Search results for: {search_term_string}/get-quote

New Zealand Pathfinder

Apple Mortgage

Contents Calculator

Bachcare

How do I get a Certificate of Insurance?

The Certificate of Insurance is a document that proves your cover is in place once you’ve purchased a policy. It’s also known as a Certificate of Currency. Banks and finance companies often ask for one when you apply for a mortgage or loan or when you are wanting to draw on the loan.

If you are yet to purchase the home or only looking to make an offer, you would alternatively obtain a “Letter of Intent” rather than a Certificate of Insurance.

Get your Certificate

Certificates are available at anytime once you have purchased cover through initio. You can download your certificate directly from your dashboard login. Click the Bank Certificate option on the relevant policy details. A certificate will open which you can save.

If you haven’t yet purchased your policy, please find more information here on how to get started.

Need to change the bank noted on your Certificate?

If you need to change the Interested Party (bank/loan provider) or the Insured Name on the policy, select the “Change” option on the right side-menu of the relevant policy. You can then update the policy and we’ll automatically send you an updated Certificate to your email.

Need to change the dates?

We are unable to alter the inception (effective) date of a policy once it’s been purchased. You can, however, cancel that policy from your dashboard back to the original inception date and re-purchase the policy (from your dashboard) with the correct date. A new certificate will be forwarded within minutes. Our system will also automatically provide you with a full refund for the original policy.

Please find more information regarding changes to a purchased policy on our site here.

Useful Links

When do I need house insurance?

Navigating your dashboard

Confirmation of cover

Stonewood Homes

First Lane NZPIF Insurance

There’s been a natural disaster, what happens next?

This is why you have insurance.

You’ve purchased insurance from us for exactly this type of situation. Most importantly, make sure you and your family are safe and dry. We are here to get your house, vehicles and belongings back up and running. Here’s some important information and tips on how to best handle things:

Your response

- Follow advice: Listen to official information channels and follow the directive of Civil Defence and emergency services

- Ensure safety: Make sure you, your family, and pets are safe. If someone is missing, contact emergency services immediately.

- Grab essentials: Take your emergency bag and a lockbox containing important and financial documents.

- Address health needs: Look after any physical injuries and emotional distress.

- Secure your home: If your home is damaged but standing, secure it. This might include temporary repairs.

- Document damage: Take photos of any damage for insurance purposes.

- Safeguard valuables: If possible, move valuable items to a secure location, like a friend’s house or a storage unit. Your insurance might cover storage costs.

- Contact your insurance provider: If your home needs urgent repairs and is still habitable, contact your insurance provider. Remember to document everything and keep all repair receipts. Be cautious of repair scams.

- We will prioritise claims with serious damage and uninhabitable houses. If this is your situation and you require additional support after lodging your claim you can get a hold of us through [email protected] or by phone 0800 763 929

- If you have ‘black water’, i.e. rising flood damage, and you want to get on with cleaning up you can lift the carpet and underlay and move it outside.

- For damaged contents, start to make a list and take photos. Retain as many items as you can as an Assessor may want to see them.

- If emergency temporary repairs are needed to mitigate further loss/damage to the property, engage a tradesperson and send us the costs to add to the claim. For example, securing lose roofing.

Vehicle damage?

- If your vehicle has been in deep water (over the tyres) do not attempt to drive the vehicle due to the potential risk of electrical damage and contamination.

- Use a permanent marker to mark on the vehicle where you think the water level got to.

- Lodge a claim online through your dashboard when you get a chance.

- For abandoned vehicles we will arrange for the vehicles to be towed when roads are open and tow trucks have availability. Please let us know during the claim lodgement if the vehicle has been abandoned away from your usual residence.

- Where possible and only if it is safe, remove personal belongings from the vehicle.

If you have had to leave your home

If you’ve moved into temporary accommodation, lodge your claim as soon as you can and include the cost of your stay so it can be prioritised as part of your claim.

Owner-occupied homes: Do I have cover for alternative accommodation, a place to stay?

Yes, all initio own-home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you are required to evacuate your residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR if your home is at risk from an insured event such as a flood. Keep receipts and note the dates of your stay — these costs will be included in your claim.

Rental properties: Do my tenants have cover for alternative accommodation?

If you are a landlord and your rental property is unable to be lived in because of the damage you are not responsible for finding your tenant’s alternative accommodation. This is something they are responsible for and their renters insurance would usually cover. However, with initio’s landlord policy, you do have cover for loss of rent if your rental property is uninhabitable.

Lodging a claim

With initio, lodging a claim is easy. Just login to your customer dash and click on the ‘claim’ icon to the right of your personal information.

Our easy-to-use questionnaire will step you through lodging your claim. We don’t expect you to understand your policy thoroughly, so we explain things along the way. Once your claim is lodged you will get a confirmation email and you can also see the claim’s progress on your dashboard.

To learn more, this guide walks you through how to claim with initio.

Provide as much detail as possible

When you make a claim, include clear and detailed information. This helps initio assess how urgent your claim is and what support you need. The smart claims platform can adjust its questions during large events, making it easier to understand your situation and prioritise help where it’s most needed.

Upload photos of the damage

Photos are key to understanding the extent of the loss. Upload them when lodging your claim — or later, if needed. Include shots of anything relevant, like flood levels, structural damage, or affected areas. The more visual evidence you provide, the faster and more accurately your claim can be handled.

Timing after a major event

Your safety comes first. Once it’s safe and you have internet access, submit your claim as soon as you can. If you’re unable to do this right away, that’s okay — just lodge it promptly when possible. If you need immediate advice, you can always call for help.

Our response to major events

Following any natural disaster, we usually receive a significant number of claims. Our team will work on prioritising and acknowledging your claims. Our focus will be to ensure people are safe and that homes are secure following damage.

If you receive a quote from a contractor please send it to us as we take a pragmatic approach to repairs. We prioritise claims for those vulnerable, most in need, emergency accommodation, and serious damage.

Other tips

- Never wade through flood water and avoid using vehicles or electrical appliances that might have water damage.

- Wear gloves, masks, and protective gear so you don’t come into contact with anything dangerous.

- Turn off the power at the mains if flood water has entered the home.

- If you are a landlord, check in with your tenants

- Learn more about staying safe on the Civil Defence website

NHC (previously EQC) Claims

Claims from a significant event may include areas of damage which NHC covers and also areas which NHC does not cover. All claims need to be lodged with us in the first instance, and then any NHC aspects are referred to NHC internally. This means that you only have to deal with initio (rather than also with NHC), but in the case of significant events, NHC claims can take a while to be processed. NHC claims are assessed in line with the Natural Hazards Insurance Act 2023 (NHI Act), we are bound to the due process that has to be followed.

FAQ’s

Can I start cleaning up?

Yes, but take photos and keep a schedule of damaged contents/items you remove from the house

When will an Assessor come and see me?

We are currently appointing assessors and priority will be given to those with serious damage and to those homes that are accessible.

Do I need to find accommodation for my tenants?

No, you can if you like but this is not your responsibility. Your tenant(s) will have to sort this on their own and they will incur costs to do this, however, if the house is not habitable they will be entitled to stop paying you rent. You can claim this loss of rental income through your landlord policy.

My house needs drying, how do I do that?

We use the services of Jaes for drying and extracting water. We will be working with them on the most serious losses, but it could take many days before they can get to you. If you have your own ability to source pumping or drying equipment you can add this to the cost of your claim.

Do I have cover for alternative accommodation, a place to stay?

Yes, all initio Own Home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you the homeowner is required to evacuate the residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR because the property is at risk of damage, from an event that would be covered by the policy. Flood damage is automatically covered for initio policyholders. Keep copies of accommodation receipts and record timing/dates and we will include these costs as part of the claim.

Am I covered for damage to my land?

The Natural Hazards Commission (previously EQC) provides certain cover for land damage; the NHC provides more than just cover from earthquake damage. Your insurance policy with initio includes NHC cover, and if your land is damaged by storm or flood, you’re eligible to make an NHC claim. To make the claim process simpler, you no longer have to claim through the NHC, we/our underwriter (IAG) will handle your NHC claim on behalf of the NHC. To understand more about how NHC land cover works see this NHC Landcover Guide

Other resources

- GENERAL: Civil Defence

- EARTHQUAKES: Geonet | NHC

Other initio articles of interest

Holiday home insurance basics

If you’re lucky enough to own a holiday home, you’ll want to make sure you’ve got the best insurance protection, especially considering you’ll not always be there in person to look after it. Whether you keep it for personal use or decide to rent it out to short term guests – we’ve got you covered.

