Search results for: {search_term_string}/get-quote/house-insurance-calculator

On the questions of: how does Initio make money? Does Initio charge fees? It is first important to know what type of business initio is:

Initio is an Underwriting Agency of registered insurer IAG. Initio is not an insurance company in its own right. This means that initio has delegated authority from the insurer to establish and manage insurance for houses, contents and cars. In addition, Initio has authority to pay claims on behalf of the insurer.

Initio is a licensed Financial Advice Provider under the Financial Markets Authority of New Zealand. Initio have staff who are Registered Financial Advisors, which enables initio to provide customers with insurance advice specific to their situation.

On the sale of an insurance policy, including its subsequent renewal, initio is remunerated by commission and fees. The commission is a payment that recognises the cost of delivering such functions, administration, and services that would otherwise be a cost to the insurer, and the fee is a transaction and platform fee designed to recover costs associated with transaction processing including bank and payment provider processing costs, credit card merchant charges, and obtaining property risk and vehicle data, and regulated financial advice. For details of charges and remuneration see our disclosure statement, and/or refer to the quote and invoice when transacting with us.

Related Articles

Initio’s landlord insurance policy requires landlords to meet the ‘Landlord Obligations’ for cover under the Landlord Protection and Meth Contamination extensions. The cover in these extensions are:

Landlord’s Protection

- Malicious damage by tenants, and associated loss of rents.

- Theft by tenants.

- Loss of Rent following a tenant vacating the property.

- Loss of Rent following a tenant eviction for non-payment of rent.

- Meth Contamination, and associated loss of rents.

If a landlord has a property manager, it is usually the property manager’s responsibility to meet the obligations. Otherwise, the landlord will need to meet these themselves.

If you don’t meet the Landlord’s Obligations all the standard cover included in the policy remains in place. You are still covered for natural disasters such as an earthquake as this does not involve the risk of the tenant. However, if you do NOT meet the obligations but then lodge a claim for meth contamination at your property, your claim may be declined.

Landlord’s Obligations

You, or the person who manages the tenancy on your behalf, must:

- Exercise reasonable care in the selection of the tenant(s) by at least obtaining satisfactory identification and written or verbal references for each adult tenant and when a reasonable landlord would consider it appropriate also check their credit and Tenancy Tribunal history.

- Keep written records of pre-tenancy checks conducted for each adult tenant, and provide to us a copy of these if we request it.

- Collect a total of 3 weeks’ rent in any combination of rent in advance and bond that will be registered with Tenancy Services.

- Complete an internal and external inspection of the home at a minimum of 3-monthly intervals at the relevant residential dwelling upon every change of tenant(s).

- Keep photographs and a written record of the outcome of each inspection, and provide us a copy of these if we request it.

- Monitor rents on a weekly basis with written notification being sent to the tenant(s) whenever rent is 14 days in arrears, together with a personal visit to determine if the tenant(s) remains in residence.

- Make application to the Tenancy Tribunal for vacant possession in accordance with the provisions of the Residential Tenancies Act 1986 if:

(a) the rent is 21 days in arrears, or

(b) you become aware of any illegal activity by the occupant(s) at the home, or

(c) intentional damage to the home is caused by the occupant(s).

What if the home is occupied by employees as part of their employment package?

If the home is provided to and occupied by your employee as part of their employment package with you, then obligations 3, 6. and 7.(a) do not apply.

What if this is my holiday home which is occasionally let to short term paying guests?

If the home is occupied by short-term paying guests such as a AirBnB or BookaBach, then the obligations do not apply to have cover for damage and theft by guests.

What if the home is occupied by Family Members?

You would need to decide if a Landlord policy is the right product for you. Are you wanting to cover Loss of Rents and Intentional Damage by Tenants? Does the family member pay rent? Get in touch with our support team to discuss the available options.

Protect your rental with initio’s landlord insurance

Get a quote in seconds

Related Articles:

Initio is pleased to announce that replacement contents insurance cover is available online. This means NEW for OLD replacement of your property’s contents. When you use our quote calculator to obtain a premium for your property you will also be given the choice of increasing your contents insurance cover [from $20,000 current value which comes for free] to either $60,000, $90,000 or $120,000. This cover is especially important for those of you who own holiday homes.

For our existing clients, the option to increase your contents cover is available when you renew your policy. Feel free to contact us if you would like to discuss your contents insurance.

All the same great benefits are extended to the contents cover as they are the home itself, including deliberate damage and theft by tenants / guests. Especially for holiday homes that are rented out, this is real risk – and as a property owner and landlord it a risk that is not worth taking.

Major losses to dwellings caused by fire and flood are all to common – just ask us, we have seen and paid significant claims on quite a few. Having been through this process with our clients it is imperative that you do not under-estimate the value of the contents in your property…. It adds up a lot quicker than you think. Have a walk around your property and make a quick list of some of the more significant items, beds, lounge suites, TVs, electronics, bikes, tools. Think about what it would cost to buy these new and to a tally on the cost; this is only the beginning – there are still all your clothes, and the pots and pans to include.

Feel free to call or email the initio team if you would like to discuss your contents insurance. Have a look at the online pricing. As always – with initio you can quote and start your cover online in a mater of minutes.

Accidental damage is irksome, someone or something has damaged your property and it needs to be made right. Don’t worry, that’s what you’ve got home and contents insurance for and we’re here to help.

IMPORTANT: If your house is unsecured, unsafe or vulnerable to more damage, get a professional to make the house safe and we can work through the costs together later.

If you think your claim will be under $5,000, here’s what you need to do:

- Take photos of the damage.

- Get a quote to repair any damage.

- Log in your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach your photos and quotes.

- We’ll email or call you within one business day.

If the damage is severe, we might need an assessor’s opinion, here’s what you need to do:

- Log in to your dashboard on the initio website and click on ‘Make a Claim’. Fill in the form and attach any photos you’ve taken.

- We’ll email or call you within one business day.

FAQ’s:

- Can I use my own repairer or do initio have approved repairers that I must use?

You can use any repairer you like, as long as their costs are reasonable and you’re happy with the standard of work, then we’re happy.

- Who will pay my excess: me, or the person who damaged my house?

This is case-by-case. If a tenant caused the damage accidentally, then we cannot hold them responsible. However, if a neighbour accidentally drives through your fence, then we’ll probably be able to get the money back from their insurance company and your excess will be reimbursed to you.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

A stranger accidentally reversed their car into this garage door, damaging not only the door, but block work too. Initio worked with the property manager and repairer to get the door replaced and brickwork repaired efficiently and with as little fuss as possible to the tenants. Best of all, initio recovered the costs from the driver and refunded the excess to the insured.

Related articles

What can be insured under our Multi Unit Rental Policy?

At initio we have a multi-unit rental policy which was designed to insure a block of flats owned by a single landlord. For the purposes of this policy, a Multi-Unit Rental Property is defined as;

- two or more units, townhouses or flats that are combined under one building, so connected under the same roof or are physically connected in some other way (e.g. car-port or deck) and

- with each unit being self contained and

- having the same owner and

- on a standard long-term residential lease

Some examples of multi-units that we can insure under this policy are;

- a two story house where each level has a separate tenancy

- a block of flats owned by one person/entity – up to 8 units

- cross lease units, connected by a carport

- duplex townhouses

- rental house with physically attached self contained studio / granny flat – also rented out

There are some limitations as to what the multi unit properties we can insure.

- We cannot insure more than 8 units.

- We cannot insure properties that are more than 3 stories.

- The tenancies must not be short term or holiday lets.

- The property must be residential use only.

- We cannot insure individual or multiple units that form part of a body corporate.

- We cannot insure more than one rental unit at different addresses under this policy.

Related Articles:

Navigating the intricacies of insuring a home with an attached flat in New Zealand, especially one that is rented out part-time, can be overwhelming for landlords and property investors. At Initio, we are dedicated to helping you make sense of these complexities, equipping you with the tools needed to make the right insurance choices for your unique situation. This article is specifically designed to assist you in understanding the process for homes with attached flats rented out occasionally.

Guidelines on Insuring Your Home and Attached Flat in NZ

If you happen to own a home with an attached flat rented out occasionally, you may find yourself unsure about how to secure the right insurance coverage. This situation differs from one where both units are exclusively used as long-term rentals (which are catered for by our multi-unit policy). Insuring a property where you live and have an attached flat rented out part-time necessitates a more nuanced approach.

Here’s what you need to know:

- Own Home policy: This policy has been crafted to cover the portion of the property that you inhabit.

- Landlord/Rental policy: This policy needs to be put in place to provide coverage for the attached flat when it’s rented out. Even if the rental isn’t full-time, coverage for the times when the flat is tenanted is ensured by the landlord/rental policy.

Should a significant claim arise, both policies would be engaged, with the combined sum insured being applicable to the whole property.

Why do I need Two Policies?

Each policy is designed specifically to cover one self-contained home/unit only and for the risks associated with the type of occupancy. The Own Home policy provides coverage for the main house/unit where you live, while the Landlord/Rental policy covers your rental home/unit including the legal liabilities and other specific risks associated with renting.

Conclusion

The process of insuring a home with an attached flat, rented out on occasion, needn’t be a difficult one. With an understanding of how Initio’s insurance products can be strategically combined, comprehensive protection of your property is ensured. Additional information on this topic, as well as other insurance solutions offered by Initio, can be found here.

Get a quote

Useful links

You can buy a policy today, and for a future effective date within the next 30 days. We’ll ask you to enter a cover start date on the initial quote page before proceeding to the application form.

Purchasing a new house

If you’ve purchased a house, you should set the cover start date as the same day as the settlement date for the purchase. This means your insurance will start when you own the house. We are unable to provide cover prior to the day you become the legal owner.

Changing your insurance company

If you’re changing to initio from another insurer, it’s a good idea to set the cover start date on your new initio policy to the day that your existing policy expires. This way, there is no period where you are not insured.

Ready to get your journey started with initio?

Get a quote

Related articles:

Found intentional damage at your rental property? Don’t worry, your Initio landlord insurance policy covers up to $25,000 of intentional damage by tenants. If you’ve found holes in walls, smashed windows, graffiti etc, please follow our below steps.

What you need to do

- Take photos of the damage – it helps us if scale is provided in the photos, take both close up and pulled back photos

- Get a quote to repair any damage – a room-by-room- itemised quote will speed up the settlement process

- Login to your initio dashboard and select ‘Make a Claim’ on the property. Complete our smart claims process and attach your photos and quotes.

- Hold tight. We will email or call within a business day to tell you what happens next.

- Consider applying to the tenancy tribunal for vacant possession, and to recover any uninsured losses.

Remember the more information the better. We will require other documents such as:

- Tenancy agreement

- The most recent 3 inspection reports

- Tenant references & application

- Or anything you might think is relevant

This can help us determine when damage occurred, and speed up our claims process for you.

What will we cover?

The intentional damage caused by the tenant is covered. However, bear in mind that insurance is designed to help you recover from unexpected sudden losses, but does not cover damage that has occurred throughout the tenancy. Like all insurance, an excess will apply to each damage incident.

If there has been damage from one event – such as an out of control tenant party – all the damage could be covered under one excess. However, if any of the damage has occurred throughout a tenancy, multiple excesses will apply.

What won’t we cover?

House insurance covers sudden and unexpected events. We understand that there can be other areas of damage or neglect to your property. Unfortunately, insurance cannot cover everything!

- Rent arrears

- Wear and tear

- Rot or other gradual deterioration

- Rubbish removal

- Cleaning costs

- Gardening costs

- Repairs under excess

- Removal of tenants belongings

Some of your ‘uninsured losses’ can be claimed back via the tenancy tribunal.

FAQ’s

Am I covered for loss of rent?

If the home is so badly damaged that it is deemed ‘uninhabitable’, you might be entitled to loss of rent. ‘Uninhabitable’ means unable to be lived in. For example, no access to kitchen or bathroom facilities, water or electricity. There is no cover for loss of rent if the repairs are just cosmetic (carpet/painting/plastering etc).

Will initio send an assessor?

If damage is significant and needs further examination we may get an assessor to your property. Usually, if the damage is likely to be under $5,000 then we are happy to proceed based on photographs and formal written quotations.

What is my excess?

Your standard policy excess will apply. This amount is chosen when you first purchase your policy. If you can’t remember, check your policy schedule which you can find on your dashboard.

Can I use my own repairer or does initio have companies I must use?

You can use any repairer or supplier you like as long as their costs are reasonable. Please make sure you are happy with the standard of work they provide.

Related Articles:

Methamphetamine contamination in a rental property can be an alarming and confusing time for property owners. There are conflicting theories on what levels are acceptable and what needs to be done to get the house livable again. Initio keeps it simple and adheres to the Ministry of Health Guidelines which state that any house reading more than 1.5mg of methamphetamine per 100 cm2 needs to be decontaminated.

If your short or long term rental property has tested positive for the presence of methamphetamine and you have house insurance with Initio, here’s what you need to do:

- If you haven’t already, you need to get a detailed room-by-room test completed. This will show you which specific areas of the house are contaminated.

- Log into your dashboard on the initio website and click on the make a claim button.

- Fill in the form and attach your test results.

- We’ll email or call you within one business day.

FAQ’s:

- Does my initio landlord insurance policy cover methamphetamine contamination?

Yes; however, the cover is specific and limited to $30,000:

Where the contamination damage occurs in connection with any tenancy or occupancy of:

- More than 90 days, there is no cover unless you, or the person who manages the tenancy on your behalf, have fully met the ‘landlord’s obligations’ under the ‘Policy conditions’; or

- 90 days or less, there is no cover unless the contamination damage was caused by an accidental incident in connection with the manufacture, distribution or storage (but only where the storage is in connection with supply or distribution) of methamphetamine at the home.

All methamphetamine contamination claims have a specific excess of $2,500.

- Can I start cleaning the house?

Not yet, please follow steps 1-3 above and then we’ll work together on getting the house livable again.

“All claims are different and they are assessed on their own merits and facts. The above does not imply a guaranteed approach to all such claims”

Methamphetamine is not a discriminatory drug … anyone could be using or manufacturing methamphetamine in your rental property … even your tenants!

Methamphetamine is not a discriminatory drug … anyone could be using or manufacturing methamphetamine in your rental property … even your tenants!

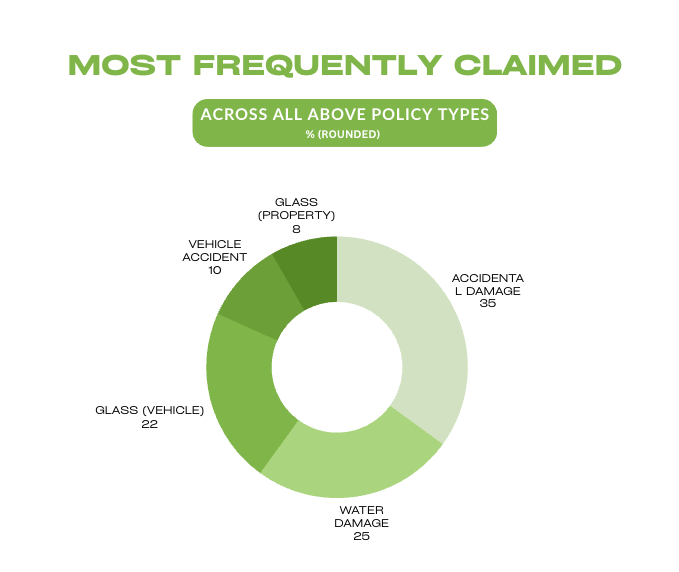

What claims cost the most, and what are the most common claims of 2024?

As we approach the end of 2024, we’ve taken a closer look at the trends in claims across the range of insurance policies we offer. The main ones being holiday homes, rental properties, owner-occupied homes and vehicles. Understanding these trends helps us, as your insurance provider, to stay on top of the risks that matter most to you – and also gives a bit of insight into what’s happening out there in the real world. Here’s a summary of what we’ve found.

Please note these figures only cover the most common categories. They are not an all-inclusive list and may not total 100%.

The most common claims this year

Across all policy types discussed in this article – Own Home, Holiday Home, Rental/Landlord, and Vehicle – two trends dominate: accidental damage and water damage.

Accidental damage is one of the most common types of insurance claims because it covers a wide range of unexpected scenarios. Accidents are often unavoidable, even with the best precautions, which is why having comprehensive insurance is so important. It ensures you’re protected from the financial impact of repairs or replacements, helping you get back to normal quickly without unnecessary stress.

Water damage, including hidden water damage, is another significant area of cover. Hidden water damage applies to gradual leaks from internal water pipes or tanks that aren’t visible. Coverage is subject to specific conditions and limits, so it’s worth understanding what’s included in your policy. Sudden water damage, such as from a burst pipe, is generally covered under most policies.

For more details about how we handle water damage, visit our water damage support page – it’s always good to know exactly what’s included.

For more information:

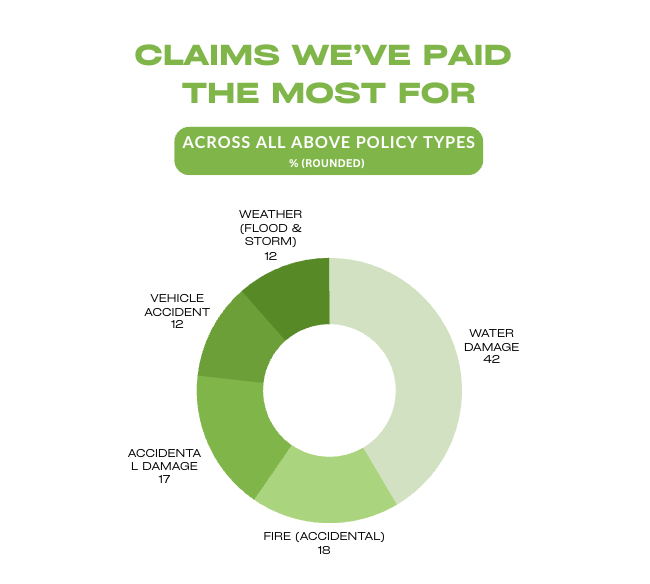

The most expensive claims across all policy types

While frequency tells one side of the story, cost paints a different picture. Here’s a look at the claims that we’ve paid out the most amount of money for this year:

Some key insights stand out when it comes to the costliest claims. Thankfully, weather-related claims have dropped a few spots this year, providing some much-needed relief.

While accidental damage was the most frequent reason for our claims, it accounts for just 10% of the total payouts – indicating many smaller, less costly incidents.

When accidental fires occur, they’re among the most financially costly claims. These events often result in extensive damage, sometimes requiring a complete rebuild of the home.

Prevention is always the best defence against accidental fires. Simple steps like never leaving candles or cooking unattended, regularly testing smoke alarms, and ensuring your electrical systems are safe can greatly reduce the risk. While the financial cost of a fire can be substantial, the threat to human lives is immeasurable.

For more information:

General insights by property type

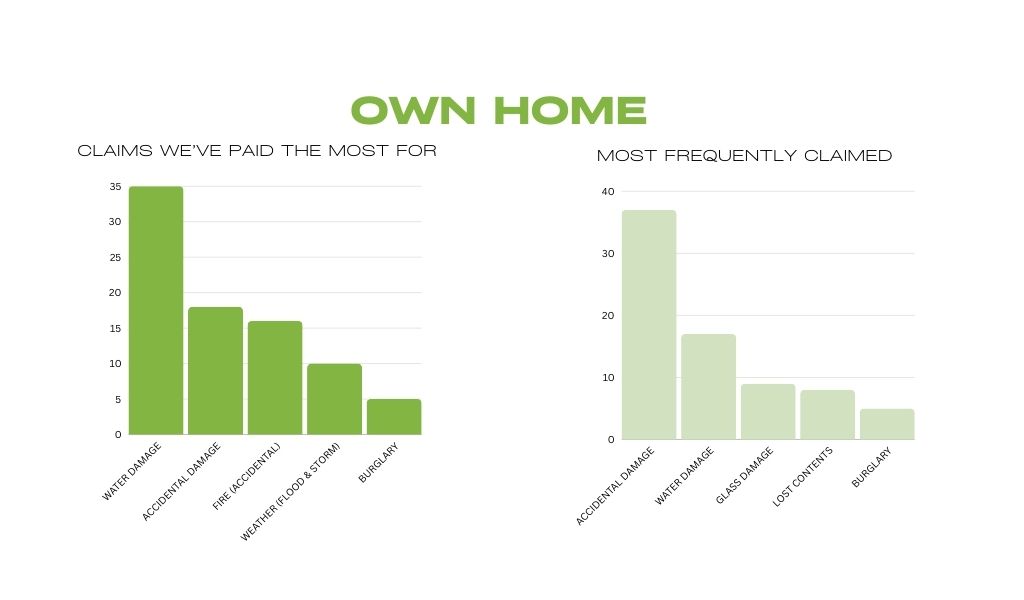

Own Home/Owner-Occupied

Weather has raised its ugly head again this year, but thankfully we’ve been spared the extreme damage experienced in 2023. Historically, summer is a season when storms and flooding can cause significant damage, so it’s a good time to take precautions to protect your property. If you’d like to learn more, check out our support articles for helpful tips and information:

Rental/Landlord

Similar to own home and holiday home insurance, water damage and accidental damage are the most common claims for rental properties. These issues often arise from the higher turnover of tenants or insufficient regular maintenance. What sets rental properties apart, however, is the added risk of loss of rent & malicious damage cover.

Learn more about these topics:

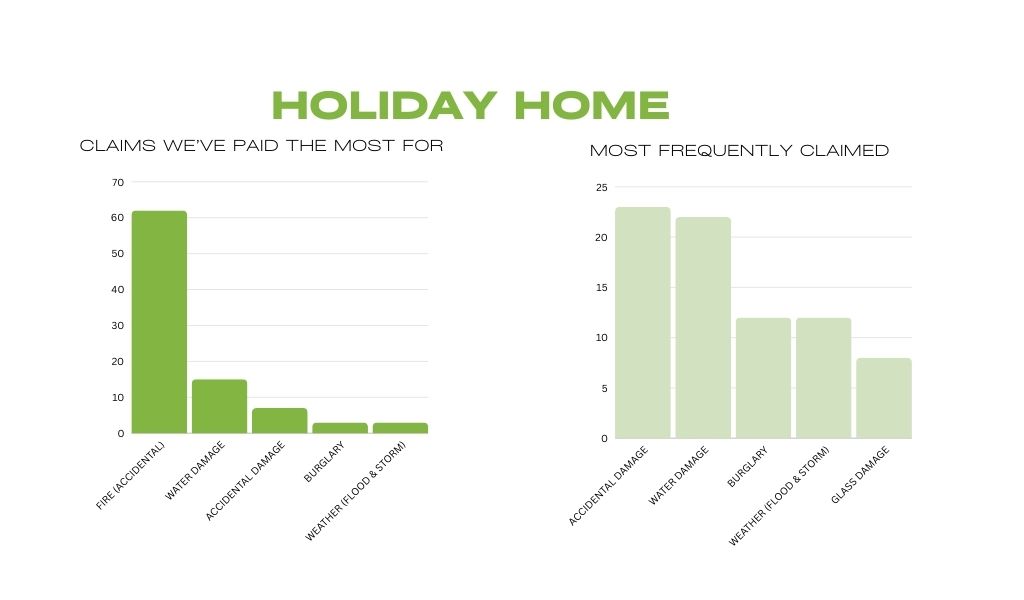

Holiday Home

After the usual suspects of accidental damage & water damage, these properties see a higher risk of burglary and weather-related claims. Being unoccupied for long stretches makes them vulnerable, particularly during storm seasons. Burglary ranks as the third most common issue. Our Holiday Home insurance basics article offers helpful tips on mitigating these risks.

For more information:

Vehicle

One of the main standouts in 2024 is glass damage – it’s the most common claim by far. These claims, while annoying and inconvenient, usually don’t cost much to fix.

When we look at the vehicle claims we’ve paid out the most for, major accident damage tops the list. The good news? The Roadside Assist portal is now available for vehicle customers who’ve added the Roadside Assist feature to their policy. If you haven’t added it yet and want to know more, you can start here.

Another common (and costly) culprit is damage from static collisions – when your car meets an immovable object.

For more information

Roadside Assist for initio vehicle customers

When we look at the vehicle claims we’ve paid out the most for, accident damage tops the list. The good news? Roadside Assist Online is now available for vehicle customers who’ve added the Roadside Assist feature to their policy. If you haven’t added it yet and want to know more, you can start here.

Another common (and costly) culprit is damage from static collisions – when your car meets an immovable object. And we hate to break it to you, but that pole you reversed into didn’t sneak up behind you.

For more information

What does this mean for you?

These trends highlight the importance of staying proactive with maintenance, securing your property, and ensuring your insurance is comprehensive enough to cover frequent and high-cost risks. As your insurance provider, we’re here to help – whether it’s providing advice on minimising risks or ensuring your cover matches your needs.

Did you find this interesting? You might also enjoy our article on the weird and wonderful claims from this past year.

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2024 (1 Dec 2023 – 27 Nov 2024), spanning our entire claims portfolio. Please note that all figures are approximate percentages, calculated to offer a representative overview of claim trends during this period. These figures only cover the most common categories. They are not an all-inclusive list and may not total 100%.

The requirement for 3 monthly property inspections forms part of most landlord insurance policies.

A rental property that is inspected regularly is less likely to be ill treated by its tenants, and if the property does suffer some damage it is easier to establish what and when it happened.

There is widespread debate among landlords, tenants, property managers and insurers as to whether 3 monthly inspections are too frequent and disruptive to tenants.

What is not well understood by landlords is that superior landlord insurance policies (like initio) provide insurance irrespective of whether property inspections are being completed or not.

So, here’s three things you need to know:

1. You are still insured if you don’t do property inspections

From an insurer’s perspective the landlord obligations are NOT a requirement to make ANY claim acceptable. At claim time, property inspection information will only requested when the claim is for a tenant related loss such as meth or malicious damage.

So if you are making a claim for intentional damage caused by the tenant or meth contamination – your insurer may ask to see copies of your property inspections. However, if your claim is for damage not related to the tenancy such as a burst water pipe, a storm blowing the roof off, an earthquake, or total loss house fire (to name just a few) the insurer will not be interested in your property inspections as they are not relevant.

2. 6 monthly inspections used to be the norm, until …. Meth.

It is only recently that insurers have moved to 3 monthly inspections. This is a direct consequence of the rising cost of methamphetamine contamination claims.

To put this in perspective, at its height Initio was receiving a new meth claim per day, and that cost a lot of money. We noticed that a large number of meth claims could have been avoided or at least mitigated by better risk management, namely more regular property inspections. So instead of pushing prices up further to offset this risk (or excluding meth cover all together) we decided that if landlords wanted ongoing meth cover they would need to take an active role in managing the risk through, among other things, property inspections.

Good insurers (like initio) will not use the landlord obligations as a way to avoid claims, but as a way to fast track claims for landlords with good risk management.

3. New Zealand Property Investors Federation members – 4 monthly inspections periods.

We are proud to be the insurance partner to the New Zealand Property Investors Federation (NZPIF). The NZPIF take an active role in professionalising property investing in New Zealand with knowledge, leadership and resources for members.

Our data shows that property investor members have approximately 50% lower incidence of meth and malicious damage claims, compared to non members.

Members of the NZPIF who insure with Initio receive the benefit of 4 monthly inspection periods. Visit NZPIF to find out more about organisation, including how to become a member of a local property investors association. Associate membership starts from just $25 per year.

Established in 2010, Initio is a digital insurance provider specialising in property insurance, including rental property insurance, landlord insurance, holiday homes, and home and contents. Customers can quote, start cover, modify cover and make claims – all online. Initio is underwritten by NZI (IAG New Zealand Ltd)

In most cases insurers won’t provide cover for houses that were sold under a mortgagee sale. This is because of the increased and known risk associated with this type of property sale. However, we know that all mortgagee sales are different so can consider cover on a case by case basis if some requirements are met. We can only consider cover from the settlement date of the property, not from the fall of the hammer/purchase date.

Mortgagee Sales are typically purchased on an “as is where is” condition, and often purchased without being inspected. The property is either left unoccupied which can add to the overall risk of the property, or the defaulting owner is still living in the property, which adds another level of complexity.

A major issue with the insurance of mortgagee sales houses is that the buyer can be required to insure the property before they are the legal owner. A condition is often applied to the sales agreement requiring insurance of the property from the “fall of the hammer”, i.e the date you agree to purchase the dwelling and not from the settlement date. It can be very difficult to get insurance cover from “fall of hammer”. Fall of the hammer cover, if you can get it, is normally for a short period only (up to 3 months), is provided by a offshore insurer, and will cost at least $3,000. The cover will also be limited to loss from weather damage, natural disaster, water damage and will not include cover for malicious damage.

Minimum requirements for insurers to consider cover

Insurance providers like Initio will generally only consider mortgagee sale cover for existing clients, and will provide cover from the settlement date not fall of the hammer. You will need to provide information on the following:

- Purchase date

- Settlement date

- Are you required to insure the home prior to the settlement date?

- Overall condition of the home

- Whether the current or previous owner lives in the house, if it is a rental, or empty

- Your intentions after settlement (e.g. moving in immediately, or putting tenants in after renovations etc.)

- Have the locks been changed? If not, when will they be changed?

Send your details to [email protected] and our team will get back to you.

There are a number of reasons why your premiums may have seen a recent rise. Some of those reasons are associated with passing on costs such as recent claims and securing reinsurance, but the most recent hike will be due to increases in government levies.

Levies are charges that are applied to insurance premiums and then paid to the government by insurers. They help cover the cost of services that benefit all New Zealanders, such as the Earthquake Commission and Fire and Emergency New Zealand. Sometimes these levies can make up half of the cost of house insurance . Effective from 1 July 2019 the Government Earthquake Levy (EQC Levy) increased by between $69 and $115 per house. Learn more about the EQC levy change here

In addition to this, many insurers (including initio) have now changed to a risk-based pricing model, which has affected how they calculate premiums. Instead of being spread across different areas, if you buy a risky home or a property in an area prone to disaster, for example, this risk will be reflected in a higher premium specifically for you.

Due to the increasing prevalence of extreme weather events, reinsurers are also re-examining New Zealand’s risk exposure to natural disasters. As a result, may insurance companies have begun pricing for seismic risk, flood risk and the effects of climate change.

Initio recently featured in the New Zealand Property investor magazine. Our policy and pricing was compared to all the mainstream insurance providers…. the result …. Initio provides some of the best landlord insurance cover in New Zealand. The initio policy extensions provide our clients with robust landlord insurance cover.

As well as providing extensive cover, the NZ property investor magazine proved that our premiums are the most competitive (at time of publishing).

Landlord insurance for your rental property online with initio insurance.

As 2025 comes to a close, we want to take a moment to reflect on some of the ways we’ve helped our customers this year. It’s been a year of quick claims and responsive support at initio – all driven by our core values of customer satisfaction, speed, and making insurance easy. From fast claim resolutions to lightning-quick answers on our support lines, 2025 showed what our team and technology can do to take care of you when it matters most.

Ways we’ve helped our customers with their claims

When it comes to insurance claims, we know you want a swift, clear outcome. In 2025, our claims team made sure “waiting around” was rarely part of the experience. Many claims were sorted out within just a day of being lodged – yes, some were literally resolved overnight. A large number of others were wrapped up within the first week. Nearly half of all claims were resolved within 30 days, with many settled much sooner. Our approach is all about fast assessments and clear communication, so you’re never left hanging.

Speed doesn’t mean we cut corners, even on the tough cases. Big or small, every claim got the same careful attention. We handled hundreds of claims even during the busiest periods (think wild weather weeks and the holiday rush) without breaking stride. And while most claims were everyday-sized or moderate, we also helped customers through some major events – including a few very large claims like house fires and water damage. Those high-value claims were supported just as promptly and compassionately as a cracked window or a burst pipe. Whether it was a minor accident or a serious loss, we followed the same straightforward process and kept our customers informed at each step.

Several clear patterns stood out in our 2025 claims data.

Vehicle glass claims (like damaged windscreens) made up about 12% of all claims. These are the everyday mishaps many drivers run into, and they are usually simple to assess and settle quickly.

Water damage was another common claim type, at around 10% of total claims. While it was not the biggest category by volume, it had a much bigger impact on cost, making up roughly 27% of total payouts. Problems like hidden leaks and burst pipes can get worse fast, so acting early really helps.

At the more serious end, accidental fire claims were uncommon, at about 1% of claims in 2025. But when they happened, they were often significant, accounting for around 12% of total claim costs. It’s a strong reminder that the right cover, plus a responsive claims team, matters most when something major goes wrong.

We also saw how external events can cause short, sharp spikes in claims. 29 April was our busiest claims day of the year, lining up with a bout of severe weather that brought heavy rain and strong winds to parts of the country. As you’d expect, that drove an increase in weather-related claims, with customers reaching out for support when it mattered most.

This year, we saw claims for just about everything under the sun (and rain). The most common claims by number were the ones you might expect – accidental damage around the home, car-related mishaps, and weather events. Life happens, and sometimes that means a stray cricket ball through a window, a parking-lot fender bender, or a blustery storm knocking over a fence. These everyday issues kept us busy, but that’s exactly what we’re here for.

Support when you need it

Our commitment to speedy, helpful service wasn’t just on the claims side. The initio customer support team had a standout year in 2025 as well, making it easier than ever for you to get the answers or help you need. We handled over 22,000 customer enquiries throughout the year – and we did so with an emphasis on being both quick and effective. In fact, most customer questions or issues were resolved within about an hour. A huge portion (over 90%) were solved in a single interaction, meaning one call or message was all it took to sort things out. No endless email chains, no multiple phone transfers – just one conversation and you’re sorted. “No follow-ups needed” became a bit of an unofficial motto for us this year, and we’re proud of that.

We also made sure you could reach us in whatever way suits you best. The majority of our customers chose to contact us online – whether by email, live chat, or through their initio dashboard – and they got the same friendly, professional care as if they’d called us on the phone. Of course, whenever a phone call was preferred or needed, we were right there too. Real people, real help, every time. We know sometimes you just want to hear a reassuring voice on the other end of the line, and our phone support team was ready whenever those moments came.

Chatbot Chad played a big part in that easy, quick support experience too. In 2025, Chad handled nearly 3,000 conversations and sent over 7,000 messages, helping customers get answers fast when it suited them. Chad achieved a 95% answer rate, and the vast majority of customers rated their experience with Chad highly, showing that self-serve support can still feel genuinely helpful and human.

Despite handling thousands of enquiries, we didn’t let quality slip during busy seasons. Even in our peak months, response times stayed consistently quick and our service stayed personal. We like to say we’re “built for busy days” – and in 2025, we proved it, delivering the same care and speed no matter how high the volumes got.

Looking back at these highlights, what makes us happiest is knowing each number represents a customer who got the help they needed and could move forward with peace of mind. Thank you for trusting us with your insurance in 2025 – we’re truly honored to have helped you through everything from everyday hiccups to life’s big storms. We’re excited to keep that momentum going into 2026, with even more improvements on the way to make things faster, easier, and smarter for you. From everyone at initio, we wish you a safe and happy New Year. Here’s to a bright 2026 ahead!

Related articles

It’s the stuff of nightmares. The family car is booked in for a Warrant on Tuesday, but you still have to do the Monday school run.

Everything runs to plan until a distracted driver rear-ends you at the lights. Will your insurance still cover the damage?

Don’t worry, your insurance company won’t automatically decline your claim just because your WoF expired.

The government requires a WoF on cars to keep people and roads safe. It means a certified mechanic has confirmed the vehicle is safe to operate on our roads, including safety features, and mechanical components like tyres and brakes.

While a WoF is a legal requirement, we’ve all been in the position where you simply forgot, or just have to get through another few days before you can get it to the workshop.

When would your claim be declined?

If you make a claim on your car, and your insurance company discovers it doesn’t have an active WoF (they can easily find this), they will want to find out:

1. Was the cause of the accident an issue with the car?

2. Would the issue have been resolved by a WoF check?

Your claim could be declined if it’s proved that an issue with the car was the cause of the accident. This could be bald tyres with no tread causing you to spin out, or tattered brakes meaning you couldn’t stop in time to avoid a collision.

These are obvious causes that are easy to pick up. If the issue is something less obvious, your insurance company might determine whether the issue would’ve been picked up by a WoF. If it would’ve, your claim could be declined. These are all reviewed on a case-by-case basis.

What if the cause was not an issue with the car?

Generally, most accidents don’t involve an issue with the car, so it won’t affect the ability to make a claim.

If your car wasn’t being operated at the time of a crash, there’s no reason to deny your claim as the lack of warrant has nothing to do with the damage. If someone else reverses into you and caves in your front bumper while your car is parked, that’s hardly your fault and nothing a warrant would prevent so you won’t be pinged.

Remember not to drive your car if you notice an issue, and fix it as soon as you can. This way if you have an accident and forgot about your WoF, your insurance coverage is still valid.

Related Articles:

As a landlord, you work hard to provide safe and comfortable homes for your tenants. But were you aware that a significant portion of rental-related claims stem from criminal activity?

In 2023, 14% of the claims we processed at initio were related to criminal actions, such as malicious damage, methamphetamine contamination, and burglary. These incidents not only cause stress and financial strain but also unexpected expenses for landlords.

Burglary and theft

As a part of the criminal activity, 30% were related to burglary and theft. This can be a common issue, especially when a rental property is occasionally vacant, making it an easier target due to the absence of people within the home.

Your property being empty for over 60 consecutive days will change your policy terms, and a higher excess of $5,000 will apply if you need to make a claim. If you’re expecting your property to be vacant for reasonably long periods – beyond 60 days, get in touch with us.

Just over 41% of burglary-related claims we received last year were related to theft of copper piping, plumbing, or hot water cylinders!

Not only does this result in stress for landlords to replace these items, it also results in a hefty bill to cover, as well as a potential loss of rent. The average cost for the accepted claim, relating to repairs for our clients last year was just over $8,000.

Our policy offers an automatic benefit for malicious damage, or theft by tenants. 41% of rental-related claims were paid out through our automatic benefit. You can enhance property security with locks and lighting to deter burglars. Consider installing surveillance cameras or alarm systems and maintaining your property adequately. This will help it look lived in as well as deterring unwanted activity.

Malicious damage

Of all the rental-related claims we received throughout 2023, 24% were related to malicious damage. Such damage can occur throughout a tenancy, but we saw 31% of these claims stemming from eviction. In this stressful scenario, landlords face the dual challenge of evicting a tenant as well as addressing significant property damage. These types of claims result in an average claim cost of just over $9,000 – an expensive, and unexpected type of bill!

Fortunately, our landlord cover offers an automatic benefit of $25,000 per event, for claims resulting from malicious damage caused by tenants. Make sure you conduct thorough tenant screenings through reference checks, credit checks and tenancy tribunal history. Also, establish clear lease agreements to minimise risks of eviction-related damage.

In the event that a key is lost or stolen, you can take action and replace it, and initio’s policy has a benefit designed exactly for this! This will help minimise the risk of someone returning while it might be vacant. With our landlord policy, we offer an excess-free keys and locks benefit – where we cover up to $1,000 for the replacement of keys and locks.

Methamphetamine contamination

While not common, this is a costly issue. Across all the criminal activity-related claims that occurred in rental properties in 2023, just over 11% of these claims were related to methamphetamine contamination. While this represents a small percentage, it is the most costly and widespread type of incident to affect your rental property, with an average cost of just over $20,000. Since your property cannot be tenanted when this sort of situation occurs, you as a landlord, will also suffer from loss of rent, another cost that heavily affects you.

Initio’s landlord cover includes an automatic benefit of $30,000 for methamphetamine contamination which will cover the testing, and cleaning costs in the event of a contamination taking place. We also offer an automatic benefit of $20,000 for loss of rent, which can be increased. We are prepared to cover you for this criminal activity as we understand the costs – and time it can take until your property is thoroughly cleaned.

Regular property inspections can help detect early signs of drug-related activity. Also performing reference checks, as well as tenancy tribunal history will help determine in the early stages if they will be good tenants.

Arson

While we only saw one claim relating to arson last year, it can also be the most expensive rental crime-related claim we pay for. This is because a house fire causes extensive damage, which can affect the overall structure of your property. To mitigate this risk, install smoke detectors and fire extinguishers. You could also provide a fire blanket, an invaluable tool for smothering fires. It’s a good idea to have fire safety equipment easily accessible, offering tenants a quick solution to douse flames before they spread.

Check your sum insured

In tough times, lowering your sum-insured to reduce your premium might seem appealing. However, this could lead to ‘under-insurance,’ a risky strategy that could backfire if significant damage occurs. Insurance is there to put you back in the position you were in before any mishaps, and cutting corners on your sum-insured might leave you short when you need support the most. We have seen the occasional customer not having their property fully insured for the right amount. This creates large amounts of stress, so we always recommend reviewing your sum-insured yearly, at the renewal of your insurance policy.

Initio, your partner in landlord insurance

Initio is dedicated to helping New Zealand landlords safeguard their rental properties against unforeseen events. By understanding the potential criminal activities, or accidents, that can impact your investment, you can take proactive steps to protect it. With our comprehensive landlord cover, you can enjoy peace of mind knowing that your property, and your financial well-being, are protected.

Let initio be your partner in navigating the challenges of rental property management. Our goal is to provide the protection and support you need to ensure your rental homes remain safe, secure, and profitable.

Get a quote in seconds

FOR MORE INFORMATION

ARTICLES OF INTEREST:

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2023, spanning our entire rental claims portfolio. Please note that all figures are approximate and have been calculated to provide a representative view of the claim trends during this period.

A closer look at property damage for New Zealand Landlords

Rental properties, for all their promise of steady income and long-term value can, if not managed correctly, become ground zero for an array of unforeseen problems and potential hazards.

The reality is that damages, an often neglected aspect of rentals, pose a considerable risk to your investment. These risks are as varied as they are prevalent, raising a pertinent question in the minds of property owners: “What damage is most likely to occur at my rental property?”

Safeguarding your investments and mitigating potential losses, and understanding these risks is essential to success as a landlord.

A thorough examination of our 2022 loss data provides a detailed analysis of the challenges faced by New Zealand property owners. Last year, claims related to rented properties — including traditional rental properties, own homes partially rented, and properties with multiple rentals, made up 35% of all the claims we received. When focusing on these rental-specific claims, we identified a broad spectrum of loss types, which we’ve classified below in terms of number of claims:

Water-related damage: At 21.6%, this was the most common type of damage. These losses typically involved scenarios including suddenly bursting pipes and rodent damage, while blocked pipes accounted for 6.4%.

Accidental damage: This category, representing 18.1% of the claims, includes an array of unexpected incidents, from minor mishaps to substantial accidents, illustrating the diverse risks property owners encounter. The losses range from outdoor misadventures, such as balls shattering windows or trees falling onto the property (while being pruned), to indoor accidents like stains on carpets and damaged rugs, often due to spills or pet-related incidents. There were also multiple kitchen bench damage incidents – caused by hot pots.

Weather-related damage: Severe weather events substantially contributed to the claims we received, with flood-related incidents constituting 11.2% and wind-induced damage representing 9.9% of the total claims. These statistics do not include the severe flooding and storms experienced earlier this year. Weather damage events are hard for property owners to mitigate.

Other incidents: Some more specific types of damages also occurred, albeit less frequently. These included

- Malicious damage by tenants (4.6%),

- Fire – accidental or unknown reasons (1.1%),

- Meth contamination (1.5%),

- Issues with keys and locks (3.5%),

- Impact damage, typically involving a vehicle (5.5%) eg car versus house

Loss of rent: There were several circumstances that led to a loss of rental income, resulting in insurance claims. Property damage rendering the property uninhabitable was one such factor and is the most common.

However, issues such as tenant abandonment, non-payment of rent, and eviction also significantly contributed. These loss-of-rent-only situations accounted for 3.3% of the total claims made.

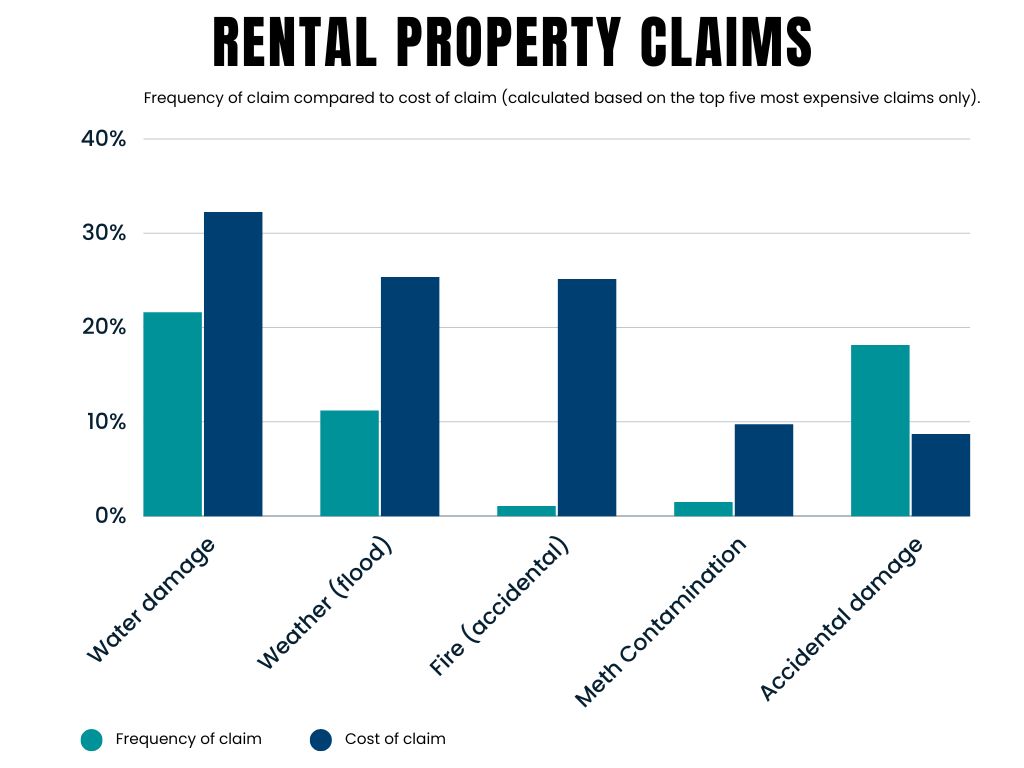

Frequency of claim vs. cost

The above numbers are based on frequency (i.e number of claims made). We also analysed the payout values for rental property claims. The graph below shows the top five losses by value. This data is presented alongside the frequency of each of these claims. It illustrates that losses like fire are uncommon but are high in value.

Fire-related claims constituted a mere 1.1% of the overall number of rental property claims, but made up 25% of the total value of claims paid. This underscores the potential devastation that fires can cause to rental properties. The significance of this cannot be overlooked, highlighting the importance of equipping your rental properties with smoke alarms, and fire extinguishers. By taking these simple proactive measures, you can significantly reduce the risks associated with fires and safeguard your valuable assets and your tenants.

Final word

Understanding the potential risks involved in rental property ownership can help landlords to better prepare for and protect their investments.

Proactive and pragmatic management of landlord risk is a form of insurance in its own right. In our experience, with the losses we see on a daily basis, a landlord that focuses on tenant selection, tenant vetting, regular property inspections, fire extinguishers in kitchens, regular maintenance including plumbing and electrical checks will outperform and not contribute to the statistics in this article.

Choosing an insurance provider that knows landlord insurance and who provides an insurance policy that is dedicated to the diverse needs of rental property owners is the icing on the cake for a well-rounded risk mitigation approach to landlording.

Learn more about initio’s Landlord insurance cover

The statistics presented in this article are based on a comprehensive analysis of claims data from initio for the calendar year of 2022, spanning our entire claims portfolio. Please note that all figures are approximate and have been calculated to provide a representative view of the claim trends during this period.

Want to check over the full details of your cover? It’s best to read your policy wording. You should also check your summary policy schedule from your dashboard to see what applies to your cover.

If you’re not sure what everything means, our guide on how to read an insurance policy walks you through each section in a simple, easy-to-follow way.

Owner-occupied Homes

See our full house insurance policy wording below. If you’ve included contents with your cover, download the separate contents insurance wording.

Download House Wording Download Contents Wording

Rental properties (including multi-units) and Holiday homes

Our holiday home and landlord cover are both under the below combined policy wording. To see what applies to your policy, it pays to check your policy schedule.

Download Landlord Wording

Car Insurance

See all the details of our comprehensive car insurance cover below.

Download Car Wording

If you have any questions about your cover, feel free to get in touch with our friendly team.

Related articles

As we wrap up another year, it’s time to reflect on the fascinating, bizarre, and occasionally head-scratching world of insurance claims. While we see plenty of the usual suspects – cars driving into garage doors, kids toppling TVs, and the inevitable shattered dentures – this year’s claims have had their fair share of unexpected surprises. Let’s dive into some of the more unusual and recurring themes that stood out in 2024.

Up in flames

Fire claims are nothing new, but some of the culprits this year were particularly creative. Among the singed and scorched items:

- Electric scooters: Handy mode of transport, but not so handy when left charging unattended.

- Homebrew heating pads: A DIY fermentation item that ended in flames rather than fizz.

- Phone chargers: Reminder that dodgy chargers can do more than just overheat your phone.

- Electronic toys: A child’s aeroplane toy that transformed into an unexpected firestarter during charging.

While these incidents thankfully ended safely, they serve as a good reminder to keep an eye on electronics – especially when they’re charging.

Robots on the rampage

This year, robotic helpers had their share of mishaps, including a memorable case involving a Hydro Robotic Pool Cleaner. While the cleaner was hard at work, the family’s puppy, with a love for chewing, got to the power/control cable, gnawing it clean in half – a reminder that even tech isn’t safe from a curious dog’s teeth!

Another memorable incident involved a robotic mower and a bonfire. While the mower was navigating the lawn, a nearby bonfire burned behind a barricade. Once the fire died down, heat weakened part of the barricade, allowing the mower to wander onto the hot coals. An alert from the mower app came too late – the damage was already done.

We’ve also had our fair share of claims involving robotic mowers being run over by vehicles. Whether these mowers have simply given up on life or were just in the wrong place at the wrong time, it’s a good reminder to check under your vehicle before driving off!

Lost gems and broken dreams

Losing jewellery is heart-wrenching, and this year saw a steady stream of claims for lost or damaged treasures. These included rings, bracelets, and other cherished pieces that were either misplaced, damaged, or, in one case, fell victim to a rogue drainpipe.

PSA: If your jewellery has seen better days, now might be a good time to have it checked for maintenance or repairs. Keeping them in good nick can prevent heartbreak later.

For more details, check out our article on which items need to be specifically listed in your insurance policy.

Wild is the wind

Some claims highlight the unpredictable ways life can get messy – literally. This year, wind played a starring role in several liability claims, showing just how easily the elements can cause chaos. A few standouts include:

- Airbnb fire damage: Strong winds carried hot ashes from an outdoor fireplace through open sliding doors, burning the timber floors inside the accommodation. (We’re betting that bond didn’t cover it!)

- Marquee mishap: While being packed away, a marquee at an event was caught by a gust of wind and struck a parked vehicle.

- Flying debris: In another incident, a gust of wind sent wood from someone’s yard soaring over a fence, denting a parked car.

- Flying trampolines: Unsecured trampolines and strong winds are a recipe for disaster, as we’ve seen in multiple claims this year. In one case, even a properly secured trampoline was no match for particularly strong winds, showing just how unpredictable Mother Nature can be. If yours isn’t secured, now’s the time to make sure it is.

These moments remind us how easily accidents can happen – and why insurance is the best way to protect yourself against life’s unexpected mishaps.

Some of the more unusual…

Some claims stood out for their unique and unexpected nature this year, with these two being particularly memorable:

- The Broken Turtle Tank: A shattered aquarium caused water damage that made a big splash – literally.

- Fireworks inside a holiday rental: Yes, you read that right. Guests decided it was a good idea to let off fireworks indoors. (We can’t imagine the host’s reaction when they walked in to assess the damage.)

Here’s to 2025

While some of the above gave us a chuckle (and occasionally a gasp), they’re also a reminder of the diverse risks we all face. Fires, gadgets with minds of their own, and jewellery mishaps are just the tip of the iceberg.

As we move into the new year, we’ll keep an eye out for trends, helping to ensure we’re always ready to protect the unexpected.

Here’s to another year of keeping you covered – whether it’s for the weird, the wonderful, or the downright bizarre. It’s our privilege to provide the protection and peace of mind you need, no matter what life throws your way. Here’s to a safe, secure, and hopefully less eventful 2025 – though if it isn’t, we’ll be here to help every step of the way.

For more information:

Scenario: Existing client of yours that has a house(s) insured with initio, processed through broker software (e.g. eGlobal), and policy is due to expire.

Getting your client online is easy with initio

- Use your Broker landing page to quote your customer’s house

- Choose the relevant property type (own home, rental, holiday home)

- See instant quote on screen. From the quote screen email yourself the quote

- Select the start date of insurance (ie expiry date of current cover)

- Set the sum insured to the expiring amount or amount already discussed with your client.

- Click ‘Save & email this quote’.

- Enter your client’s name and then your email address.

- Separately email your client your pre-renewal email. Your email will say that they can continue to insure with initio but that it will need to be started and paid for online through a collaboration with your firm and initio.

- This email will include the initio premium and may include other traditional offline options.

- It may include an explanation of changes in premium, levies etc. compared to last year.

- It will include a request of how the client would like proceed.

- If your client elects to continue to insure with initio (online), then you will need to email initio [email protected] and request that an existing client is onboarded. You will need to provide the relevant info (as per the detailed offline to online document) in order for initio to onboard

- Initio will onboard your client by setting up an account and loading the policies, subject to payment.

- Initio will email you the login details for you to send to the client.

- You then just need to email your client with the login details and advise them that once logged in they will see the house policies ready to activate. The customer will need to make a payment to activate the policies.

Double whammy on levies

Did you know that a large portion of your house insurance premium goes to the government in levies? For the average initio house insurance policy sold through our site www.initio.co.nz, over a THIRD of the cost to the home owner is levies…… and unfortunately that proportion is about to jump significantly with fire service levies increasing by 40% from 1 July 2017 and earthquake commission levies increasing by 33% from 1 November 2017, which will mean total levies will then make up almost HALF of the cost of an average initio house insurance policy.

While levies are perceived as a bad thing, because they hit each of us in the pocket, it is important to take account of the fact that the fund essential community necessities such as the New Zealand Fire Service, many of which are volunteer fire brigades in smaller communities. These brigades require specialized trucks and machinery to attend fires and accidents of all types. So as the running costs increase, so too do the levies.

The good news is that the team at initio continue to work hard to keep the actual insurance premium down so that home and rental property owners can enjoy some of the best value cover around.

Initio keeps premiums down by making the process of insurance simple, and its online. Get a quick quote in seconds and get covered in a little more…. ‘no death by a thousand cuts’ paperwork or long winded phone calls. Unfortunately, we just can’t do anything about the levies.

Crack the champagne – a toast to our focus on insurance claims!

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

We are incredibly proud to be recognised for our hard work and innovation with the 2024 Canstar Innovation Excellence Award, which honors our efforts in setting new insurance claims standards for convenience and efficiency in the insurance industry.

Initio stands out not just for its technology, but for its practical, impactful applications that significantly improve the customer experience. Let’s explore the technological innovations at the core of our submission, which we call Smart Claims:

A fully digital, seamless claims process

Initio is one of the few insurance providers offering customers a 100% online claims process from start to finish, setting a new standard for convenience and efficiency in the insurance industry. Our Smart Claims platform eliminates the need for traditional phone calls to confirm details, handling everything online with ease and precision. This approach not only simplifies the claims process but also significantly speeds it up, allowing customers to focus on recovery and rebuilding without unnecessary stress.

Key features of our Smart Claims process:

- Streamlined submission: Customers can submit claims quickly and effortlessly, without the traditional hassles of paperwork and long waiting times.

- Efficient claims management: Our system ensures claims are managed efficiently, significantly reducing wait times and allowing our staff to focus on expediting claim processing rather than making follow-up calls.

- Reduced need for customer calls: Our online dashboard’s transparency and instant access mean fewer calls are needed, making us more available to pick up when you do call. This enhancement significantly improves your experience while allowing our support team to assist you more efficiently..

Proactive customer support and real-time updates

During Cyclone Gabrielle, Initio leveraged its advanced mapping tool, Locatio, to proactively identify and contact customers likely affected by the disaster. This not only ensured timely assistance but also demonstrated our proactive approach to customer care.

Enhancements in customer support:

- Claim support and updates: Our efficient system freed up our claims consultants to provide personalized support, focusing on those in critically affected areas.

- Continuous availability: Despite the digital focus, our claims consultants remained available via phone for those needing personal interaction, further supported by continuous online chat and easy claim access.

- Transparency and real-time updates: Customers could monitor the status of their claims through their dashboards, which included detailed updates such as site visits by builders and a comprehensive communication history.

Initio’s offerings are not only innovative but also distinctly superior to what is currently available in the market, both domestically and internationally.

What makes smart claims different?

- Complete online management: Our website allows customers to fully manage their policies independently, from purchase to claims, providing unparalleled control and flexibility.

- Advanced risk assessment: Utilising data from Regional and Government Councils and updates from the LINZ database, we provide precise risk assessments, enhancing our underwriting process.

- Synergy of smart claims and Locatio: The integration of these technologies not only reduces administrative burdens but also accelerates claims resolution, improving overall customer satisfaction.

What the Canstar judges said about initio’s online insurance experience

The awards panel recognised that initio is the pioneering insurance provider in New Zealand. We enable customers to secure quotes, arrange cover, and file claims swiftly via a digital platform. They praised initio for its effective service that simplifies insurance management for homeowners, utilising technology to evaluate risks promptly and precisely.

The judges were most impressed by the ease and efficiency of receiving a quote with Initio. There was consensus around the judging table that this could be disruptive as other insurers look to adopt a similar approach.

Our ongoing promise

Initio will continue to refine and enhance our platform, committed to providing the finest digital experience available in New Zealand, ensuring our customers receive outstanding service tailored to their needs.

For more information

From 1 January 2019 the initio Holiday Home insurance policy is changing. We’ve added some extra benefits, enhanced and simplified some of the existing covers, and put some restrictions on some areas. This is a summary of the good, the improvements, and the not so good.

THE GOOD:

New cover benefits

New building work

Up to $10,000 of cover is available per annual period for a new structure valued at $10,000 or less being built at the home, including any associated materials that are to be included in the new structure. Covers loss or damage caused by specified events only. Please contact us if you need separate cover for building work that falls outside of the above criteria.

Post-event inflation protection

Under the home section of this policy, up to 10% of the relevant policy limit or sum insured is available as additional cover if building costs increase due to widespread damage following a natural disaster, storm or flood.

Stress payment

If we pay a total loss claim for the home, we’ll also pay you $1,000 for stress caused by the loss.

Water or sewage pipe blockage

Up to $1,000 of cover is available per annual period towards unblocking water or sewerage pipes at the home. No excess applies.

Electronic Programs

If your electronic equipment suffers loss or damage covered under the home section of this policy, you’re also covered for the reasonable cost of restoring, re-setting or re-programming programs, software and other coded instructions necessary to operate that equipment. There’s no cover for any data that may be stored on that equipment.

Keys and locks

The maximum amount payable during an annual period for your home’s keys and locks is $1,000. No excess applies.

Improvements to existing cover:

Vacant homes

Where the home has been vacant for more than 60 consecutive days we continue to provide insurance cover but with a higher than standard excess ($5,000). If you have an active, professionally-installed alarm, the excess reduces from $5,000 to $1,000. Under the old policy the alarm excess was $2,500.

Landlord’s protection

Additional Benefits for landlords (in addition to existing benefits for malicious damage):

- Loss of rent due to non-payment of rent because of prevention of access or failure of public facilities, up to 6 weeks’ rent

- Loss of rent due to the tenant vacating the property without notice, up to 6 weeks’ rent

- Loss of rent due to eviction for non-payment of rent, up to 6 weeks’ rent.

The excess has changed from minimum $500 to the standard policy excess.

Learn more about landlords protection here

Simplified cover for contents

The following items are covered for present value only:

- watercraft and their parts and accessories (there’s no cover under this policy for watercraft with a present value of over $2,500)

- bicycles

- linen

- items that you choose not to repair or replace.

For all other items we’ll either pay:

- to replace the item if it’s under 5 years of age, or

- the present value of the item if it’s 5 years of age or over, or

- to repair the item as close as possible to the condition it was in before the loss or damage.

There is no cover for personal effects, and cover only applies at the home or whilst you are transiting items from your permanent residence or its place of purchase.

Legal liability

Your legal liability cover of up to $2,000,000 for damage to another person’s property is extended to cover liability for another person’s accidental death or bodily injury in connection with your home or its grounds. The limit is now GST inclusive. Defence costs you incur with our prior approval are now covered on top of this. Clarification that there’s no cover for liability in connection with seepage, pollution or contamination, unless it occurs during the period of cover and is caused by a sudden and accidental event that occurs during the period of cover.

Carpets

Fitted floor coverings, including glued, smooth edge or tacked carpet and floating floors are defined as part of the home under the policy and now covered for replacement (new for old).

Clarification to existing cover:

Reduction and reinstatement of sums insured

Following damage to your home for which a claim is payable under the home section of this policy or by the Earthquake Commission, the sums insured are reduced from the time of the loss by the amount required to repair the loss. When payments are applied to the repair of the home, the sums insured are reinstated.

GST

All amounts shown are inclusive of Goods and Services Tax (GST).

Outbuildings

Cover for outbuildings used for domestic purposes now extends to outbuildings that may have limited rural lifestyle use, i.e. for the storage of tools, animal feed, uninstalled equipment or machinery and vehicles only.

THE NOT SO GOOD:

Tree disposal

Your policy no longer covers the disposal of tree debris following damage to your home or contents caused by a falling tree or part of a tree.

Landscaping

The maximum amount payable to restore your garden or lawn has reduced from $3,000 to $2,500. Cover applies only where a claim is payable for damage to the home and the landscaping damage occurred during the same event.

Recreational features and retaining walls

There is now a sub-limit of $45,000 for all recreational features (tennis courts, pools etc) and a sub-limit of $25,000 for all retaining walls, unless these items are specified with a higher limit as shown in your schedule. More details here

Methamphetamine contamination

We continue to provide cover for meth however the maximum amount payable for cleaning or repairing the house and its contents damaged by methamphetamine contamination (manufacture and consumption) has reduced from the house sum insured to the amount shown in the schedule, currently $30,000. An excess of $2,500 applies to each claim. There are additional conditions and limitations for tenancies or occupancies of 90 days or less. Learn more about meth here

Landlord’s obligations

This section outlines the increased standard of care that is now required of landlords. To make a valid claim on a tenanted property, you’ll need to have fulfilled these obligations.

The inspection and monitoring requirements must be met from when your policy renews. The updated tenant-vetting requirements will only apply to new tenancies that commence after your policy renews, not to your existing tenants.

You’ll also need to test for methamphetamine contamination before and after each tenancy, in order to be covered for methamphetamine contamination-related liability as a landlord. Learn more about landlord obligations here

This is not an exhaustive or comprehensive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio landlord and holiday home policy NZ1811

If you insure your home with initio, part of what you pay includes a compulsory levy for Natural Hazards Insurance. This levy gives you access to cover provided by the Natural Hazards Commission Toka Tū Ake (NHC), previously known as the Earthquake Commission (EQC). It sits underneath your initio policy and covers specific parts of your land and home when they are damaged by natural disasters.

NHC cover is a type of government-provided insurance that operates under the Natural Hazards Insurance Act 2023 to help with the cost of repairing or replacing your residential home and specific parts of your land that are damaged by:

- Earthquake

- Tsunami

- Landslip

- Volcanic eruption

- Hydrothermal activity

- Storm or flood (land only)

You receive the NHC cover automatically when you purchase a house insurance policy. If a natural disaster damages your home, NHC will help to pay for the cost and your home insurer, such as initio, will pay the rest up to your selected sum insured (within the terms of your policy).

What Natural Hazards cover is provided by NHC for your home?

- Cover for your home or holiday home, plus related outbuildings such as a shed, garage or pergola.

- Essential services connected to your home (for example water, drainage, sewerage, gas, electricity or telecommunications) up to 60 metres from the home.

The maximum amount the NHC will pay towards repairing or rebuilding a home for a covered event is $300,000 plus GST for events on or after the 1 October 2022. If the damage relates to an event prior, the cap may be lower. The limit is per insured dwelling unit.

Anything above that cap is covered by your private insurer through your home policy.

Although your initio policy pays for the top up cover on your home, it’s important to know that initio cannot top up or extend any land cover beyond what the NHC provides. The amount paid by the NHC is the full entitlement for land under the Natural Hazards Insurance Act, and insurers are not able to offer additional land cover above this cap.

This means that if the cost to repair or stabilise the land is higher than the NHC settlement, initio is unable to pay the difference. Your initio policy will continue to respond to damage to your home and other insured buildings, but any extra cost relating purely to land sits outside the policy and cannot be covered.

What Natural Hazards cover is provided by NHC for your land?

Under the NHC, you are insured for the land that is inside your legal property boundaries AND;

- under your home and some related outbuildings

- within 8 metres of your home and select outbuildings

- under or supporting your main accessway for up to 60 metres (for example, the land under your driveway)

New Zealand is one of the only countries where homeowners have access to residential land cover. But it’s important to understand that this cover is limited and does not extend to all parts of your section.

Your land cover is based on a land cover cap, made up of:

- the market value of your insured, damaged land

- the value of insured retaining walls, bridges and culverts (to a limit)

If it costs more to repair the land than it is worth, the NHC will cash settle based on the land’s market value at the time of damage.

This means Natural Hazards Insurance usually contributes toward repairs rather than fully covering them.

What if my property has a Section 72 or Section 51 Notice?

Section notices are warnings placed on a property’s title that inform current and future owners, insurers and lenders about known or newly identified natural hazard risks. They affect how claims under the NHC’s natural hazards cover are assessed. There are two main types:

-

Section 72 notices (under the Building Act 2004).

- A Section 72 notice may be placed when a building consent is granted for land that has a known hazard (erosion, slippage, inundation etc).

- If you later make a claim for damage caused by the hazard listed in that notice, the NHC may fully or partly decline your claim.