Search results for: {search_term_string}/get-quote

A candid take on initio’s approach to you and your home

At initio we are ‘all-in’ on customer experience. We ruthlessly pursue customer satisfaction with our technology, support and communications …. But only for a certain type of customer. In short, we are not for everyone.

Yes, we’re audacious enough to say: “Sorry, we can’t be your insurance provider” – at least not if it means compromising the ethos that underpins our brand, or transacting with you in a way that doesn’t celebrate the use of our tech. We provide superior ease of insurance and customer service, but only to a specific kind of customer who appreciates and respects our ‘digital by default’ approach.

Catering to the Modern, Digital-Savvy Customer

Our business model is laser-focused on a modern, self-reliant breed of customers. The digital age has dramatically reshaped the insurance industry, and initio remains at the forefront of this transformation. We are designed for customers who value autonomy, speed, and convenience, rather than the traditional, hands-on approach.

Customers who are comfortable transacting online, managing their property portfolios with digital tools, and who comprehend that competitive premiums and high-touch hand-holding services are often mutually exclusive, are our ideal clientele. For these customers we are digital by default, and human when you need us.

The Interplay of Technology and Affordability

“Why can’t you just start the policy for me over the phone”

“Why don’t you call me every year when my policy renews so we can have a chat about it”

“Why can’t you just send me your bank account and I’ll transfer the premium funds”

“Send me a quote”

It’s a ‘no’ on all fronts. The truth is, high-touch insurance services involve considerable operational costs – think travel, long-winded phone calls, time, and administration. We’ve spent over 10 years building a digital platform that substitutes for these things; its frictionless insurance, that’s quote in one click, cover in 2 minutes, claim in an instant. By utilising technology to automate many aspects of our services, we increase efficiency and are able to offer competitive pricing.

Our system has been designed to suit a certain type of customer, and it’s not for everyone.

This doesn’t mean we shirk our responsibility to our customers that embrace our technology. Quite the contrary – we provide comprehensive digital and phone support, and abundant online resources to help.

Why we decline to insure some houses

Sometimes we have to say no to insuring your house. It’s not you, or your house, it’s simply the way we want to run our business and the rules we, and our insurer, have had to create to be able to offer our services long-term.

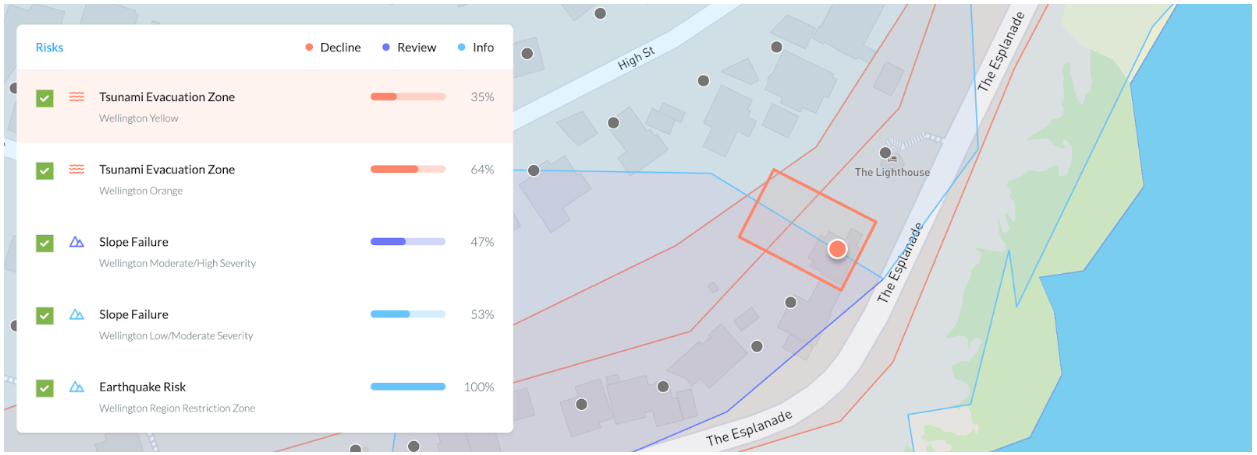

It’s digital too: The primary decision making on whether or not to insure your property is done by a smart tool we built called ‘Locatio’. When you type in your address with initio, Locatio makes decisions about whether initio can provide cover by using things like council property data, flood maps, earthquake and land risk.

In order to remain a sustainable and successful insurance provider we choose to focus on certain types of houses, and this means that there are some locations where we can’t provide cover, and certain risk exposures such as flood or land instability that are just not our bag.

We are constantly updating our business and underwriting rules, so just because we say no today, doesn’t mean that it’s a no forever.

You also need to know that we cannot sell you something that isn’t right for your situation either. So if your property does not fit our product we’ll decline to provide cover, and we don’t mean any offence by this.

The cost is the cost

A number of factors go into calculating the total cost of your home insurance, including location, age of the property, and other things like government-imposed levies. Our award-winning insurance technology computes the insurance cost, and we rely on that to run our business. The premiums need to be set at a level that allows the insurer the margins to continue to pay claims and reinsurance costs. In short, the cost is the cost.

Learn more about how the insurance risk component of your insurance cost is calculated

It’s 100% your choice whether or not to accept the insurance cost we offer. You can ring or email and challenge a cost but ultimately it’s out of our hands as the system has spoken. You need to know though that we work incredibly hard to maintain competitive premiums for our customers. We do this by continually investing in our technology for efficient processes, negotiations with our insurer, constantly refining the rules that determine how risky our portfolio of houses is (ultimately the more aggregated risk we take on, the bigger our premium pool needs to be).

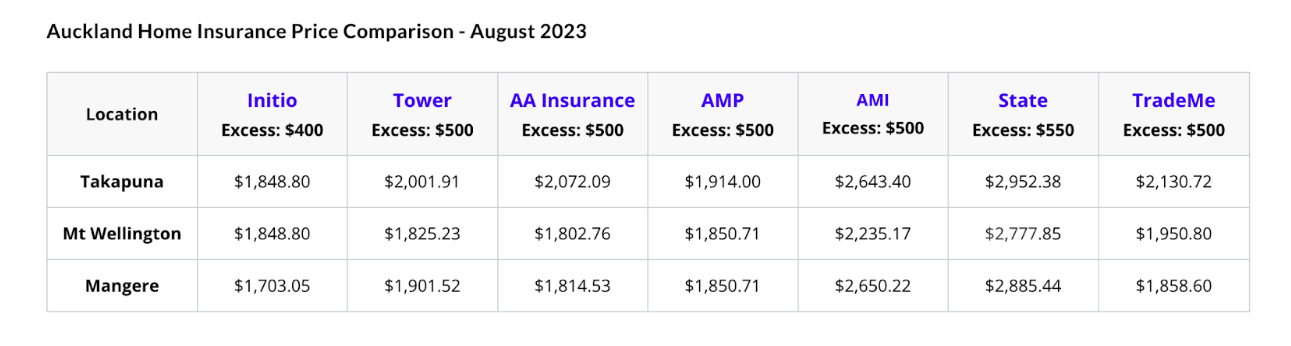

Our efforts to keep premiums competitive have been confirmed by feedback from our customers and also by financial resource websites like Moneyhub.

Source: Moneyhub

It’s simply not possible to be the most competitive all of the time, and we implore our customers to take a long and holistic view of their insurance that takes account of things like support (can you get you easily get ahold of your insurer), claims responsiveness, ease of use, technology and overall confidence in your provider.

It’s worth bearing in mind that not all policies are built the same, so just comparing price vs price doesn’t quite cover it. We highly recommend using our comparison tool if you want to see how we stack up when you also take the policies into consideration.

An Unapologetic Philosophy

Our philosophy is blunt but honest: “We are not for everyone”. Our model isn’t all things to all people, and that’s intentional. We’re looking for customers who align with our ethos – those who want a superior digital service.

While we understand some may expect more traditional customer service methods, we respectfully suggest they may be happier elsewhere. This is not a dismissal, but a candid admission that our service model may not suit everyone’s expectations.

In sum up, initio is unyieldingly committed to delivering our unique brand of customer experience, one that is unabashedly shaped by the needs of modern, digital-savvy customers. While our approach may not resonate with everyone, we are firm in our refusal to compromise on the affordability and efficiency that our model provides.

To our customers who find value in what we offer, we welcome you wholeheartedly. To those who don’t, we don’t hesitate to say: “We are not for you” And that’s how we maintain the balance that allows us to continue delivering what we believe is the optimal blend of service and affordability in today’s market… all driven by our technology.

There’s a lot to juggle when you’re buying your first place – deposits, lawyers, moving trucks, the lot. Sorting out home insurance when buying your first house is another step, but it doesn’t have to be confusing.

That’s why we created the First Home Buyer Insurance Guide. It explains what house and contents insurance is all about, answers the questions first-home buyers ask most, and helps you avoid common mistakes.

You’ve got enough to think about. We’ll make insurance the easy part.

When do you need insurance?

One of the biggest surprises for first-home buyers is when insurance is actually required. Most banks won’t release your loan until they’ve seen confirmation of cover. You can’t leave it until after settlement.

Here’s how timing works:

Sorting your insurance early gives you peace of mind and avoids last-minute stress.

Proof of cover: two simple options

Letter of Intent

Best when you’re still finalising the purchase or need something fast. Get a quote online, customise your cover, and download the Letter of Intent instantly to show your lender the property can be insured.

Certificate of Insurance

Once you’ve bought the home, complete your sign-up, pay your premium, and receive the Certificate of Insurance by email. This confirms your cover is active from settlement day. All you need is your new address – no phone calls, no delays.

What to look for in your policy

Insurance isn’t one-size-fits-all. Before you buy, think about:

- Sum insured: The rebuild cost of your home (not the market value). Include demolition, site clearance, and GST. Use our calculator to help you estimate the rebuild cost.

- Excess: What you’ll pay if you make a claim. Higher excess lowers premiums but increases out-of-pocket costs.

- What’s covered: Fire, flood, storm, burglary, accidental damage, and natural disasters.

- What’s not: Wear and tear, gradual damage, or maintenance issues.

And don’t forget contents cover – your furniture, electronics, and valuables add up quickly.

Mistakes first-home buyers often make

It’s easy to treat insurance like a box to tick, but the wrong choice can leave you out of pocket. Common mistakes include:

- Underinsuring: Cutting corners on your sum insured lowers premiums but leaves you short if disaster strikes.

- Guessing rebuild costs: Use a calculator or valuation instead of rough estimates. Learn more about calculating rebuild costs.

- Chasing the cheapest price: Low-cost policies often have gaps in cover or poor claims support. Use our online comparison tool to compare cover options between leading NZ insurance providers.

- Picking the wrong excess: Balance affordability with what you could realistically pay. Learn more about insurance excess

- Forgetting contents and car cover: Protecting your house is step one, but your belongings and car matter too. Access our contents calculator tool to work out the value of your belongings.

Why initio works for first-home buyers

You don’t just need cheap insurance – you need cover that works when it matters. That’s where initio comes in:

We built initio to take the hassle out of insurance. No hold music. No confusing forms. Smart cover made simple.

Ready to get started?

Read the full First Home Buyer Insurance Guide for step-by-step instructions, examples, and practical tips to help you get it right from the start.

Make insurance one less thing to stress about – so you can focus on enjoying your new home.

Ready to begin your journey with initio? Start with a quote

Related articles

Want to dive deeper?

Watch our video where Guy, our Head of Partnerships, explains what insurance actually does, why banks care about confirmation of cover, and how to avoid common traps as a first-home buyer.

Is it only used as extra space for your household?

If you have two dwellings on your property and the second one is used only by you or your family—without being rented out—it’s important to have the right insurance to cover both spaces.

What counts as an extension to your own home?

If the second unit/home is;

- Used like a sleepout for members of your immediate family, such as teenagers or elder family members.

- And you all predominantly share meals and/or facilities OR

- Used as a hobby room such as an art or music room OR

- Used as a home office space, then

It’s considered as an extension to your home and counts towards the one home unit/dwelling.

What insurance do you need?

For this setup, you only need one home insurance policy, which will cover both your main home and the second dwelling under the same policy. This ensures protection for:

- Your home and any structures used as part of your home for residential purposes on the property

Get covered today

With initio, you can get a quick quote and buy insurance online in minutes, making it easy to ensure your home and second dwelling are fully protected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

Buy house insurance

Need help? If you’re unsure about what policies are right for your situation, contact us to make sure you’re fully protected.

Get covered today with initio – Quick quotes, easy online cover.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

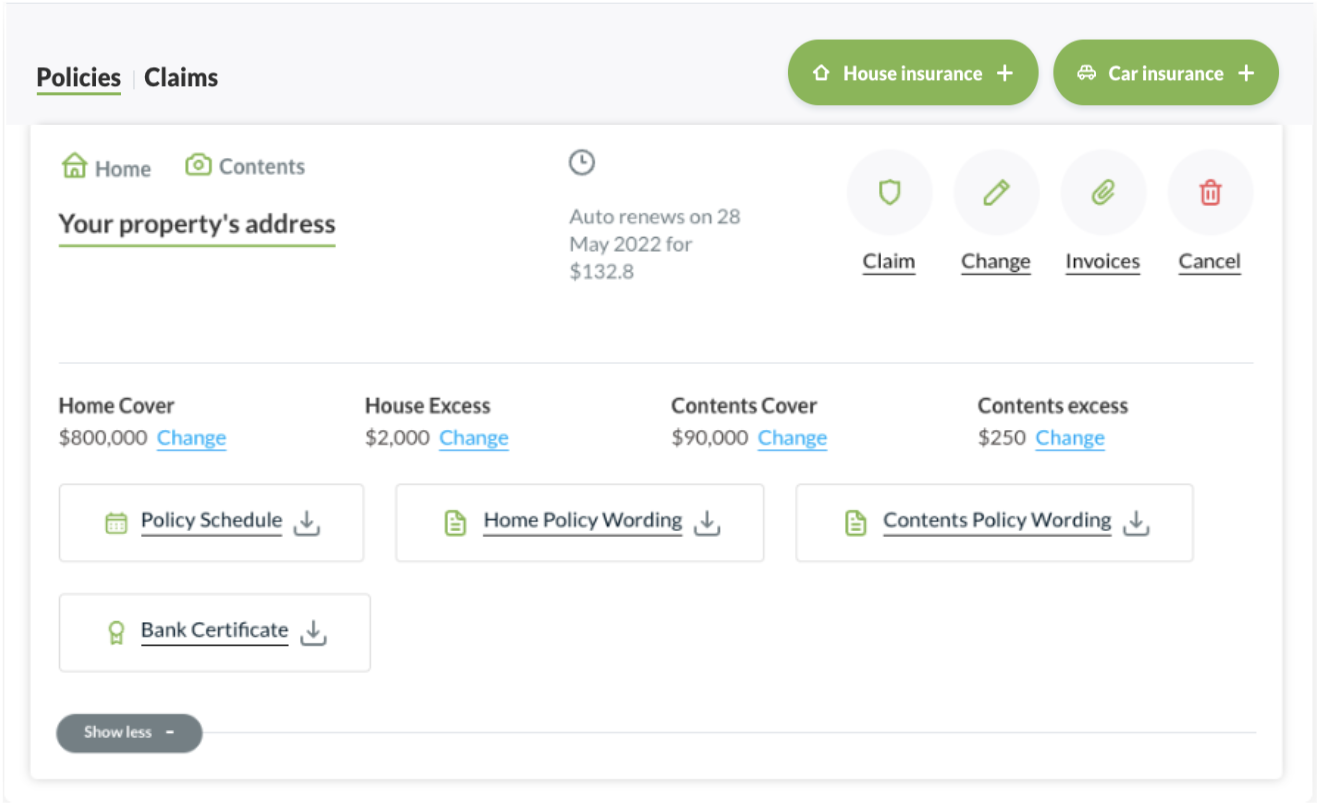

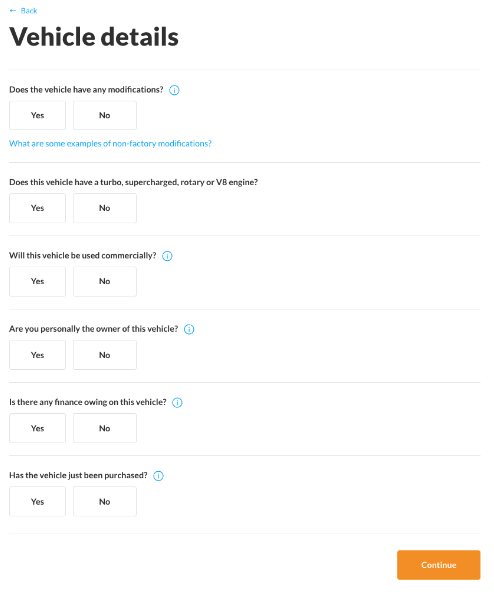

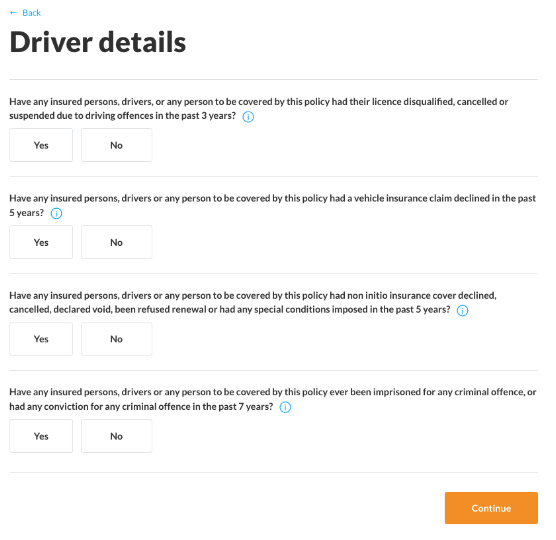

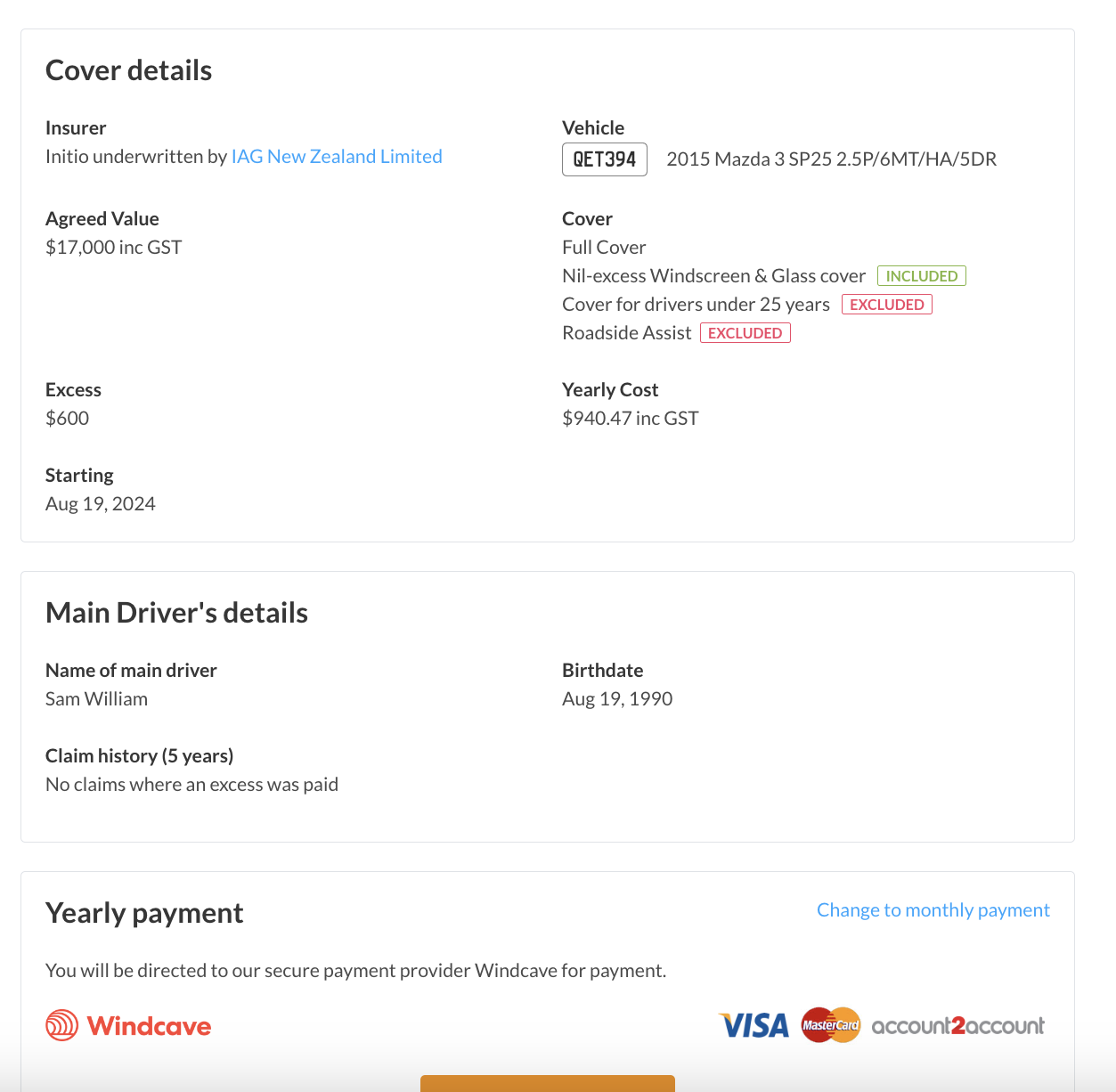

So you have just insured your property with us. Awesome! But you are wondering how to add insurance for your vehicle? This guide will walk you through the essential steps: getting a quote, customising your cover, disclosing necessary information, and making your payment.

1. Get an instant quote

When you purchased your insurance policy for your property, you would’ve been introduced to your initio dashboard. Within a few moments of your home product purchase, we would have provided you with login information for your initio dashboard. You will need to login to your dashboard to begin the process of getting vehicle insurance. This is because we only offer vehicle insurance to customers who have a property insured with initio.

Simply click on the green “Car Insurance +” button, which takes you to a page asking for your vehicle registration number.

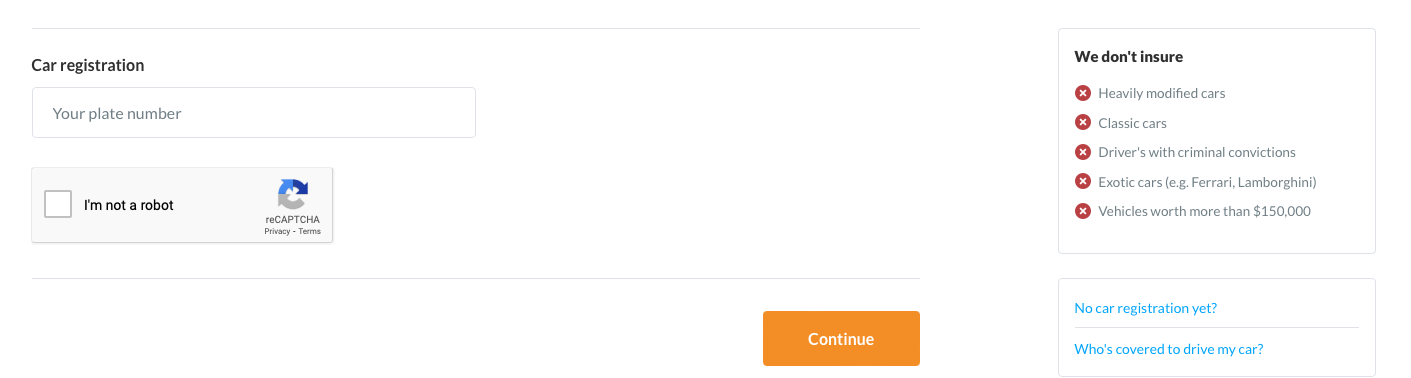

2. Get a quote

Enter your vehicle’s registration number to continue. If you have a brand new vehicle that has not been registered yet; email our team, they can assist you further.

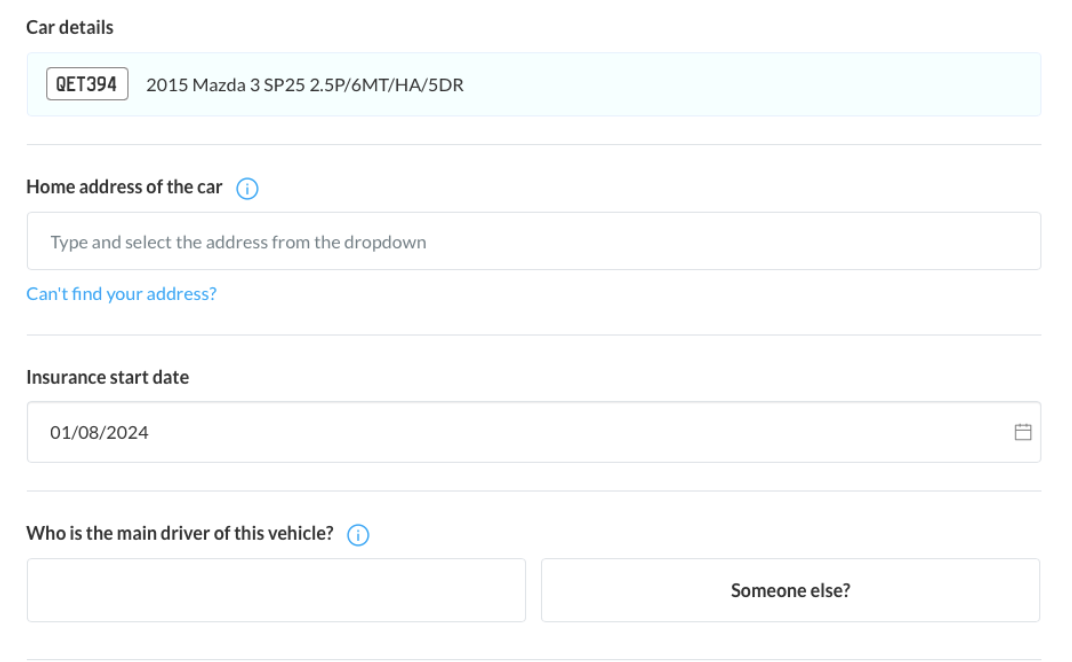

3. Enter your details

Enter the details above to proceed to the next step. This information helps us understand where the car will be parked overnight and during the day, who the main driver is, and when you’d like the insurance to start.

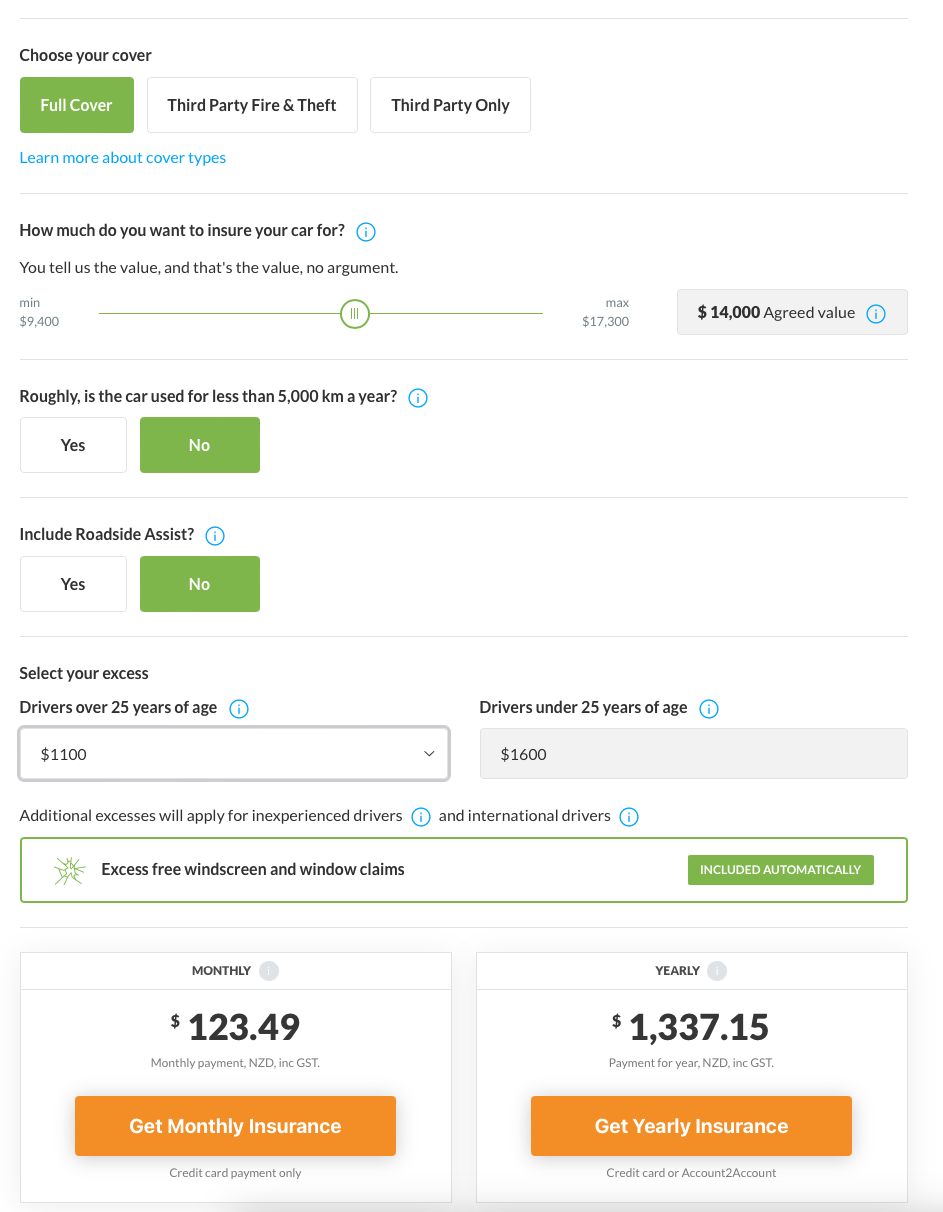

4. Select vehicle cover, customise quote & select payment option

For our vehicle insurance, we offer the following which include different policy extensions and exclusions:

- Comprehensive Full Cover

- Third Party – Fire & Theft

- Third Party Only

5. Enter vehicle details

6. Complete driver details

7. Sign the application form

To sign the application form, use your device keyboard to type your name in full (as the person completing the form) in the space provided.

8. Review and make payment

Once you have customised your insurance policy, you will need to select a payment option. For more information regarding our payment options, please refer to our support page, here.

There you have it! We will instantly email your confirmation documents.

Useful links

My Mortgage & Initio have teamed up to provide clients with house and contents insurance, and dedicated claims management when you need it. You can get a quick quote below, and cover can be started online.

Accidental damage is irksome, someone or something has damaged your property and it needs to be made right. Don’t worry, that’s what you’ve got home and contents insurance for and we’re here to help.

IMPORTANT: If your house is unsecured, unsafe or vulnerable to more damage, get a professional to make the house safe and we can work through the costs together later.

If you think your claim will be under $5,000, here’s what you need to do:

- Take photos of the damage.

- Get a quote to repair any damage.

- Log in your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach your photos and quotes.

- We’ll email or call you within one business day.

If the damage is severe, we might need an assessor’s opinion, here’s what you need to do:

- Log in to your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach any photos you’ve taken.

- We’ll email or call you within one business day.

FAQ’s:

- Can I use my own repairer or do initio have approved repairers that I must use?

You can use any repairer you like, as long as their costs are reasonable and you’re happy with the standard of work, then we’re happy.

- Who will pay my excess: me, or the person who damaged my house?

This is case-by-case. If a tenant caused the damage accidentally, then we cannot hold them responsible. However, if a neighbour accidentally drives through your fence, then we’ll probably be able to get the money back from their insurance company and your excess will be reimbursed to you.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

A stranger accidentally reversed their car into this garage door, damaging not only the door, but block work too. Initio worked with the property manager and repairer to get the door replaced and brickwork repaired efficiently and with as little fuss as possible to the tenants. Best of all, Initio didn’t charge an excess and recovered the costs from the driver.

Related articles

You have the right to cancel your insurance at any time. However, most insurance companies don’t advertise this fact, and sometimes they make it a bit difficult to leave them. We believe insurance companies should allow you to cancel and receive a refund as fast as they insure you, which is why our customers can cancel with the click of a button.

Will I get my money back?

Your insurance company must refund you the unused part of your premium (unless they have some hidden clause about keeping a certain percentage of your premium). So, if you cancel your annual house insurance policy halfway through the year, you should be refunded half the premium you paid.

You have paid a certain period of insurance, so if you don’t use all of that period (because you want to change insurers, you don’t want cover any more or you have sold your house for example) then you are entitled to receive back the cover you have not used

Will there be a cancellation fee?

It depends on the company. There may be a small fee for processing the cancellation, it should never be more than $30.

Initio does not charge cancellation fees. With initio, you can come and go as you please, and you get a full pro-rata refund of your insurance costs back if cancel a policy.

What do I need to do to cancel?

All you need to do is contact your insurance company and tell them to cancel your policy. Here are the steps:

STEP 1: First make sure your new insurance policy is in place (e.g. with initio). The initio platform allows you to place cover instantly on a day of your choosing up to a month in advance.

STEP 2: Call or email your insurance company telling them to cancel your policy from the date your new initio policy begins. We recommend providing:

- Full Name

- Policy Number(s)

- Address

- Cancellation Date (same date as start date of your new initio policy)

- Bank Account Number (for refund to be paid to)

STEP 3: Check your bank account to confirm the refund has been paid.

Having trouble contacting your insurer?

Get in touch with our support team who will be happy to help guide you through the cancellation process with your existing insurer.

Once you’ve completed the steps above and are ready to start your journey with initio, simply get a quote online, set your start date, and you’ll be covered in minutes. It’s fast, easy, and built for people who want insurance sorted without the faff.

Buy House Insurance

Related Articles:

Accidental damage is irksome, someone or something has damaged your property and it needs to be made right. Don’t worry, that’s what you’ve got home and contents insurance for and we’re here to help.

IMPORTANT: If your house is unsecured, unsafe or vulnerable to more damage, get a professional to make the house safe and we can work through the costs together later.

If you think your claim will be under $5,000, here’s what you need to do:

- Take photos of the damage.

- Get a quote to repair any damage.

- Log in your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach your photos and quotes.

- We’ll email or call you within one business day.

If the damage is severe, we might need an assessor’s opinion, here’s what you need to do:

- Log in to your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach any photos you’ve taken.

- We’ll email or call you within one business day.

FAQ’s:

- Can I use my own repairer or do initio have approved repairers that I must use?

You can use any repairer you like, as long as their costs are reasonable and you’re happy with the standard of work, then we’re happy.

- Who will pay my excess: me, or the person who damaged my house?

This is case-by-case. If a tenant caused the damage accidentally, then we cannot hold them responsible. However, if a neighbour accidentally drives through your fence, then we’ll probably be able to get the money back from their insurance company and your excess will be reimbursed to you.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

A stranger accidentally reversed their car into this garage door, damaging not only the door, but block work too. Initio worked with the property manager and repairer to get the door replaced and brickwork repaired efficiently and with as little fuss as possible to the tenants. Best of all, initio recovered the costs from the driver and refunded the excess to the insured.

Related articles

Paying your premium with initio is simple and hassle-free.

Monthly payments can be made using Visa or Mastercard (credit or debit). Annual policies have the additional options of online EFTPOS and Account2Account transfers for easy, secure bank payments.

Please note, initio does not currently offer direct debit OR manual transfers via your banking app or bank website. Our staff will therefore not be able to provide you with bank account information. Payment options are strictly limited to those outlined below.

Payment Frequency – We have options to pay either annually or monthly

Payment is required immediately upon the purchase of any policy. You can choose to either pay annually or monthly at that time. We do not offer other frequencies or payment terms. Paying the annual premium up front is more cost effective, this can be seen in the quoted amounts. Depending upon whether you are paying annually or monthly the following methods of payment are available;

Credit or Mastercard/Visa Debit Card (Monthly or Annual Policies)

Payment can be made online using your credit/visa debit card. We accept both Visa and Mastercard, including credit and visa debit cards.

- Monthly policies automatically renew and charge your card on the same day of each month.

- On an annual payment you purchase a years worth of insurance upfront (that you can cancel at anytime and get a refund for the un-used portion). Each year we will remind you when your policy is up for renewal and you will need to login to your dashboard to renew and pay for your policy

- There is no credit card fee applied to your insurance purchase.

Common Queries for Card Transactions

- Can I change from monthly to annual payments after I’ve started my cover? If you would like to change from a monthly renewing policy to an annual renewing policy you will need to set up a new quote from your dashboard and select the “pay annually” option before continuing to fill out your property details again. Unfortunately we cannot switch a monthly policy to an annual policy any other way at this time. After you have set up a new annual policy we can cancel your initial monthly policy and issue you a refund of any overpaid premium.

- Can I pay with American Express? No, we do not currently have an option for payment via American Express cards

- Do you charge a credit card fee? No, we do not.

- What if I need to change the card used for my monthly payments? This can be changed at anytime via your initio dashboard, please login, proceed to ‘account’ in the top right hand corner and then select ‘credit card’ to update.

- My monthly payment didn’t go through this month, how can I fix it? You can arrange for the payment to be re-tried by either contacting our support team, or updating your credit card details in your initio dashboard. When card details are updated, the system will automatically try to process any outstanding payment—even if you re-enter the same card details.

Account2Account Transfer (annual policies only)

An additional option is provided for annual policies where you can use your bank account login details to load an automatic transfer payment from your selected account using the Account2Account service. “Account2Account” is an online facility which processes payments directly from your account in real time, it creates a one-off online payment utilising the online banking system. The payment is set up via our policy purchase system, please choose the Account2Account option when you come to the initio payment screen.

To use Account2Account, your banking account must be with one of the following banks:

- ANZ

- ASB

- BNZ

- Kiwibank

- The Co-operative Bank

- TSB

- Westpac

For a demo and/or further information of how Account2Account transfers work, please see here.

Online EFTPOS (annual policies only)

Online EFTPOS is a modern payment method that lets you make online purchases through your bank’s mobile app. This secure payment solution connects directly to your bank account without requiring you to share sensitive banking details. Currently available to ANZ, ASB, BNZ, The Co-operative Bank and Westpac customers.

How to make a payment

-

- Choose your bank from the payment options

- Enter your mobile phone number

- Open your bank’s app and approve the payment notification

Key benefits

-

- Direct account-to-account transfers

- No need to share banking credentials

- Secure payment process

- Simple smartphone-based payments

Frequently asked questions

How secure is Online EFTPOS?

Online EFTPOS is one of the most secure payment methods available today. This is because it doesn’t ask you to enter your bank or payment details directly. Instead, you approve each payment through your bank’s app, adding an extra layer of security.

What is the maximum purchase limit for Online EFTPOS?

The purchase limit for Online EFTPOS depends on your bank:

-

- ANZ: $5,000 per transaction

- ASB: $5,000 per day

- BNZ: $12,000 per day

- Westpac: $5,000 per day (unless otherwise agreed with Westpac)

- Co-operative Bank: Flexible daily limit, based on your individual agreement with the bank

How long do I have to approve my payment?

You have 4 to 7 minutes from the time the payment request is sent to approve the transaction in your bank app.

Annual Payment Transaction Not Working?

It can be frustrating when your insurance payment doesn’t go through, especially if there’s money in your account. In most cases, the decline is coming from the bank rather than your insurance provider.

Below are the most common reasons this happens, and what you can do to fix it.

Two-factor authentication (2FA) approval required

Some banks require extra confirmation for payments now, especially larger or less frequent ones like an annual insurance premium. This is known as two-factor authentication, or 2FA. Instead of automatically approving the payment, your bank may pause it until you confirm it’s really you.

How this usually works:

-

- Your bank sends a push notification to your banking app, or

- You receive a one-time code by text, or

- You’re asked to approve the payment in-app or via internet banking

If the approval step is missed or times out, the payment may be declined. What you can do:

-

- Keep your phone nearby when making the payment

- Check your banking app and text messages for an approval request

- Make sure your bank has your correct mobile number

- If your bank uses an App, open the app and approve the transaction, then try the payment again

If you don’t see any approval request, contact your bank to check whether 2FA is required for this type of payment and whether anything is blocking it. Once the authentication step is completed, payments usually go through without issue.

Insufficient available funds – Even if your account balance looks fine, some of that money may be unavailable. This can happen if:

-

- There are pending transactions

- Your account has a hold or overdraft limit

- Funds are reserved for another payment

What you can do:

-

- Check your available balance, not just your total balance

- Wait for pending transactions to clear

- Transfer funds from another account if needed

Daily transaction or payment limits – Banks often place limits on how much can be paid in one transaction or within a day. What you can do:

-

- Check your daily payment or card limit in your banking app

- Temporarily increase the limit

- Contact your bank for help

Card security or fraud checks – Banks monitor card payments closely. Larger or less common payments, like an annual premium, can sometimes trigger a security block your block. This is one of their methods to protect you from scams. What you can do:

-

- Check for a notification from your bank

- Confirm the transaction is legitimate in your banking app

- Call your bank to remove the block

- Try the payment again once cleared

Expired or replaced card details – If your card has recently expired, been replaced, or reissued, the old details may no longer work. What you can do:

-

- Update your card details in your online dashboard

- Use your new card number and expiry date

- Make sure the name and CVV match exactly

Online or international payment restrictions – Some banks restrict online payments or certain merchant types by default. What you can do:

-

- Check that online payments are enabled on your card

- Ask your bank if any merchant restrictions apply

- Enable the payment type if it has been turned off

Temporary bank outages or system issues – Sometimes the issue is simply a temporary banking problem. What you can do:

-

- Wait a short time and try again

- Check your bank’s service status page

- Try a different payment method if available

What to do if your payment is declined

If your annual premium payment doesn’t go through:

-

- Check your bank account and card details first

- Look for messages from your bank

- Contact your bank if the reason isn’t clear

- Once resolved, log back in and retry the payment

- If you are still having issues please give our team a call to assist.

If you’re ever unsure, our team can help guide you on next steps and make sure your cover stays on track. Insurance payments should be simple, and most declines are quick to fix once you know the cause.

Want to switch between Monthly and Annual Payment Options?

For details on how to switch between monthly and annual payments, check out our article on ‘Switching Payment Frequency‘. For details on how to renew an existing annual initio policy and where to find that payment information, please check our this support article “How to renew your annual policy with initio”

Direct Debit?

Please note, initio does NOT currently offer direct debit as a payment option.

Get a quote

Useful links:

How to set up an account with a visa debit card

Does initio offer multi policy discounts?

Why has my house insurance premium changed?

How does initio get paid?

How to set up an account with a visa debit card

Switching your house insurance to initio is quick and easy, but timing is important to make sure you stay covered every step of the way. Here’s what to do and in what order.

1. Get your initio policy lined up first

Before you cancel your current policy, start a quote with initio. You can do this online in minutes. Once you’re happy with the cover and price, set the start date for your new policy.

- If you want your cover to roll over seamlessly, choose the day after your current policy ends.

- If your old policy ends at midnight, set your new one to start the next day, you don’t want a gap in cover.

2. Make sure the dates line up

Your current policy should stay active until your new one begins. Even a short gap could leave you without cover if something unexpected happens.

- Example: If your old policy ends on 14 June, set your initio policy to start on 15 June.

3. Sign up with initio

Once you’ve confirmed the start date, complete the sign-up online. You’ll get instant confirmation of cover and policy documents sent straight to your inbox.

4. Cancel your old insurance

When your initio policy is locked in, contact your old insurance provider to cancel your policy from the day your new cover starts. Most providers will refund the unused portion of your premium if you’ve paid in advance.

- Be prepared for them to ask for proof of your new cover (you can email them your initio confirmation).

5. Double-check everything

Before your initio policy starts, check that:

- Your start date is correct

- You’ve got confirmation that your old policy is ending on the right date

- You’ve downloaded and saved your initio policy documents

Tip: If you’re unsure about dates, start your new policy a couple of days before your old one ends — a small overlap is better than no cover.

Get a quote

Useful Links

Help with adding more than one property to your cover

If you own more than one rental property, you might be wondering how landlord insurance for multiple rentals works. With initio, it’s simple – you can manage all your insured rentals under one dashboard, add new properties when you’re ready, and keep your cover consistent across your portfolio.

If I want to add more than one property, do I need separate quotes and invoices?

You can buy your first policy online, then add more properties from your initio dashboard by selecting the “House insurance +” button. Here’s a step-by-step guide to navigating the initio dashboard.

Each property usually needs its own quote, so the right details and cover apply to that address. If you own a block of connected flats or units (up to 8 units) on standard residential leases, you could look at our Multi-Unit Rental policy, which covers the whole block under one policy.

Can I pay with a different account for each of my rental policies?

If you’re paying monthly, initio can only hold one card per account to cover all monthly policy payments. To use a different card for a specific monthly policy, you’d need to set up a separate initio account under a different email.

If you’re paying annually, you can choose a different card for each policy at the time you buy it.

Learn more here: Common Queries and How monthly insurance works.

“When managing landlord insurance with multiple rentals, it’s a good idea to review each property’s cover once a year. Different homes can have different risks – like flood zones, tenant types, or rebuild values – so checking that your sum insured and excess still make sense helps ensure you’re not under- or over-insured. Keeping your details up to date also means any claims can be processed faster and without surprises.”

If you get stuck while adding another property or managing multiple rental insurance, help is only a click away. You can chat with Chad, our friendly digital assistant, directly on the initio website for quick answers and step-by-step guidance. Just click on the ‘help’ button at the bottom of the screen to get started. If you’d prefer to talk to a real person, our support team is always happy to help – just head to our contact us page to get in touch.

Related articles

Reduce your insurance costs by insuring online, and know that Frank has got your back with support and claims management.

Get a quick quote and start your cover

With First Lane you can insure your rental property, house or holiday home insurance online. Enter your property details to get an instant quote, if you like what you see you can start cover online with payment by credit card or bank transfer.

Scenario: Existing client of yours that has a house(s) insured with initio, processed through broker software (e.g. eGlobal), and policy is due to expire.

Getting your client online is easy with initio

- Use your Broker landing page to quote your customer’s house

- Choose the relevant property type (own home, rental, holiday home)

- See instant quote on screen. From the quote screen email yourself the quote

- Select the start date of insurance (ie expiry date of current cover)

- Set the sum insured to the expiring amount or amount already discussed with your client.

- Click ‘Save & email this quote’.

- Enter your client’s name and then your email address.

- Separately email your client your pre-renewal email. Your email will say that they can continue to insure with initio but that it will need to be started and paid for online through a collaboration with your firm and initio.

- This email will include the initio premium and may include other traditional offline options.

- It may include an explanation of changes in premium, levies etc. compared to last year.

- It will include a request of how the client would like proceed.

- If your client elects to continue to insure with initio (online), then you will need to email initio [email protected] and request that an existing client is onboarded. You will need to provide the relevant info (as per the detailed offline to online document) in order for initio to onboard

- Initio will onboard your client by setting up an account and loading the policies, subject to payment.

- Initio will email you the login details for you to send to the client.

- You then just need to email your client with the login details and advise them that once logged in they will see the house policies ready to activate. The customer will need to make a payment to activate the policies.

Loss of rent insurance helps protect your rental income if your property cannot be lived in or your tenant stops paying rent. Under initio’s landlord insurance, loss of rent cover is included automatically. This guide explains when it applies, how much cover you get, and what is not covered. This can also be included in our holiday home cover if you also rent your bach to guests.

Quick summary

-

Loss of rent is automatically included with landlord insurance.

-

Standard cover is $20,000, with options to increase to $40,000 or $80,000.

-

Cover applies if damage makes the property uninhabitable.

-

Cover may also apply after tenant eviction or abandonment.

-

Overdue rent before eviction is not covered.

-

Holiday homes have cover for cancelled guest bookings due to damage.

What is loss of rent insurance?

Loss of rent cover replaces rental income when you cannot collect rent due to certain insured events. This usually happens when:

-

Damage makes your property unliveable, or

-

A tenant is evicted for non-payment, or

-

A tenant leaves without notice.

It helps reduce financial pressure while you repair the property or secure a new tenant.

How much loss of rent cover do I get?

Landlord insurance includes $20,000 of loss of rent cover as standard.

You can increase this to:

For property damage claims, payments stop when:

-

Repairs are complete and the property can be rented again, or

-

You reach your selected cover limit, or

-

12 months of rent has been paid,

whichever happens first.

When does loss of rent cover apply?

Property damage that makes the home uninhabitable

If claimable damage means your tenants must move out, loss of rent cover replaces the rental income during repairs.

Example: A flood damages carpets and internal walls. Your tenants move out while repairs are completed. Loss of rent cover replaces the rent you would have received during that period.

Cover is paid until the property is liveable again, up to your selected limit or 12 months.

Tenant eviction for non-payment of rent

If a tenant is more than 21 days behind in rent, you may apply to the Tenancy Tribunal for eviction.

Once the tenant is evicted, landlord protection under your policy can pay up to 6 weeks of rent, or until you find a new tenant, whichever comes first.

-

Overdue rent (arrears) before eviction is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations under the policy.

Tenant leaves without notice

If a tenant vacates the property unexpectedly and stops paying rent without giving the required notice, the policy can pay up to 6 weeks of lost rent, or until a new tenant is secured, whichever comes first.

-

Normal vacancy between tenancies is not covered.

-

Your selected property excess applies.

-

You must be meeting your landlord obligations.

Does loss of rent apply to holiday homes?

Yes. If you rent out your holiday home to paying guests, loss of rent protection is included.

Holiday home damage and cancelled bookings

If claimable damage makes the property uninhabitable, we will cover lost rental income from cancelled guest bookings.

You automatically receive:

Payments may consider:

-

Confirmed bookings that must be cancelled.

-

Expected future bookings, using previous rental income history where appropriate.

The maximum payment is your selected limit or 12 months, whichever comes first.

What does not apply to holiday homes?

The 6-week tenant eviction or abandonment benefit does not apply to holiday homes, as short-term guests do not have formal tenancy agreements.

What is not covered?

Loss of rent cover does not include:

-

Rent arrears before eviction.

-

Normal vacancy between tenants.

-

Guest cancellations unrelated to claimable damage.

-

Eviction benefits for holiday homes.

Always ensure you are meeting your landlord obligations under the policy.

Frequently asked questions

Does landlord insurance cover unpaid rent?

It may cover rent after eviction or abandonment, but it does not cover overdue rent before eviction.

How long is loss of rent paid for?

For property damage, up to 12 months or your selected limit. For eviction or abandonment, up to 6 weeks.

Do I need to add loss of rent cover separately?

No. It is automatically included in landlord insurance and holiday home cover (if rented).

Related Articles:

Owning multiple properties can sometimes make insurance decisions tricky, especially for New Zealand homeowners who use their homes differently throughout the week. For example, you might have one home you stay in during the weekdays and another you visit mostly on weekends.

Understanding the right insurance policy for each property is crucial to ensure you’re fully covered.

The main difference between holiday home insurance and own home insurance lies in the occupancy and associated risks. Own Home insurance is for your primary residence where you would reside the majority of the home, not generally suitable if you leave it vacant for periods of 60 consecutive days or more. Holiday homes are not primary residences and are often empty for reasonable periods, increasing risks such as break-ins. Therefore, holiday home insurance has specific conditions and coverage tailored to these unique risks. If you aren’t using your holiday home all year round, you might rent it out between stays.

The following is a list of cover specific to each type of policy to help you determine which is the best policy for your property:

Holiday home insurance specific cover:

- Optional – Guests: Cover for damage, theft, and loss of rent if you host guests.

- Fixed contents: $20,000 standard cover for fixed contents at the home, with options to increase. This covers furniture that stays in your home permanently (not personal belongings). Cover is limited to the property address.

- Blocked pipes: Up to $1,000 to unblock an underground pipe, with no excess.

- Keys and locks: Up to $1,000 for replacing keys and associated locks, with no excess.

- Legal liability: $2 million legal liability costs if an accident damages other property or people.

- Optional – Loss of rent: Up to 12 months or $20,000 following damage to your house.

Own home insurance specific cover:

- Personal contents (available as an add-on to any Own Home policy): Replace or repair lost or damaged belongings, majority of items are insured on a new-for-old basis. Includes cover for contents including personal effects whilst at the property and temporarily removed anywhere in New Zealand.

- Temporary accommodation: $20,000 of alternative accommodation if your damaged house can’t be lived in.

- Reduced glass breakage excess: Reduced $250 excess for glass breakage claims.

What if you split your time equally between two homes?

If you divide your time equally between two homes, each property may require different insurance considerations. The home you use during the weekdays might need a standard home insurance policy, while the one you visit on weekends could be classified as a holiday home, or potentially you may need two Own Home (owner occupied) policies. It’s crucial to assess the specific usage patterns of each property to ensure you have the appropriate coverage. This should also take what belongings you use the majority of the time at each property into consideration.

Holiday home or rental?

Provided you use the home as your holiday home we can also offer the option of including short-term rental cover for you. If this describes your situation, select ‘Holiday Home – sometimes rented’ from the dropdown menu, and initio’s clever software will do the rest. If you’re not sure which cover is best for you – we’re here to help.

What special terms apply (regarding vacancy) on each policy?

Holiday Homes:

If no one has been living or holidaying at the home for a period of more than 60 consecutive days, and the home is recorded as a holiday home, expectations are that the following criteria can be met:

- the home is inspected inside and outside by you or a nominated person at least every 60 days, and

- the home and its grounds are adequately maintained, mail is cleared regularly and

- the water supply is turned off and

- all doors are locked and windows secured

If you are unable to meet those conditions, cover will continue with a higher standard excess of $5,000 applying to any claim. If however, a loss results from a break-in or attempted break-in at the home while it is fitted with an active, professionally-installed alarm or security system, then an excess of $1,000 applies.

Own Homes (primary residence):

If no one has been living at the home for a period of more than 60 consecutive days, we will only pay for loss that is:

- caused by fire, explosion or lightning, or

- covered under the ‘Natural disaster’ automatic additional benefit.

These terms can be reviewed upon request for special circumstances.

What if I only use the house for guests?

Under our cover, you need to use the house at least occasionally yourself over the course of a typical year. If you;

- don’t use the house yourself as your holiday home and as such also

- don’t keep personal items at the home, and

- it is only rented to short-term guests,

it is considered a commercial operation, similar to a motel. Our cover is domestic-based house insurance, and cannot be used if the above requirements are not met.

Are my personal contents covered under a holiday home policy?

Your personal contents items, like phones, jewellery, and laptops, won’t be covered under your holiday home cover as they should be protected by your contents cover at your main home. Belongings that remain at your holiday home, like furniture, TVs, and glassware, are covered. You can only insure your personal contents with initio as an add-on to an owner-occupied home you also insure with us.

What else can you do to ensure you choose the best insurance provider for your needs?

When researching and comparing insurance providers, it’s essential to evaluate them based on their reputation, customer satisfaction, and claims processing efficiency. Reading customer reviews and testimonials can provide valuable insights into real-world experiences with different insurers. Additionally, carefully reviewing policy details, such as coverage limits, exclusions, excess amounts, and additional features, is crucial. Don’t hesitate to ask questions or seek clarification on any confusing terms or conditions.

Key takeaways

- Tailored insurance coverage: Ensure each property has the appropriate insurance policy based on its usage, whether it’s a primary residence or a holiday home.

- Personal belongings: Secure and appropriately insure personal belongings at both properties, ensuring valuables are covered and managed efficiently.

- Maintenance and security: Maintain regular upkeep and robust security measures for both homes to prevent risks associated with extended vacancies.

- Be aware of policy restrictions/conditions relating to how long a home is vacant for.

- Thoroughly research and compare to make an informed decision.

USEFUL LINKS

Choosing the right insurance excess can feel confusing. Your excess is the amount you pay towards a claim before your insurer contributes.

Understanding how excess works helps you balance your annual premium against what you would need to pay if something goes wrong.

Quick summary

-

An excess is the amount you pay when you make a claim.

-

A higher excess usually lowers your annual premium.

-

A lower excess usually increases your premium.

-

An excess applies per incident.

-

The right choice depends on your financial situation and risk tolerance.

What is an insurance excess?

An insurance excess is the portion of a claim you pay yourself.

For example, if you have a $1,000 excess and make a $10,000 claim, you pay $1,000 and your insurer pays the remaining $9,000.

Excess applies per incident. If multiple separate incidents occur, more than one excess may apply.

High excess vs low excess

When selecting an excess, you are balancing two costs:

High excess

Low excess

A higher excess can work well if you are financially able to fund the excess and want to protect yourself mainly against major events.

How insurers calculate excess levels

Insurers use claims data and risk modelling to determine how excess levels affect premiums. They analyse:

-

How often claims occur

-

The average size of claims

-

Risk trends in different regions

-

Historical claims behaviour

The balance between premium reduction and excess size is based on these numbers. While some policyholders expect larger premium discounts for higher excesses, insurers must maintain a balance between premiums collected and claims paid.

When does a higher excess make sense?

Insurance is most valuable for significant events such as fires, floods or earthquakes.

Some property owners prefer a higher excess, such as $1,150 or $2,000, because they:

-

Are less concerned about small claims

-

Want lower annual premiums

-

Have the savings available to fund the excess

For landlord or owner-occupied properties, the highest available excess option is currently $2,000.

A practical example

Consider an Auckland property with a $700,000 replacement value.

-

With a $400 excess, the annual premium may be around $2,000.

-

With a $2,000 excess, the premium may reduce to around $1,500.

That saves $500 per year. However, if you make a $10,000 claim:

-

With a $400 excess, you pay $400.

-

With a $2,000 excess, you pay $2,000.

In that scenario, the higher excess leaves you approximately $1,100 worse off after factoring in the premium saving.

Over time, if you rarely claim, the savings from a higher excess can accumulate. The key question is whether you can comfortably afford the excess if a claim occurs.

Is choosing a high excess a form of self-insurance?

Yes, in a sense.

Selecting a higher excess means you are sharing more of the risk with your insurer. You are effectively self-insuring smaller losses while relying on insurance for large, financially stressful events.

Your personal circumstances matter

The right excess depends on:

-

Whether you are a homeowner or landlord

-

Your cash flow and savings

-

The age and condition of your property

-

Your claims history

-

Your tolerance for financial risk

New homeowners or landlords may prefer lower excesses for certainty. More experienced property owners, particularly those with multiple properties, may choose higher excesses to manage long-term premium costs.

How data can help your decision

Claims probability plays a role in choosing an excess.

For example, if you own 10 properties, statistics suggest you may expect at least one reasonable claim each year across the portfolio.

Understanding the following can help you make a more informed decision about your excess level:

-

Local weather patterns

-

Crime rates

-

Property condition

-

Historical claims data

Frequently asked questions about insurance excess

Does excess apply per claim?

Yes. An excess is applied per incident. If multiple incidents occur, more than one excess may apply.

Does choosing a higher excess always save money?

It reduces your premium, but may cost more overall if you claim frequently.

What is the highest excess available?

The highest available excess for landlord and owner-occupied properties is currently $2,000.

Should landlords choose a higher excess?

Some landlords with multiple properties prefer higher excesses to reduce premiums, but this depends on financial flexibility.

Making a confident decision

Insurance excess is about balance. It is not about choosing the lowest premium or the lowest out-of-pocket cost. It is about selecting an amount that matches your financial comfort level and long-term strategy.

Understanding how excess works allows you to make a clear, informed decision rather than guessing.

You might also be interested in:

Landlord Insurance is designed specifically for rental property owners. It protects not only the house itself, but also the additional risks that come with renting to tenants. Unlike standard house insurance, landlord insurance includes cover for tenant damage, loss of rent and other landlord-specific exposures.

What is landlord insurance?

Landlord insurance is a specialised policy for long-term residential rental properties. It covers the physical building against events like fire, floods, and earthquakes, while also protecting landlords from risks that do not apply to owner-occupied homes.

While standard house insurance focuses on homeowner risks, landlord insurance extends cover to include tenant-related damage, rental income loss, eviction scenarios and other risks unique to renting out your property.

Quick summary

-

Landlord insurance covers rental property risks not included in standard house insurance.

-

Includes tenant damage, intentional damage and vandalism.

-

Covers loss of rent due to damage, eviction or abandonment.

-

Includes meth testing and cleaning cover.

-

Provides automatic landlord contents cover.

-

Designed for long-term residential rental properties in NZ.

What extra cover does Landlord Insurance provide?

Damage by Tenants Loss of Rents Meth Contamination Landlord Contents

Tenant damage cover

Standard house insurance may cover accidental damage caused by tenants, but it does not cover intentional damage.

Landlord insurance protects you against both accidental and intentional tenant damage. This includes vandalism, theft, and deliberate damage such as holes punched in walls or damage from unruly gatherings.

Under our landlord insurance policy :

-

Accidental tenant damage is covered up to your full sum insured.

-

Intentional damage, vandalism or theft is covered up to $25,000 per event.

-

Serious fire or explosion damage is covered above the $25,000 limit and up to your full property sum insured.

Cover applies to damage caused by your tenant, paying guests, or anyone occupying the home, including their guests.

Loss of rent cover

Rental income is essential for most landlords. If your property cannot be rented, you may still have mortgage payments and other costs to meet. Landlord insurance includes loss of rent protection in two main scenarios:

Loss of rent due to property damage

If physical damage makes your rental unlivable, we cover:

-

Up to 52 weeks of rent, or

-

The loss of rent sum insured you select, whichever comes first.

We automatically include $20,000 of loss of rent cover in all landlord policies, with options to increase this to $40,000 or $80,000.

This applies while repairs are completed following insured damage, such as flood or fire.

Loss of rent due to eviction or abandonment

Loss of rent can also arise when there is no physical damage. If your tenant:

-

Is evicted for non-payment after falling 21 days behind, or

-

Leaves without giving the required notice, we cover lost rent for up to six weeks.

This also extends to situations where tenants can legally cease rent payments under their tenancy agreement, such as when access to the property is prevented or essential utilities fail.

Meth contamination cover

Meth contamination is a serious risk for landlords in New Zealand. Cleaning a contaminated property can cost tens of thousands of dollars and may render the home unlivable for months.

Standard house insurance does not cover meth contamination. Landlord insurance includes cover for:

Meth cover with initio

We provide up to $30,000 for meth testing and cleaning costs.

Loss of rent cover applies over and above this $30,000 limit. We will pay your weekly rent while the property is being cleaned, for up to 52 weeks or up to your selected loss of rent sum insured.

You might also be interested in:

Landlord contents cover

Many rental properties are furnished or partially furnished. This can include appliances, curtains, rugs, heaters and other non-fixed items. Some landlord policies require contents to be added separately. Our landlord policy automatically includes contents cover.

How much landlord contents cover is included?

We include $20,000 of landlord contents cover as standard. This is the minimum level and cannot be reduced.

If your property is more fully furnished, you can increase this to $40,000 or $60,000.

What is covered?

Cover applies to fixtures and fittings and landlord-owned contents included in the tenancy.

This does not cover your personal belongings.

Frequently asked questions about landlord insurance

Can I reduce the $20,000 landlord contents limit?

No. The $20,000 landlord contents cover is automatically included as the minimum under our landlord policy. This amount cannot be reduced. You are covered for landlord contents up to that figure as standard, with options to increase the limit for more fully furnished properties.

Is furnished property covered under landlord insurance?

Yes. Whether your rental property is furnished or unfurnished, it is covered.

Landlord insurance automatically includes cover for landlord contents such as non-fixed appliances, curtains, rugs and heaters. If the property is fully furnished, you can increase the contents limit to ensure everything is adequately protected

Does landlord insurance cover intentional tenant damage?

Yes. Our landlord insurance policy covers intentional damage caused by tenants.

Intentional damage, vandalism or theft by tenants is covered up to $25,000 per event. In cases of serious fire or explosion damage, cover can extend beyond this limit and up to your full property sum insured.

More information about landlord insurance

Explore these additional articles that may interest you:

What can be insured under our Multi Unit Rental Policy?

At initio we have a multi-unit rental policy which was designed to insure a block of flats owned by a single landlord. For the purposes of this policy, a Multi-Unit Rental Property is defined as;

- two or more units, townhouses or flats that are combined under one building, so connected under the same roof or are physically connected in some other way (e.g. car-port or deck) and

- with each unit being self contained and

- having the same owner and

- on a standard long-term residential lease

Some examples of multi-units that we can insure under this policy are;

- a two story house where each level has a separate tenancy

- a block of flats owned by one person/entity – up to 8 units

- cross lease units, connected by a carport

- duplex townhouses

- rental house with physically attached self contained studio / granny flat – also rented out

There are some limitations as to what the multi unit properties we can insure.

- We cannot insure more than 8 units.

- We cannot insure properties that are more than 3 stories.

- The tenancies must not be short term or holiday lets.

- The property must be residential use only.

- We cannot insure individual or multiple units that form part of a body corporate.

- We cannot insure more than one rental unit at different addresses under this policy.

Related Articles:

Homes that are rented out to short-staying paying guests are experiencing booking cancellations and reduced occupancy (loss of income) due to fears and government restrictions relating to Covid-19. We take a look at whether insurance provides cover.

Covid-19, also known as the Coronavirus has caused major impact to visitor travel arrangements. The reduced sentiment to travel as well as New Zealand’s move to protect itself from the rest of world with Government imposed restrictions on travel and self-isolation will and has lead to holiday home (Bookabach, AirBnB etc) cancellations and reduced future bookings.

So, as a AirBnB or Bookabach property owner is there insurance for loss of income where there is no physical damage to the property?

The short answer is No. Let’s explain;

- Most insurance policies include a Loss of Rents provision that specifies an amount of cover (e.g. $20,000) and a payment period (e.g. 12 months)

- This cover is triggered by a physical loss to the home or property that results in house being unliveable.

- Some common examples include, a fire at the property, a burst pipe that floods the house, earthquake damage or rising flood waters.

- The policy responds to cover the damage from these things and also the associated loss of rental income while the damage is being repaired.

- So, if the property is a holiday home and is damaged the loss of income would include the confirmed bookings you know about that need to be cancelled, and the other future bookings you miss because the property is not available to be booked. Its the perfect solution…. until non-physical things like Covid-19 come long.

No physical damage – the Covid situation

As Coronavirus (or any other illness, virus or disease for that matter) does not cause any physical loss to the property, it does not trigger the loss of rents cover. The key component for cover is missing.

But wait, what about cover loss of rents due to tenant eviction and prevention of access and the like – that’s not physical damage? Yes, some policies like Initio, have a special benefits that provide loss of rental income cover from other causes that are not necessarily physical.

The one that is most relevant here is the ‘prevention of access’ policy benefit. Prevention of access relates to not being able to access the property, and typically comes in the form of a road closure or a washed out driveway for example. While Covid-19 is causing bookings to be cancelled, access to the property is not actually prevented, meaning that this part of the cover does not provide any assistance for Corona virus related income losses.

It is also important to note that most house insurance policies out-rightly exclude cover for “financial loss or expense of any type in connection with a Notifiable Infectious Disease under the Health Act 1956”.

While this provides little comfort to holiday home and own home owners who rent out their properties to short term guests, it does mean that home owners can make informed decisions about how to manage their lower income risk over the coming months.

About Initio

Initio is a New Zealand-based online house insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home and contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with built-in cover for loss of rent and damage by the tenant.

Having completed over 35,000 automated insurance transactions, Initio’s market-leading policies can be quoted, bought and amended online – all in an instant.

Initio is underwritten by NZI, a business division of IAG New Zealand Limited.