Search results for: {search_term_string}/get-quote/house-insurance-calculator

Pro-tips for property owners. Tip #5: Streamlined insurance

For our final topic, we’re looking at why having all of your insurance eggs in one basket is actually a good thing. Last year’s natural disasters brought numerous challenges for those who suffered losses. Managing multiple claims with different insurance providers would’ve been like trying to herd cats during a thunderstorm. You should never undervalue your time of peace of mind.

Consider streamlining your insurance

Having all your policies with one insurance provider simplifies your insurance management. It’s about making your life easier, reducing the jigsaw puzzle of policies to a single, manageable picture. Less time spent on paperwork means more time for…well, anything else.

Initio offers a range of insurance options to cover all aspects of your life. From home & contents to vehicle, landlord, and holiday home insurance, we have you covered. It’s like having a Swiss Army knife in your pocket, but for insurance. Fancy a quick quote? It couldn’t be simpler. In less than 10 seconds, you can see how we stack up against your current provider across the board.. And who knows? You might be pleasantly surprised by our competitive rates and the convenience of having all your insurance needs met under one roof.

Get a quote in seconds for our most popular insurance options:

| House & Contents | Landlord | Vehicle | Holiday Home |

|---|---|---|---|

Combining your insurance policies with the same provider is a smart move. You could save some cash, keep your insurance documentation tidy, and make claiming a breeze. Why not review your current insurance cover and see if bundling them might suit your needs better?

Here’s something to chew on: sticking with one provider for all your insurance needs means less hassle and fewer payments to juggle. As the old saying goes, time is money.

OTHER ARTICLES OF INTEREST

Initio Insurance launches Live Policy

Initio, the first insuretech company in New Zealand to provide instant online house insurance, announces that it has given even more control to customers by launching another NZ first, Live Policy.

Live Policy means that customers can instantly modify or add to their insurance in an on-demand fashion without having to nervously wait for a confirmation.

The traditional process of getting and modifying insurance remains clunky and broken. When it launched in 2010 initio was transformative in giving homeowners and landlords the ability to effortlessly quote and purchase house insurance online and in real time through its website www.initio.co.nz. A process that takes less than five minutes without the need for paper applications or long winded phone calls.

Initio has today taken their market leading approach a step further. Through a personalised dashboard, Initio customers can now fully manage and modify their insurance policy instantly and whenever they want. This luxury does not exist with other insurers, who require the customer to make direct contact by phone or email to request the cover change.

Initio’s Live Policy means that the customer is in charge. Anytime, day or night, the customer can modify their insurance cover in a multitude of ways. This includes being able to increase or decrease the replacement value or excess of their own home, holiday home or rental property. Crucially, Live Policy also means that the customer can add to their cover an engagement ring they purchased on the weekend. Waiting till business hours on Monday to get insurance cover is now a thing of the past.

“It’s about giving the customer total control over their insurance and it’s about getting away from having to wait in-line at a call centre. We felt that being able to modify your insurance when you wanted adds significant value to a more transparent and responsive insurance experience – so we built Live Policy.” says initio CEO and co-founder, Rene Swindley.

Since its inception initio has always used technology to push the boundaries of insurance for the benefit of the end user. “Insurance doesn’t need to be complicated” says initio CTO and co-founder Sam Brook. “Our overriding mission is to make insurance more approachable for homeowners and landlords, Live Policy is a significant digital milestone for both initio and insurance in New Zealand”.

There’s been a natural disaster, what happens next?

This is why you have insurance.

You’ve purchased insurance from us for exactly this type of situation. Most importantly, make sure you and your family are safe and dry. We are here to get your house, vehicles and belongings back up and running. Here’s some important information and tips on how to best handle things:

Your response

- Follow advice: Listen to official information channels and follow the directive of Civil Defence and emergency services

- Ensure safety: Make sure you, your family, and pets are safe. If someone is missing, contact emergency services immediately.

- Grab essentials: Take your emergency bag and a lockbox containing important and financial documents.

- Address health needs: Look after any physical injuries and emotional distress.

- Secure your home: If your home is damaged but standing, secure it. This might include temporary repairs.

- Document damage: Take photos of any damage for insurance purposes.

- Safeguard valuables: If possible, move valuable items to a secure location, like a friend’s house or a storage unit. Your insurance might cover storage costs.

- Contact your insurance provider: If your home needs urgent repairs and is still habitable, contact your insurance provider. Remember to document everything and keep all repair receipts. Be cautious of repair scams.

- We will prioritise claims with serious damage and uninhabitable houses. If this is your situation and you require additional support after lodging your claim you can get a hold of us through [email protected] or by phone 0800 763 929

- If you have ‘black water’, i.e. rising flood damage, and you want to get on with cleaning up you can lift the carpet and underlay and move it outside.

- For damaged contents, start to make a list and take photos. Retain as many items as you can as an Assessor may want to see them.

- If emergency temporary repairs are needed to mitigate further loss/damage to the property, engage a tradesperson and send us the costs to add to the claim. For example, securing lose roofing.

Vehicle damage?

- If your vehicle has been in deep water (over the tyres) do not attempt to drive the vehicle due to the potential risk of electrical damage and contamination.

- Use a permanent marker to mark on the vehicle where you think the water level got to.

- Lodge a claim online through your dashboard when you get a chance.

- For abandoned vehicles we will arrange for the vehicles to be towed when roads are open and tow trucks have availability. Please let us know during the claim lodgement if the vehicle has been abandoned away from your usual residence.

- Where possible and only if it is safe, remove personal belongings from the vehicle.

If you have had to leave your home

If you’ve moved into temporary accommodation, lodge your claim as soon as you can and include the cost of your stay so it can be prioritised as part of your claim.

Owner-occupied homes: Do I have cover for alternative accommodation, a place to stay?

Yes, all initio own-home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you are required to evacuate your residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR if your home is at risk from an insured event such as a flood. Keep receipts and note the dates of your stay — these costs will be included in your claim.

Rental properties: Do my tenants have cover for alternative accommodation?

If you are a landlord and your rental property is unable to be lived in because of the damage you are not responsible for finding your tenant’s alternative accommodation. This is something they are responsible for and their renters insurance would usually cover. However, with initio’s landlord policy, you do have cover for loss of rent if your rental property is uninhabitable.

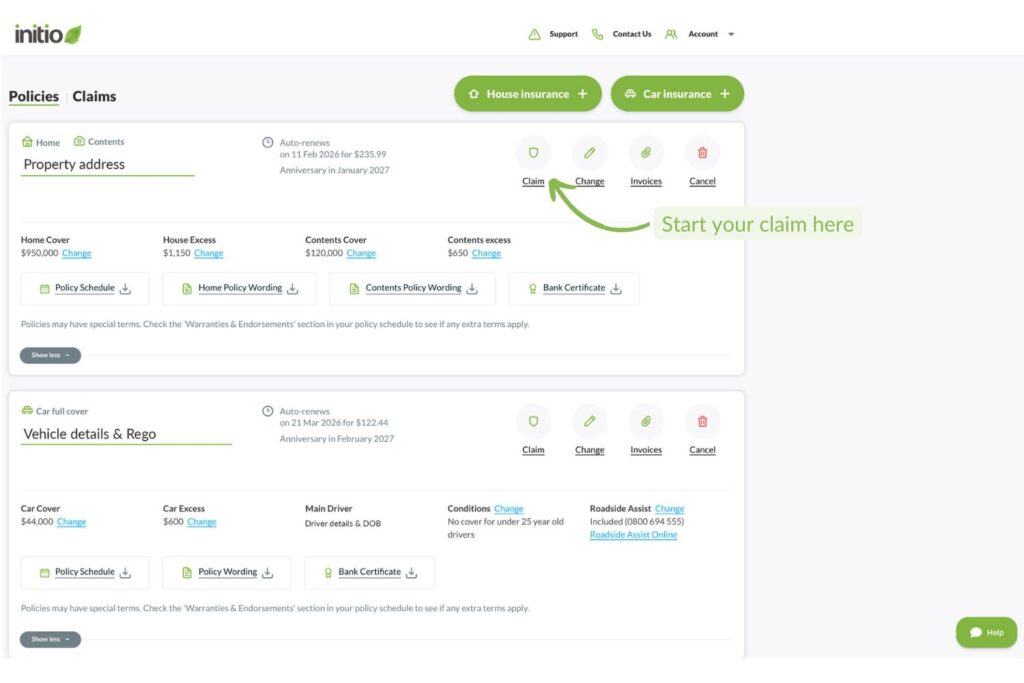

Lodging a claim

With initio, lodging a claim is easy. Just login to your customer dash and click on the ‘claim’ icon to the right of your personal information.

Our easy-to-use questionnaire will step you through lodging your claim. We don’t expect you to understand your policy thoroughly, so we explain things along the way. Once your claim is lodged you will get a confirmation email and you can also see the claim’s progress on your dashboard.

To learn more, this guide walks you through how to claim with initio.

Provide as much detail as possible

When you make a claim, include clear and detailed information. This helps initio assess how urgent your claim is and what support you need. The smart claims platform can adjust its questions during large events, making it easier to understand your situation and prioritise help where it’s most needed.

Upload photos of the damage

Photos are key to understanding the extent of the loss. Upload them when lodging your claim — or later, if needed. Include shots of anything relevant, like flood levels, structural damage, or affected areas. The more visual evidence you provide, the faster and more accurately your claim can be handled.

Timing after a major event

Your safety comes first. Once it’s safe and you have internet access, submit your claim as soon as you can. If you’re unable to do this right away, that’s okay — just lodge it promptly when possible. If you need immediate advice, you can always call for help.

Our response to major events

Following any natural disaster, we usually receive a significant number of claims. Our team will work on prioritising and acknowledging your claims. Our focus will be to ensure people are safe and that homes are secure following damage.

If you receive a quote from a contractor please send it to us as we take a pragmatic approach to repairs. We prioritise claims for those vulnerable, most in need, emergency accommodation, and serious damage.

Other tips

- Never wade through flood water and avoid using vehicles or electrical appliances that might have water damage.

- Wear gloves, masks, and protective gear so you don’t come into contact with anything dangerous.

- Turn off the power at the mains if flood water has entered the home.

- If you are a landlord, check in with your tenants

- Learn more about staying safe on the Civil Defence website

NHC (previously EQC) Claims

Claims from a significant event may include areas of damage which NHC covers and also areas which NHC does not cover. All claims need to be lodged with us in the first instance, and then any NHC aspects are referred to NHC internally. This means that you only have to deal with initio (rather than also with NHC), but in the case of significant events, NHC claims can take a while to be processed. NHC claims are assessed in line with the Natural Hazards Insurance Act 2023 (NHI Act), we are bound to the due process that has to be followed.

FAQ’s

Can I start cleaning up?

Yes, but take photos and keep a schedule of damaged contents/items you remove from the house

When will an Assessor come and see me?

We are currently appointing assessors and priority will be given to those with serious damage and to those homes that are accessible.

Do I need to find accommodation for my tenants?

No, you can if you like but this is not your responsibility. Your tenant(s) will have to sort this on their own and they will incur costs to do this, however, if the house is not habitable they will be entitled to stop paying you rent. You can claim this loss of rental income through your landlord policy.

My house needs drying, how do I do that?

We use the services of Jaes for drying and extracting water. We will be working with them on the most serious losses, but it could take many days before they can get to you. If you have your own ability to source pumping or drying equipment you can add this to the cost of your claim.

Do I have cover for alternative accommodation, a place to stay?

Yes, all initio Own Home policies provide cover for the cost of finding emergency accommodation or temporary accommodation if you the homeowner is required to evacuate the residence by a local authority or government agency (like a council, Civil Defence, NZ Police or Fire and Emergency NZ) OR because the property is at risk of damage, from an event that would be covered by the policy. Flood damage is automatically covered for initio policyholders. Keep copies of accommodation receipts and record timing/dates and we will include these costs as part of the claim.

Am I covered for damage to my land?

The Natural Hazards Commission (previously EQC) provides certain cover for land damage; the NHC provides more than just cover from earthquake damage. Your insurance policy with initio includes NHC cover, and if your land is damaged by storm or flood, you’re eligible to make an NHC claim. To make the claim process simpler, you no longer have to claim through the NHC, we/our underwriter (IAG) will handle your NHC claim on behalf of the NHC. To understand more about how NHC land cover works see this NHC Landcover Guide

Other resources

- GENERAL: Civil Defence

- EARTHQUAKES: Geonet | NHC

Other initio articles of interest

Do you rent out a second dwelling solely for short-term stays?

If you have two dwellings on your property and one is used exclusively for short-term stays – such as an Airbnb or similar short-term rental arrangement – it’s important to understand your insurance options.

What insurance do you need?

Homes used this way are no longer classified as residential, as they are considered to function more like motels. Because of this you will require a commercial product to insure the home/unit.

What are your options?

Unfortunately, initio does not currently offer an insurance product that fits this type of use. Please contact a provider who offers commercial solutions, such as a broker.

Not quite what you’re looking for? Maybe some of these other scenarios suit you better:

- Renting out part of your home short-term

- Do you have a second dwelling on your property that you rent out?

- Insurance for a non-rented second home on your property

- Second dwelling on your property that your family lives in

- Renting out two dwellings on your property

How to think about risk (and why location isn’t everything):

Smart moves, part IV

In the fourth part of our chat with Graeme Fowler, we dig into risk – where it comes from, how to think about it as a property investor, and why you shouldn’t assume location alone will keep you safe.

Do natural disaster risks influence where you buy property?

“Not really. Any location can be hit. Look at Cyclone Gabrielle – it hit parts of the country hard, but none of my properties were affected. That wasn’t strategy – that was just luck.”

Graeme believes that chasing the “perfectly safe” location is unrealistic. Disasters don’t follow predictable maps, and if you’re insured properly, where your property is becomes less important than how it’s protected.