Standard house insurance requires someone to be living at the home for more than 60 consecutive days. If it’s vacant for longer than this, it’s considered a holiday home. Because a holiday home isn’t your primary residence there are more risks involved, for example; the property may be empty for long periods of time, increasing its chances of break-ins.

What are my obligations?

We expect holiday houses to be empty more often, so our conditions are a little more lenient, but we do require:

- You or your family stay at the holiday house at least once a year

- The house is inspected (inside and outside) by you or a nominated person at least every 60 days

- The home and its grounds are maintained

- Mail is cleared regularly

- Water supply is turned off

- All doors and windows are secured when the home is vacant.

If you can’t meet these conditions, then a standard $5,000 excess will apply to your policy. Alternatively, if it’s fitted with a professional alarm* this will reduce to $1,000 when you claim for a break-in or burglary.

* Systems which include surveillance cameras only do not meet this criteria – the system needs the ability to provide an external alert (audible or direct to a monitoring company)

How do I get holiday home cover?

It’s as simple as selecting holiday home as the property type when you generate your instant quote. Alternatively, if you are changing your current home into a holiday home, all you need to do is change your cover in the property type drop down menu. The monthly costs will automatically update and will take effect as soon as you confirm the change online.

Holiday home or rental insurance?

The main difference between holiday homes and year round short term rentals is how often they are rented out. We have multiple options available depending on how frequently you rent your house out – just select the right option in the dropdown menu and initio’s clever software will do the rest. If you’re not sure which is the best cover for you, get in touch anytime. We’re here to help.

At initio, we offer comprehensive protection for your bach or holiday home, with flexible cover if you also rent to guests. Learn more: https://initio.co.nz/holiday-home-insurance/

This guide is intended to be a quick reference to vacant houses. We recommend reading the full policy wording for the full details of your holiday home coverage.

Useful articles:

What are my obligations as a landlord?

Initio’s landlord insurance policy requires landlords to meet the ‘Landlord Obligations’ for cover under the Landlord Protection and Meth Contamination extensions. The cover in these extensions are:

Landlord’s Protection

- Malicious damage by tenants, and associated loss of rents.

- Theft by tenants.

- Loss of Rent following a tenant vacating the property.

- Loss of Rent following a tenant eviction for non-payment of rent.

- Meth Contamination, and associated loss of rents.

If a landlord has a property manager, it is usually the property manager’s responsibility to meet the obligations. Otherwise, the landlord will need to meet these themselves.

If you don’t meet the Landlord’s Obligations all the standard cover included in the policy remains in place. You are still covered for natural disasters such as an earthquake as this does not involve the risk of the tenant. However, if you do NOT meet the obligations but then lodge a claim for meth contamination at your property, your claim may be declined.

Landlord’s Obligations

You, or the person who manages the tenancy on your behalf, must:

- Exercise reasonable care in the selection of the tenant(s) by at least obtaining satisfactory identification and written or verbal references for each adult tenant and when a reasonable landlord would consider it appropriate also check their credit and Tenancy Tribunal history.

- Keep written records of pre-tenancy checks conducted for each adult tenant, and provide to us a copy of these if we request it.

- Collect a total of 3 weeks’ rent in any combination of rent in advance and bond that will be registered with Tenancy Services.

- Complete an internal and external inspection of the home at a minimum of 3-monthly intervals at the relevant residential dwelling upon every change of tenant(s).

- Keep photographs and a written record of the outcome of each inspection, and provide us a copy of these if we request it.

- Monitor rents on a weekly basis with written notification being sent to the tenant(s) whenever rent is 14 days in arrears, together with a personal visit to determine if the tenant(s) remains in residence.

- Make application to the Tenancy Tribunal for vacant possession in accordance with the provisions of the Residential Tenancies Act 1986 if:

(a) the rent is 21 days in arrears, or

(b) you become aware of any illegal activity by the occupant(s) at the home, or

(c) intentional damage to the home is caused by the occupant(s).

What if the home is occupied by employees as part of their employment package?

If the home is provided to and occupied by your employee as part of their employment package with you, then obligations 3, 6. and 7.(a) do not apply.

What if this is my holiday home which is occasionally let to short term paying guests?

If the home is occupied by short-term paying guests such as a AirBnB or BookaBach, then the obligations do not apply to have cover for damage and theft by guests.

What if the home is occupied by Family Members?

You would need to decide if a Landlord policy is the right product for you. Are you wanting to cover Loss of Rents and Intentional Damage by Tenants? Does the family member pay rent? Get in touch with our support team to discuss the available options.

Protect your rental with initio’s landlord insurance

Related Articles:

What work is covered by a House flip policy?

Our house flip cover is designed for short-term cosmetic renovations. If you’ve got a do-up project that’s liveable, in reasonable condition, and just needs a refresh to get it market-ready, this policy is ideal.

We can cover homes that:

-

Are safe and habitable

-

Have no major outstanding maintenance or damage

-

Only need light updates to improve their appeal

We cover cosmetic renovations — things like painting, new carpet, or replacing fixtures.

We don’t cover structural alterations — so it’s important to know the difference before purchasing this policy.

If you’re planning work that involves changing the structure of the home, you’ll need a separate contract works policy.

Is your project suitable for initio’s Flip Policy?

Works covered by a House flip policy

Cosmetic Renovations

If you’re doing cosmetic renovations to your house (with no structural alterations) you can place cover under a House flip policy.

What’s considered ‘Cosmetic Renovations’?

Cosmetic renovations are work that doesn’t involve structural alterations or changes to the house. Some examples that are covered by the House flip cover are:

- Painting (outside and inside)

- Installing new carpets

- Replacing a toilet

- Removing a non-load bearing wall

Works that won’t be covered by a House flip policy

Structural Renovations

The House flip cover is not designed to cover work that involves changes to the house’s structural make-up. This kind of work should be covered by a separate contract works policy on the house.

What’s considered ‘Structural Renovations’?

Some examples of structural work are:

- Re-roofing

- Building a new extension to the house

- Removing a load-bearing wall

- Re-cladding the house’s exterior

Note that this isn’t an exhaustive list. If you’re still unsure if the work you’re doing is structural, please get in touch.

Doing Structural Work and need contract works cover?

For a specialist online contract works solution we’re partnered with BuiltIn Insurance. BuiltIn are New Zealand’s trade insurance experts and have an online Contract Works insurance offering where you can get a quote for your works online, and purchase online too.

Like initio, BuiltIn are underwritten by IAG so this means that you will have the same ultimate underwriter for the house and contract works risk, which is important.

BuiltIn Contract Works Quote

Contact us

Getting in touch with us

We are all about online insurance so we can better understand your query if you send us an email or chat with us online (see the green button at the bottom right of screen). But do feel free to give us a call.

Phone:

0800 763 929

From Overseas:

+64 7 929 4126

Email:

[email protected]

Claims

Claims can be lodged and you can follow progress on your Initio dashboard. But you can also get hold of us using the following:

Email:

[email protected]

Claims Assistance (monday-friday 8.30-5.00):

0800 763 929

Claims Emergency Only (IAG after hours)

0800 560 333

Post

By Mail:

PO Box 19497, Hamilton

In Person:

6 Garden Place, Hamilton

Why do I need house insurance?

House insurance protects you financially when the unexpected happens to your home, like a fire, flood, or sudden water damage. Without it, you’d need to pay the full cost of repairs or rebuilding yourself, which can be extremely expensive.

Most New Zealand homes are worth hundreds of thousands of dollars. Rebuilding or repairing after a disaster is not something most homeowners can afford out of pocket, and these expenses often come without warning.

That’s why it’s important to set the right sum insured – the maximum amount your insurance will pay to rebuild your home. You can learn more about how to work this out in our guide to calculating your sum insured.

Tempted to skip it to save money?

In tough financial times, it can be tempting to look for areas to cut back, and insurance can feel like an easy one to drop, especially if you haven’t made a claim in years. But it’s worth asking yourself:

If disaster struck tomorrow, could you afford to recover without insurance?

A single fire or flood can destroy years of financial progress. Even minor repairs can cost tens of thousands, and that’s before factoring in things like temporary accommodation. When you don’t have cover, you’re gambling with your biggest asset.

When you pay for insurance, you’re not just buying cover, you’re paying a provider to take on the financial risk for you, so you’re not left to carry it alone if something goes wrong.

Insurance isn’t about being pessimistic; it’s about being prepared.

You can reduce your premium without losing cover

If you’re looking for ways to keep your costs down, one of the most effective options is to increase your excess. This is the amount you agree to pay if you make a claim.

By choosing a higher excess, you’re taking on a bit more risk upfront, but it usually means you’ll pay a lower premium year to year. It’s a good option for homeowners who:

- Want to keep their cover but lower their premium

- Haven’t made a claim in a while

- Could comfortably pay a higher excess in the rare event they do need to claim

At initio, our quick quoting tool makes it easy to adjust your excess when you get a quote, so you stay protected, without paying more than you need to.

Insurance is about protecting what matters most

Your home is likely your most valuable asset. House insurance is designed to shield it from things you can’t plan for: fires, floods, storms, and earthquakes.

With initio, you’re covered for sudden and accidental damage, and you can lodge a claim online in minutes. It’s fast, flexible protection, backed by real people.

The bottom line: why you need house insurance

- Because disasters can happen to anyone at any time

- Because the cost to rebuild or repair is high

- Because insurance offers security when you need it most

- Because there are smart ways to stay covered without overspending

Still thinking it through? Get a quote online in minutes, or learn more about what our house insurance covers

Related articles:

Navigating your initio dashboard

Your initio dashboard is your secure online space to manage your house and vehicle insurance in one place. From here you can make a claim, update your details, download important documents, renew or cancel your policy at any time. It is designed to give you full control of your cover, without needing to call or email.

When you purchase your first house or vehicle policy with initio, you will create an account as part of that process, giving you access to online management of your policies. At initio we refer to the area where you manage your covers as your ‘dashboard’.

Initio’s online dashboard is designed for you to manage your policies, make claims, update your details, or even cancel your policy, without needing to call or message us. This makes it easy to check on your covers, claim, download documents and make changes as required, all from one place and with instant confirmation.

Quick summary:

-

Manage your house and vehicle insurance online, anytime.

-

Make a claim, update details, renew or cancel in one place.

-

Download your policy schedule and certificate of insurance instantly.

-

Only the property owner can be the main account holder.

-

Update payment card and contact details through your profile.

-

Start new quotes and add policies from your dashboard.

-

Get help via support articles or Chatbot Chad.

How to log in to your dashboard

Following your first policy purchase with initio, you will immediately receive a welcome email from us.

To log into your account, click the button at the top right-hand side of the initio website. Enter the email address used for your purchase and the password you used when you created your account. This will give you access to your dashboard.

What you can do in your dashboard

Once logged into your initio dashboard, you’ll have full access from any device, at any time.

Here’s what you’ll see:

View your account overview

If you hover over the account button in the top right corner you will see additional options of “dashboard”, “profile”, “credit card” and “sign out”.

Update your profile

One of the first things you may want to do is update your password to something more secure or easier to remember. You can do this through the “Profile” section. From there, you can also update your email address, phone number, postal address and password. Whilst you can view the contact name details, if you need to make a change to those, please let us know via phone (0800 763 929) or email ([email protected]).

Don’t forget to click on the update button once you’ve made any changes.

Update your contact details

For security and legal reasons, we can only allow the property owner (you) to be recorded as the main account holder for your insurance.

This is because the main login has full authority to manage your policy, including signing legally binding documents, changing cover details, and updating or accessing your payment and banking information.

While we’re happy for your property manager to be added as an authorised contact to help with day-to-day matters, it’s important that full control of your insurance stays with you as the owner. This protects your interests and ensures any major changes are properly authorised.

Should you need to lodge a claim, you can include details of your property manager within the online claim form if you wish them to assist with the claim management. The initial claim form, however, does need to be completed by you.

Update your payment card details

If you are paying for any of your policies monthly, the system will automatically process the transactions to your card used for the initial purchase. If your credit or debit card expires, is lost, or replaced, or you wish to change the payments to a different card, you can quickly view and/or update the card details here.

You can also log out of your dashboard from this section.

Your dashboard

Use this button anytime to navigate back to the main dashboard screen.

Sign out

Use this option to sign out of your account on the browser/device you are using.

Lastly, you’ll find contact information and quick access to our support articles if you need further assistance.

Get a new quote or add a policy

You can easily obtain a new quote or add a new policy through your initio dashboard.

To the right of the property’s address, you’ll find two green buttons: “House Insurance +” and “Car Insurance +.” These will guide you through the process of first obtaining a quote and then if you wish to continue, starting a new policy, whether it’s for another house or vehicle. The new policy will then also be stored on the same dashboard for easy management.

Don’t forget to ‘save your quote’ by emailing yourself a copy. This can then be restored at anytime from your email inbox.

Claim, change, invoices & cancel

Below each property’s address/policy, you will see the above options to;

- “Claim”

- “Change” – update your policy, i.e. bank/mortgage details, amend your sum insured, excess, etc.

- “Invoices” – view and/or download historical invoices, obtain copies for your accountant. If you need an annual financial summary of your monthly payments for Tax Purposes, please contact the support team.

- “Cancel” – cancel your policy, any refunds will also be automatically calculated as part of this process.

Within 30 days of any policy’s annual anniversary, you will also see another button called “review & confirm”. Use this button to view, customise and/or pay for the upcoming year’s insurance.

All of this can be done directly through your dashboard.

If you need further guidance on how to complete some of these tasks, check out our support articles:

Cover details +

Underneath your property’s address is a button with “Cover Details+”. If you click on this button, it will open up a section that allows you to perform quick changes as well as find the important documentation for downloading.

Important documentation

As a digital insurance provider, all your key documents, such as the latest policy schedule, policy wording, and bank certificate, are issued as PDFs rather than paper copies.

You’ll likely use this section when you need to provide a bank with confirmation of cover, ie. a certificate of insurance. If you’re a landlord you will also find the tenant insurance certificate(s) in this section also.

These documents will be emailed to you when you first purchase your policy, but they are also stored on your dashboard, making them easy to access and download whenever needed. If you do need a printed copy, you can download and print these from home at any time.

If you need a document that is not available from your dashboard, such as an older policy schedule (for a previous insurance period), please get in touch with our support team and they will be more than happy to assist.

Getting help from the dashboard

Chatbot Chad

Along with our helpful staff we also have our AI chatbot Chad, he is always available if you have any questions or need some general help. Simply click the “Help” button at the bottom of the dashboard for assistance. If there’s something he can’t help with, you can always escalate the query to our support team via the same chat option (during business hours).

Video overview

Not a fan of reading? We’ve got you. Check out our video overview here:

Useful links:

House Flip Insurance

Life Direct

Nelson Marlborough Insurance Limited

movinghub

Provincial insurance brokers

Affiliated Waikato

Northco Insurance Brokers

dawson

Insurance Design

Wayne Grayson

How to claim for water damage

If you have home and contents insurance with initio and your home suffers water damage, here’s what you need to do:

- Get the water turned off or at least isolate the leak to stop water flowing to it. You might need to get a plumber to do this for you.

- Make sure the house is safe. If the wiring could be wet, turn the power off and get an electrician to check it.

- Get the house dry quickly. Call a professional drying company such as ChemDry or JAE and get them to install some commercial dryers and blowers as soon as possible, they’ll also know if carpets need to be uplifted, walls opened and insulation removed etc.

- Log in to your dashboard on the initio website and click on Make a Claim, fill in the form and send us any photos you’ve taken. We’ll email or call you within 1 business day.

Black water alert

As a precaution, where homes have been contaminated by black water (sewage or storm water), extra care must be taken. See our guidelines on black water and cleaning up after a flood.

FAQs

Will Initio send an assessor?

An assessor won’t be able to do anything until the property is dry. If there is significant damage to your home afterwards, then we can get an assessor to go to site.

Can I use any plumber, electrician, drying company, or do Initio have approved companies that I must use?

You can use any repairer or supplier you like. So long as their costs are reasonable and you are happy with the standard of work, then we’re happy. Please be aware that in some instances the cost of the tradesman’s work may not be covered under your policy, that may still need to be determined.

What is my excess?

This amount is chosen by you when you buy the insurance, if you can’t remember, just check your policy schedule (you’ll find this document on your dashboard).

Our plumber has told us that the leak was caused by a rusted nail in a pipe in the wall, it’s been slowly leaking for the past few weeks but we’ve only just noticed it. Is this covered?

Because the damage has been happening over a long period of time, we need to claim under the ‘Hidden Gradual Damage’ benefit of the insurance policy. This benefit covers leaks stemming from internal water pipes and tanks that are hidden from site and have been leaking over a long period of time, the cover is capped at $3,000 and your excess will be deducted from that limit.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

An initio customer returned from a holiday overseas to discover a sudden burst pipe had resulted in almost $8,500 worth of damage. Initio paid the claim efficiently, straight to the customer’s bank account.

Related articles

How does initio get paid?

On the questions of: how does Initio make money? Does Initio charge fees? It is first important to know what type of business initio is:

Initio is an Underwriting Agency of registered insurer IAG. Initio is not an insurance company in its own right. This means that initio has delegated authority from the insurer to establish and manage insurance for houses, contents and cars. In addition, Initio has authority to pay claims on behalf of the insurer.

Initio is a licensed Financial Advice Provider under the Financial Markets Authority of New Zealand. Initio have staff who are Registered Financial Advisors, which enables initio to provide customers with insurance advice specific to their situation.

On the sale of an insurance policy, including its subsequent renewal, initio is remunerated by commission and fees. The commission is a payment that recognises the cost of delivering such functions, administration, and services that would otherwise be a cost to the insurer, and the fee is a transaction and platform fee designed to recover costs associated with transaction processing including bank and payment provider processing costs, credit card merchant charges, and obtaining property risk and vehicle data, and regulated financial advice. For details of charges and remuneration see our disclosure statement, and/or refer to the quote and invoice when transacting with us.

Related Articles

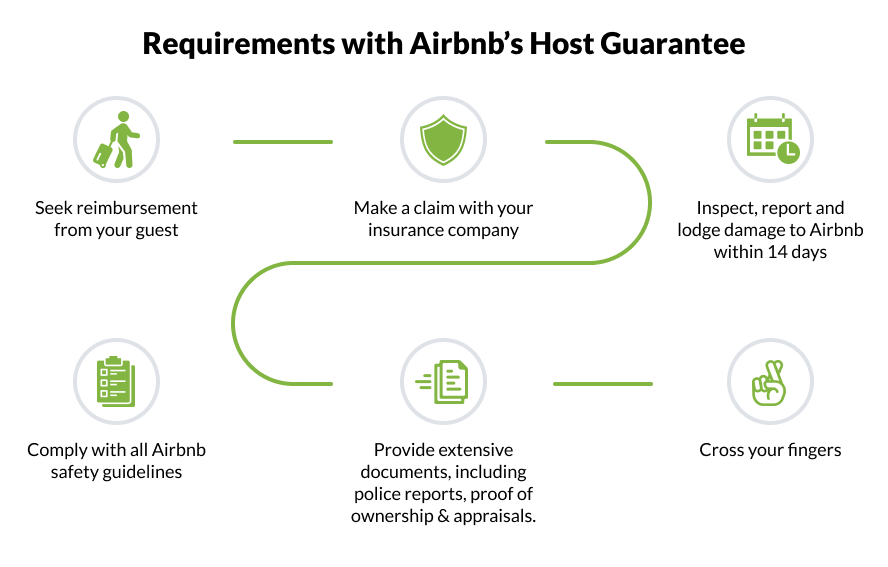

Should you rely on the Airbnb Host Guarantee?

Many hosts rely on Airbnb’s well-advertised $1USD million of free Host Guarantee cover. But be warned, this can lull you into a false sense of security leaving many disappointed when they make a claim but find they don’t tick the boxes.

The rules are specific, which can make it hard to claim especially when innocent hosts unknowingly violate the conditions.

What does it cover?

The Airbnb Host Guarantee isn’t a formal insurance policy, but rather a strongly-worded promise to rectify guest damage providing your situation meets certain conditions.

It isn’t regulated by the New Zealand Financial Markets Authority, so you would struggle to take them to court locally if things really turn sour.

Last Resort for Recovery

In Airbnb’s own words they say the Host Guarantee is not an insurance policy, and shouldn’t be considered a replacement.

Firstly, the guarantee can only be claimed on after trying to recover compensation from the guest, and then your own insurance (if you have this). Already the Host Guarantee is a last resort.

For a chance of recovery from the guarantee, you’re going to have to prove you persistently chased up that festival-goer to get $800 back for a living room wall repair.

There are many examples of people angry about their payout from the guarantee. Usually it’s because they aren’t aware of the conditions.

A main stump is that damage needs to be inspected, reported and lodged to Airbnb within 14 days, or else you’re out of luck.

By the time you’ve checked in your next guest it could already be too late. This could be enough to kill any claim through the Guarantee if you live away from your Airbnb.

Remember that you need to seek recover from the guest, and then your insurance before you lodge a claim in the 14 day window. The requirements almost seem like a trap to get you to exceed the strict 14-day deadline.

Watch out for Exclusions

- Only damage that happens during the booking period is covered. If an unwelcome guest overstays their welcome and causes damage, there won’t be cover.

- Cover only applies to part of the house that’s in your listing. If you rent a room, but your guest uses another bathroom and causes damage, you’ll need to foot the plumber’s bill yourself.

- It’s full of various exclusions; like damage from excessive water utility use (a sink overflow won’t be covered), and any damage by animals or pets (are you sure your guests won’t bring their dog?).

- Be prepared for stacks of bureaucracy when you make a claim. Airbnb require extensive police reports, proof of ownership and request form documents for damage.

The list of exclusions goes on. To read the full terms, conditions and exclusions see here.

No Liability Insurance

Finally, the Host Guarantee doesn’t help when it comes to legal liability. If your guest suffers an injury and they sue you, the Host Guarantee will fall seriously short.

The idea of someone stubbing their toe on the coffee table and suing might seem ridiculous, but legal liability also extends to things like sickness (if an illness is caused by the condition of your house) or freak accidents.

Is it worth the Risk?

One-in-seven Kiwi Airbnb hosts report damage. That’s about a 15% chance you’ll suffer damage one-day.

While most reports are minor and hosts voluntarily pay to avoid the lengthy resolution process, we’ve heard some shocking stories ranging from vomit-covered walls to 100-person guest parties.

Hosts should ask themselves if relying on the Guarantee is worth the risk? After all, Airbnb themselves recommend having robust insurance in place in the first instance.

Learn more today about our specialist short-term guest cover.

Initio Insurance are the pioneers of online house insurance in New Zealand, with cover specifically designed for own homes and holiday homes also rented on Airbnb.

Related articles:

Join our team!

Digitally savvy, human touch; The heart of initio

Since 2011 we have been redefining insurance. We are creating an insurance experience that customers love! At initio, we are all about creating better digital experiences for buying and managing insurance exclusively online. We’re best known for being the first insurance provider in New Zealand to quote and bind an insurance policy online. We consider ourselves to be the challenger brand to the domestic insurance market in New Zealand and as such we are on a mission to redefine the way insurance is managed and delivered to customers digitally.

At initio, we’re not just hiring; we’re on the lookout for thinkers, creators, and lively souls eager to influence the next chapter of insurance for our clients. If you’re brimming with creativity and ready to make an impact, you’re in good company.

Award-Winning Workplace

Yes, you read it right; we’ve got a brand-new accolade. initio has been named one of the Best Insurance Companies to Work for in Australia and New Zealand in 2023! If you want to be part of a company that’s officially recognised as a brilliant place to work, one that truly looks after its staff, then look no further. Come join our award-winning team and let’s transform those brilliant ideas into something that shines even brighter.

Open Positions

Here’s a sneak peek at our roles currently on offer. Can’t find the perfect role just yet? Keep swinging by – new opportunities land faster than you can say “Cheeseburger Fridays.”

How to: Storm Damage Claim

IMPORTANT: If your house is unsecure, unsafe or vulnerable to more damage, get a professional to make the house livable and we’ll work through the costs together later.

After ensuring the house is secure and everyone is safe, here’s what to do if you have home and contents insurance with Initio:

- Take a photo of the damage.

- Complete any urgent repairs ie glazing, tree removal etc

- Get a quote to repair the remaining damage.

- Log in to your dashboard on the initio website and click on make a claim

- Fill in the form and send us the photo and quote.

- We’ll email or call you within 1 business day.

Black water alert

As a precaution, homes that have been inundated with flood waters from the street or rivers should be treated as contaminated (black water) and extra care taken. See our guidelines on black water and cleaning up after a flood.

FAQ’s:

- Can I use my own repairer or do Initio have approved repairers that I must use?

You can use any repairer you like. So long as their costs are reasonable and you are happy with the standard of work, then we’re happy.

- My holiday home has potentially been damaged by a storm, but we’re not going there for another month, can I claim that late after the date of the storm?

You can claim for damage after the loss; however, it is an absolute requirement that you do everything you can to ensure any damage is kept as minimal as possible. If you are not able to get to your holiday home yourself, then you’ll need to get someone else to go and check it to make sure that no urgent repairs are needed.

- What is my excess?

This amount is chosen by you when you buy the insurance, if you can’t remember, just check your policy schedule (you’ll find this document on your dashboard).

- Will Initio send an assessor to look before I fix anything?

An assessor may be appointed to your claim if the loss looks to be substantial. Please note that you don’t have to wait for an assessor, to complete urgent repairs like smashed windows and doors.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

Initio were on site for this client within 24 hours following a tornado in the National Park.

Related articles: