talk, you don’t make the list.

What this means for us

We’ve always believed that doing great work starts with enjoying where you work. That doesn’t mean ping pong tables and bean bags, it means feeling trusted, supported, and free to be yourself. It means flexibility that actually flexes. And it means being able to grow without having to shout for attention.

The fact that our team rated us so highly means the world. We’re not perfect (we’re still figuring out how to keep the office plants alive), but we’re committed to making initio a workplace that’s safe, empowering, and – dare we say it – fun.

Why it matters

At the end of the day, great insurance isn’t just about technology or pricing, it’s about people. People who care about customers, push boundaries, and back each other every day. That starts with culture. So this award isn’t just a nice badge, it’s a reflection of what we’ve built together.

Thanks to our team for making initio what it is. Let’s keep doing it differently.

Related articles

Meet some of our team

Navigating the intricacies of insuring a home with an attached flat in New Zealand, especially one that is rented out part-time, can be overwhelming for landlords and property investors. At Initio, we are dedicated to helping you make sense of these complexities, equipping you with the tools needed to make the right insurance choices for your unique situation. This article is specifically designed to assist you in understanding the process for homes with attached flats rented out occasionally.

Guidelines on Insuring Your Home and Attached Flat in NZ

If you happen to own a home with an attached flat rented out occasionally, you may find yourself unsure about how to secure the right insurance coverage. This situation differs from one where both units are exclusively used as long-term rentals (which are catered for by our multi-unit policy). Insuring a property where you live and have an attached flat rented out part-time necessitates a more nuanced approach.

Here’s what you need to know:

- Own Home policy: This policy has been crafted to cover the portion of the property that you inhabit.

- Landlord/Rental policy: This policy needs to be put in place to provide coverage for the attached flat when it’s rented out. Even if the rental isn’t full-time, coverage for the times when the flat is tenanted is ensured by the landlord/rental policy.

Should a significant claim arise, both policies would be engaged, with the combined sum insured being applicable to the whole property.

Why do I need Two Policies?

Each policy is designed specifically to cover one self-contained home/unit only and for the risks associated with the type of occupancy. The Own Home policy provides coverage for the main house/unit where you live, while the Landlord/Rental policy covers your rental home/unit including the legal liabilities and other specific risks associated with renting.

Conclusion

The process of insuring a home with an attached flat, rented out on occasion, needn’t be a difficult one. With an understanding of how Initio’s insurance products can be strategically combined, comprehensive protection of your property is ensured. Additional information on this topic, as well as other insurance solutions offered by Initio, can be found here.

Get a quote

Useful links

Can I insure my boat with initio?

No, we do not provide boat and/or marine insurance products.

Can I insure my motorcycle with initio?

No, we do not provide motorcycle insurance.

Can I change my payments from monthly to annual at renewal?

If you wish to change from monthly to annual (yearly), please take out a new annual policy from your initio dashboard and then cancel the original monthly policy. The system will also automatically arrange a refund for any unused portion of the monthly policy.

If I’m going to rent out one of the rooms in the house I live, do I need to get a landlord insurance policy?

If the boarder/tenant will be sharing facilities with you, such as kitchen and/or bathroom, then you will not need a separate policy. Our “Own Home, that’s also rented” will suit that purpose.

If the area they will be living in is self-contained (either attached to or separate from the main dwelling) with it’s own facilities, to the extent that they don’t share rooms/areas with you, then you will need to take out an additional landlord policy for that part of the property. That policy would be in addition to your Own Home policy for the portion of the home that you occupy. Together, both policies should make up the total sum insured required over the whole property.

Can I pay for one or some of my policies using a different credit card?

If you are purchasing annual insurance, you can use a different card for each and every purchase. If you are purchasing monthly insurance, we are only currently able to facilitate one card for any monthly payments under your account. If you wish to use a different card for a monthly policy, you will need to set up a new initio account using an alternative email address for any policy to be paid via the new card.

How do I login?

If you are a current policy holder already with initio you will have an initio dashboard where you can manage your insurances. You will have been emailed your login details following your first purchase with initio. Please login to your initio account here.

Your email is the first login credential required, followed by your password. If you can’t recall the email you used when you purchased your policy, please contact initio staff.

If you’ve forgotten your password, click the “Forgot my password” option to reset it. Simply follow the instructions to complete the process.

Please note that logins are only provided upon purchase of a home policy with initio.

Where do I find my renewal invoice to pay?

We don’t send invoices for the upcoming year in the traditional sense, if you are looking for the cost to renew your annual policy for the upcoming year, you can find that information by using the “review & confirm” button on the relevant policy. More information regarding that can be found here.

Once the renewal has been completed and paid, the paid invoice information is immediately emailed to you and is thereafter available on your initio dashboard for viewing. All of your historical Invoices/Receipts will remain available via your initio dashboard.

How do I determine the amount of replacement cover to take for my home? Does the amount of replacement cover includes demolition costs?

Please refer to our support page here for your home and here for your contents.

Which cover should I choose to insure my rental?

To insure a rental property set up as one self contained dwelling that you lease to tenants on a long term residential lease, please use our Landlord policy. We also have a multi-unit landlord cover for small blocks of flats or if you own more than one connected rental unit.

If I hire a car, does my vehicle policy insure the hired car?

No, your initio policy does not cover the hire vehicle, we recommend arranging cover with the hire company.

With Winter well and truly upon us, the heaters have come out. Not surprisingly most residential house fires occur during winter. Kitchen fires make up about a quarter of all house fires – they commonly start from unattended cooking and can quickly spread. As a landlord there are steps you can take to improve the safety of your tenants and home against fire:

- Consider removing curtains from kitchen windows as these provide an excellent fuel source for fire.

- Recommend tenants use camping type gas cookers outside only. When used indoors, these are both a fire hazard and health risk.

- Test smoke alarms at each property inspection. If tenants are removing the batteries considering replacing with a newer model that has a 10 year sealed battery and hush button.

- To reduce the risk of electrical fires, check power points for overloading. Where necessary consider installing additional power points. Faulty power boards are a common cause of fire.

- If your house has downlights installed prior to 2012, check that the ceiling insulation has the correct spacing around the lights to prevent overheating and fire.

- Consider installing safe and efficient heating sources. Tenants may even be happy to pay more rent in exchange for installing a heat pump.

- Clean chimney flues annually and make sure heat pumps are serviced and cleaned regularly to prevent fires and ensure heating sources are operating efficiently.

From 1 January 2019 the initio Rental Property insurance policy is changing. We’ve added some extra benefits, enhanced and simplified some of the existing covers, and put some restrictions on some areas. This is a summary of the good, the improvements, and the not so good.

THE GOOD:

New cover benefits

New building work

Up to $10,000 of cover is available per annual period for a new structure valued at $10,000 or less being built at the home, including any associated materials that are to be included in the new structure. Covers loss or damage caused by specified events only. Please contact us if you need separate cover for building work that falls outside of the above criteria.

Post-event inflation protection

Under the home section of this policy, up to 10% of the relevant policy limit or sum insured is available as additional cover if building costs increase due to widespread damage following a natural disaster, storm or flood.

Stress payment

If we pay a total loss claim for the home, we’ll also pay you $1,000 for stress caused by the loss.

Water or sewage pipe blockage

Up to $1,000 of cover is available per annual period towards unblocking water or sewerage pipes at the home. No excess applies.

Electronic Programs

If your electronic equipment suffers loss or damage covered under the home section of this policy, you’re also covered for the reasonable cost of restoring, re-setting or re-programming programs, software and other coded instructions necessary to operate that equipment. There’s no cover for any data that may be stored on that equipment.

Keys and locks

The maximum amount payable during an annual period for your home’s keys and locks is $1,000. No excess applies.

Improvements to existing cover:

Vacant homes

Where the home has been vacant for more than 60 consecutive days we continue to provide insurance cover but with a higher than standard excess ($5,000). If you have an active, professionally-installed alarm, the excess reduces from $5,000 to $1,000. Under the old policy the alarm excess was $2,500.

Landlord’s protection

Additional Benefits for landlords (in addition to existing benefits for malicious damage):

- Loss of rent due to non-payment of rent because of prevention of access or failure of public facilities, up to 6 weeks’ rent

- Loss of rent due to the tenant vacating the property without notice, up to 6 weeks’ rent

- Loss of rent due to eviction for non-payment of rent, up to 6 weeks’ rent.

The excess has changed from minimum $500 to the standard policy excess.

Learn more about landlords protection here

Simplified cover for contents

Landlords contents is automatically included under the policy ($20,000 of cover for free). you have the choice of increasing this cover up to $60,000. The policy is designed to cover things like ovens, curtains, drapes. Under the old wording these items were covered for their present day value. The cover has been improved so we’ll now either pay:

- to replace the item if it’s under 5 years of age, or

- the present value of the item if it’s 5 years of age or over, or

- to repair the item as close as possible to the condition it was in before the loss or damage.

learn more about contents cover for rental properties here

Legal liability

Your legal liability cover of up to $2,000,000 for damage to another person’s property is extended to cover liability for another person’s accidental death or bodily injury in connection with your home or its grounds. The limit is now GST inclusive. Defence costs you incur with our prior approval are now covered on top of this. Clarification that there’s no cover for liability in connection with seepage, pollution or contamination, unless it occurs during the period of cover and is caused by a sudden and accidental event that occurs during the period of cover.

Carpets

Fitted floor coverings, including glued, smooth edge or tacked carpet and floating floors are defined as part of the home under the policy and now covered for replacement (new for old).

Clarification to existing cover:

Reduction and reinstatement of sums insured

Following damage to your home for which a claim is payable under the home section of this policy or by the Earthquake Commission, the sums insured are reduced from the time of the loss by the amount required to repair the loss. When payments are applied to the repair of the home, the sums insured are reinstated.

GST

All amounts shown are inclusive of Goods and Services Tax (GST).

Outbuildings

Cover for outbuildings used for domestic purposes now extends to outbuildings that may have limited rural lifestyle use, i.e. for the storage of tools, animal feed, uninstalled equipment or machinery and vehicles only.

THE NOT SO GOOD:

Tree disposal

Your policy no longer covers the disposal of tree debris following damage to your home or contents caused by a falling tree or part of a tree.

Landscaping

The maximum amount payable to restore your garden or lawn has reduced from $3,000 to $2,500. Cover applies only where a claim is payable for damage to the home and the landscaping damage occurred during the same event.

Recreational features and retaining walls

There is now a sub-limit of $45,000 for all recreational features (tennis courts, pools etc) and a sub-limit of $25,000 for all retaining walls, unless these items are specified with a higher limit as shown in your schedule. More details here

Methamphetamine contamination

We continue to provide cover for meth however the maximum amount payable for cleaning or repairing the house and its contents damaged by methamphetamine contamination (manufacture and consumption) has reduced from the house sum insured to the amount shown in the schedule, currently $30,000. An excess of $2,500 applies to each claim. There are additional conditions and limitations for tenancies or occupancies of 90 days or less. Learn more about meth here

Landlord’s obligations

This section outlines the increased standard of care that is now required of landlords. To make a valid claim on a tenanted property, you’ll need to have fulfilled these obligations.

The inspection and monitoring requirements must be met from when your policy renews. The updated tenant-vetting requirements will only apply to new tenancies that commence after your policy renews, not to your existing tenants.

You’ll also need to test for methamphetamine contamination before and after each tenancy, in order to be covered for methamphetamine contamination-related liability as a landlord. Learn more about landlord obligations here

IMPORTANT: This is not an exhaustive or comprehensive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio landlord and holiday home policy NZ1811

From 1 January 2019 the initio Rental Property insurance policy is changing. We’ve added some extra benefits, enhanced and simplified some of the existing covers, and put some restrictions on some areas. This is a summary of the good, the improvements, and the not so good.

THE GOOD:

New cover benefits

New building work

Up to $10,000 of cover is available per annual period for a new structure valued at $10,000 or less being built at the home, including any associated materials that are to be included in the new structure. Covers loss or damage caused by specified events only. Please contact us if you need separate cover for building work that falls outside of the above criteria.

Post-event inflation protection

Under the home section of this policy, up to 10% of the relevant policy limit or sum insured is available as additional cover if building costs increase due to widespread damage following a natural disaster, storm or flood.

Stress payment

If we pay a total loss claim for the home, we’ll also pay you $1,000 for stress caused by the loss.

Water or sewage pipe blockage

Up to $1,000 of cover is available per annual period towards unblocking water or sewerage pipes at the home. No excess applies.

Electronic Programs

If your electronic equipment suffers loss or damage covered under the home section of this policy, you’re also covered for the reasonable cost of restoring, re-setting or re-programming programs, software and other coded instructions necessary to operate that equipment. There’s no cover for any data that may be stored on that equipment.

Keys and locks

The maximum amount payable during an annual period for your home’s keys and locks is $1,000. No excess applies.

Improvements to existing cover:

Vacant homes

Where the home has been vacant for more than 60 consecutive days we continue to provide insurance cover but with a higher than standard excess ($5,000). If you have an active, professionally-installed alarm, the excess reduces from $5,000 to $1,000. Under the old policy the alarm excess was $2,500.

Landlord’s protection

Additional Benefits for landlords (in addition to existing benefits for malicious damage):

- Loss of rent due to non-payment of rent because of prevention of access or failure of public facilities, up to 6 weeks’ rent

- Loss of rent due to the tenant vacating the property without notice, up to 6 weeks’ rent

- Loss of rent due to eviction for non-payment of rent, up to 6 weeks’ rent.

The excess has changed from minimum $500 to the standard policy excess.

Learn more about landlords protection here

Simplified cover for contents

Landlords contents is automatically included under the policy ($20,000 of cover for free). you have the choice of increasing this cover up to $60,000. The policy is designed to cover things like ovens, curtains, drapes. Under the old wording these items were covered for their present day value. The cover has been improved so we’ll now either pay:

- to replace the item if it’s under 5 years of age, or

- the present value of the item if it’s 5 years of age or over, or

- to repair the item as close as possible to the condition it was in before the loss or damage.

IMPORTANT: For multi-units the contents sum insured you choose is shared across all units and is not a per unit contents cover. For example if you have 3 units insured and have selected $40,000 landlords contents cover – in the event of a total loss fire the $40,000 is the total amount of landlords contents cover.

learn more about contents cover for rental properties here

Legal liability

Your legal liability cover of up to $2,000,000 for damage to another person’s property is extended to cover liability for another person’s accidental death or bodily injury in connection with your home or its grounds. The limit is now GST inclusive. Defence costs you incur with our prior approval are now covered on top of this. Clarification that there’s no cover for liability in connection with seepage, pollution or contamination, unless it occurs during the period of cover and is caused by a sudden and accidental event that occurs during the period of cover.

Carpets

Fitted floor coverings, including glued, smooth edge or tacked carpet and floating floors are defined as part of the home under the policy and now covered for replacement (new for old).

Clarification to existing cover:

Reduction and reinstatement of sums insured

Following damage to your home for which a claim is payable under the home section of this policy or by the Earthquake Commission, the sums insured are reduced from the time of the loss by the amount required to repair the loss. When payments are applied to the repair of the home, the sums insured are reinstated.

GST

All amounts shown are inclusive of Goods and Services Tax (GST).

Outbuildings

Cover for outbuildings used for domestic purposes now extends to outbuildings that may have limited rural lifestyle use, i.e. for the storage of tools, animal feed, uninstalled equipment or machinery and vehicles only.

THE NOT SO GOOD:

Tree disposal

Your policy no longer covers the disposal of tree debris following damage to your home or contents caused by a falling tree or part of a tree.

Landscaping

The maximum amount payable to restore your garden or lawn has reduced from $3,000 to $2,500. Cover applies only where a claim is payable for damage to the home and the landscaping damage occurred during the same event.

Recreational features and retaining walls

There is now a sub-limit of $45,000 for all recreational features (tennis courts, pools etc) and a sub-limit of $25,000 for all retaining walls, unless these items are specified with a higher limit as shown in your schedule. More details here

Methamphetamine contamination

We continue to provide cover for meth however the maximum amount payable for cleaning or repairing the house and its contents damaged by methamphetamine contamination (manufacture and consumption) has reduced from the house sum insured to the amount shown in the schedule, currently $30,000. An excess of $2,500 applies to each claim. There are additional conditions and limitations for tenancies or occupancies of 90 days or less. Learn more about meth here

Landlord’s obligations

This section outlines the increased standard of care that is now required of landlords. To make a valid claim on a tenanted property, you’ll need to have fulfilled these obligations.

The inspection and monitoring requirements must be met from when your policy renews. The updated tenant-vetting requirements will only apply to new tenancies that commence after your policy renews, not to your existing tenants.

You’ll also need to test for methamphetamine contamination before and after each tenancy, in order to be covered for methamphetamine contamination-related liability as a landlord. Learn more about landlord obligations here

This is not an exhaustive or comprehensive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio landlord and holiday home policy NZ1811

How do I get a quote with initio?

Getting a house insurance quote with initio is quick and simple. Just pop your property address into our quick quote tool and we’ll do the heavy lifting for you. You’ll see your premium instantly and can customise your cover to suit your needs.

When you’re ready, choose either annual or monthly payments and follow the prompts to buy online – no paperwork, no waiting.

For more details, check out our step-by-step guide to buying your first house insurance policy.

What information do I need to get a house insurance quote?

Most of the time, all you need is your property address, and our quick quote tool will pull in the important details. You might just need to answer a few simple questions, including:

- Approximate house size (no exact measurements needed)

- Estimated rebuild cost (your “sum insured”)

- Age of the home

- The date you want cover to start

Not sure about your rebuild cost? Our quote tool links to the Cordell SumSure Calculator, which helps you estimate it. You can also read our guide to choosing your sum insured for more details.

How fast can you really get a quote?

This short demo puts our quote tool through its paces to show how fast and easy it is to use.

How do I log in?

If you already have a policy with initio, you’ll have access to your dashboard to manage your insurance. Login details are emailed to you when you buy your policy. Login here

To log in:

- Enter the email address you used when purchasing your policy.

- Enter your password.

- If you’ve forgotten your password, click Forgot my password and follow the steps.

If you’re not sure which email you used, contact our team, we can help.

Logins are only provided once you’ve purchased a home policy with initio.

Calculate your sum insured

Related articles

Double whammy on levies

Did you know that a large portion of your house insurance premium goes to the government in levies? For the average initio house insurance policy sold through our site www.initio.co.nz, over a THIRD of the cost to the home owner is levies…… and unfortunately that proportion is about to jump significantly with fire service levies increasing by 40% from 1 July 2017 and earthquake commission levies increasing by 33% from 1 November 2017, which will mean total levies will then make up almost HALF of the cost of an average initio house insurance policy.

While levies are perceived as a bad thing, because they hit each of us in the pocket, it is important to take account of the fact that the fund essential community necessities such as the New Zealand Fire Service, many of which are volunteer fire brigades in smaller communities. These brigades require specialized trucks and machinery to attend fires and accidents of all types. So as the running costs increase, so too do the levies.

The good news is that the team at initio continue to work hard to keep the actual insurance premium down so that home and rental property owners can enjoy some of the best value cover around.

Initio keeps premiums down by making the process of insurance simple, and its online. Get a quick quote in seconds and get covered in a little more…. ‘no death by a thousand cuts’ paperwork or long winded phone calls. Unfortunately, we just can’t do anything about the levies.

Want to check over the full details of your cover? It’s best to read your policy wording. You should also check your summary policy schedule from your dashboard to see what applies to your cover.

If you’re not sure what everything means, our guide on how to read an insurance policy walks you through each section in a simple, easy-to-follow way.

Owner-occupied Homes

See our full house insurance policy wording below. If you’ve included contents with your cover, download the separate contents insurance wording.

Download House Wording Download Contents Wording

Rental properties (including multi-units) and Holiday homes

Our holiday home and landlord cover are both under the below combined policy wording. To see what applies to your policy, it pays to check your policy schedule.

Download Landlord Wording

Car Insurance

See all the details of our comprehensive car insurance cover below.

Download Car Wording

If you have any questions about your cover, feel free to get in touch with our friendly team.

Related articles

Rental properties generate income and grow in value over time, but they can also come with unique risks and costs.

One common question for landlords is, “What damage is most likely to occur at my rental property?” Knowing the risks and how to reduce them is key to protecting your investment.

A shift in claim trends: weather makes its mark

In 2023 we experienced exceptional circumstances, notably the Auckland Anniversary storms and Cyclone Gabrielle. Our, and industry, data shows a 10x increase in weather-related claims in the past year. Damage from floods and rain saw a substantial rise in claim payouts compared to 2022, while wind and storm-related claims also showed a notable increase.

Now, more than ever, natural hazard risks such as flood susceptibility, land stability, coastal surge and slope failure (all of which are being identified by local councils) are key to determining a property’s insurability. For existing properties, and for those you intend to purchase, it is essential that you do your research and this could affect future costs, and even saleability.

Outside of natural hazards, other risks still exist, and focusing solely on weather-related issues might leave you unprepared for other landlord challenges.

A closer look at 2023 rental property losses

Flood & rain damage:

For initio in 2022, this category of damage represented 9% of the total number of claims lodged. However, in 2023, this has increased to 21% of the total number of claims. This underscores the substantial financial impact of flood and rain events. The damage to rental properties ranged from minor ceiling leaks to total destruction of the property.

Wind & storm damage:

Unsurprisingly payouts rose by just over 50% compared to the previous year. While the number of claims lodged was similar between the two years, the severity and cost of damage was significantly higher, partly due to rising construction costs.

Other water-related damage:

These are typically problems like bursting pipes and leaking hot water cylinders. In 2022, these made up 22% of claims lodged, dropping to 16% in 2023. The most common water damage claim in both 2022 and 2023 is hidden gradual water damage (HGWD), such as pipes leaking under the kitchen sink, and blocked sewage pipes. HGWD is often excluded from standard rental property insurance policies, but some policies like initio’s offer limited cover (usually $2,000 – $3,000) through a special extension. The key to proactively managing this risk is regular property inspections and educating tenants to notify as soon as they see something damp.

Accidental damage:

We’ve seen a wide range of claims in this category. These usually include unexpected incidents like broken windows, damaged cooktops and carpet stains. Accidental damage made up 13% of claims lodged in the 2023 period. Not every accidental damage loss allows the landlord to hold the tenant responsible for the insurance excess. Understanding where your responsibility as a landlord ends and the tenant’s begins will guide your communications with tenants following any damage.

Other rental property incidents (by number of claims, not value):

- Malicious damage from tenants (3.8%)

- Fire (accidental and arson combined) (1.8%).

- Meth contamination (1.7%)

- Problems with keys and locks (2.7%)

- Impact damage, typically involving vehicles (2.5%). Eg, car versus garage.

While fire is a relatively rare type of loss, its severity is substantial when it does occur. The average value of a fire claim in 2023 is just over $50,000.

Loss of rent:

Loss of rent applies when damage occurs and the house can no longer be lived in. The floods in early 2023 displaced many tenants, resulting in loss of rent payments to landlords. During the floods insurers needed to be practical and work with landlords in situations where the property was partially damaged and still able to be lived in.

In situations where a tenant can no longer reside at the property due to an event like a fire or flood, the tenant must pay for their own relocation and temporary accommodation. It is not your responsibility as a landlord. If a tenant has their own contents insurance this will usually cover these displacement costs.

Some policies, like initio’s, also cover rent in scenarios where there is no physical damage to the house. So this includes eviction or tenant abandonment. These situations made up 2.7% of total claims lodged in the past year.

Final word

Taking a proactive and sensible approach to managing risks as a landlord is its own kind of insurance. From what we observe in daily claim reports, landlords who prioritise choosing the right tenants, conducting thorough tenant checks, carrying out regular property inspections, installing fire extinguishers in kitchens, and keeping up with routine maintenance such as clearing gutters, plumbing and electrical work, have fewer damage issues and don’t add to the above statistics.

Selecting an insurance provider well-versed in landlord risk and that offers tailored policies for rental property owners complements a comprehensive strategy to reduce the risks you face as a landlord.

The statistics presented in this article are based on analysis of claims data from initio. The annual period being October to October. Please note that all figures are rounded and in some cases, where the claim type is embedded within a larger loss type, have been calculated to provide a representative view of the claim trends during this period. Data from the Insurance Council of New Zealand was also utilised.

Paying your premium with initio is simple and hassle-free.

Monthly payments can be made using Visa or Mastercard (credit or debit). Annual policies have the additional options of online EFTPOS and Account2Account transfers for easy, secure bank payments.

Please note, initio does not currently offer direct debit OR manual transfers via your banking app or bank website. Our staff will therefore not be able to provide you with bank account information. Payment options are strictly limited to those outlined below.

Payment Frequency – We have options to pay either annually or monthly

Payment is required immediately upon the purchase of any policy. You can choose to either pay annually or monthly at that time. We do not offer other frequencies or payment terms. Paying the annual premium up front is more cost effective, this can be seen in the quoted amounts. Depending upon whether you are paying annually or monthly the following methods of payment are available;

Credit or Mastercard/Visa Debit Card (Monthly or Annual Policies)

Payment can be made online using your credit/visa debit card. We accept both Visa and Mastercard, including credit and visa debit cards.

- Monthly policies automatically renew and charge your card on the same day of each month.

- On an annual payment you purchase a years worth of insurance upfront (that you can cancel at anytime and get a refund for the un-used portion). Each year we will remind you when your policy is up for renewal and you will need to login to your dashboard to renew and pay for your policy

- There is no credit card fee applied to your insurance purchase.

Common Queries for Card Transactions

- Can I change from monthly to annual payments after I’ve started my cover? If you would like to change from a monthly renewing policy to an annual renewing policy you will need to set up a new quote from your dashboard and select the “pay annually” option before continuing to fill out your property details again. Unfortunately we cannot switch a monthly policy to an annual policy any other way at this time. After you have set up a new annual policy we can cancel your initial monthly policy and issue you a refund of any overpaid premium.

- Can I pay with American Express? No, we do not currently have an option for payment via American Express cards

- Do you charge a credit card fee? No, we do not.

- What if I need to change the card used for my monthly payments? This can be changed at anytime via your initio dashboard, please login, proceed to ‘account’ in the top right hand corner and then select ‘credit card’ to update.

- My monthly payment didn’t go through this month, how can I fix it? You can arrange for the payment to be re-tried by either contacting our support team, or updating your credit card details in your initio dashboard. When card details are updated, the system will automatically try to process any outstanding payment—even if you re-enter the same card details.

Account2Account Transfer (annual policies only)

An additional option is provided for annual policies where you can use your bank account login details to load an automatic transfer payment from your selected account using the Account2Account service. “Account2Account” is an online facility which processes payments directly from your account in real time, it creates a one-off online payment utilising the online banking system. The payment is set up via our policy purchase system, please choose the Account2Account option when you come to the initio payment screen.

To use Account2Account, your banking account must be with one of the following banks:

- ANZ

- ASB

- BNZ

- Kiwibank

- The Co-operative Bank

- TSB

- Westpac

For a demo and/or further information of how Account2Account transfers work, please see here.

Online EFTPOS (annual policies only)

Online EFTPOS is a modern payment method that lets you make online purchases through your bank’s mobile app. This secure payment solution connects directly to your bank account without requiring you to share sensitive banking details. Currently available to ANZ, ASB, BNZ, The Co-operative Bank and Westpac customers.

How to make a payment

-

- Choose your bank from the payment options

- Enter your mobile phone number

- Open your bank’s app and approve the payment notification

Key benefits

-

- Direct account-to-account transfers

- No need to share banking credentials

- Secure payment process

- Simple smartphone-based payments

Frequently asked questions

How secure is Online EFTPOS?

Online EFTPOS is one of the most secure payment methods available today. This is because it doesn’t ask you to enter your bank or payment details directly. Instead, you approve each payment through your bank’s app, adding an extra layer of security.

What is the maximum purchase limit for Online EFTPOS?

The purchase limit for Online EFTPOS depends on your bank:

-

- ANZ: $5,000 per transaction

- ASB: $5,000 per day

- BNZ: $12,000 per day

- Westpac: $5,000 per day (unless otherwise agreed with Westpac)

- Co-operative Bank: Flexible daily limit, based on your individual agreement with the bank

How long do I have to approve my payment?

You have 4 to 7 minutes from the time the payment request is sent to approve the transaction in your bank app.

Annual Payment Transaction Not Working?

It can be frustrating when your insurance payment doesn’t go through, especially if there’s money in your account. In most cases, the decline is coming from the bank rather than your insurance provider.

Below are the most common reasons this happens, and what you can do to fix it.

Two-factor authentication (2FA) approval required

Some banks require extra confirmation for payments now, especially larger or less frequent ones like an annual insurance premium. This is known as two-factor authentication, or 2FA. Instead of automatically approving the payment, your bank may pause it until you confirm it’s really you.

How this usually works:

-

- Your bank sends a push notification to your banking app, or

- You receive a one-time code by text, or

- You’re asked to approve the payment in-app or via internet banking

If the approval step is missed or times out, the payment may be declined. What you can do:

-

- Keep your phone nearby when making the payment

- Check your banking app and text messages for an approval request

- Make sure your bank has your correct mobile number

- If your bank uses an App, open the app and approve the transaction, then try the payment again

If you don’t see any approval request, contact your bank to check whether 2FA is required for this type of payment and whether anything is blocking it. Once the authentication step is completed, payments usually go through without issue.

Insufficient available funds – Even if your account balance looks fine, some of that money may be unavailable. This can happen if:

-

- There are pending transactions

- Your account has a hold or overdraft limit

- Funds are reserved for another payment

What you can do:

-

- Check your available balance, not just your total balance

- Wait for pending transactions to clear

- Transfer funds from another account if needed

Daily transaction or payment limits – Banks often place limits on how much can be paid in one transaction or within a day. What you can do:

-

- Check your daily payment or card limit in your banking app

- Temporarily increase the limit

- Contact your bank for help

Card security or fraud checks – Banks monitor card payments closely. Larger or less common payments, like an annual premium, can sometimes trigger a security block your block. This is one of their methods to protect you from scams. What you can do:

-

- Check for a notification from your bank

- Confirm the transaction is legitimate in your banking app

- Call your bank to remove the block

- Try the payment again once cleared

Expired or replaced card details – If your card has recently expired, been replaced, or reissued, the old details may no longer work. What you can do:

-

- Update your card details in your online dashboard

- Use your new card number and expiry date

- Make sure the name and CVV match exactly

Online or international payment restrictions – Some banks restrict online payments or certain merchant types by default. What you can do:

-

- Check that online payments are enabled on your card

- Ask your bank if any merchant restrictions apply

- Enable the payment type if it has been turned off

Temporary bank outages or system issues – Sometimes the issue is simply a temporary banking problem. What you can do:

-

- Wait a short time and try again

- Check your bank’s service status page

- Try a different payment method if available

What to do if your payment is declined

If your annual premium payment doesn’t go through:

-

- Check your bank account and card details first

- Look for messages from your bank

- Contact your bank if the reason isn’t clear

- Once resolved, log back in and retry the payment

- If you are still having issues please give our team a call to assist.

If you’re ever unsure, our team can help guide you on next steps and make sure your cover stays on track. Insurance payments should be simple, and most declines are quick to fix once you know the cause.

Want to switch between Monthly and Annual Payment Options?

For details on how to switch between monthly and annual payments, check out our article on ‘Switching Payment Frequency‘. For details on how to renew an existing annual initio policy and where to find that payment information, please check our this support article “How to renew your annual policy with initio”

Direct Debit?

Please note, initio does NOT currently offer direct debit as a payment option.

Get a quote

Useful links:

How to set up an account with a visa debit card

Does initio offer multi policy discounts?

Why has my house insurance premium changed?

How does initio get paid?

How to set up an account with a visa debit card

What Information is important to initio

There are 2 main categories of information:

- Information relating to you, e.g. your insurance history, any claims made, any criminal convictions you have, if you have been bankrupt; and

- Information relating to your property e.g. if you have tenants in your house, if you live on a flood plain, any businesses that operate from the home.

What do you need to tell initio?

The policy application that you complete when you first take out insurance is used to collect the information that we need to know about you and your property. Insurance is a legal contract, and you must answer the questions truthfully.

Legally, you need to tell us about anything that could affect our decision to insure you or the terms and conditions you will be offered, even if we don’t specifically ask the question. For example, if a previous insurer had put terms on your policy, like a higher excess or not provided cover for burglary, we would want to know about this.

Why do you need to tell initio this information?

In order to properly assess the risk of insuring your property (and you), we want to know as much as possible. As you have knowledge of the property you are insuring, we rely on you to share this information with us.

When do you need to give initio this information?

You need to disclose all information to initio when you arrange the policy. Changes or new disclosures must be advised every time the policy is renewed. If there have been major changes you should advise these when they happen.

What happens if you leave out information?

The consequences can be serious. Legally, your policy can be treated as though it never existed and your insurer can refuse to consider your claim. For example, if you did not disclosure that you had previously had your insurance cancelled because you had lodged a fraudulent claim, your new insurer could cancel your policy from inception, refund any premiums paid and refuse your claim.

If you forgot to tell us that you live in a 100 year flood zone, we wouldn’t cancel your policy. We would act as if we knew about it when you first took out insurance. That would mean applying the applicable flood endorsement and excess. So while some omissions can be serious, others can be easily resolved.

The Golden Rule

If in doubt, disclose, disclose, disclose.

How do you advise a disclosure?

Our application forms will ask you a number of questions which may or may not cover the information you need to disclose. If not, please provide any further information under the question “Is there any further information likely to affect the acceptance of this insurance”. Answer “Yes” and enter the information not yet disclosed on the application within the field provided.

If you have a policy already in place and have new information to disclose, send an email to the team and our team will come back to you if they require any further detail or let you know if the information changes any terms/cover.

Duty of Disclosure

Disclosure vs. Declaration

Related articles:

Welcome to our newest blog series, where we delve into the essentials of readiness and resilience, covering everything from crafting a solid emergency plan to ensuring your sum insured is spot-on, and streamlining your insurance for the holiday season and beyond. However, before we explore these topics, we’re turning the spotlight on ourselves. While we remain hopeful for a calmer year ahead, we wouldn’t be in the insurance game if we didn’t value cautious optimism and thorough preparation for unforeseen events.

Join us as we kick off this series by demonstrating our commitment to continuous improvement and meticulous preparation, paving the way for a discussion on how you can do the same. It’s the first step in a series dedicated to empowering you with the knowledge and tools to protect what matters most.

We’ve got our house in order

Behind the scenes, we’ve been busy beefing up our infrastructure and services. Why, you ask? Because we want to be rock-solid for our customers when they need it. It’s all about making sure we’re ready with a helping hand, especially in those critical moments. By bringing in some of the coolest tech and smoothing out our processes, we’re not just hitting the mark; we’re aiming to soar way past it. Our mission? Building a stronger, niftier initio that’s ready to tackle whatever twists and turns come our way, giving our customers that awesome feeling of being in good hands. So, how exactly have we been doing this? Let’s dive in:

- Smart Claims upgrade: We’ve upgraded our smart claims system for quicker, more efficient processing. This ensures easier claims lodging and faster assistance in a crisis.

How to claim

- More team members: We want to make sure we’re always ready to help. So, we’ve brought more people into our team. This means when things get tough, you’ve got more friends at initio to support you when you need it most.

About us

- Location adjustments: We now use more detailed data in our location-based risk assessments. This helps us offer advice and solutions tailored to the unique risks of different New Zealand regions.

- Website upgrades: Our development team recently completed a 4-month platform refresh project to help us go faster and make your insurance even more seamless.

- Continuous learning: Following the 2023 events, we’ve refined our policies and practices to stay ahead in disaster preparedness.

No system can be entirely foolproof against the forces of nature. However, by taking these steps, we aim to enhance our resilience and readiness, providing our customers with the assurance that we’re better prepared to support them through any future challenges. Remember, being prepared is not just about having insurance; it’s about having the right support when you need it most.

The choices you make now can significantly impact your peace of mind and financial security in the future. Our team are always ready to assist you in making informed decisions about your insurance. Feel free to reach out with any questions, or visit our website for more information and resources.

Visit our FAQ pages for more insights and updates on how to manage your insurance effectively. Our goal at initio remains to make insurance easy.

To be completed by the insured(s) shown and also on behalf of any other person to be covered by this insurance.

I declare that:

- All information contained in this proposal and on any attachment is complete and correct;

- I have disclosed all material facts to Lumley;

- I agree that this proposal shall be the basis of the contract between me and Lumley and I am willing to accept the terms, conditions and exclusions of this insurance;

- I am authorised to complete this proposal on behalf of all people to be covered by this insurance and they give the same declarations.

By signing this form I authorise the insurer to:

- Check our details on the Insurance Claims Register and place our claims information on the Insurance Claims Register which other insurers can access;

- Disclose our personal information about this insurance to other members of the insurance industry and/or parties who have a financial interest in the subject matter of this insurance;

- Obtain our personal information held by any other party regarding my/our existing and previous insurances.

Crack the champagne – a toast to our focus on insurance claims!

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

Initio stands out not just for its technology, but for its practical, impactful applications that significantly improve the customer experience. Let’s explore the technological innovations at the core of our submission, which we call Smart Claims:

A fully digital, seamless claims process

Initio is one of the few insurance providers offering customers a 100% online claims process from start to finish, setting a new standard for convenience and efficiency in the insurance industry. Our Smart Claims platform eliminates the need for traditional phone calls to confirm details, handling everything online with ease and precision. This approach not only simplifies the claims process but also significantly speeds it up, allowing customers to focus on recovery and rebuilding without unnecessary stress.

Key features of our Smart Claims process:

- Streamlined submission: Customers can submit claims quickly and effortlessly, without the traditional hassles of paperwork and long waiting times.

- Efficient claims management: Our system ensures claims are managed efficiently, significantly reducing wait times and allowing our staff to focus on expediting claim processing rather than making follow-up calls.

- Reduced need for customer calls: Our online dashboard’s transparency and instant access mean fewer calls are needed, making us more available to pick up when you do call. This enhancement significantly improves your experience while allowing our support team to assist you more efficiently..

Proactive customer support and real-time updates

During Cyclone Gabrielle, Initio leveraged its advanced mapping tool, Locatio, to proactively identify and contact customers likely affected by the disaster. This not only ensured timely assistance but also demonstrated our proactive approach to customer care.

Enhancements in customer support:

- Claim support and updates: Our efficient system freed up our claims consultants to provide personalized support, focusing on those in critically affected areas.