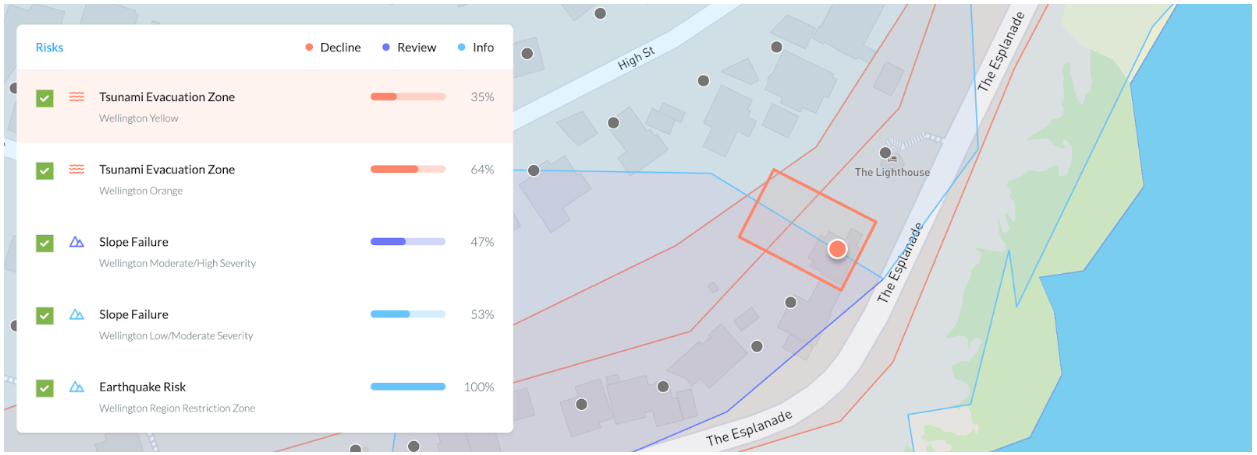

From initio: our quick quote tool, shows your property’s natural hazard profile upfront.

Do you consider climate risk in your buying strategy?

“I’m aware of it, but I don’t let it stop me. What matters more is making sure you’re insured properly – because whether it’s a storm, fire, or flood, anything can happen.”

Graeme says the best protection isn’t where you buy – it’s what you’re covered for.

From initio: Our landlord policies include comprehensive cover for events like storms and floods. But having the right type of cover is only part of the picture. It’s just as important to make sure your sum insured is accurate. This is the maximum amount your property will be rebuilt for after a total loss, so it needs to reflect today’s building costs – not what it might’ve cost a few years ago. You can check and update your sum insured anytime through your online account. Not sure how to calculate your sum-insured? The Cordell Sum insured calculator is a great place to start.

So, how should landlords think about risk?

“You can’t avoid it entirely – so accept that some risk is part of the game. Just make sure it’s managed. For me, that means keeping insurance current and making sure I’ve got enough cover.”

Graeme suggests thinking about risk as part of the cost of doing business, not something to fear, but something to plan for.

From initio: Risk management is at the core of what insurance does – we carry the risk for you. That’s what you pay us for when you buy a policy: to take on the financial risk of the unexpected, so you don’t have to.

Location plays a big role in how risk is assessed. Some properties sit in higher-risk zones – floodplains, liquefaction-prone areas, or coastal regions exposed to storms. But risk isn’t just about the region. Two houses on the same street can have different risk profiles based on their floor level, drainage, slope, or construction.

That’s why we do the heavy lifting in the background. Our system automatically pulls up-to-date risk data from government hazard mapping, scientific assessments, and advisory updates. When these maps change, due to new modelling or recent weather events, we update our software accordingly.

Our quick quote tool includes these insights from the start, showing you a property’s natural hazard profile upfront. So you’re not just getting insurance – you’re getting a risk management tool that helps you make smarter decisions.

When you quote or renew your policy, we make it easy to check your current risk profile, coverage level, and any potential gaps. If something doesn’t look right, we’ll let you know.

What’s your advice to landlords who worry about “what if” scenarios?

“That’s exactly why you have insurance. Fires happen. Storms happen. And sometimes you get lucky – but sometimes you don’t. The point is being prepared either way.”

Coming up next in the Smart Moves Series:

Is self-insurance ever a smart move for landlords? (Spoiler: Graeme says no.)

Want the quick version?

We’ve pulled together the key takeaways from this series into our Landlord Insurance Fundamentals Guide—including a bite-sized version of our interview with Graeme Fowler. It’s a great place to start if you’re after a practical overview of insurance essentials for NZ landlords. Read it here

Related support articles:

It’s not you, it’s us

A candid take on initio’s approach to you and your home

At initio we are ‘all-in’ on customer experience. We ruthlessly pursue customer satisfaction with our technology, support and communications …. But only for a certain type of customer. In short, we are not for everyone.

Yes, we’re audacious enough to say: “Sorry, we can’t be your insurance provider” – at least not if it means compromising the ethos that underpins our brand, or transacting with you in a way that doesn’t celebrate the use of our tech. We provide superior ease of insurance and customer service, but only to a specific kind of customer who appreciates and respects our ‘digital by default’ approach.

Catering to the Modern, Digital-Savvy Customer

Our business model is laser-focused on a modern, self-reliant breed of customers. The digital age has dramatically reshaped the insurance industry, and initio remains at the forefront of this transformation. We are designed for customers who value autonomy, speed, and convenience, rather than the traditional, hands-on approach.

Customers who are comfortable transacting online, managing their property portfolios with digital tools, and who comprehend that competitive premiums and high-touch hand-holding services are often mutually exclusive, are our ideal clientele. For these customers we are digital by default, and human when you need us.

The Interplay of Technology and Affordability

“Why can’t you just start the policy for me over the phone”

“Why don’t you call me every year when my policy renews so we can have a chat about it”

“Why can’t you just send me your bank account and I’ll transfer the premium funds”

“Send me a quote”

It’s a ‘no’ on all fronts. The truth is, high-touch insurance services involve considerable operational costs – think travel, long-winded phone calls, time, and administration. We’ve spent over 10 years building a digital platform that substitutes for these things; its frictionless insurance, that’s quote in one click, cover in 2 minutes, claim in an instant. By utilising technology to automate many aspects of our services, we increase efficiency and are able to offer competitive pricing.

Our system has been designed to suit a certain type of customer, and it’s not for everyone.

This doesn’t mean we shirk our responsibility to our customers that embrace our technology. Quite the contrary – we provide comprehensive digital and phone support, and abundant online resources to help.

Why we decline to insure some houses

Sometimes we have to say no to insuring your house. It’s not you, or your house, it’s simply the way we want to run our business and the rules we, and our insurer, have had to create to be able to offer our services long-term.

It’s digital too: The primary decision making on whether or not to insure your property is done by a smart tool we built called ‘Locatio’. When you type in your address with initio, Locatio makes decisions about whether initio can provide cover by using things like council property data, flood maps, earthquake and land risk.

In order to remain a sustainable and successful insurance provider we choose to focus on certain types of houses, and this means that there are some locations where we can’t provide cover, and certain risk exposures such as flood or land instability that are just not our bag.

We are constantly updating our business and underwriting rules, so just because we say no today, doesn’t mean that it’s a no forever.

You also need to know that we cannot sell you something that isn’t right for your situation either. So if your property does not fit our product we’ll decline to provide cover, and we don’t mean any offence by this.

The cost is the cost

A number of factors go into calculating the total cost of your home insurance, including location, age of the property, and other things like government-imposed levies. Our award-winning insurance technology computes the insurance cost, and we rely on that to run our business. The premiums need to be set at a level that allows the insurer the margins to continue to pay claims and reinsurance costs. In short, the cost is the cost.

Learn more about how the insurance risk component of your insurance cost is calculated

It’s 100% your choice whether or not to accept the insurance cost we offer. You can ring or email and challenge a cost but ultimately it’s out of our hands as the system has spoken. You need to know though that we work incredibly hard to maintain competitive premiums for our customers. We do this by continually investing in our technology for efficient processes, negotiations with our insurer, constantly refining the rules that determine how risky our portfolio of houses is (ultimately the more aggregated risk we take on, the bigger our premium pool needs to be).

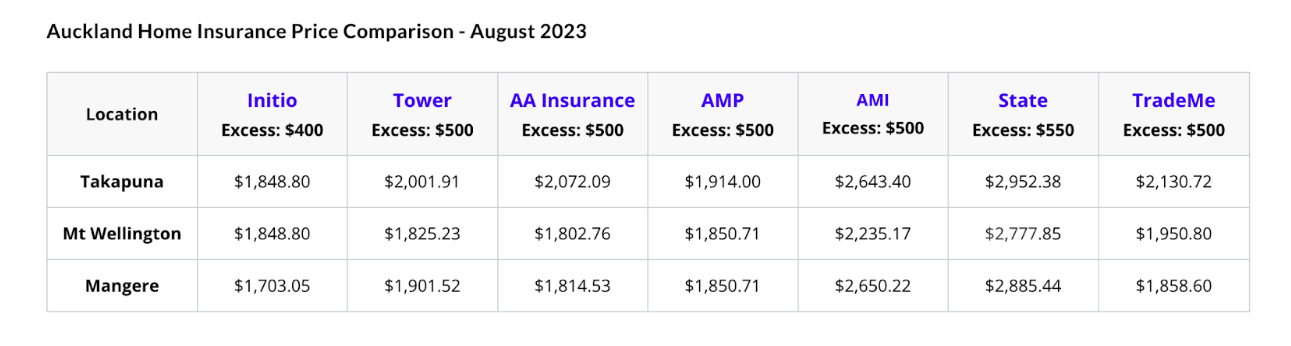

Our efforts to keep premiums competitive have been confirmed by feedback from our customers and also by financial resource websites like Moneyhub.

Source: Moneyhub

It’s simply not possible to be the most competitive all of the time, and we implore our customers to take a long and holistic view of their insurance that takes account of things like support (can you get you easily get ahold of your insurer), claims responsiveness, ease of use, technology and overall confidence in your provider.

It’s worth bearing in mind that not all policies are built the same, so just comparing price vs price doesn’t quite cover it. We highly recommend using our comparison tool if you want to see how we stack up when you also take the policies into consideration.

An Unapologetic Philosophy

Our philosophy is blunt but honest: “We are not for everyone”. Our model isn’t all things to all people, and that’s intentional. We’re looking for customers who align with our ethos – those who want a superior digital service.

While we understand some may expect more traditional customer service methods, we respectfully suggest they may be happier elsewhere. This is not a dismissal, but a candid admission that our service model may not suit everyone’s expectations.

In sum up, initio is unyieldingly committed to delivering our unique brand of customer experience, one that is unabashedly shaped by the needs of modern, digital-savvy customers. While our approach may not resonate with everyone, we are firm in our refusal to compromise on the affordability and efficiency that our model provides.

To our customers who find value in what we offer, we welcome you wholeheartedly. To those who don’t, we don’t hesitate to say: “We are not for you” And that’s how we maintain the balance that allows us to continue delivering what we believe is the optimal blend of service and affordability in today’s market… all driven by our technology.

Contents

Initio named MoneyHub’s favourite home insurance quote platform

We’re proud to share that initio has been recognised by MoneyHub as their Favourite Home Insurance Quote Platform. It’s an honour to be featured by one of New Zealand’s most trusted consumer platforms, known for cutting through the noise and helping Kiwis make confident financial decisions.

In a market where “best” is rarely clear-cut, MoneyHub doesn’t hand out praise lightly. Their awards focus on innovation, value, and customer benefit, not just big marketing budgets. That’s why we’re especially proud they’ve recognised initio for what truly sets us apart: our technology and market-leading customer service.

Real quotes, really fast

According to MoneyHub, initio’s platform delivers “a high-quality insurability assessment and property premium in under six seconds.” That means when someone’s looking to insure their home, they don’t get vague pricing or hoops to jump through – they get a tailored result, instantly.

And this isn’t by accident. Our quoting engine is the result of years of dedicated development. We’ve built the tech in-house, from the ground up, to be the fastest, smartest and most accurate in the industry. Every part of it is designed with the customer in mind, whether it’s pulling property data, calculating risks, or accounting for tricky scenarios like flood zones or multi-dwelling sites.

The gold standard in quoting

While some providers give a rough estimate or send your details to a call centre, initio delivers a real quote in real-time. No salespeople, no follow-up calls – just clarity and speed. It’s why landlords and homeowners alike rate our quoting platform as the most seamless and transparent in the market.

As MoneyHub puts it:

“The cyclone and flood devastation in early 2023 highlights the need for insurers to prioritise technology for claims and risk-pricing… Initio is future-focused and propelling the industry forward.”

We couldn’t have said it better ourselves. Because great insurance starts with great tech – and at initio, we’ve made that our mission.

Try our award winning quick quote out for yourself:

Quick House Insurance Quote

Related articles:

Residential Tenancies Amendment Act 2019 breeds uncertainty (Media Release)

Auckland, New Zealand – Initio media release

New tenancy legislation comes in effect today under the Residential Tenancies Amendment Act 2019 (RTAA). Among other things, the RTAA attempts to clarify liability for property damage between tenants and landlords.

As a specialist online landlord property insurance provider, Initio handles landlord property damage claims on a daily basis. Initio asserts the RTAA’s approach to property damage is misconstrued, creating uncertainty for both landlords and tenants.

Intention of the act

For property damage, the Residential Tenancies Amendment Act, seeks to:

- Make tenants liable for ‘careless damage’ caused to the rental property; but

- Allow tenants to share in and receive protection from the landlord’s insurance policy; and

- Limit tenant liability for careless damage to the amount of the landlord’s insurance policy excess or 4 weeks rent (whichever is less).

- Re-open the ability for the landlord to recover against the tenant for damage, albeit on a very limited basis.

Practical reality of property damage

Determining who pays for the cost, or insurance excess, of property damage is going to lead to disagreements between landlords and tenants.

“Many landlords have misunderstood the changes to the RTA and believe that the tenant will be responsible for the insurance excess on all types of claims,” said Rene Swindley, Initio CEO.

“The reality is that the tenant is only responsible for the excess on careless damage claims, which are uncommon. Over the last 12 months only 7% of our claims would be considered careless, meaning that for the remaining 93% it is the landlord who will be funding the insurance excess.”

The type of damage determines who pays

Initio has analysed its last 12 months of claims and determined that there are five broad ways a rental property can suffer damage:

- Damage (g. storm damage to the roof, or a leaking pipe). These account for 55% of Initio’s rental property claims. If the landlord is insured, the landlord pays the excess.

- Accidental damage by tenant (e.g. tenant slips and spills a glass of red wine on the carpet). This loss type accounts for 14% of initio claims. If insured, the landlord pays the excess for this damage.

- Careless damage by tenant (e.g. tenant leaves a pot cooking on the stove and goes to bed). Only 7% of initio claims are considered careless, meaning that the tenant is rarely responsible for the excess.

- Intentional damage by tenant (e.g. tenant smashes holes in a wall, meth contamination). Due to meth still dominating this damage type, 16% of initio claims are considered intentional. Landlords can obtain insurance for this type of damage. A landlord or their insurer can hold a tenant fully liable for this type of damage, but historically it is a difficult and lengthy process recovering costs (or an excess) from the tenant for intentional damage.

- Damage by a third party (e.g. a third-party vehicle impacts the fence). Only 8% of initio claims fall into this category. The landlord is responsible for the excess, but the landlord’s insurer has the right to recover the excess from the third party for the benefit of the landlord.

Accidental or careless? Arguments to come

While the RTAA assumes that the landlord and tenant will agree on the damage, there are many subjective damage scenarios where this may be unclear. For example, a glass of wine dropped on the carpet or hot pot burn on the kitchen bench can be construed as either ‘careless’ or ‘accidental’. As the classification of the damage has financial implications to tenant and landlord alike, it is inevitable that disagreement will arise.

Given that the cause of the damage determines who pays, Initio expects disagreements between landlords and tenants as to responsibility. If the landlord and tenant cannot agree on the type of damage the parties can apply to the Tenancy Tribunal for the mater to be resolved.

Change of insurance excess

Initio is a digital insurer that allows landlords to make on-demand policy changes.

“As Initio’s digital insurance offering makes it so easy for landlords to change an excess our technology has become a landlord sentiment barometer,” said Initio CEO Rene Swindley.

Initio does not recommend that landlords increase excesses as a reaction to the RTAA, as the higher excess will apply to all claims, not just the rare situation in which the tenant can be held responsible for payment. Swindley says that initio is watching its ‘barometer’ with interest.

When deciding on a policy excess, landlords need to think about the insurance excess in terms of both their own and their tenants’ ability to fund and cope with the excess. Given that it is a requirement for the landlord to provide details of insurance to a tenant, it’s clear that the level of insurance excess will form part of a tenant’s decision to rent a property.

In coming weeks as real-life damage to rental properties meets the new RTA, it remains to be seen how much tension is put on the landlord-tenant relationship.

About Initio

Initio is a New Zealand based online property insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home & contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with loss of rent, and cover for damage by the tenant.

Initio’s market-leading policies can be quoted, bought and amended online – all in an instant. Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

For more information on landlord insurance see https://initio.co.nz/landlord-insurance/

2019 Initio Claims Awards

Covering yourself for an unexpected event that leads to damage and financial loss is exactly what insurance is for. For house and contents insurance, you are most likely to think of your typical risks that might include fire, property flooding or theft of contents. However, insurance goes much further the ‘usual’ losses.

At initio we come across our fair share of unusual claims. As part of our ‘2019 in Review’ we go over our top 5 most unexpected claims – with a few honourable mentions. We are calling this the ‘Annual Initio Claims Awards’

Expect the Unexpected?

#1. Runaway Trailer

Sometimes damage can come from something outside of your control and your property. In late 2019, an initio customer in Te Awamutu was taken by surprise by a runaway trailer. Concrete was being laid at the building site next door and one the contractors loaded trailers became unhitched. The trailer was sent rolling down the hill and ended its journey by colliding the corner of our customers house and garage door.

This resulted in significant damage to the interior lining, exterior cladding and the garage door. Lucky for the insured their vehicles were not parked in the garage at the time, however a shelving unit and set of golf clubs were also destroyed. Saturday golf was put on hold unfortunately.

Total claim cost $19,187. In this instance, the concrete layers public liability insurer was pursued for the costs of this claim.

# 2. Colouring-in competition

When a customer rented their holiday home to short term guests they were not counting on their TV taking part in a kids colouring competition. The guest’s toddler thought they would hone their colouring in skills on the large flatscreen TV.

The artistic crayon drawings were cleaned off but the hard crayons left permanent scratches across the screen that could not be removed. A claim was made under their ‘landlord-holiday home contents’ which meant that the homeowner was able to replace their TV.

#3 . The Phantom Bather

An initio client with a multi-unit rental property was expecting it to be unoccupied for eleven days between tenancies. Two days into the property being untenanted, they received a call from their neighbour to say that there was water coming out of the property. It appeared an intruder had entered the property gone up the stairs and decided to run a bath.

Extensive water damage included saturated carpet upstairs that then seeped through the floor to downstairs. The ceiling in the kitchen and dining room downstairs collapsed, and significant water damage and clean-up was required through the property.

While we don’t know what the motives were for running the bath, we know that the landlord was happy to have an initio landlord insurance policy come to the rescue. With further costs still to come in the claim cost of repairs so far exceeds $32,000.

#4 . Rampant Puppies

After a tenancy had ended at an initio rental property early in 2019, an initio client lodged a claim for damage to the underfloor insulation. When repairers investigated the cause of loss, it appeared that the previous tenants family of puppies had found their way under the house, and shredded the flooring insulation from below.

Unlike many domestic insurance policies in New Zealand, the initio landlord insurance policy does not exclude damage caused by pets. After the landlord’s excess, Initio paid out $2,225.16 to repair and reinstate the insulation.

#5. Clumsy Chopping Board

While renting a holiday home, the guests popped down the road only to return to water running out the front door. They certainly didn’t expect to find water everywhere, a swelling to the kitchen, kitchen bench, cupboards, walls and floor.

It turns out that while they were out of the house a bread chopping board fell from its stand and landed on the sink tap. Not only did this turn the tap on, the awkward way it landed meant it also redirected the water away from the sink, running down the bread board and into the kitchen cabinets.

The aftermath damage resulted in water damage to the kitchen structures, damage to electrical components, and loss of rent payments as the sodden kitchen meant the property could no longer be rented. Total repairs amounted to $21,151.38 and are covered as sudden accidental water damage under the customers initio holiday home policy.

2019’s Honourable Vehicle v House Mentions

From AirBnB guests throwing a party to lightning strikes – we have had some interesting ‘honourable mentions’ lodged throughout the year.

Six claims were lodged with initio in 2019 for vehicle damage to properties – where a member of the public lost control of their vehicle and damaged our customers houses.

Three were involved in a police chase, whilst a further two were caused at the hands of drunk drivers.

Drivers who are responsible for damage caused are liable to cover the costs of repair. However in reality it’s difficult to get those responsible to accept liability (especially where it involves a police chase or drunk driving). Regardless of the driver accepting responsibility or being insured themselves (not that they would have insurance if drunk or in a police chase) initio provides cover for the damage caused to the property. We then pursue the driver.

The average claim for vehicle house damage in 2019 was $4,761.

‘Expect the Unexpected’ – You never know what could happen to your property. This is why it’s best to make sure you are covered for such unexpected and unusual events.

For more information on insuring different types see our insurance covers designed specifically for:

Home Insurance – for your own home, and contents.

Holiday Home Insurance – for the bach and for holiday homes that are also rented out (eg Bookabach, AirBnB)

Landlord Insurance – all in one house and landlord insurance, including loss of rents, malicious damage & more.

218-1 The Residential Tenancies Amendment Bill – how does it impact my landlord insurance?

This week, law changes to the Residential Tenancies legislation is set to strengthen renter’s rights. It aims to transition a landlord’s rental house into a tenant’s home.

Looking specifically at landlord insurance, the change that will have the most ramifications on landlord insurance is the removal of no-cause evictions. Essentially, it will be more difficult for landlord’s to remove bad tenants and from a risk management perspective this is not a good thing. Other changes to the legislation such as limiting rent increases, and banning rent bidding are unlikely to have a direct impact on landlord insurance.

Landlord insurance provides cover for intentional damage by tenants. If troublesome tenants are harder to remove then landlord insurers will consider that there is a higher risk that the tenant will cause damage to the property. It remains to be seen but this could lead to an increase in the value of deliberate damage insurance claims. Working out how and when the damage occurred could be further protracted when there is a tenant that is unwilling to co-operate and cannot be removed from the property. It has always been about working with the landlord, the tenant, and the property manager (if applicable) and this will not change when it comes to insurance.

While tenant damage could increase under the new rules, the legislation changes could in fact improve risk management and reduce the incidence of damage. Our view is that with bad tenants being hard to evict, it will mean that landlords increase their scrutiny during tenant selection. So, ultimately tenants with a poor record and lack of supporting references may find it harder to get rent a property, which would filter out bad tenants and lead to lower claims payouts for insurers.

The ultimate outcome of the law changes is difficult to predict. It is unlikely that insurers will make any adjustments to premiums or policy conditions as a result of the reforms.

The bulk of the legislative changes are set to be put into practice in early 2021. We expect that it will take at least 12 months before we see any outcomes or trends on claims.

About Initio

Initio is a New Zealand-based online house insurance provider. Founded in 2011 by a couple of Kiwis, Initio set out to change the broken insurance industry by using technology to put control back into the hands of the customer.

Covering landlord insurance, short-term holiday rentals and home and contents, Initio specialises in tailored online property insurance, including an all-in-one landlord insurance with built-in cover for loss of rent and damage by the tenant.

Having completed over 35,000 automated insurance transactions, Initio’s market-leading policies can be quoted, bought and amended online – all in an instant.

Initio is underwritten by NZI, a business division of IAG New Zealand Limited.

Stonewood Homes

dawson

Demystifying Insurance Excess

Choosing the right insurance excess can feel confusing. Your excess is the amount you pay towards a claim before your insurer contributes.

Understanding how excess works helps you balance your annual premium against what you would need to pay if something goes wrong.

Quick summary

-

An excess is the amount you pay when you make a claim.

-

A higher excess usually lowers your annual premium.

-

A lower excess usually increases your premium.

-

An excess applies per incident.

-

The right choice depends on your financial situation and risk tolerance.

What is an insurance excess?

An insurance excess is the portion of a claim you pay yourself.

For example, if you have a $1,000 excess and make a $10,000 claim, you pay $1,000 and your insurer pays the remaining $9,000.

Excess applies per incident. If multiple separate incidents occur, more than one excess may apply.

High excess vs low excess

When selecting an excess, you are balancing two costs:

-

Your yearly insurance premium

-

Your potential out-of-pocket cost at claim time

High excess

-

Lower annual premium

-

Higher payment if you make a claim

Low excess

-

Higher annual premium

-

Lower payment when you claim

A higher excess can work well if you are financially able to fund the excess and want to protect yourself mainly against major events.

How insurers calculate excess levels

Insurers use claims data and risk modelling to determine how excess levels affect premiums. They analyse:

-

How often claims occur

-

The average size of claims

-

Risk trends in different regions

-

Historical claims behaviour

The balance between premium reduction and excess size is based on these numbers. While some policyholders expect larger premium discounts for higher excesses, insurers must maintain a balance between premiums collected and claims paid.

When does a higher excess make sense?

Insurance is most valuable for significant events such as fires, floods or earthquakes.

Some property owners prefer a higher excess, such as $1,150 or $2,000, because they:

-

Are less concerned about small claims

-

Want lower annual premiums

-

Have the savings available to fund the excess

For landlord or owner-occupied properties, the highest available excess option is currently $2,000.

A practical example

Consider an Auckland property with a $700,000 replacement value.

-

With a $400 excess, the annual premium may be around $2,000.

-

With a $2,000 excess, the premium may reduce to around $1,500.

That saves $500 per year. However, if you make a $10,000 claim:

-

With a $400 excess, you pay $400.

-

With a $2,000 excess, you pay $2,000.

In that scenario, the higher excess leaves you approximately $1,100 worse off after factoring in the premium saving.

Over time, if you rarely claim, the savings from a higher excess can accumulate. The key question is whether you can comfortably afford the excess if a claim occurs.

Is choosing a high excess a form of self-insurance?

Yes, in a sense.

Selecting a higher excess means you are sharing more of the risk with your insurer. You are effectively self-insuring smaller losses while relying on insurance for large, financially stressful events.

Your personal circumstances matter

The right excess depends on:

-

Whether you are a homeowner or landlord

-

Your cash flow and savings

-

The age and condition of your property

-

Your claims history

-

Your tolerance for financial risk

New homeowners or landlords may prefer lower excesses for certainty. More experienced property owners, particularly those with multiple properties, may choose higher excesses to manage long-term premium costs.

How data can help your decision

Claims probability plays a role in choosing an excess.

For example, if you own 10 properties, statistics suggest you may expect at least one reasonable claim each year across the portfolio.

Understanding the following can help you make a more informed decision about your excess level:

-

Local weather patterns

-

Crime rates

-

Property condition

-

Historical claims data

Frequently asked questions about insurance excess

Does excess apply per claim?

Yes. An excess is applied per incident. If multiple incidents occur, more than one excess may apply.

Does choosing a higher excess always save money?

It reduces your premium, but may cost more overall if you claim frequently.

What is the highest excess available?

The highest available excess for landlord and owner-occupied properties is currently $2,000.

Should landlords choose a higher excess?

Some landlords with multiple properties prefer higher excesses to reduce premiums, but this depends on financial flexibility.

Making a confident decision

Insurance excess is about balance. It is not about choosing the lowest premium or the lowest out-of-pocket cost. It is about selecting an amount that matches your financial comfort level and long-term strategy.

Understanding how excess works allows you to make a clear, informed decision rather than guessing.

You might also be interested in:

How digital insurance makes things easier for customers

Digital only matters when it makes things easier at the moments that count.

You’ll often hear us described as a fully digital insurance provider. That’s true. But what does being digital actually mean for the people who insure with us?

For us, digital isn’t about removing people from the process. Removing the friction that gets in the way of something that should be simple is what it’s about.

Because our systems do the heavy lifting. Our support and claims teams avoid manual paperwork. They don’t have to re-enter details. They also don’t have to chase forms. Claims don’t need to be lodged through multiple phone calls. You don’t need to stitch insurance policies together by hand.

That time shifts to what truly matters when you feel overwhelmed, under pressure, or just want a clear answer.

It means we pick up the phone when you call or respond to you online in an instant.

Technology that gives time back to people

We use technology to make things faster and clearer. Things like online quotes, a customer dashboard, and a chatbot that can answer common questions at any time of day.

But here’s the key part: if our chatbot can’t give you the answer you need, it doesn’t trap you in a loop. It puts you through to a real person, straight away.

Digital tools should never be a barrier. They should be a shortcut.

That’s why we design everything we build on the technical side to give our team more time to help, not less.

People first, always

Have a look at our reviews, and you’ll see a common theme. People talk about being able to get hold of someone. About feeling listened to. About their insurance claims being handled with care.

Insurance claims can be stressful for customers, and sometimes emotions run high; not every situation is simple. But when things are stressful, the last thing you need is to be playing phone tag with your insurance provider.

Digital insurance on its own isn’t enough. Digital only works if it makes human support easier to access when you need it most.

Why this matters when things go wrong

I saw this first-hand over Christmas when a family member was involved in a car accident. Thankfully, no one was seriously hurt.

In the middle of it all there were police, ambulances, fire trucks, people from the other vehicles, and broken glass mixed with Christmas pavlova scattered throughout the car, alongside tow trucks that needed organising. It was already stressful. Trying to get hold of someone, anyone, about the insurance only made it worse.

We couldn’t find details about their insurance policy details online, and their login didn’t show anything useful. There was no clear next step, just waiting and uncertainty at a time when answers mattered.

All I could think was how different this would have been if they’d been with initio. A claim could have been lodged immediately online; the system would have provided clear instructions on what to do next and what to expect from your insurance provider. All policy details and cover information would have been sitting there in one place.

Simple, transparent, and there when it counts

That’s one of the things we’re most proud of. With initio, your insurance policy, documentation, and details are available online through your dashboard. No digging through emails. No wondering what you’re covered for. No guessing who to call.

Insurance is stressful enough without added complexity.

Being a digital insurance provider isn’t about doing less for our customers. It’s about doing better. Using technology to remove the noise, so when you really need us, we’re available, responsive, and human.

Because at the end of the day, we’re not just digital. We’re people first.

You might also be interested in:

Written by Megan Fisher, Head of Marketing at initio.

Megan has been with initio since 2022 and has over 20 years’ experience in marketing and product strategy. She works closely with initio’s claims and customer experience teams, giving her a first-hand view of how insurance works when customers need it most.

Covid-19 Response

Life Direct

movinghub

Affiliated Waikato

Wayne Grayson

Real online insurance with initio. Don’t be tricked by others

Don’t fall for insurers making you think that you can buy their insurance online.

Many of them advertise [and have google results] for online insurance, buy rental insurance online etc. A customer is lead to believe that he/she can get insurance online but is usually presented with the following:

“One of our insurance consultants will be in touch to provide you with a rental house insurance quote….”

“Online house insurance… Please fill in your details below…Please select what time you would like to be contacted”. – the worst thing about this is that you have to give them your details before you even get a price (initio doesn’t ask you for your details until you want the insurance)

“Call … now on 0800… for a quote”

Talking to someone on the phone completed insurance documentation by mail defeats the whole purpose of being online.

The process of talking to someone on the phone and filling in physical forms is inefficient and likely costs you more in premium. Stick to the real online providers – Initio Insurance.

Rest assured that you CAN actually purchase AND manage your insurance online with initio.

Compare Landlord Insurance Policies

One insurer = One headache

While it might be tempting to find the cheapest insurance for each of your insurance policies, it may not be worth it in the long run. Auckland Anniversary Weekend flooding followed by Cyclone Gabrielle in 2023 showed us the worst-case scenario; some families lost everything and are still struggling to navigate their way through the aftermath. Having multiple insurance providers can make it tough to claim. If your home, contents, and car are all insured with different providers, that’s three claims to lodge, three claims handlers to follow up, and three call centres to wait on hold with. While you may have saved $10 or even $100, the cost of your sanity is worth so much more.

It’s not worth the hassle, so why not put down the panadol and consider getting comprehensive coverage for everything with one provider?

Streamlined Claims Process

If you accidentally crash your own car into your own house and knock the TV off the wall, dealing with multiple insurers can be a hassle. It could take a lot of time and effort to make individual claims for each item. By having all your insurance with one provider, you can claim against all affected policies at once (and potentially pay only one excess*). Consider a provider with online claim submission to save time and avoid phone calls to call centres.

How Quickly are Claims Processed?

When it comes time to make a claim, is your insurer easy to deal with? Or do they give their customers the run-around? Some of the giants in the insurance industry can make their customers jump through hoops when it comes to paying out claims. Look for a provider who has a reputation for paying claims, and see if they offer any real-life reviews from customers who have claimed.

Everything in One Place

With all your policies in one place, it’s easier to find important information when you need it. When stress levels are high, because something has happened to your property, you’ll be relieved that all your important insurance information is easy to find. If your insurer still sends you documentation via the mail, keep your documents safe by scanning or taking photos and storing them in the cloud, so you can still access them if your home is destroyed by fire or flood. Better yet, choose an insurer with an online dashboard for even easier access.

What do you actually need?

Think about what kind of coverage suits your needs and do your research. It may be tempting to go with a policy suggested by your bank or mortgage broker – these plans are marketed to you as a way to save time and have everything in one place. But there’s a chance you might end up paying above-market rates and you could miss out on benefits available with other insurance policies. It might be easier to hand the reins over to someone else to sort it for you, but it really pays to look around and compare your options.

How do the policies stack up?

While on the subject of policies, does the cheapest policy give you the same amount of cover as one that costs a little more? You could spend hours trawling through the different insurance websites and looking up their individual policies. Or, save your time (and possibly sanity) by using the comparison tool created by initio. There are two versions available; house for those who own and live in their own property and landlord for those with rentals.

What are the reviews like?

Choosing an insurance provider with a great reputation might just be worth more to you in terms of time and stress levels – as opposed to saving a few dollars each month. After all, cheaper definitely doesn’t always mean better.

Isn’t it Risky To Have All Your Insurance Eggs in One Basket?

What if for some reason your insurance provider goes under and couldn’t afford to pay? The reality is that most people will be insured across multiple IAG platforms.

IAG, the oldest and largest general insurer in New Zealand, underwrites multiple insurance platforms including initio, NZI, State, and AMI. In fact, at the request of the government, IAG acquired AMI after it faced financial difficulties due to the Christchurch earthquakes. Many people in New Zealand hold insurance policies across various IAG platforms, but this does not necessarily spread the risk, as they are all underwritten by the same provider.

Your direct insurance provider would not fail due to an excessive number of claims, as it is not the end insurer. Insurance companies typically have reinsurance in place to manage large losses and catastrophe claims, as part of their risk management strategy.

In Summary

Bundling multiple insurance policies with the same insurer can save you money, make managing your coverage easier, and streamline the claims process. Consider reviewing your insurance portfolio and see if bundling makes sense for you.

A final point to remember, when one business is handling all of your insurance policies, that’s less time you’ll spend sorting through and paying each policy. And as they say: Time is money.

*Under specific circumstances (in this example, it would be the highest excess for the property affected)

UBT Protect

properli

New Zealand Pathfinder

Member Advantage

Should you rely on the Airbnb Host Guarantee?

Many hosts rely on Airbnb’s well-advertised $1USD million of free Host Guarantee cover. But be warned, this can lull you into a false sense of security leaving many disappointed when they make a claim but find they don’t tick the boxes.

The rules are specific, which can make it hard to claim especially when innocent hosts unknowingly violate the conditions.

What does it cover?

The Airbnb Host Guarantee isn’t a formal insurance policy, but rather a strongly-worded promise to rectify guest damage providing your situation meets certain conditions.

It isn’t regulated by the New Zealand Financial Markets Authority, so you would struggle to take them to court locally if things really turn sour.

Last Resort for Recovery

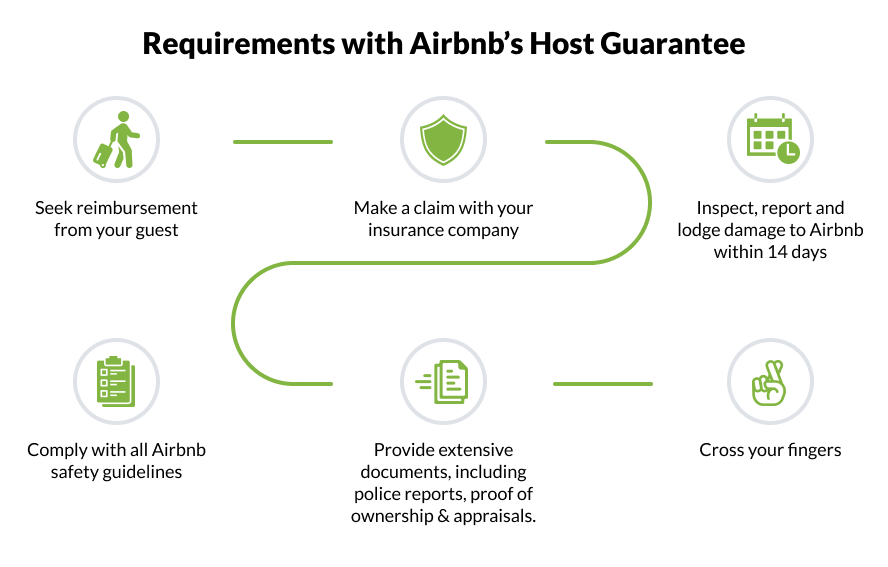

In Airbnb’s own words they say the Host Guarantee is not an insurance policy, and shouldn’t be considered a replacement.

Firstly, the guarantee can only be claimed on after trying to recover compensation from the guest, and then your own insurance (if you have this). Already the Host Guarantee is a last resort.

For a chance of recovery from the guarantee, you’re going to have to prove you persistently chased up that festival-goer to get $800 back for a living room wall repair.

There are many examples of people angry about their payout from the guarantee. Usually it’s because they aren’t aware of the conditions.

A main stump is that damage needs to be inspected, reported and lodged to Airbnb within 14 days, or else you’re out of luck.

By the time you’ve checked in your next guest it could already be too late. This could be enough to kill any claim through the Guarantee if you live away from your Airbnb.

Remember that you need to seek recover from the guest, and then your insurance before you lodge a claim in the 14 day window. The requirements almost seem like a trap to get you to exceed the strict 14-day deadline.

Watch out for Exclusions

- Only damage that happens during the booking period is covered. If an unwelcome guest overstays their welcome and causes damage, there won’t be cover.

- Cover only applies to part of the house that’s in your listing. If you rent a room, but your guest uses another bathroom and causes damage, you’ll need to foot the plumber’s bill yourself.

- It’s full of various exclusions; like damage from excessive water utility use (a sink overflow won’t be covered), and any damage by animals or pets (are you sure your guests won’t bring their dog?).

- Be prepared for stacks of bureaucracy when you make a claim. Airbnb require extensive police reports, proof of ownership and request form documents for damage.

The list of exclusions goes on. To read the full terms, conditions and exclusions see here.

No Liability Insurance

Finally, the Host Guarantee doesn’t help when it comes to legal liability. If your guest suffers an injury and they sue you, the Host Guarantee will fall seriously short.

The idea of someone stubbing their toe on the coffee table and suing might seem ridiculous, but legal liability also extends to things like sickness (if an illness is caused by the condition of your house) or freak accidents.

Is it worth the Risk?

One-in-seven Kiwi Airbnb hosts report damage. That’s about a 15% chance you’ll suffer damage one-day.

While most reports are minor and hosts voluntarily pay to avoid the lengthy resolution process, we’ve heard some shocking stories ranging from vomit-covered walls to 100-person guest parties.

Hosts should ask themselves if relying on the Guarantee is worth the risk? After all, Airbnb themselves recommend having robust insurance in place in the first instance.

Learn more today about our specialist short-term guest cover.

Initio Insurance are the pioneers of online house insurance in New Zealand, with cover specifically designed for own homes and holiday homes also rented on Airbnb.

Related articles:

Switching Payment Frequency

You can change how you pay for your policy. There are two key timings to be aware of when making a change:

- At renewal (your annual anniversary) – the change can be done as part of the renewal transaction.

- Mid-term (during the insurance year) – a new policy is required.

You should also check current premium rates before taking out a new policy. These may have changed since your last rates were set. You can check current premium rates at any time by using the quote options from your dashboard (home insurance + or car insurance +).

Changing from monthly to annual

If you want to change from monthly to annual payments at anytime, you will need to set up a new annual policy. Here’s how:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “Pay annually” option.

- Complete the application form and make the annual payment.

- Once the new annual policy is active, cancel your original monthly policy. Any unused portion of premium will then be automatically calculated and refunded.

Unfortunately, due to the different payment technologies used for monthly and annual payments, we’re unable to simply change an existing policy mid-term.

Changing from annual to monthly

What if I want to switch from annual to monthly payments?

How to achieve this depends upon the timing of your insurance year;

At your annual renewal

If your home policy is due for renewal, you can switch from annual to monthly by selecting the “Pay monthly” option during the renewal process from your customer account/dashboard.

Mid-term (during the insurance year)

If you want to change to monthly payments before or after your renewal date, you’ll need to set up a new monthly policy:

- Log in to your dashboard.

- Create a new quote using the ‘+’ options available. The new policy will be subject to the rates in place on the day you change. You may therefore, wish to check the pricing options before deciding to change.

- Customise the quote as required.

- Select the “pay monthly” option.

- Complete the application form and make the first monthly payment. The subsequent monthly payments will fall on the same day of the month that you start this policy from.

- Once the new monthly policy is active, cancel your original annual policy. Any unused portion of premium will then be automatically calculated and refunded.

Payment Options

Can I pay monthly by bank transfer or direct debit?

No, Monthly payments require a valid credit card or visa debit card and cannot be paid for by any other means.

Can I pay fortnightly, weekly or quarterly?

No, we only offer monthly or annual payment frequencies. We do not have alternatives available.

Remember, it’s always important to review your options carefully to make sure you’re selecting the best one for your needs.

Useful links: