Having started a company that challenged the way things have always been done in insurance, our director, Rene Swindley, who is the recipient of the 2018 Young Insurance Professional of the Year, was asked to speak to the 2019 Insurance Council of New Zealand Conference on how insurers need to change to meet the expectations of tomorrows insurance buyer. Here is the abridged transcript of his presentation.

Young insurance professional view

I turn 35 this month so I’m no spring chicken… but I’m arguably still very young by industry standards (something I would love to see change).

After finishing Law school, at 23 years of age, I co-founded a company called Frank… so I suppose you could say that I’ve taken an immature approach to insurance over the last decade. Back then I had a lot more hair, a lot less stress, and couldn’t understand why insurance was so clunky.

The early days (2009) – Tristram Street, Hamilton

It was this Naïve approach to insurance that has allowed us to challenge the way “things have always been done”.

By way of background Frank Risk. Is our Commercial Insurance Broking brand – it rebates commissions to clients and charges a disclosed fee for service, and this approach removes the conflict of interest most other brokers face. From its inception 10 years ago Frank has challenged the market to do insurance the way we do.

Frank Risk (Nov, 2018) – Celebrating 10 years in business

Frankie is the digital version of Frank – we built this in-house to be a client-facing tech lead platform for business insurance.

Initio is our domestic brand – it’s a digital provider of domestic insurance (houses, contents). The platform, which we built from scratch, is a full on-demand, customer-facing quote, bind, manage, claim online. It’s customer-centric and it’s faster, easier, smarter. It was the first of its kind in 2011, and back then insurers were in denial about tech lead custom driven insurance….. These days they call it “Insuretech”.

So with that background on how we’ve been trying to effect change for the benefit of the customer – here’s my opinion on how we (the industry) needs to change for the next generation of insurance buyers:

Initio (2019)

How insurers need to change

Insurers need to provide value

Tomorrow’s customer is buying on value – not price or $50 pressie cards. They want an insurer that provides flexibility, provides assistance with managing risk, and communicates with them in plain English.

So let’s cut the jargon, let’s give the customer control, let’s help the customer reduce risk.

We are starting to see examples of insurers and tech companies providing tools for managing the things people own. Trov in the US pioneered single-item, micro duration insurance. The founder, Scott Walchek asked ‘What would happen if you could give individuals control over the information about their things’. What happens is the customer sees value in the relationship with their insurer as it departs from a pure transactional relationship.

Value for the business customer is by way of tools that help to identify their commercial risks in real-time – I’m talking about connected devices that tell a line manager that a steel saw is becoming blunt and causing heat. Insurance becomes secondary.

The provision of value like this is just the beginning. The buyer of tomorrow won’t be thinking of insurance as a primary service – it will be secondary to the provision of other core business tools and personal management strategies.

Make insurance accessible

Insurance lags way, way behind millennial’s expectations of obtaining intangible services.

For a product that does not need to sit on a shelf, has no physical logistics associated with it, and for many risk lines, has no short supply issues – insurance is nowhere near as accessible as it should be.

We need to change to adapt to the buying and living patterns of the next generation, which means on-demand insurance cover that’s also available at point of sale, and aligns intricately with how the customer works, lives, eats, plays. What I’m proposing is a policy of the future that wraps around the customer not what they own. Just imagine an insurance world with fewer policies and less fragmentation.

One of the reasons insurance is not as accessible is it should be is because of the human factor. Let’s get smarter about this and use computing power not humans to do the soul-destroying processing work for no complex risks. I challenge you to work out how many humans need to be involved in a single material damage placement. I’m guessing its 6+.

Increase the trust

Insurers don’t trust their customers, and customers don’t trust their insurers. By any relationship standard – that’s a pretty bad one.

The next generation of insurance buyer wants to trust their insurer and they want to be trusted.

Let’s compare it to the taxation system in New Zealand. It trusts the end-user implicitly. For example – with a GST return, if you claim a cash refund [by disclosing that your GST collected on sales income is less than the GST paid on expenses] you receive the refund to your bank account – no questions asked. But god help you if you are dishonest. It’s a trust everyone until proven otherwise approach – and it works.

That used to be the way insurance worked (absolute good faith – uberiemae fidea) but it seems to have evolved into a “prove your loss” approach including proofs of purchase, photographs, assessors, investigators – all at great cost.

I totally accept that insurance fraud is a real issue – but there are smart ways to combat this. We are seeing examples of how technology and analytics are providing huge value gains here. Insurers are using anti-fraud algorithms to detect fraud and some US insurers are employing social scientists and psychologists to senior positions in their companies so that they can understand the mentality of their customers and build it into the technology.

So, in short, the industry’s current approach does not align with the expectation of what a millennial expects of their insurance experience.

As an industry, we can also increase trust by getting rid of the ‘black box’ stigma of insurance. We all know insurance but the customer doesn’t. We can start but introducing smart, searchable, plain English wordings. Wordings that are opensource that are a collaboration between the insurer and the buyer is my vision here. Tomorrow’s buyer doesn’t want a ‘gotcha’ moment. The next generation wants to contribute to how their policy is built – and for that insurers will get respect, earn trust, and have a customer for life.

Education also increases trust. Everyone believes that there’s a pot of money for earmarked for them. “I’ve been a customer for 20 years and I’ve never Claimed”.

I even had someone say to me the other day “I’ve just returned from overseas and all went well – no issues, do I still need to pay my travel insurance premium”

These comments seem odd to people who are in the insurance industry but I can’t emphasize enough that there is a widespread misunderstanding among customers of how insurance actually works. And this isn’t the fault of the customer – the insurance industry is the one who has dropped the ball here.

We need to teach customers that insurance is, in fact, a community-based pooling of resources administered by an organization [an insurer] who charges a margin for the privilege.

Know your customer – Know your data

Tomorrow’s insurance buyer expects that their insurance provider knows them and their stuff intricately.

The next generation expects this because they have willingly shared personal data with their insurer (and in many cases the public at large) already.

So to this end when they make a claim they don’t want to be asked how old they are or what their name is. Think about the current claims process… “Here you go customer – please repeat everything we already know about you on this manual form”. Not a great experience.

And when it comes to starting insurance, the things they own are data mapped and the next generation knows this. So let’s not ask the customer how many KM’s their vehicle has done or how susceptible their house is to flood.

Often the customer struggles with accuracy on these pieces of information and there is a fear that if they get them wrong they will invalidate their insurance. So, let’s NOT put that responsibility on the customer when we all have data we can access already. My point here is that its the insurer’s responsibility not the customers

I think as an industry we have been missing the real opportunity here. Data is where the real value is – and it’s a huge opportunity to impress our customers. Once you have data the sky is the limit, and insurers are the biggest data houses in the world.

You may have heard all the buzz words like AI, machine learning, and blockchain. But put simply we need to find patterns in the data and share this knowledge with the customer. Transparency breeds loyalty.

To recap the insurance buyer of tomorrow wants:

We can be smart with technology and achieve all of these things

I’m excited about the next few years for insurance. The insurance industry will continue to go through some dramatic change – there will be some winners and some losers but one thing is for sure, the customer will benefit immensely.

If you own a property with two dwellings and rent them both out long-term (90 days or more per tenant), it’s important to have the right insurance to protect your investment. Whether the dwellings are separate or physically connected will determine the type of insurance you need.

What type of rental arrangement is this?

Two homes, same site

Both rented on long-term residential leases

What insurance do you need?

The right insurance depends on whether the dwellings are physically connected or separate:

If the dwellings are NOT physically connected (e.g., separate buildings on the same section):

If the dwellings ARE physically connected (e.g., one upstairs and one downstairs, or connected by a wall, roof, or garage):

You can use our Multi-Unit Rental policy, which provides coverage for both units under a single policy. you’ll need to state the number of self-contained dwellings at the address. This helps ensure you get the right level of cover for your property setup.

On the full quote screen, click ‘back’ to edit the second dwelling’s details if needed.

If both properties are the same size or the details are already correct, no changes needed.

Once you go back, edit the property details, then click ‘continue’

This will adjust the quote to reflect the correct figures for the property.

Finish the quoting process from here per the usual process – Easy!

You can get a quick quote and buy insurance online in just a few minutes with initio. Make sure you choose the right policy based on whether your dwellings are separate or connected. Getting a quote and buying insurance online with us is easy, but our cover is anything but basic. We offer comprehensive protection to ensure you’re fully covered.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

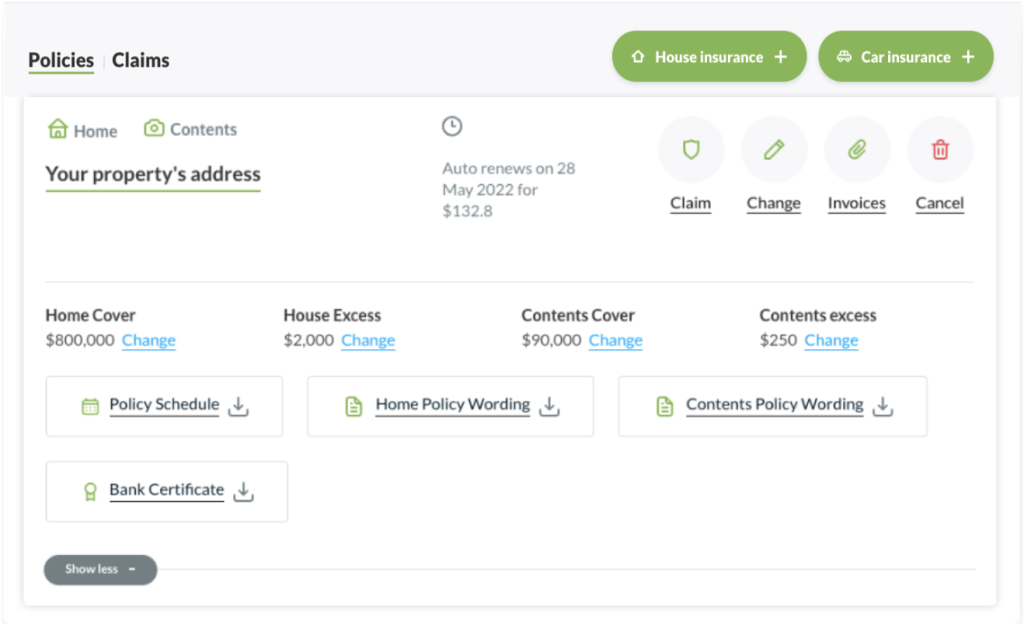

Once you have purchased your first policy with initio, you get access to a personal dashboard where you can modify and manage all your policies online.

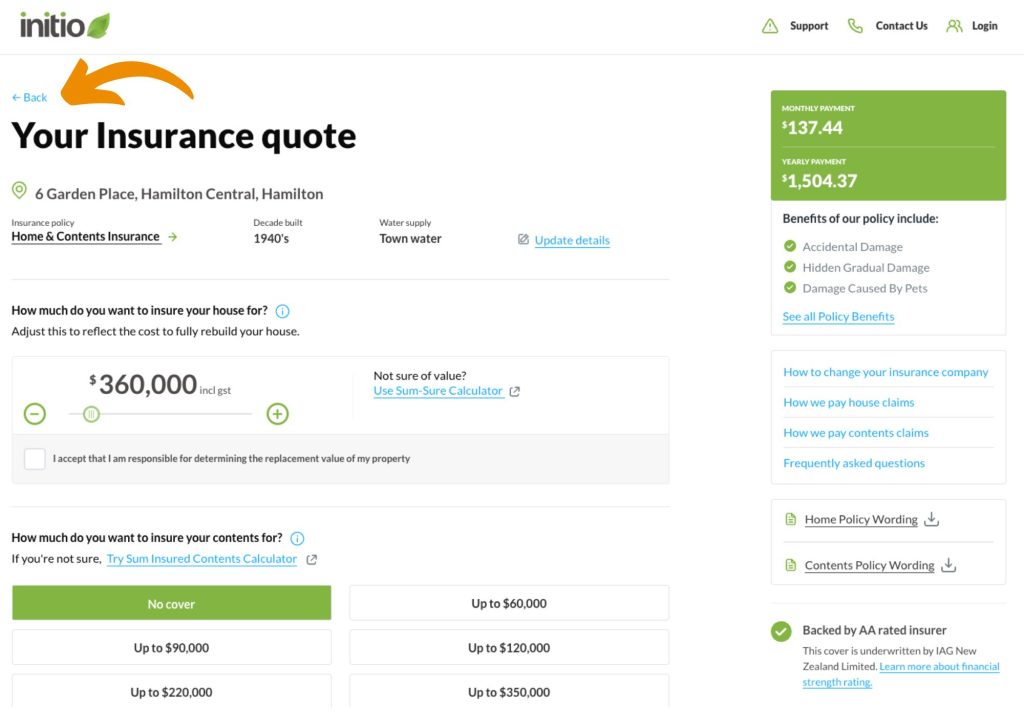

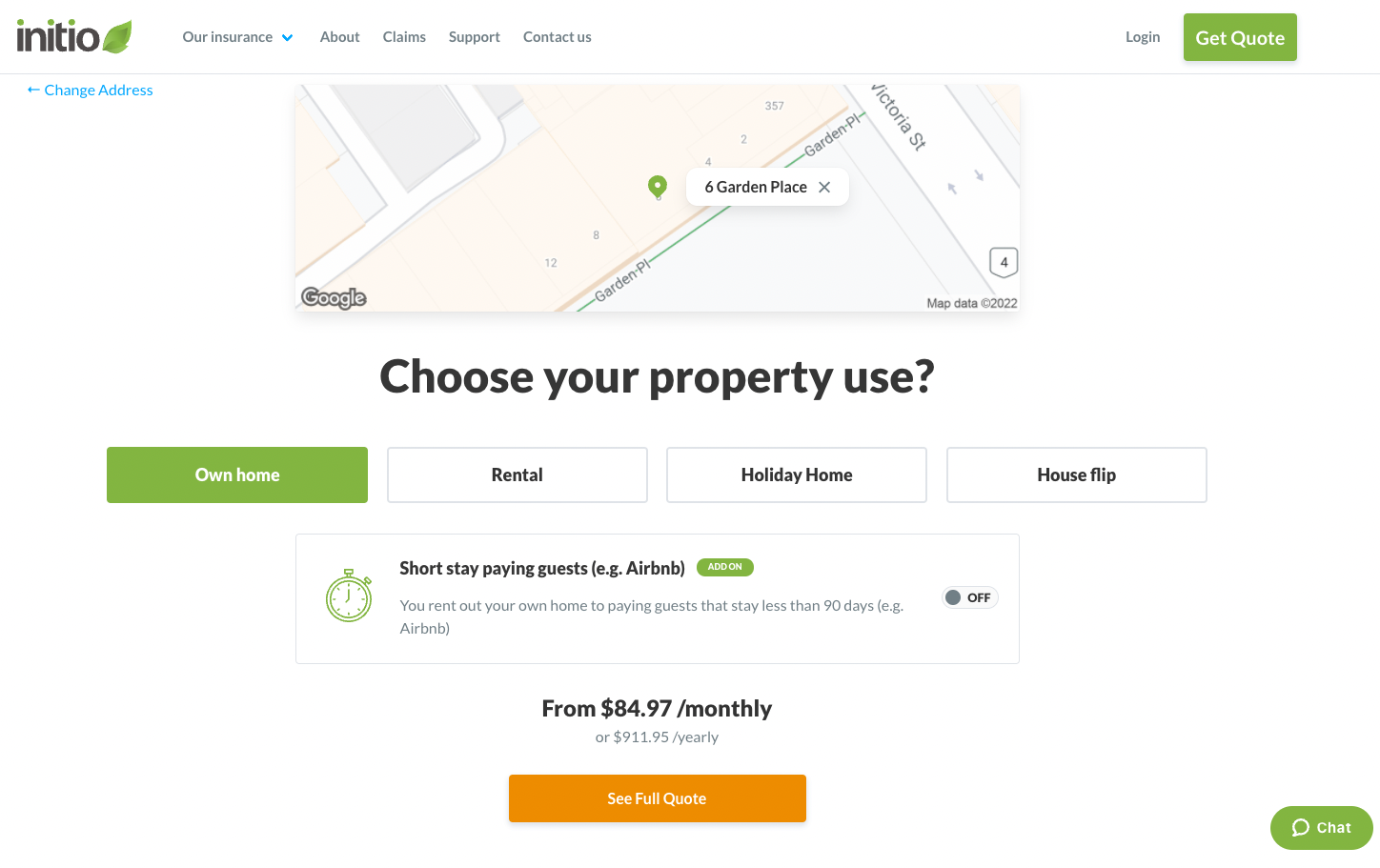

Get an instant quote – enter property address

If your address doesn’t come up with the details you have entered, please use the blue option below the address box that then comes up showing as “I can’t find my address”. Clicking on that option will let you enter both the house number and street manually.

If your home is a new build in a particularly new street, potentially our database may not be able to locate the street, if so, please give our team a call to obtain a quote.

Select property use

If you’re uncertain about the type of property insurance that best suits your needs, visit our ‘Choosing Your Insurance‘ support page. There, you’ll find detailed information and guidance to help you make an informed decision tailored to your unique circumstances.

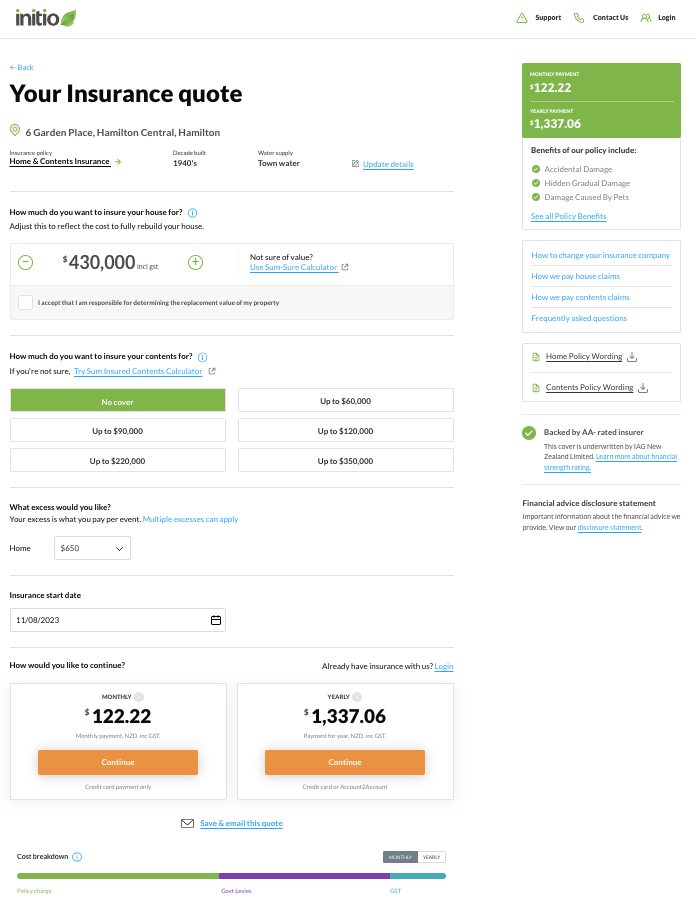

Customise quote

From here you can edit the details of the quote and customise as required. This can also be done from a home quote you have previously emailed yourself using the “restore” button.

Uncertain about the proper amount to insure your property for? We’ve designed a support page that walks you through the essential factors you need to consider regarding the sum insured.

Choosing the right amount of insurance for rebuilding your home is important. This amount should be what it costs to build your home again, not what your home is worth on the market. Don’t forget to include things like fences and swimming pools, and remember that building costs might go up over time. For example, if two neighbors with the same houses insure for too little or too much, they could lose money if their houses are destroyed. The right amount saves worry and money. Tools like the Cordel Sum Sure Calculator can help you figure out how much it might cost to rebuild your house.

If you’re wondering about how much excess you should have on your insurance policy, this support page covers some of the basics. Many property owners choose to cover minor losses themselves, avoiding insurance claims for low-value damages. If this applies to you, consider raising your excess to $1,000 or $2,000 to save on premiums. Think about what you’re comfortable claiming for and your financial risk tolerance when selecting house insurance. Under initio’s landlord insurance, tenants only cover the excess on careless damage, so assess your comfort level with potential out-of-pocket expenses, and set your excess to match your ability to absorb those costs.

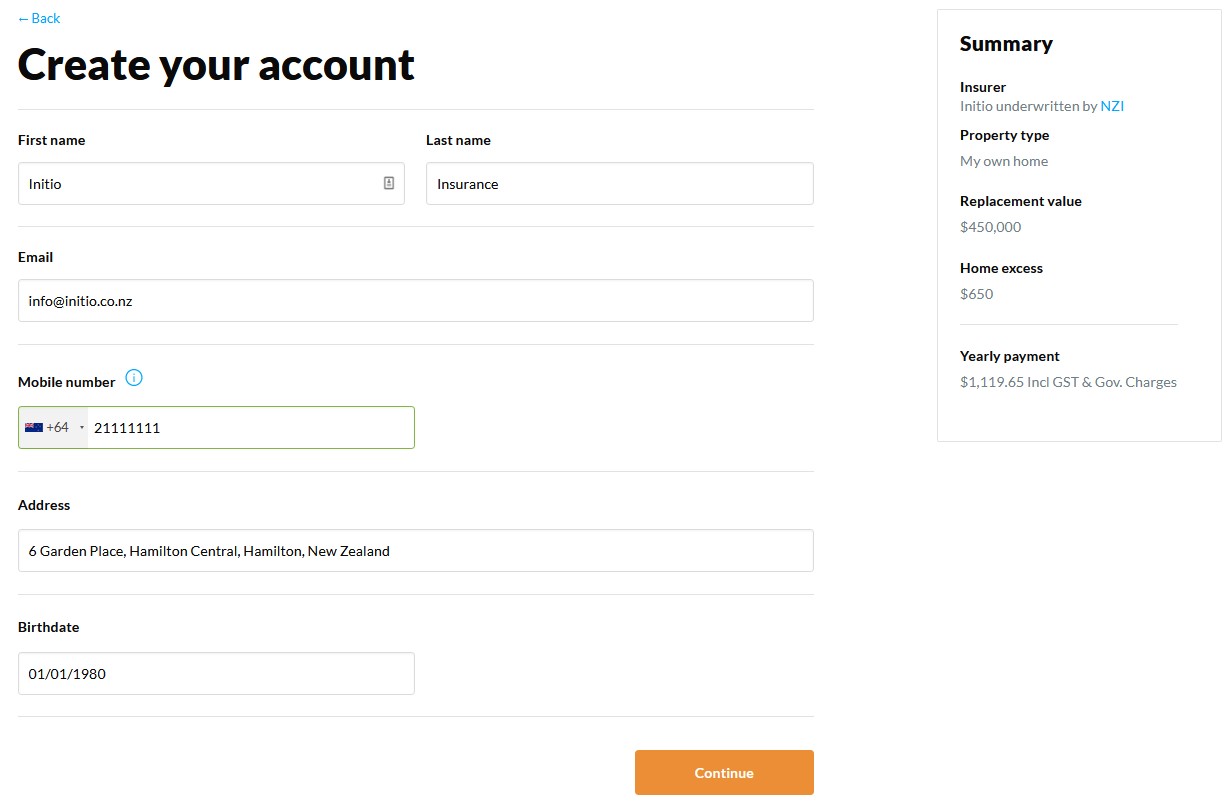

Insurance Start Date? Enter the date that you would like the cover to start from should you proceed with purchasing. If it’s a new home, that should represent the sale’s settlement date. If you’re changing from another insurer, use your existing expiry date. Please note that we are only able to provide confirmed quotes for policies with effective dates of up to 30 days in advance. If the effective date you need is more than 30 days ahead, please wait till you are closer to that time to quote/apply.

Once you are happy with your customised quote, you can either;

Email yourself a copy to save a copy of the quote

Proceed to purchase the policy by selecting either the “annual” or “monthly” payment option at the bottom of the quote. Then follow the steps below.

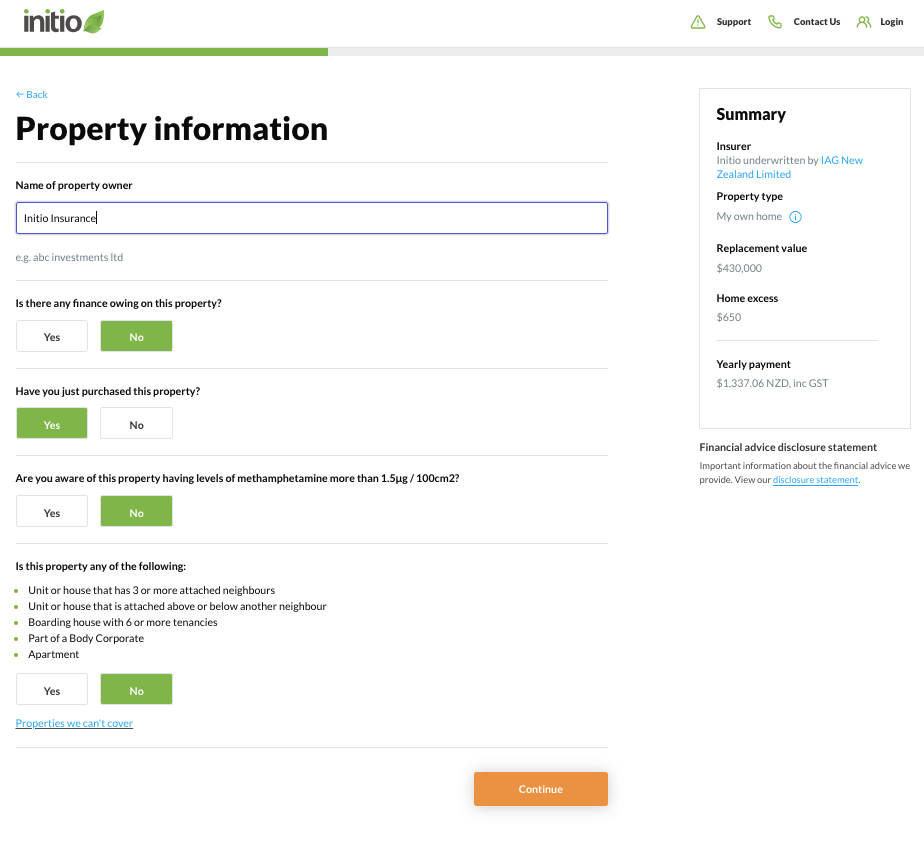

Enter property details

A note about selecting start date of cover; ensure its the same date as the expiry/renewal date of your current policy to ensure cover continuity (or the settlement date if purchasing a new house)

Confirm your details

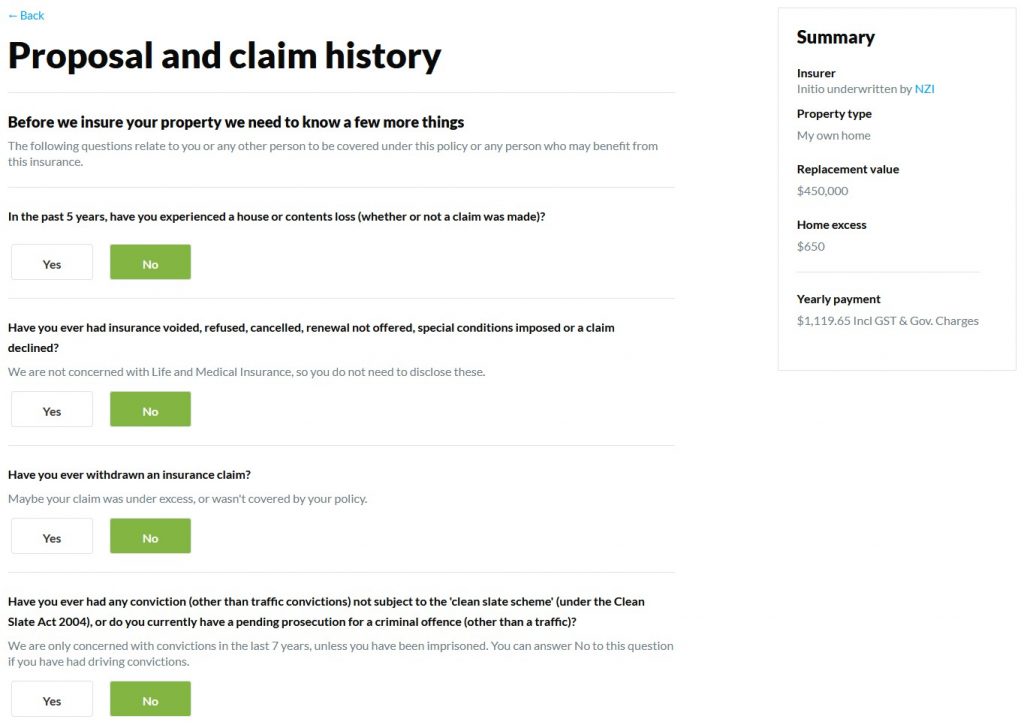

Complete online proposal form

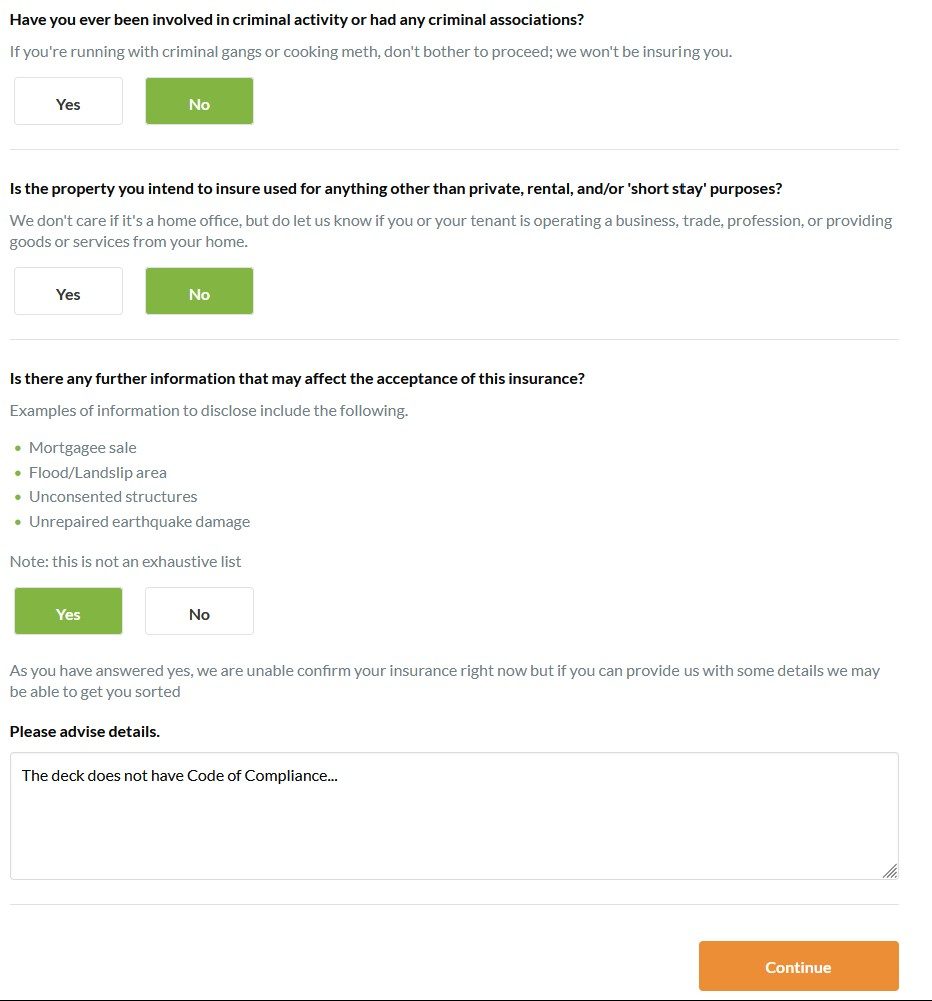

Unsure if something may affect your cover? Disclose it

How to sign your application form

Use the device keyboard to type your name in full (as the person completing the form) in the space provided.

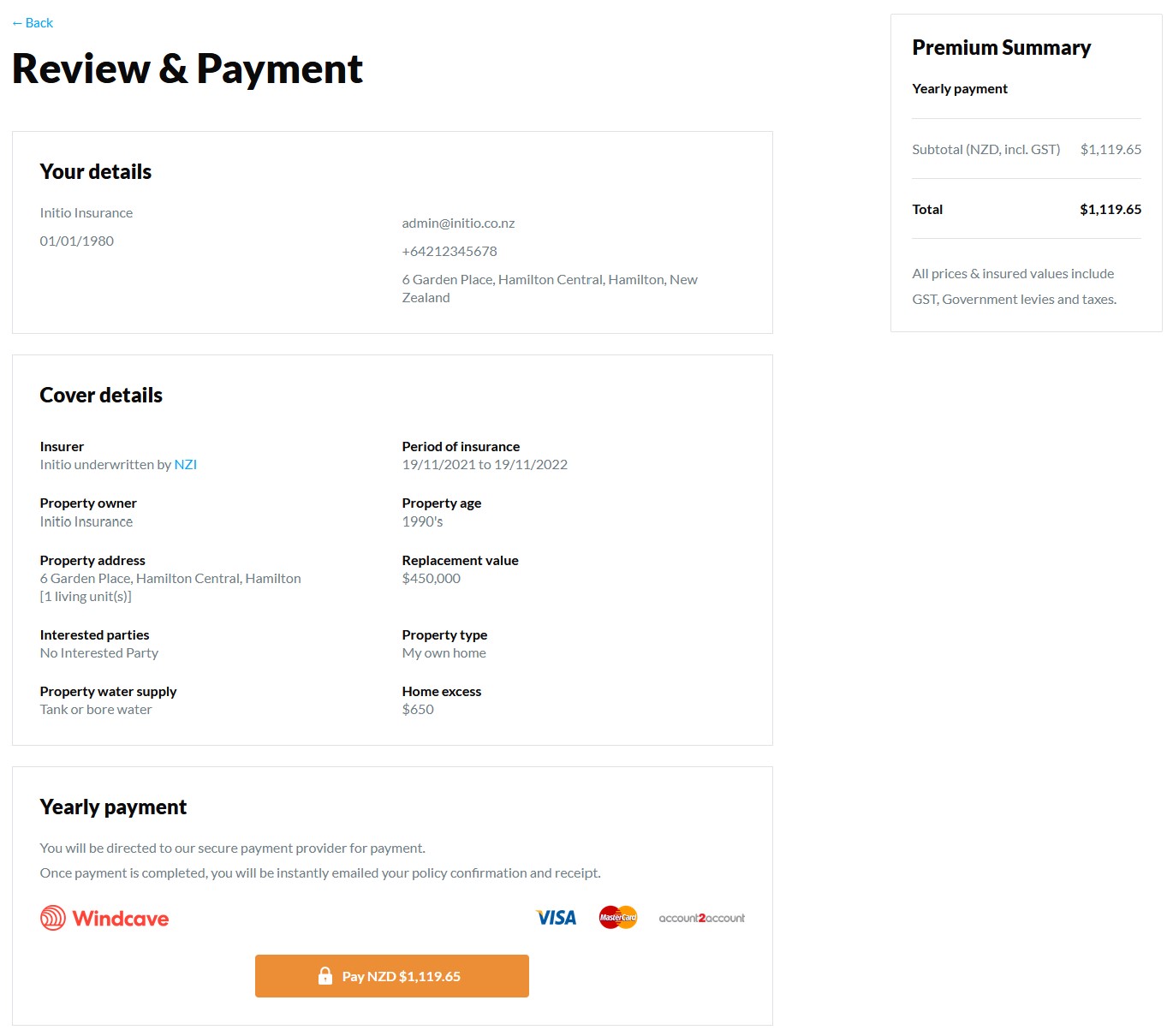

Review and make payment OR Application requires a review?

If the payment option isn’t offered it’s because a human will need to review the application for you. Please continue to submit the application for review and we will aim to come back to you within one business day to let you know the status of the request.

Otherwise, if the payment option is available, you can either

proceed to purchase the policy OR

if you’re not ready to commit or haven’t yet bought the property, you can choose to download a “letter of intent” on this page. The letter of intent simply outlines that based on the information provided we are able to insure the property when you’re ready.

ALL DONE! We will instantly email you confirmation documents

Want to add another property? Click “Add insurance”

Need to make a change to your policy?

Refer to our guide here. Our website is informative and the go to for accessing your account. No need for an app, our site is available in a user friendly format on all your devices.

Our vehicle insurance is exclusive to our home policy holders. Once you become a home policy holder with initio you can easily add car insurance from your initio dashboard using the “vehicle insurance +” option.

Most people do not have the time, or the expertise, to sit down and work out exactly what it could cost to rebuild their home from scratch. If you are looking at your house insurance options, an online house insurance calculator can be a helpful place to start.

It does a lot of the heavy lifting by using property details and current building cost data to give you an estimated rebuild cost. Most of the questions are things a homeowner can usually answer themselves, such as the size of the home, how many levels it has, and what materials it is built from.

Online calculators do not provide advice, and they may not capture every detail that could affect the rebuild cost of your home. Instead, they use the information entered, along with property and construction data, to provide an estimate. If you would like a more tailored assessment for your specific property, a builder, architect, quantity surveyor, or insurance valuation service may be the best option.

It is also important to remember that your sum insured should reflect the cost to rebuild your home, not what you paid for it, what it might sell for, or what the land is worth.

Demolition, professional fees, and site-related costs should also be considered

Reviewing your sum insured regularly can help reduce the risk of underinsurance

What is a house insurance calculator?

A house insurance calculator, also called a sum insured calculator, is an online tool that helps estimate how much it could cost to rebuild your home after a total loss.

It is designed to provide an estimate based on typical building replacement costs. It is not intended to provide personal advice, and it may not allow for every detail that affects the rebuild cost of your home.

For many people, it is a practical and straightforward way to get started.

Rebuild cost is different from market value

One of the most important things to understand is that your insurance should be based on rebuild cost, not market value.

The price you paid for your home can include the land, location, school zones, and housing market demand. A rates valuation or QV can also include land value and broader market factors. None of those figures tell you what it would cost to physically rebuild the house itself.

That is why your sum insured should not be based on:

the purchase price

the market value

the rates valuation

the QV

the land value

Instead, it should reflect the likely cost to rebuild the home to a similar size and standard using today’s building costs. See ‘Why does my rebuild value change?‘ for more information.

What your sum insured should cover

Your sum insured should reflect the full cost to rebuild your house to its current size and standard.

That can include:

demolition and clearing the site

rebuilding the house itself

current material and labour costs

architect, engineer, or consent-related costs

site access or complexity that may make rebuilding harder

Not every property is simple to rebuild, so it is important to think beyond just the floor area.

What can affect your rebuild cost estimate?

A calculator is a helpful starting point, but it may not reflect every detail of your home. That is why it is worth reviewing the result carefully, especially if your property is more complex than average.

Renovations, unusual features, and non-standard materials

The estimate may need a closer look if your home has features that are not typical, such as:

If you have made improvements such as building a deck, installing a swimming pool, adding a new room, or upgrading your kitchen or bathroom, those changes may affect your rebuild cost.

Size, layout, and standard of finish

Rebuild cost is not just about floor area. Two homes of the same size can cost very different amounts to rebuild depending on their design, layout, and level of finish.

Things that can affect the estimate include:

ceiling height

kitchen and bathroom quality

custom joinery

roof shape

cladding type

number of storeys

architectural design

Site access and demolition costs

The site itself can also affect rebuild costs. For example:

steep sections can be harder to access

tight urban sites can increase labour and delivery costs

This matters because building costs can change over time, and your home may have changed too. While your policy may include a general inflation adjustment at renewal, that will not usually account for significant improvements, extensions, or alterations you have made.

If you do not review your sum insured from time to time, you could find yourself overinsured or underinsured at claim time.

When should you get a more detailed estimate?

For many homes, a calculator gives a useful estimate. But you may want a more detailed assessment if your home:

In these situations, a builder, architect, quantity surveyor, or other valuation expert may be able to give you a more tailored estimate.

Why this matters in New Zealand

In New Zealand, sum insured matters because house insurance is generally based on the amount you choose as your cover limit.

That means it is important to choose a figure that feels realistic for your home and its likely rebuild cost. If the amount is too low, it may not go far enough in a major claim. If it is too high, you may be paying for more cover than you need.

Final thoughts

A house insurance calculator is one of the easiest ways to get started when working out your sum insured. It saves time, uses relevant property and construction data, and helps give you a practical estimate without having to calculate everything yourself.

But it is still only a starting point. The most important thing is to check whether the estimate reflects your home, its features, its level of finish, and the likely cost to rebuild it. If you are unsure, getting a more tailored assessment from a builder, architect, quantity surveyor, or insurance valuation service may give you more confidence in the amount you choose.

You can use an online house insurance calculator to estimate what it may cost to rebuild your home to its current size and standard using today’s building costs. If you want a more tailored assessment, you could also speak with a builder, architect, quantity surveyor, or valuation expert.

Should my sum insured be the same as what I paid for the house?

No. Your sum insured should reflect rebuild cost, not purchase price or market value.

Does my sum insured include the land value?

No. Your sum insured is about the cost to rebuild the house, not the value of the land.

Is a rates valuation or QV the right figure to use?

Not usually. These figures do not necessarily reflect what it would cost to rebuild your home.

How often should I review my sum insured?

It is worth reviewing it regularly, especially at renewal time or after any renovations, extensions, or major improvements.

Written by Toby Pudney – Initio’s Support Team Lead

Toby has been with initio since 2023 and is the Support Team Lead. He brings more than six years of experience in the insurance industry, giving him strong knowledge of general insurance. He has studied with ANZIIF and holds a qualification in New Zealand Compliance for Advisers (General Insurance Broking).

Here’s what you need to know to insure your main home if it’s also rented to short-term guests.

What can be covered? A shared primary residence

If the house is your primary residence, we can cover your own home that’s also rented with our Own Home Rented product. However, it’s required that you share the use of the property with guests.

The two most common scenarios for renting your own home are:

You rent out part of your home to short stay guests while you still live in the property (e.g. a room or downstairs).

You rent out you whole house to short stay guests when you’re not living there (e.g. you go overseas or stay in your holiday home).

If your house is not your primary residence, it may be able to be insured as a Holiday Home also Rented. Learn more about insuring holiday home rentals here.

Essentially, our guest rental cover only applies to properties that have shared use (at-least occasionally) by the owner. We’ll explain why next.

What can’t be covered? A dedicated short-stay accommodation

We can’t insure a dedicated short-stay living unit that’s only used for guest accommodation. When a unit is used solely for guests it becomes a commercial property – similar to a motel.

The EQC’s $150,000 of natural disaster cover will not apply to a ‘dedicated short stay’ as they are considered commercial risks. Our domestic house insurance policy assumes part of the natural disaster risk is covered by the EQC. A dedicated short stay rental therefore needs to be covered under a commercial material damage policy, where the insurer covers 100% of the natural disaster risk.

Please note the definition of a dedicated short stay property is any living unit that is set up purely as a commercial enterprise and the owners don’t use it or intend to use it for their own purposes (or for somebody else to use it as their home).

Is a secondary unit at my house covered under my house insurance policy?

Yes, as long as it’s not a dedicated short stay unit – and it’s used by yourself (at least occasionally) as part of your own home.

It’s common for people to have an additional self contained living units at their houses. It’s common to have a separate unit at the back of the house, or a downstairs living unit with its own access. Often these are rented to short term guests (via Airbnb or BookaBach), or longer term boarders for additional income.

If you don’t use this unit yourself (at least occasionally) then we can’t insure it together with the main house.

If the unit is used purely for short terms guests a commercial policy is required. If the unit is simply rented to tenants you’ll need a separate landlord insurance policy for it.

Short Stay Airbnb Unit Example

If the additional unit is used by both the owner and short-term guests we can provide cover under our own home rented.

If the additional unit’s use is shared by the owner (themselves or family) as well as short-stay guests, it can be covered under our Own Home Rented product.

When the living unit is solely rented to guests and not utilised by the owner, it is deemed a dedicated short stay. EQC cover does not apply, and we can’t provide cover.

An example of this is where the unit is used for children when they return home from university and other times the unit is rented to short stay guests. This can be insured under a Own Home Rented policy on the main house.

Renters or Boarders Unit Example

If the rental unit (for example downstairs unit) is only used for a longer term tenants (i.e. more than 90 days) or boarders and not utilised by the owner themselves – this can’t be insured under a single Own Home Rented policy. In this instance, a separate Landlord Insurance policy is required to cover the self-contained rental unit.

If you need help working out which insurance or combination of insurance is best for you, see our home & income insurance page.

What is Covered?

Our Own Home Rented product takes all of the standard owner occupied policy features, and includes extra cover for the risks of renting. You can also choose to add personal household contents cover. You can get the peace of mind that your property and contents itself is covered, while the risks associated with renting your house to guests is insured.

Generally a standard house insurance policy won’t cover guest risks, so it’s important for owners to get the right cover. The extras included in the own home rented cover includes:

What happens if my house is too damaged and can’t be lived in?

If your house is too damaged to be lived in (like a fire or flood) there is cover (up to $20,000) to go towards moving into a temporary house while repairs are completed. If you also get regular rental income from guests there is cover for your lost rents you would otherwise have got if your house wasn’t damaged.

We provide $20,000 of loss of rents cover for free, with options to increase to $40,000 or $80,000. Both loss of rents and alternative accommodation have a payout period of 12 months.

The Loss of Rent calculation will take account of future actual guest bookings that are cancelled, and expected bookings based on the same period in the previous year. If you are new to the home and income game then we will use short-stay occupancy rates in that particular region to estimate the loss. If you have a boarder or tenant with a fixed weekly rent then that amount will be used.

The policy aims to put the owner in the same financial position they were in before the loss, by paying for the repair costs and lost rental income – all while paying for the owners temporary accommodation costs.

If you’re serious about property investing, it is likely that you have a block of units in your portfolio. We have the insurance policy designed to keep premiums low and help your yeilds.

Initio provides an all-in-one cover for your residential multi unit rental property (up to six attached units) and the extra risks you take on as a landlord, such as one of the tenants deliberately damaging your property.

IMPORTANT This is a summary of the policy only. Please refer to the policy wording for full details of cover

What if I live in one of my units?

The Multi-Unit Rental policy is designed for rental properties. If you own a block of units and personally reside in one unit, this will need to be insured individually as an owner occupied home. This way you can include cover for your contents and personal effects, and get premium savings on your own home. The remainder of the units in the block can be insured either together or individually.

What if it is a Body Corporate?

Sorry we are unable to insure properties which are part of a Body Corporate.

How do I note the ownership of each unit?

If each unit has a different owner the unit will need to be insured individually. To qualify for the multi-unit policy the units must have the same ownership and be under the same roof.

How many units can I insure on one policy?

You can insure up to SIX attached residential units under a single Initio multi-unit policy. So as long as all units are attached you can insure the lot under one Initio policy.

Initio allows you to buy insurance online and enjoy some of the best policy coverage and claims management available to Landlords of multi units.

Buying a home or property is a large part of the classic Kiwi lifestyle, and it tends to be the biggest investment most Kiwis will make in their lifetimes. When it comes to arranging house or landlord insurance, New Zealander’s want peace of mind for their asset – and so some property owners will seek advice from their insurer. However, others don’t – and those investors remain unaware of these avoidable insurance pitfalls. We’ve put together a list of the top five mistakes people make when purchasing house insurance, so you can avoid making them too.

1. Saving money on your premium by reducing the sum insured

On face value, it seems to make sense: reduce the sum insured to pay less premium. You could justify this by calculating the odds of having a total loss are slim… but therein lies the issue: what if you do have a total loss? Would you be able to rebuild the house (and its site improvements, such as driveways and fences) if the insurance proceeds were less than you needed? House insurance is about getting you back on track – replacing like for like, and ultimately, saving you from financial ruin by properly protecting your home and investment. When calculating your sum insured, you need to know you’ll be covered in a worst case scenario. If you are wanting to save on premium, insure the house for its correct replacement value and consider a high excess; which means you’ll still be covered for the big stuff while also saving money on your premium.

2. Not knowing the replacement value of the property

Some property owners assume that insurers know how much it will cost to replace their home. The reality is that while an insurer might provide a guide they don’t actually know your house like you do. Insurers and brokers are not valuers or quantity surveyors and they are not materials cost specialists. When you get an instant quote from initio, the sum insured is based on a standardised per square meter rebuild cost, but it’s important to know that all houses are different as some will cost a lot more than this, and in those cases the sum insured should be increased. It is also important that the property owner or landlord takes account of improvements such as driveways, fences, and pools when calculating the replacement value.

initio guides you to tools, such as online sum insured calculators, to assist property owners with calculating their rebuild value. If you’re still unsure, or you want to be precise consider engaging a quantity surveyor such as Construction Cost Consultants.

A large number of property owners are happy to avoid the claims process by not claiming for smaller losses, and just repairing or replacing low-value losses themselves. If this is you and you have a low excess (of say, $400), we recommend increasing this to $1,000, or even $2,000 to save money on your house insurance premium.

If you wouldn’t bother claiming for anything less than $1,000, why would you waste your money insuring it?

On the flip side, if you wouldn’t be comfortable contributing the first $2,000 each time you claim, then a lower excess will be best for you. It’s certainly personal preference but we encourage property owners to think about their own financial risk tolerance when purchasing house insurance. Remember that under initio’s landlord insurance policy the tenant is only responsible for covering the excess on careless damage claims, so don’t assume they will be paying the excess every time there is damage at your rental property.

Ask yourself; “How much of a dent to my cash flow am I able to cover myself?” This amount is what your excess should be.

4. Choosing the cheapest (or most expensive) policy

Cheap doesn’t necessarily mean good. To ensure your home insurance adequately protects your most valuable asset, you need to make sure that you have the right cover. If for example, where the property is tenanted, an own homeowner’s insurance policy won’t cover you for damage caused by tenants. By the same token, the most expensive policy isn’t necessarily the best either. You could be paying extra for a brand name, its marketing budget, or bells and whistles that are simply not relevant to your to situation and requirements (such as ‘hole in one’ compensation…), or you could be unknowingly paying a middleman to just clip the ticket.

It is recommended that you take the time to understand what you are getting for your money. A good place to start is your insurance policy wording. initio has recently launched a policy comparison tool on our homepage to makes things a little easier for the customer when deciding on their house insurance.

5. Thinking that house insurance should cover everything

There are some losses not covered by a house insurance policy. Some of these are un-insurable, like leaky house syndrome and acts of terrorism. Other risks might require an additional policy, such as a contract works policy if you are doing renovation work (removing the roof or exterior cladding for example). Gradual things like wear and tear are not covered either; an insurable loss needs to be caused by a sudden and accidental event; insurance is not designed to pay out every time the property needs maintenance work done or a tenant leaves the house messy and worn. These things are just part of the risk parcel of being a homeowner or landlord. Consider that if your policy covered every possible loss, the annual premium would be tens of thousands of dollars.

Remember, your insurance policy needs to work for your own peace of mind, so make sure you consider what risks you want covered, and what risks you are comfortable absorbing – keep the above tips in mind when making this decision.

Insurance policies can look complicated at first. They usually contain multiple sections, detailed explanations, and specific defined terms.

This is intentional. Insurance policies are legal contracts designed to clearly explain the agreement between the insurer and you, the customer. Insurance policies are detailed by design so that both the insurer and the policyholder understand the agreement.

They set out what is covered, what is not covered, and how claims will be assessed. Taking the time to review your policy schedule, policy wording, and definitions can help you understand how your cover works before you ever need to make a claim.

Once you understand the structure of a policy, it becomes much easier to navigate.

Key takeaways

Insurance policies explain what is covered, what is excluded, and how claims are settled.

Your policy wording and policy schedule should always be read together.

Key sections to review include cover (sometimes known as the insuring clause), exclusions, limits, excess, and policy conditions.

AI tools can help explain insurance wording, but the policy document itself is always the final authority.

If anything is unclear, it is always best to confirm details with your insurance provider.

Who this guide is for

This guide is designed for New Zealand homeowners and landlords who want to better understand their insurance policy. Whether you are reviewing your cover for the first time or simply want to understand how your policy works, knowing where to find key information in your policy schedule and policy wording can make the process much easier.

Understanding your policy schedule and policy wording

Your insurance policy is made up of two key documents that work together: the policy schedule and the policy wording.

The policy schedule contains the details specific to your cover, such as the insured address, sum insured, excess, and any specified items.

The policy wording explains how the policy works. It outlines what events are covered, what exclusions apply, and the conditions of the insurance. Both documents need to be read together to fully understand your cover.

Policy schedule

This is the personalised summary of your cover. It includes details such as:

the insured risk (property address or vehicle details)

the type of cover you have

the sum insured

your excess

The schedule tells you what applies to your specific policy.

Policy wording

The policy wording explains how the insurance works. It includes the rules of the policy, such as:

what events are covered

what exclusions apply

how claims are settled

policy conditions and definitions

Think of it this way: The schedule shows your cover. The policy wording explains how that cover works.

The key sections to check in an insurance policy

Insurance policies follow a fairly consistent structure. Instead of reading every page straight away, it can help to focus on the sections that explain the most important parts of the cover.

1. What you are covered for

This section explains the events the policy protects you against. For example, many home and contents policies cover sudden and accidental loss or damageto your property that occurs during the period of cover.

This part of the policy (sometimes referred to as the insuring clause) outlines the main purpose of the cover and the types of incidents that may trigger a claim.

When starting an insurance claim, in the first instance, you need to provide enough information to support that the claim is covered by the policy (called a prima facie claim). In the above situation, you’d need to demonstrate that something caused 1) sudden and unintended, 2) loss or damage (which is often defined as physical loss or physical damage), 3) to property which belongs to you, and 4) that the damage occurred during the period of cover. This is why you need to understand each of the criteria of what you are covered for.

2. What you are not covered for

The exclusions section explain situations where cover does not apply. These sections are important because they define the boundaries of the cover. Common exclusions across many insurance policies include:

wear and tear or gradual deterioration

corrosion or rust

damage caused intentionally

pest or vermin damage

damage linked to construction work

These exclusions help both the insurer and the policyholder understand where the cover begins and ends.

3. What the policy will pay

This section explains how claims are settled. Depending on the policy, the insurer may:

repair the damage

replace the item

pay the present value of the item

This section will also outline limits that apply to certain items or categories.

For example, some policies set maximum limits for jewellery, bicycles, or collections unless they are specified separately on the policy.

4. Policy conditions

Policy conditions explain the responsibilities that come with having insurance. These include obligations such as:

taking reasonable care to prevent damage

notifying the insurer if circumstances change

providing accurate information when applying for cover

notifying the insurer as soon as possible after a loss

additional obligations of landlords

These conditions help ensure that the policy continues to operate as intended.

5. Definitions

Insurance policies often use defined terms to keep the wording clear and consistent throughout the document. Words with specific meanings are usually bolded in the policy and explained in the definitions section of the policy wording.

Even words which have ordinary meanings, may be defined by the policy so it’s important to read through the definitions section for each policy, even for words you’re familiar with. For example “Home” has an ordinary everyday meaning, but the policy may provide its own definition to describe that when the policy says “Home”, it means: the dwelling plus fences, pools, utility connections and so on.

Some common insurance terms you may come across include:

Excess:The amount you must contribute towards each incident before the insurer pays the remaining cost.

Sum insured: The maximum amount the insurer will pay to repair or replace insured property after a covered loss.

Incident: something that occurs at a particular point in time, at a particular place and in a particular way.

Accidental: Unexpected and unintended by you as the policyholder.

Hidden gradual damage: hidden rot, hidden mildew or hidden gradual deterioration, caused by water leaking from any internal: tank that is plumbed into the water reticulation system of the home and is permanently used to store water; or water or waste disposal pipe installed at the home.

Present Value: the estimated reasonable cost to replace an item with an item in New Zealand that is of equivalent age, quality and capability, and is in the same general condition

Reviewing these definitions can help make the rest of the policy wording easier to understand.

The initio glossary page also explains many other general common insurance terms in more detail. Note that if a policy provides a specific definition, then that prevails over any other general definitions.

Three common mistakes people make when reading their insurance policy

When people first look at their insurance documents, it’s common to focus on the parts that feel most relevant at the time. However, this can sometimes lead to important details being missed.

1. Only reading the policy schedule

The policy schedule shows details specific to your cover, including the insured address, the sum insured, and the excess.

While this information is important, the schedule needs to be read alongside the policy wording, which explains how the cover works and what conditions apply.

2. Skipping the exclusions

Exclusions explain situations where the policy does not apply. They are not there to catch people out, but to clearly define the boundaries of the cover.

Understanding the exclusions helps you know what types of loss the policy is designed to protect against, and where other solutions or maintenance may be required.

3. Not checking the definitions

Insurance policies use defined terms that have a specific meaning within the policy.

These words are usually bolded, and are explained in the definitions section of the document. Checking these definitions can make the rest of the policy wording much easier to understand.

Taking a few extra minutes to review these sections can make a big difference in understanding how your insurance works and what you can expect if you ever need to make a claim.

Using AI to help understand insurance wording

Insurance policies contain detailed explanations and legal language. Because of this, many people now use AI tools to help explain certain sections.

For example, you might paste a paragraph from your policy wording into an AI tool and ask it to explain the meaning in simpler terms.

This can be useful for understanding unfamiliar phrases or summarising longer sections of the document.

The policy wording itself remains the official document that defines the cover. If anything appears unclear, the policy wording and your insurer’s guidance should always take priority.

Where to find your policy wording

If you want to review the full details of your cover, you can access the policy wording alongside your policy schedule.

If you are unsure how a section applies to your situation, it is always a good idea to contact your insurance provider for clarification.

Frequently asked questions

Do I need to read my entire insurance policy?

Many people start by reviewing the key sections that explain what is covered, what is excluded, and how claims work. While you don’t have to read it all in one sitting, it is important to have a clear understanding of what you are and aren’t covered for.

What is the difference between the policy wording and the schedule?

The policy wording explains the general rules of the insurance cover which apply to everyone with the same type of policy.

The policy schedule contains the details specific to your policy, such as the insured address, limits, and excess.

Can AI explain my insurance policy?

AI tools can help summarise or explain complex wording in simpler language. However, the policy wording itself is always the final authority, and you should confirm any important details directly with your insurer.

What is the most important part of an insurance policy?

The most important sections to understand are:

what you are covered for

what you are not covered for

your excess

the sum insured

policy conditions

Together these explain how the cover works and what you can expect if you need to make a claim.

If you are ever unsure how your policy applies to a situation, it is always best to check the policy wording or contact your insurance provider for clarification.

Written by Hannah Gabbie, Head of Claims at initio.

Hannah has been with initio since 2023, and has more than a decade of experience with fire and general claims. She is a Senior Associate CIP of ANZIIF, and has a Diploma of Loss Adjusting.

At initio, we don’t ask you 30 questions to get a house insurance quote. We simply ask one – what’s your property address?

We can do this because we use verified property data instead of manual forms. By entering your address, our system pulls key details automatically, letting you see a quote in seconds.

While many insurance providers rely on long application forms and manual inputs, our system does all of this heavy lifting for you behind the scenes. In a few clicks, you’ll see a quick quote – no fuss, no obligations.

How does initio know about my property?

A quick quote is the starting point for your house insurance policy. It’s based on verified property data from sources like LINZ and local councils – things like the size of the home, its construction, and whether it sits in a flood or earthquake zone.

Let’s dive into this a bit more.

Why we don’t need you to answer a lot of questions

Because our quoting engine already knows the answers. And if we see something missing, our underwriting team steps in to review it with you.

Behind the scenes is Locatio, initio’s in-house property risk scoring platform. It checks things like:

The age of your house

The floor area in square metres

Whether you’re on town or tank water

If the home sits in a natural hazard zone (like floodplains or seismic areas)

This lets us assess risk instantly and provide a quote without needing to quiz you first.

Fun fact: When we first launched our quoting system, it was so fast that people thought it hadn’t worked properly. We had to add a loading screen just to provide confidence it was doing something.

We keep it up to date by regularly refreshing the data and adapting it to new hazard insights across New Zealand. That means what you see on screen is backed by real-time information and market-leading risk modelling.

Why we built Locatio

It was built by our in-house development team in response to one of insurance’s biggest pain points: slow and confusing quote processes. By building an innovative platform to minimise a pain point in the industry, we can power thousands of quotes every month for almost every property in New Zealand, in seconds.

Does this affect my cover or my ability to choose?

No, initio’s quoting tool allows you to view at glance what you could be paying. Once you have viewed your quote, you can tailor your cover by adjusting the sum insured, choosing your excess, and adding any extras. It’s simple, clear, and takes minutes, not hours.

When we might still ask for more information

Sometimes our quoting system may not be able to find or pull data for your address. Because Locatio relies on council and LINZ data, there may be occasions where this information isn’t available. If that happens, we may need to ask you for a few extra details.

Things like new builds, title changes, multi-unit properties or subdivisions can cause the information to be unavailable due to the council records or data not being updated as of recent. Sometimes our quoting tool may not be able to pull one piece of information that is missing.

When this does happen, you will be reverted back to the property information and asked to manually add it in. While this may cause an inconvenience, it is important we have this information so we are able to calculate the risk at hand.

So what does this actually mean for you?

All of this clever tech is there for one simple reason: to make getting house insurance easier, faster, and less frustrating.

For you, that means:

You don’t have to hunt down paperwork or guess details about your home

You can get a quote in minutes, not hours

You can see a price upfront without pressure or obligation

You’re less likely to get surprises later, because the quote is based on real property data, not assumptions

By using verified information from the start, we reduce back and forth, delays, and confusion. You stay in control, with clearer information and fewer hoops to jump through.

In short, less admin for you. More confidence in what you’re looking at.

Our technology doesn’t stop at the quote

The same thinking behind our quoting tool runs through everything we do.

If your situation is straightforward and uncomplicated, you can:

Get a quote

Tailor your cover

Set up your policy

Become a customer

All in just a few minutes, online.

That tech-first approach also carries through to claims. Lodging a claim is designed to be simple and clear, with digital tools that guide you through the process and keep things moving. No unnecessary steps, no guesswork about what happens next.

We use technology where it genuinely helps, and people where it matters. That balance is what allows us to move quickly without losing the human side of insurance.

Summary

What began as a simple solution to a common problem has grown into an award-winning innovation. But the real benefit isn’t the awards. It’s the time saved, the clarity gained, and the confidence customers feel when organising their house insurance online.

Natasha has been with initio since 2023. In her first year, she worked closely with the support and marketing teams before moving into digital marketing.

She has studied with ANZIIF and holds a qualification in Understanding General Insurance Products and Policies. She also completed a Bachelor of Business at the University of Waikato, majoring in Strategic Management and Marketing.

There’s a lot to juggle when you’re buying your first place – deposits, lawyers, moving trucks, the lot. Sorting out home insurance when buying your first house is another step, but it doesn’t have to be confusing.

You’ve got enough to think about. We’ll make insurance the easy part.

When do you need insurance?

One of the biggest surprises for first-home buyers is when insurance is actually required. Most banks won’t release your loan until they’ve seen confirmation of cover. You can’t leave it until after settlement.

Here’s how timing works:

Auction: Check in advance that the property is insurable before bidding.

Settlement day: Even with an unconditional offer, you’ll want cover active from the moment you take ownership. Learn more about when your cover needs to begin.

Sorting your insurance early gives you peace of mind and avoids last-minute stress.

Best when you’re still finalising the purchase or need something fast. Get a quote online, customise your cover, and download the Letter of Intent instantly to show your lender the property can be insured.

Once you’ve bought the home, complete your sign-up, pay your premium, and receive the Certificate of Insurance by email. This confirms your cover is active from settlement day. All you need is your new address – no phone calls, no delays.

What to look for in your policy

Insurance isn’t one-size-fits-all. Before you buy, think about:

Sum insured: The rebuild cost of your home (not the market value). Include demolition, site clearance, and GST. Use our calculator to help you estimate the rebuild cost.

Excess: What you’ll pay if you make a claim. Higher excess lowers premiums but increases out-of-pocket costs.

What’s not: Wear and tear, gradual damage, or maintenance issues.

And don’t forget contents cover – your furniture, electronics, and valuables add up quickly.

Mistakes first-home buyers often make

It’s easy to treat insurance like a box to tick, but the wrong choice can leave you out of pocket. Common mistakes include:

Underinsuring: Cutting corners on your sum insured lowers premiums but leaves you short if disaster strikes.

Guessing rebuild costs: Use a calculator or valuation instead of rough estimates. Learn more about calculating rebuild costs.

Chasing the cheapest price: Low-cost policies often have gaps in cover or poor claims support. Use our online comparison tool to compare cover options between leading NZ insurance providers.

Picking the wrong excess: Balance affordability with what you could realistically pay. Learn more about insurance excess

Forgetting contents and car cover: Protecting your house is step one, but your belongings and car matter too. Access our contents calculator tool to work out the value of your belongings.

Why initio works for first-home buyers

You don’t just need cheap insurance – you need cover that works when it matters. That’s where initio comes in:

Watch our video where Guy, our Head of Partnerships, explains what insurance actually does, why banks care about confirmation of cover, and how to avoid common traps as a first-home buyer.

Gilligan Rowe + Associates and Initio have teamed up to provide you with a competitive online option for your house insurance, including rental properties and holiday homes.

Add your property details below to get a quick insurance quote. If you like what you see you can start the cover online with payment by credit card or bank transfer. You will then instantly receive the cover confirmation by email. It’s that simple.

If you need any assistance insuring online, or would like to arrange cover offline, click here to contact us.

Homeowners and Landlords are facing significant financial pressure in 2023.

The increase in mortgage rates, combined with rising property insurance costs, has put a strain on homeowners cash flow and the budgets of landlords, who are facing increased costs without a corresponding increase in rental income.

In addition, over the last couple of years tax changes have meant that landlords who don’t own new builds can no longer fully deduct the cost of interest as part of their annual tax return. So it’s a double whammy when it comes to interest rates; pay more, less tax relief.

As well as mortgage interest and council rates, a major expenditure item for homeowners is insurance. This article looks at house insurance costs, where they are heading, average cost per region, and what you can do to keep yours at bay.

Why are insurance costs rising?

Build costs:

The significant increase in construction costs over the last 3 years has meant that landlords (and homeowners alike) need to increase the insured value of their homes if they are to remain fully covered.

Increasing the insured value of a house means more risk to the insurer, which ultimately means more premiums to cover that risk. In short, it costs more to buy more. In some cases, homeowners have had to buy 20%+ more cover to keep the ‘full cover’ they want. If the house is located in a remote region then the supply of materials and labour to that location will cost more.

Regulatory changes:

Contrary to popular belief, a house insurance policy does not provide cover for land damage (e.g landslides), and the cost of repairing a house damaged by an earthquake is funded (to a certain level) by the Government through the New Zealand Earthquake Commission (EQC)

In October 2022 the EQC increased their levy. For most houses this is an increase of over $200. This levy is included in the insurance bill you receive from your house insurer.

This is the insurance that insurers buy so that they can pay claims in a major event. For example if an event, such as a flood, causes losses to an insurer that exceed a certain amount, e.g. $20m, then the reinsurers pick up the tab after that.

Insurers in New Zealand are required by the Reserve Bank to carry enough capital reserves or reinsurance to pay all claims arising from a 1 in 1000 year natural hazard or weather event. This is an incredibly significant event. To put it in perspective the Auckland 2023 floods were a 1 in 200 year event.

In most other countries the requirement for insurers is 1 in 250 years, meaning that New Zealand has the highest threshold for cover imposed on its insurers compared to anywhere in the world.

This high level of cover costs insurers a lot of money, and they pass this cost onto individual homeowners.

Location of property:

The location of your property has a major influence on premium.

For example, Wellington properties are notably more expensive to insure (with insurance cover increasingly difficult to obtain). The seismic risk in Wellington, and other parts of NZ, mean that it is a lot more expensive to insure in Wellington compared to much safer areas such as Dunedin and Hamilton.

Insurers are also starting to use premium modelling called ‘risk-based pricing’. What this means is that instead of a cross-subsidisation approach, the insurer will charge a premium for a house that is directly related to the risk of that house. Traditionally insurance has been a ‘premium pool’ based approach where the many pay into the pool to help the few that need to claim – but this approach lacks fairness given that homeowners in lower-risk areas start to subsidise those that claim a lot more due to seismic risk or adverse weather. The risk-based pricing approach has its own shortcomings as it means that for some people, e.g. coastal properties, the house insurance premium becomes so high that it is not affordable.

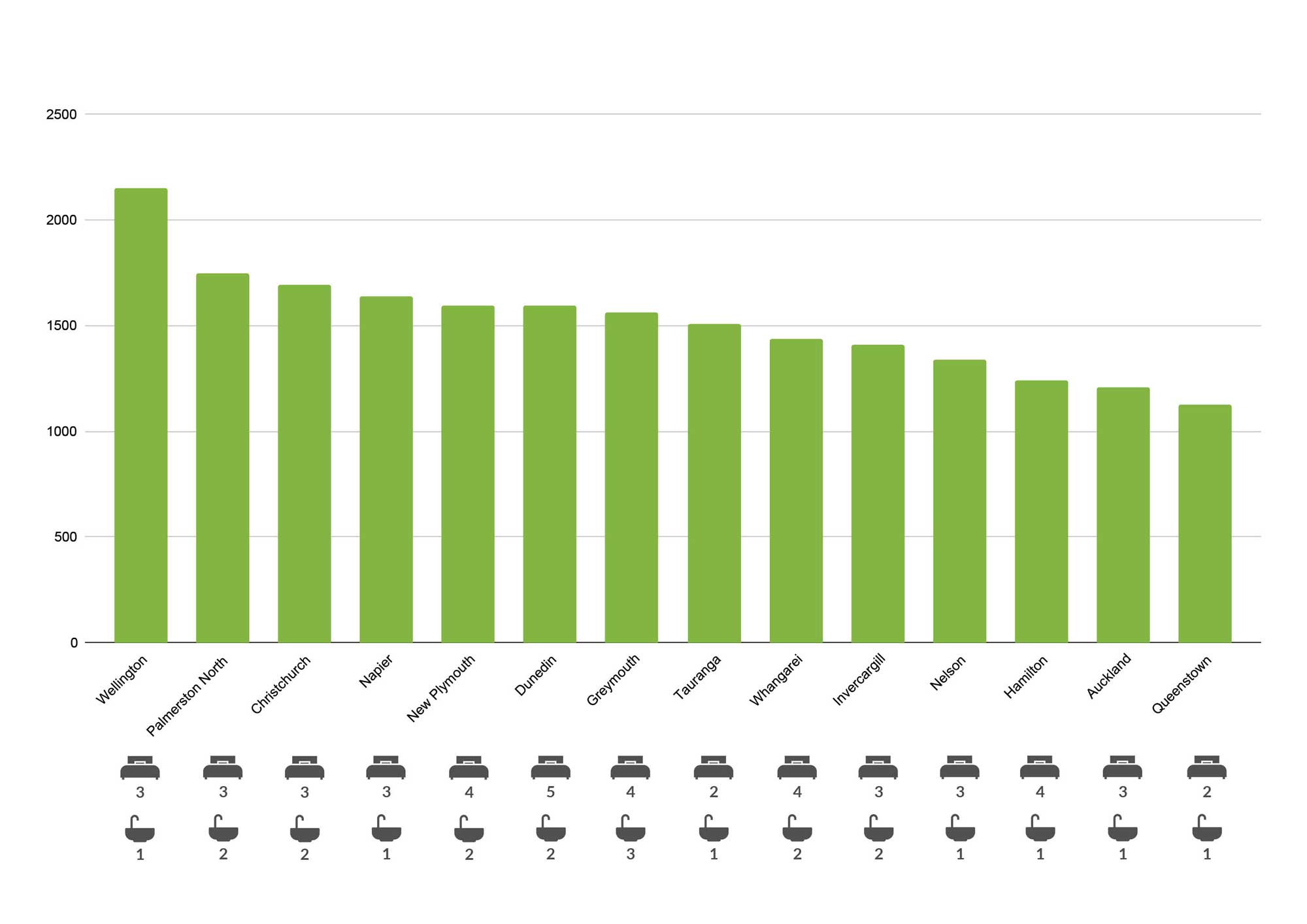

This graph provides a snapshot of the average premiums across different regions (without pure risk-based pricing):

The above graph is based on Feb 2023 homes.co.nz insurance cost estimates (powered by Initio) – for properties valued between $695,000 – $710,000. Insurance cost (incl gst) is based on an excess of $650 and does not include contents.

Attention to age of the house:

Some insurers are paying more attention to the age of the home to calculate its insurance premium. Houses built in the 1980’s for example are attracting higher premium loading due to issues with the plumbing of the era.

Similarly, houses built before 1940 are now considered ‘older homes’ by most insurers, and as well as additional requirements on the homeowner to verify that the roofing, plumbing and wiring have been replaced or are in good condition, the cost of insurance is higher than houses built post the 1940 decade.

By large newer homes (post 2010) attract the lowest premium for age.

Increase in the frequency and severity of weather events:

The average number of significant weather events for the decade ending 2020 was 9.7 per year. In 2021-22 there were 21. So far in 2023 we have seen 3 significant weather events.

More floods, cyclones and natural disaster events lead to more damage, and the majority of the repair and rebuild costs are borne by insurers. In simple terms, an insurer wants to make sure that its costs do not exceed its premium income. The single biggest cost to an insurer is what it spends on responding to and paying for insurance claims, but things like reinsurance (discussed above) and operating costs (staff, compliance costs etc) are also major expenses.

Increases in claims, at a macro level, put significant pressure on the premiums charged to homeowners, and because recent years have seen a large increase in claims, house insurance premiums have been adversely affected.

Here’s the good news! There are ways you can combat rising insurance costs.

Homeowners and landlords can adopt some strategies to help control their rising insurance costs, and also help prevent damage from occurring in the first place, as let’s face it, whether insured or not, no homeowner wants to deal with damage or loss:

Pay annually: For most home insurance, if you pay your premium annually it will be cheaper than the annualised equivalent of paying monthly.

Increase excess: The higher the excess the lower the premium. Insurers are now offering excesses as high as $2,000. This means that you will have to contribute $2,000 every time you have a claim. If you don’t claim often and you can sustain a higher excess then this is a good way of reducing your insurance costs.

Combine policies: Purchasing policies like house and personal contents together will often help reduce the overall premium, as combined to buying these policies separately.

Shop around for the best deals: Shopping around for insurance coverage can help ensure you are getting the best deal. There are comparison tools available to help you compare policies from multiple insurance providers. Remember that cheapest is not always best, so it pays to check what you are getting for your insurance spend.

Regular maintenance: A leading cause of water damage to the home water entering through overflowing pipes and gutters. Ensuring gutters are cleared regularly may just prevent that wet ceiling.

Electrical appliances: Powerboards or multi-plugs can cause house fires if they are old or low quality. Take the time to check these items in your homes or during a tenancy inspection.

Security: At home security is now more accessible than ever. The last few years have seen a number of connected security devices become available to homeowners. Products such as the Nest Protect Smoke Alarm not only save lives but can save houses too. Security cameras and alarms are a useful way to discourage intruders and reduce the risk of burglary.

Fire extinguishers: Too many kitchen fires could have been brought under control with the use of a simple, and low-cost, fire extinguisher. Having fire extinguishers in your home or rental property will reduce the severity of damage. It is also important to ensure everyone in the household knows where they are located and how to use them. Learn more about fire extinguishers.

Initio insurance; Quote in seconds, cover in minutes, claim in an instant.

As you pay for your insurance you might wonder where your premium is going? And how is it calculated? This guide explains what makes up the cost of house insurance and how it’s calculated.

Insurer Premium

This is the insurers cut of the pie and is what the insurer receives in compensation for taking on the risk that you don’t want to carry yourself. This is the variable component of the overall premium which will be higher for riskier properties and lower for a less risky property.

For example, a premium comparison between a landlord insurance policy for a rental property located in Auckland and one located in Christchurch will show a significant difference in premium. This difference in premium is due to the risk exposure to earthquakes. However, there are many factors that determine the premium of your property – such as the relative exposure to weather events, flood zones, vulnerability to theft and the historical record of claims in the area.

In short, insurers use the following factors to calculate what premium they want for the risk.

a) Location of your property

The cost of your insurance is mostly based on how likely it is that your area will have an earthquake or storm. Some places are more at risk than others because of past claims. Nowadays, many insurance providers use “risk-based pricing.” This means areas with less risk, like Hamilton, no longer help cover the cost for higher-risk areas like Napier.

b) Water supply or distance to fire station

The closer a house is to a fire station and the better the access a property has to water, the less likely it is to burn to the ground. For example, a rental property immediately next to a fire station will have a lower premium than a rental property that’s 30 minutes out of town and has rainwater tanks for its only form of water.

c) Age of the property

Houses built prior to the 1940’s are more likely to have older building materials and methods. A common cause of damage are electrical fires caused by old and corroding wiring. Water damage from by old pipes failing under increased town water pressure is also common. Learn more about insuring older homes here.

There are also certain decades where the New Zealand construction industry (and the Government) allowed the use of certain plumbing products and cladding systems that continue to be a source of significant property damage. Houses built in the 1980’s are most likely to be constructed with Dux Quest piping and fittings. Quest was taken off the market in the late 1980s but there are still a number of houses suffering water damage from poor performance of water pipes and fittings.

d) Use of the property

This one goes to human nature. It’s a fact that people take better care of things they own. This means that houses occupied by their owners have few losses than those occupied by tenants or short staying guests. A rental property attracts landlord risk (such as malicious damage and loss of rents) so a landlord insurance policy will cost you more than the insurance cost for your own home.

Holiday homes are often empty for longer periods of time. This can make water damage more expensive to fix. There’s also a higher chance of break-ins and burglary.

e) Replacement value of the property

The more your house is worth, the more you’ll pay for insurance. But it’s not as simple as saying a $1,500,000 house costs twice as much to insure as a $750,000 one. After a certain point, the cost of insurance goes up more slowly. This is because most insurance claims are for small things, like a leaking pipe, rather than big things like a house fire.

f) Excess and extras

An excess is the amount you’re willing to pay when you make a claim. The more you agree to pay, the less risk for the insurance provider, especially for small, frequent claims.

Adding extra types of cover can also make your premium go up. For example, if you decide to increase your ‘loss of rents’ cover, you’ll pay more.

Government Earthquake Levies

Your insurance cost includes a government earthquake levy. This money goes to the New Zealand Natural Disaster Fund. It covers natural disasters, like earthquakes, up to $345,000 including GST. Since October 1, 2022, this levy has gone up to $552 including GST for each home covered by your insurance each year.

If an earthquake happens, the first $345,000 of damage is paid for by the Earthquake Commission. Any amount over that is covered by your insurance provider. We collect this levy as part of your total insurance cost and give it to the Earthquake Commission.

Government Fire Service Levies

Your insurance also includes a fire and emergency service levy. This helps pay for emergency services like fire brigades and ambulances that benefit everyone in New Zealand.

This levy is $106 + GST for each living unit, and an extra $21.20 + GST if you also have cover for contents. Like the earthquake levy, we collect this money as part of your total insurance cost and give it to the Government. Even if you choose not to have home insurance, you’ll still benefit from these services.

Goods & Services Tax

Like all domestic goods and services in New Zealand, a 15% GST tax is then applied to the total insurance cost (insurer premium, NHC (was EQC) levy, and FSL levy). The total of all four of these makes up the total premium payable by you, the insurance customer.

As a practical example, a single unit landlord insurance policy with a total annual insurance cost of $1,000 including GST consists of 55% government levies and GST.

Where can I find the breakdown?

On our quotations and options of renewal, you can find the breakdown immediately below the monthly and yearly total cost figures. If you hover over the coloured bar, the system will display each relevant amount. Once you purchase a policy a receipted Tax Invoice will be emailed to you which outlines the full breakdown. Historical Tax Invoices can also be downloaded from your initio dashboard at anytime.

This guide has been produced to provide more transparency on how insurance premiums are calculated. Much of the way the insurance industry operates is a ‘black box’ of jargon – but when it comes to something so important as the cost of house insurance it shouldn’t be complicated.

Living near the coast has a lot going for it. Sea views, beach access and a relaxed lifestyle are a big drawcard. But coastal properties can also come with additional risks, which means house insurance is often one of the first questions buyers ask.

If you are buying, owning, or thinking about selling a coastal property, it helps to understand how insurers assess risk, and how to navigate coastal risks with confidence.

Key things you’ll learn in this article:

Whether coastal properties can be insured, and what insurers assess

How flooding, erosion and subsidence affect insurance decisions

Why some coastal homes require a customised solution

What long-term insurability could mean for owners and buyers

How to check if your property can be insured

Can I insure a coastal property right now?

In many cases, yes. Being close to the coast does not automatically make a property uninsurable.

Initio can insure a wide range of coastal properties, provided the risk profile meets our underwriting criteria at the time cover is considered. When assessing a coastal home, we look at factors such as:

proximity to the coastline or waterways

flood history or flood modelling for the area

exposure to coastal erosion

land stability, subsidence and coastal erosion risk

local hazard maps and council information

previous claims or known damage

You can obtain a quote online using the information available at the time and the details you disclose as part of the application. Depending on those details, the application may be able to be confirmed straight away, or it may be referred to our underwriting team for review before cover is confirmed.

In some situations, we may not be able to offer cover through our online model. This does not necessarily mean the property is uninsurable, but rather that it may require a more customised insurance approach that sits outside what initio is able to provide.

Does initio have concerns about erosion, flooding or subsidence?

These are some of the key risks we assess for coastal properties.

Flooding

Flooding is one of the most common risks for coastal homes, particularly where properties are close to estuaries, rivers, low-lying land, or stormwater outlets. Heavy rainfall, storm surge and rising sea levels can all increase flood risk over time. In some coastal areas, king tides can also contribute to higher water levels, particularly when they coincide with storm events.

Coastal erosion can occur gradually over many years, or suddenly during severe weather events. Properties built close to cliffs, dunes, or unstable shorelines can be more exposed to this risk.

Subsidence, land movement and coastal erosion

Coastal land can sometimes be affected by subsidence, erosion, or other forms of land movement, particularly where soils are soft, saturated, or influenced by changing groundwater or coastal conditions.

Subsidence and coastal erosion themselves are not covered under most house insurance policies. However, evidence of either can increase the likelihood of other insured events. For example, land that has experienced erosion or subsidence may be more susceptible to landslip or slope failure during large weather events, which can be covered under a house policy.

For this reason, insurers consider subsidence, land movement and coastal erosion together when assessing the overall risk profile of a property.

These factors do not automatically make a property uninsurable, but they do influence how insurers assess cover, pricing and long-term sustainability.

Why some coastal properties need a customised insurance solution

Initio is an online insurance provider. Our policies, pricing and underwriting are designed to work efficiently for a wide range of homes without the need for one-off or bespoke policy structures.

For most properties, this allows us to offer fast quotes, clear cover and easy ongoing management. However, some coastal properties have risk profiles that sit outside what can be supported through a standard online insurance model.

This can occur where a property has one or more higher or more complex risks, such as:

significant exposure to coastal erosion

repeated or severe flooding history

known land instability or subsidence

reliance on ongoing protective or mitigation works

access challenges that affect emergency response or repairs

Where a property has these characteristics, it may require a customised insurance solution tailored specifically to its risks.

Unfortunately, as an online insurance provider, initio is unable to offer customised or bespoke insurance solutions. This does not reflect the quality or care of the property itself, but rather the way certain risks need to be assessed and managed.

Our focus is on being upfront, consistent and clear, so customers can understand their options and navigate coastal risks with clarity.

Insurance decisions are based on the best information available at the time, including hazard modelling, claims experience and climate data. As this information evolves, insurance settings can evolve too.

For many coastal properties, any changes tend to happen gradually rather than all at once. Over time, this might mean things like:

fewer insurers offering cover in higher-risk areas

If a property already needs a more customised insurance approach today, it can be a sign that the risk profile is more complex than average. This does not mean insurance will suddenly become unavailable, but it is something buyers and owners may want to keep in mind as part of longer-term planning.

For some buyers, insurance is becoming another factor they consider alongside location, price and future maintenance.

If a property is more expensive or complex to insure, that may influence how some buyers assess value. That said, many coastal homes remain highly desirable, and insurance is just one piece of the overall picture.

Thinking ahead about insurability, maintenance and risk mitigation can help support both ongoing cover and future resale appeal. If you are purchasing at auction or under conditional agreement, our guide on obtaining a letter of intent explains how to confirm cover during the buying process.

Things to consider when buying or owning coastal property

If you are considering a coastal home, it can help to: