Holiday home insurance is good but risk management is even better

Identifying and eliminating risks in your holiday home is important for the ongoing enjoyment of your property. As Initio insurance handles a large number of holiday home claims, it has identified the top 3 causes of loss in holiday homes. Initio also has some great advice to stop these things happening in the first place.

#1 Water Damage:

The number one cause of loss in holiday homes for Initio is water damage. In many cases leaking or burst pipes cause significant damage while properties are unattended. The damage is only discovered when holiday makers arrive at the property to start relaxing, and are instead faced with the smell of rotting carpets.

Risk management includes prevention of loss or damage and general up keep of your property, Initio’s top tips for counteracting loss include:

Turn off the water at the mains whenever tenants and family leave the property for more than a week

Clean guttering and keep it clear

Respond immediately to any concerns that tenants or visitors may have about the property’s condition

Visit the property at least every 6 months to check for any signs of damage or run down structures, and arrange repairs.

# 2 Storm Damage:

Another common cause of water damage is from storms and flooding. While no one can prevent such events we can try to minimise the damage caused by them.

Secure any outside structures, such as trampolines and children’s play structures.

Take down umbrellas and move outdoor furniture inside when you leave – anything not nailed down can fly and cause serious damage in a storm.

Keep trees trimmed and remove any overhanging branches. This will help to keep the gutters clear and prevent branches breaking off and damaging your home.

#3 Burglary / Break-in

Holiday Homes are often vacant and are an easy target for opportunistic thieves. There are steps that you can take to prevent having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy. Here are some tips to prevent opportunistic burglars from targeting and gaining access to your property.

Check window joinery and replace or repair any loose latches.

Consider installing security stays on windows.

Fit deadlocks / deadbolts to all external doors; especially older doors and ranch sliders which can be easier to obtain access.

Install a burglar alarm and advertise the presence of an alarm.

Install exterior sensor lights, or check that existing lights are working correctly

Don’t advertise when you are away; keep the lawns mowed and the mail box clear.

Develop friendships with neighbours and keep an eye on each others properties.

In addition, Initio recommends the following general things to reduce risk.

Test smoke alarms to make sure they are operational, and free of dust and cobwebs.

Unplug your television, oven and other appliances to protect them from power surges

Insurance is there when you need it but if you can avoid a claim in the first place you will still be better off.

For any new tenancy agreement signed after 01 July 2021 your property will legally have to comply with all five Healthy Homes Standards within the first 90 days.

To keep on top of things here’s a reminder of what the changes mean, and what’s required.

The changes

Any new or renewed tenancy (whether it’s fixed term or periodic) in effect after 01 July 2021 has just 90 days to be fully compliant with Healthy Homes. For example, if new tenants move in on 01 July, you’ll have until 01 October to make the necessary changes.

Does your rental meet the five standards?

Heating Standard

At least one built-in heater capable of heating the main living room to 18°C or more.

Some types of heaters that are unhealthy, too energy inefficient or unaffordable to run won’t meet the requirements.

Insulation Standard

Meet minimum requirements for insulation levels in ceilings and under-floors. Levels required depend on what part of the country the property is in (zone 1, 2 or 3).

Insulation installed before 01 July 2016 acceptable under 2008 standards, and

Insulation installed after 01 July 2016 acceptable under current, post 2016 thickness levels.

Learn more about the different levels for the three zones here.

Ventilation Standard

An extractor fan that vents to the outside (not another room), in all kitchens & bathrooms. They also need to meet some performance and size levels.

Open-able ventilation (like windows) to the outside in all liveable parts of the house. Size of windows is more than 5% compared to the size of the room they are in.

Drainage and Moisture Standard

Able to manage and drain normal rainfall levels. This includes working gutters, downpipes and drains for water flow.

Houses with a closed off sub-floor (area beneath flooring) need a barricade to stop water flowing in, where feasible.

Draught Standard (air-type)

Air tight with no gaps that cause noticeable airflow into the house.

Unused fireplaces are airtight, unless there’s an agreement with tenants otherwise.

What’s the penalty?

If you haven’t already, now is a great time to make a start. If you don’t comply and there’s tenants living in the property, you’re at risk of getting a penalty of up to $4,000 (per property). Anyone can claim a breach, including your tenants. If you haven’t already, the time’s now to make the changes to avoid future problems with your tenants.

Please Note: This is simply a summary of the five standards. To get the full details and piece of mind, we recommend going to the official Tenancy Services’ Guide.

A self-contained dwelling must have facilities to cook, sleep, live, wash, and use the toilet.

These facilities do not have to be in one building, but they must be for the exclusive use of that home.

Shared facilities usually mean the property is not self-contained.

Most home or landlord policies cover one self-contained dwelling only.

If your property has more than one self-contained living area, you may need separate policies.

Is your property considered self-contained?

To be self-contained a premises must contain the facilities necessary for day-to-day living on an indefinite basis. There must be somewhere:

• to cook;

• to sleep;

• to live;

• to wash; and

• to carry out ablutions.

The facilities needed to live in a self-contained manner do not have to be in one building, but must be for the exclusive use of the dwelling.

For example, a property may have an external ablutions building in the grounds. As the whole property has the facilities to enable the people using the house to live in a self-contained manner, and the facilities are not shared with other homes, this property will be self-contained for NHC (Formally EQC) cover purposes. NHC is the Natural Hazards Commission.

How this affects your insurance cover

A typical home or landlord policy is designed to cover one self-contained unit being used as a dwelling either by the owner or a long term tenant (over 90 days). If you have a second self contained area at the property also used as a home, you may need a second policy, please check out our support page here to assist with determining the correct cover for you.

The main driver’s age and loss history is a major factor in calculating your car insurance premium.

When you get a quote from us we ask about the number of claims you’ve had in the last five years, where you or the owner paid the excess.

Each anniversary, when your policy renews, the initio system checks to see what additional initio claims the Main Driver has had during the year. The system also checks to see if historical claims have fallen outside of the five year period.

We call this ‘Driver Grade’. Other providers have a similar system referred to as “No Claims Bonus”.

How does Driver Grade work?

When the policy is first started we take the claims from the main driver’s previous 5 year period. This number determines the driver grade, and has a bearing on the car insurance premium.

When the policy anniversary comes around we re-calculate the driver grade by checking if some of those historical claims have fallen outside the 5 year period, and checking to see if the main driver has incurred any initio at fault claims during the past year.

The number of ‘at fault’ claims in the previous 5 year period determines the driver grade.

Had no claims? Your driver grade is zero and you’ll be at our lowest driver grade premium without any loading.

If you’ve had a claim, the grade increases to one which slightly increases the premium.

Each additional at fault claim increases the driver grade and premium. If you’ve had 3 at fault claims your driver grade is 3, and premium will be significantly higher than a vehicle that has a main driver with no claims.

We don’t count at fault accidents that are more than five years ago. A crash 10 years ago won’t affect the premium you pay today. We also don’t count claims where the main driver was not at fault. But know that the main driver can still be considered ‘at fault’ even if it wasn’t directly their fault (e.g the vehicle was vandalised).

What if I wasn’t at fault, but I paid an excess?

When starting cover with us we ask you to disclose claims where you paid the excess. This is the best way to determine what claims are not recoverable by your insurer (ie where another party cannot be made responsible).

We realise that you could have a claim go towards your driver grade that wasn’t really your fault (like your car being vandalised), but this is still considered at fault as we (or your insurer at the time) is not able to hold another party responsible for the damage.

Think of it as a user-pays system where those that claim more (with no ability to hold someone else responsible for the cost) pay a bit more into the claims pot.

Regular meth testing isn’t a condition you have to meet, but we do recommend it.

We cover up to $30,000 for meth cleaning under our landlord cover. You won’t need to test between tenancies to have meth cleaning cover, but regular tests can come in handy when you want to know when it occurred, or who was responsible.

If you suspect there’s meth contamination at your property and then get a positive test, we cover the test and cleaning costs. You won’t need to show us a full record of past meth tests.

We do however strongly recommend testing in these instances.

When new tenants are moving in

Testing the house in between a new tenancy is a good way to avoid future hearings at the tenancy tribunal. It will help you recognise which tenants caused contamination if you have a positive reading.

When you purchase a property

Real estate agents only have to tell buyers if a property has contamination reading over 15 μg. However, your insurer might not provide cover if the result is over 1.5 μg. You also cannot tenant a property that exceeds 1.5 μg.

A simple meth test before purchasing could save you thousands in future cleaning costs. If you haven’t already, simply ask the agent if the house has any contamination.

If you suspect drug use or manufacture

If you see signs of drug use or manufacture; or if the police have drug raided the property, it’s a good sign to get it tested. Letting a house become contaminated could effect your ability to sell or rent it in the future.

Unlawful Substances Liability Cover

There’s a small section of our cover where testing is required. The Unlawful Substances liability section covers you for losses from controlled drugs you cause to other people (or their things) in relation to your ownership of the house.

An example could be where a past tenant contaminated your rental with meth. A new tenant could then live in the contaminated property and hold you liable for the contamination damage to their belongings. For us to provide liability protection, you’ll need to test before and after each tenancy.

For full details, see page 18 of our policy wording here.

Had a positive meth test at your property?

If you’ve detected meth that you think will be over 1.5 μg, you can make a claim by logging in to your dashboard.

If you have done a meth test at your property that has showed a positive reading, you can make a claim from your initio dashboard log in. For more info on making a meth claim, see our guide here.

Recreational Features are defined as any tennis court or permanently fixed swimming pool or permanently fixed spa pool including its ancillary equipment and pump(s).

Recreational features are automatically covered by the policy, but are limited to $45,000 for all recreational features.

So in the following scenario, unless you noted the recreational features on your policy, the cover would be limited to $45,000.

Recreational Feature

Replacement Value

Swimming Pool

$30,000

Spa Pool

$10,000

Tennis Court

$20,000

Total Recreational Features

$60,000

Recreational Features can be added to your policy by sending the details to [email protected].

Retaining Walls

A retaining wall is a structure that holds land in place to prevent the earth sliding or eroding away. A retaining wall differs from a garden wall, as a garden wall is purely aesthetic and serves no purpose in protecting the structure of the land.

Retaining Walls are automatically covered by the policy with a limit of $25,000 for all retaining walls.

EQC provide cover (with no dollar cap) for retaining walls and their support systems that are necessary for the support or protection of the house or insured land (including the main access way) if they are within 60 metres of the house. For EQC claims involving damage to retaining walls, the settlement will be calculated on the basis of either the cost of repair, or the ‘indemnity value’. The indemnity value of damaged property takes into account the age and condition of the damaged structure and will likely be lower, than its replacement value.

The initio policy pays for damage to retaining walls by earthquake, volcanic eruption, hydrothermal activity tsunami and landslip as a ‘top up’ cover. This means that EQC will pay out the indemnity value of the damaged retaining wall and that initio covers the additional cost, up to the replacement value, limited to the specified value or $25,000 if no value has been specified.

To increase the cover for retaining walls we will need to be provided with the following information about the Retaining Wall(s)

Location

Height

Length

Age

Construction Type

Current Condition

Replacement Value

Details of previous losses and /or claims

If there is shared ownership, if so, what is the ownership structure (ie cross-lease, easement)

Confirmation that code of compliance and/or council consents have been obtained where required.

Please send the above details alongs with a photo, and where relevant a copy of the plans, or engineers report to [email protected].

This is not an exhaustive list of the changes to the policy but rather a high level summary. For full details of cover, benefits, conditions, and exclusions please see the policy document Initio landlord and holiday home policy NZ1811

Delving a bit deeper into getting your essentials in order, let’s look at why checking your sum insured is a crucial step. Understanding the value of your property is key. In tough times, the idea of lowering your sum insured to reduce your premium might seem appealing. However, this could lead to ‘under-insurance,’ a risky strategy that could backfire if significant damage occurs. Insurance is there to put you back in the position you were in before any mishaps, and cutting corners on your sum insured might leave you short when you need support the most.

Adjusting your sum insured often has less impact on your premium than you might think. Properly insuring your house to fully cover potential rebuilding costs might cost a bit more upfront, but it’s a move that can save you from significant financial headaches down the line. It’s not just a safety measure; it’s a wise financial decision. We recommend taking the time to consider the true value of your property and choosing a sum insured that ensures you’re fully protected. It’s all about finding that sweet spot to keep you covered without overdoing it.

Get started by logging in to your initio dash to check what cover you currently have for your property

There’s broken glass cover under all our house policies. Vehicle glass damage can also be covered on your car. The excess that applies depends on the policy that’s in place. Please refer to the product types below for which excess applies to your situation.

Home Insurance – Owner Occupied/Usual Residence (Own Home policy)

Our “Own Home” home insurance cover for owner-occupied homes has a lower “breakage” excess of $250 for glass in windows, doors and screens. This replaces the standard excess you choose on the policy. This special breakage excess applies for accidental breakage of other items, too!

✅$250 breakage excess applies: Sinks, baths, toilet bowls, shower cabinets, bidets, fixed glass lampshades, permanent mirrors, glass in built in cabinetry.

All claims need to lodged through your dashboard login. You can make a claim by selecting the Make a Claim option on the right-side menu on the policy.

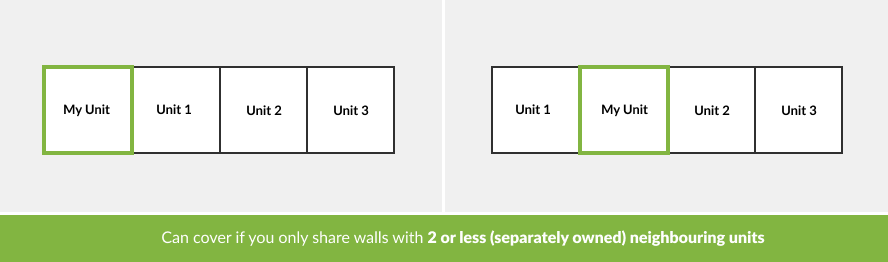

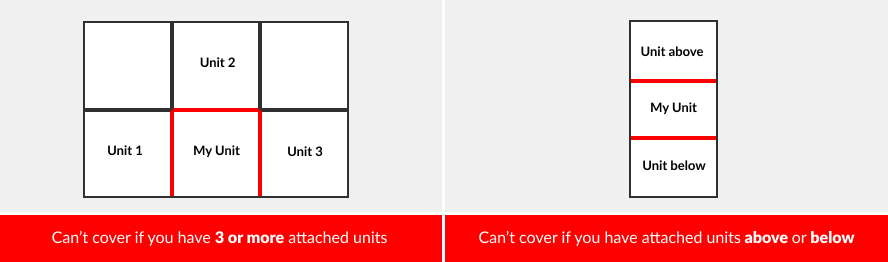

Our house insurance isn’t set up to cover units that have another unit above or below yours (stacked). It can get very complicated if you make a claim for damage that involves multiple other unit owners and insurance companies.

We can only offer insurance for a unit that –

Does not share walls with more than two (separately owned) neighbouring units on any side. So if your property is one in a row of townhouses with no neighbouring units connecting behind or above yours, then we can provide cover.

Has no other (separately owned) neighbouring unit above or below your unit, ie another unit or unit’s garage/carport stacked above or below yours.

Does not share other building structure(s) with other units, eg common hallway.

Is not part of or belongs to a Body Corporate.

Part of a Body Corporate?

We can’t provide cover on any unit or dwelling that’s owned under a Body Corporate, as it’s the Body Corporate’s responsibility to insure the building, not the individual unit owners.

Our comprehensive personal contents protection under our own home policy is generally based on new-for-old cover. There are however a few items that are covered for their current value, where your payout will be based on the item’s present (or market) value. These are listed below. Please note that other criteria/limits apply – refer to your policy wording for full information.

Market Value Replacement Items:

Books

Clothing & Footwear

Media, Software, Programs and Digital Data

Camping and Sports Equipment

Boating Accessories (not whilst attached to the boat, other limits also apply)

Remote Airplanes, and Accessories

Household Linen

Computers, Laptops over 5 years old

Camping Equipment

Watercraft, Watersport Equipment, and Accessories

Remotely Piloted Aircraft, over 2 years old, and Parts and Accessories

Sports Equipment, not including Golf Equipment

Bicycle, E-Bikes

The items listed above are contents that will be replaced for its present value.

Don’t worry, all your other belongings that aren’t listed above will be covered on a new-for-old basis.

Can I specify any of the above items so that they are covered for more than their market (present) value? No, we are unable to alter your cover outside of these terms.

Initio is an online insurance underwriting agency, which is underwritten by IAG (AA financial strength rating).

Being 100% online means all payments, changes and cancellations are done instantly on the website, at a time that works for you.

We are property insurance experts, who specialise in landlord cover. We also offer a full range of cover across house and contents, holiday home and car insurances.

Using technology to make purchasing insurance easier means that there are no wait times when you need to speak to a customer service team member. Our state of the art customer dashboard allows policies to be fully managed online, putting our customers in the driver’s seat.

The customer dashboard allows customers to add or cancel policies, manage billing and review updates on claims. Submitting claims is also made easy through the dashboard, which guides you through the information that’s needed. Once submitted, a dedicated initio claim manager handholds the claim through the process from start to finish.

Online isn’t for everyone, but we believe it’s the only way to offer great cover, great service, at a fair price. Just ask any of the thousands of initio customers!

Despite tighter laws and more public awareness, methamphetamine remains a serious problem in New Zealand. Not just for law enforcement and health agencies, but for landlords, property managers and homeowners too.

Meth in Aotearoa: the facts

New Zealanders are consuming 27.5 kilograms every week, based on nationwide wastewater testing at the end of 2024, an increase of 96% from records in 2023.

That equates to an estimated $28 million in social harm every single week.

We remain in the top four countries globally for meth use per capita:

Australia

United States

Czech Republic

New Zealand

These aren’t just distant statistics. For property owners, meth contamination can mean costly clean-ups, extended vacancies, and insurance stress.

Recent events underscore the ongoing issue. In April 2025, Customs officers seized an estimated 90.7 kilograms of methamphetamine in two separate incidents at Auckland International Airport. These seizures prevented an estimated NZ$95 million in potential harm and cost to New Zealand.

Meth is usually smoked inside, which leaves behind chemical residue. This residue can settle on walls, ceilings, carpet, and furnishings. If contamination levels are high enough, the home may be considered unsafe to live in until it has been professionally decontaminated.

How does insurance handle these claims?

With initio, meth claims are covered under our Landlord / Holiday Home policies:

Cover is up to $30,000, with a $2,500 excess.

From 2023 to now:

The average claim we’ve settled is $24,800

Just under 20% of those claims hit the $30,000 limit

The average duration of a claim is 120 days

Typical cost breakdown

A meth claim isn’t just about one thing. Even minor contamination can lead to significant costs. The $24,800 average usually covers:

Remediation (replacement of contaminated soft furnishings such as carpet and curtains etc)

Loss of rent

So, does NZ still have a meth problem?

Yes. While it might not make headlines as often, the data paints a clear picture. For landlords, it’s still a risk worth understanding – and preparing for.

New Zealand’s Leading Insurer Urges Government Action on Flood Resilience

New Zealand’s most prominent insurance provider, IAG, has called on the newly formed government to make flood resilience a top priority. This appeal comes in the wake of insurance claims exceeding $1 billion due to the summer storms, including the North Island floods and Cyclone Gabrielle. These figures are second only to the costs incurred by the Christchurch earthquakes.

IAG (initio is backed by this insurance giant), have shared insights from their latest Wild Weather Tracker. This report discloses the settlement of a staggering 51,000 claims related to these weather events. The data reflects high settlement rates across various categories including motor, contents, and home insurance.

The Wild Weather Tracker also sheds light on the rising economic impact of climate change, noting an upward trend in average claim costs. Regions like Hawke’s Bay, the West Coast, and Gisborne Tairāwhiti have emerged as the most affected in terms of weather-related claim costs.

For a detailed view of the November 2023 Wild Weather Tracker, visit IAG’s website.

Burglary prevention is as equally important for holiday homeowners and landlords, as it is for one’s own personal residence. Burglary is not just about having your contents stolen; there is also the damage that thieves can cause trying to gain access to the property.

Holiday homes are particularly vulnerable as they are often left unoccupied for extended periods of time.

Landlord Insurance cover is designed to protect you when the worst happens, but as a landlord and property owner there steps that you can take to prevent having to deal with the heartache and distress of someone illegally entering your property, and ultimately having to make a claim on your policy. Here are some tips to prevent opportunistic burglars from targeting and gaining access to your property.

Check window joinery and replace or repair any loose latches.

Consider installing security stays on windows.

Fit deadlocks / deadbolts to all external doors; especially older doors and ranch sliders which can be easier to obtain access.

Install a burglar alarm and advertise the presence of an alarm.

Install exterior sensor lights, or check that existing lights are working correctly

Don’t advertise that you are away; keep the lawns mowed and the mail box clear.

Good security makes people feel safe; it also has the added benefit of retaining good and long term tenants.

There needs to be an inspection done every three months and in between tenancies to meet our landlord obligations under our landlord insurance policy. This can be done yourself or by the person who manages your tenancy (e.g. property manager). The inspection will need to confirm the interior and exterior condition of the property and you need to keep a record of the results.

These landlord obligations and inspections only need to be met if you are making a tenancy-related claim. These include tenant damage, meth contamination and loss of rent after a tenant is evicted or leaves.

If you don’t fully complete your inspections it won’t void your policy. The cover for non-tenancy claims like floods and sudden water damage are still covered.

At initio, we require an agent or a trusted representative physically present at the property for inspections. This ensures a thorough evaluation of the property’s condition and facilitates real-time reporting, serving as your on-the-ground resource. Advantages of having an in-person representative include:

Real-time condition verification and data reporting during the inspection process.

Being your dedicated eyes and ears on the ground, diligently checking the property’s condition.

Early identification of any potential issues, damages, or repairs that could potentially be missed in a purely remote inspection.

However, we understand there may be special circumstances such as illness or lockdowns where remote inspections become necessary. These should be exceptions rather than the norm. In such cases, a trusted representative or official agent’s physical presence during the inspection is critical to maintain the assessment’s accuracy and comprehensiveness.

Looking ahead, we’re mindful of emerging technologies that could potentially streamline remote inspections. However, as of now, the value of in-person inspections is paramount. Always remember that our advice serves as a guideline, not an inflexible rule. Each property and situation may require a different approach, and decisions should be tailored to your specific circumstances and needs.

What happens if I can’t inspect my property every three months due to illness?

Initio’s landlord guidance is that you, or someone on your behalf, should carry out an internal and external inspection at least every three months, and also between tenancies. These inspections are an important part of meeting landlord obligations for tenancy-related claims, such as tenant damage, meth contamination, or loss of rent after eviction.

That said, if inspections aren’t completed exactly on time, your policy is not automatically void. Claims that aren’t tenancy-related (like fire, flood, or sudden water damage) remain covered.

For tenancy-related claims, inspections generally need to be done in person by you, a property manager, or another trusted representative. We do recognise that there may be special circumstances, like illness, where remote inspections are the only option. These should be the exception rather than the norm, and having someone physically present is always preferred to keep records accurate.

If you’re in a situation where inspections are difficult, please reach out to our team. We’ll be happy to talk through your options and help make sure you’re covered.

Further information

Please refer to the New Zealand tenancy services site for specific information around property inspections, including;

Our robust cover means it’s not the end of the world if you use your car for some business use. You’re still covered as long as it’s not being used for any of the below.

Business use that is NOT covered:

Your car will not be covered if used for the following:

Ride-sharing, or carrying fare-paying passengers such as a Taxi, or Uber.

Courier or delivery business (including food delivery such as UberEats).

In connection with a trade or servicing business that does any installation, maintenance, cleaning or repair work on homes.

To carry goods or samples for financial gain or reward, as part of any business (apart from Farming)

As part of any motor (or automotive) trade profession (such as a mechanic)

Formal driver training or education.

Towing for reward (e.g. to a tow another car)

Car being hired out (e.g. a peer to peer hire)

If your car is used for any of the activities listed above, our policy is not suitable. We would recommend purchasing commercial cover – typically available through an insurance broker or commercial insurer.

What if I don’t usually use it for the above activities but that changes later?

Your vehicle won’t be covered at any time it’s used for any of the excluded activities listed above. If you’re involved in an accident while using the vehicle for any of those purposes, your initio policy won’t respond – and the claim would be declined.

Will my cover include damage to or replacement of the car’s signwriting?

No, our policy does not include cover for any vehicle signwriting.

So, is all other business use covered?

Yes! For any business activity not listed under the exclusions above, your car can be covered – even while performing that business task.

Our policy acts as a hybrid between private and commercial cover, designed to accommodate most other business uses.

Examples of covered occupations (not exhaustive):

Office professionals visiting clients.

Property managers driving to properties for inspections or viewings.

Property Owners carrying out work on their own rentals

Farmers using a ute for on- and off-farm activities to run their operations.

Real estate agents or salespeople traveling for work.

Still unsure?

If you’re uncertain whether your business use is covered, get in touch with us – we’re here to help clarify!

Young couple Chris and Jen recently completed every young couples dream and purchased their first home. In a hot property market this is not an easy task. With house prices continuing to rise and larger deposit’s required upfront, getting your foot in the door can seem overwhelming and impossible at times. But after growing up in Zimbabwe where land ownership is fraught with controversy, nothing was going to stand in the way of Jen’s dream.

After looking for a year, Jen and local Hamilton lad, Chris found their perfect first home in the Hamilton suburb, Fairfield. Now that they have accomplished their first property milestone, initio plans to continue to support this couple as they grow their property portfolio. The couple plan to use this home as a stepping stone into something bigger before they find their dream holiday home.

Why do you insure with Initio?

Initio was recommended to us, and we were instantly impressed with the competitive pricing to insure our home and our contents. The sign-up process was quick and easy during the stressful last days of purchasing our home.

Best advise you can give to other first time home buyers?

It’s okay to miss out on the first house you make an offer on. We were lucky securing the second house we made an offer on. Which ended up being twice as good as the first. Look at as many places you can as early as possible and you will soon realise exactly what you’re after. After a while looking we knew from the which places weren’t worth looking at & what suburbs were best. Real Estate Agents websites tend to show listing first before they hit Trade Me or realestate.co.nz, so go to the likes of Lugtons first if you want to possibly get an early viewing. Check out whether you’re eligible for any grants such as the Home Start Grant. The Government is willing to help first home buyers and every little bit helps towards your deposit. A good mortgage broker will break down what you can afford and what your repayments may be. It was a stressful and long process purchasing our first home. But with the help of people like initio, once we found our home – it all happened very quick.

Baxter owned a rental property in Whangamata and employed a property manager to manage the tenancy and inspections. Baxter had model tenants, the property was always kept in good condition, the lawns mowed regularly and rent payments were never missed. Then, in March 2018 the tenant failed to pay rent for two weeks in a row. The property manager went to the house and discovered that the tenant had vacated, possibly weeks earlier and had left behind a mess of rubbish, possessions and a very dirty house, with numerous areas of damage.

Claim Process

Baxter logged into his dashboard on the Initio website to tell them about his damaged house. Because Baxter wasn’t based in Whangamata, he advised Initio that the property manager was the best person to liaise with.

Initio appointed a loss adjuster to the claim, who went to the property, took photographs and obtained quotes to repair the damage. Thankfully the property manager had completed a written and photographed inspection of the property just one month prior to discovering the damage, so the loss adjuster was easily able to differentiate between existing and new damage.

The damage to Baxter’s property was two-fold, the claimable and non-claimable.

Claimable damage:

Graffiti on walls in lounge / dining / kitchen area – It was likely that the graffiti was all completed at the same time, so one excess applied to this event.

Numerous holes in walls in the kitchen / dining / lounge area – These areas were going to be re-painted due to the graffiti, so the holes were repaired at the same time. No additional excess was applied to this event.

Large tear in the carpet in the lounge / dining / kitchen open plan area – This was one open plan room and so the carpet to the doorway of the room was covered. Another excess was applied as this was unrelated to the graffiti.

Cracked vanity top – The only way to remedy this was to replace the entire vanity, which involved re-tiling around it. A further excess was applied to this one-off event.

Loss of rent – The claimable damages would take approximately three weeks to repair, so Initio paid the lost rental income for this period. No additional excess is charged for loss of rent.

Non-claimable damage:

Rubbish removal, general cleaning, lawn mowing – Whilst there was a cost associated with these issues, they were not caused by a sudden and accidental event, so there was no cover.

Random one-off holes in walls throughout 3 bedrooms – It was not possible to confirm that the holes all occurred in the same sudden event and so an excess would have been charged per hole and therefore there was no point in claiming.

Missing and damaged curtains throughout – As confirmed by the tenancy inspections, the curtains had been removed and damaged at various times throughout the tenancy, so an excess was to apply per curtain which made them un-claimable.

Outcome

Initio deducted 3 x $400 excesses from the repair estimate of $6,500 and cash settled Baxter $5,300 directly to his nominated bank account.

“All claims are different and they are assessed on their own merits and facts. The above profiles do not imply a guaranteed approach all such claims”

Jonathan is a landlord of 12 properties in the Waikato region. Other than a few small glass claims in 20 years he had never lodged a claim. He got a call on a Saturday from a tenant who had been on a holiday for a week. While away a pipe in the bathroom had burst; water had flooded the house damaging carpets. When Jonathan arrived at the property he found the downstairs celling of his two-story property had collapse under the weight of the water pressure. Jonathan contacting a plumber who located the burst pipe and made repairs to stop the water flow.

Claim Process

Jonathan first tried to call Initio but being a weekend was able to find the after-hours emergency number. After hours services advised him to call Jae’s a carpet cleaning company. Jae’s turned up immediately and started cleaning and drying the house. Jonathan made sure he took photos of all areas where he could see that the water had affected. Monday morning he went online, logged into his dashboard and lodged his claim online. In the claim form, Jonathan provided a very detailed description of what had occurred.

The appointed loss adjuster contacted Jonathan to organise a time to inspect the property. The loss adjuster found there was a substantial amount of damage to the property that Jonathan had not been initially aware of. Both first and second levels had water damage to walls, carpets, tiles and the celling.

The damage to the property was consistent with a sudden and accidental loss, which Jonathan had declared. All costs to repair the consequential damage, including removing & replacing wall linings, replacing carpet, relaying tiles and painting were covered under Jonathan’s insurance policy.

Outcome

Jonathan was proactive getting correct advice and taking steps to minimise the damage. The policy responded exactly as he expected – the property was repaired, items were replaced, and it was restored back to the condition it was before the water damage event occurred. The cost of the claim was almost $50,000.

In the event you find yourself in a similar water damage situation to protect your property and minimise damage, call a plumber. In the first instance you need to stop the water flow and make emergency repairs. Make sure you take photos of damaged areas and contact Jae’s to arrange the cleaning and drying of your property. When you work with your insurer to provide detailed information, your claim can be serviced and completed without delays.

All claims are different, and they are assessed on their own merits and facts. The above profiles do not imply a guaranteed approached all such claims.

Insurance is full of jargon, and one piece of jargon that we use often is ‘excess’. Insurers assume that their clients know what an excess is and how it works. This article will give you a clearer understanding of excesses.

What is an Excess?

An excess is the contribution that you are required to make towards your claim. This is deducted from the loss and it is a form of self insurance. At initio you have the choice between a $400, $650, $1,150 and $2,000 excess. If you can afford to contribute more towards claims, and want cheaper premiums, you can take a higher excess. Rather than pay the excess to the insurer, the insurer will usually deduct your excess from the cash settlement or from the first repairer payment it makes. You are then responsible for settling this account directly with the repairer.

Do all losses have the same Excess?

No, not all losses have the same excess. Some policy sub-limits have higher excesses, these will be identified on your policy schedule. For example, while your nominated excess might be $400, the excess for the deliberate damage by tenants extension is $500 for each event.

What do you mean by each event?

An event is defined as an event (yes the policy defines a word with the same word!) or series of events arising from one source or original cause. Where a single claim is made up by multiple events, multiple excesses would apply.

Still confused?

Lets say a dog defecated in multiple rooms of your house. You could look at this two ways; you could say that it is multiple events because the dog relieved himself multiple times (multiple excesses would apply). Or you could say that is is a series of events arising from one source or original cause (being the dog). In this claims scenario we would consider the period of time that the damage took place. If the series of events had been happening over the period of the tenancy then multiple excesses would apply (likely an excess per room). However, if the damage took place in a very short period of time, say the dog was locked inside for a day, only one excess would apply.

To read why an excess per event needs to apply, see here.

Why do I have to pay an excess?

One reason for an excess is to eliminate the administration costs associated with minor or small claims. By making the client responsible for the first portion of a claim, small claims can be avoided. Another reason why insurers charge an excess is to try and prevent fraudulent claims. People are less likely to lodge a false claim when they are responsible for payment of an excess.

If you have any further queries regarding your excess and how it is applied, feel free to send an email with your query to [email protected].

A big decision for landlords is whether to manage their rentals themselves, or pay a property manager to do it for them.

Managing your rental yourself can be more cost effective, but sometimes it can be demanding as attending to requests, queries, and maintenance can be frustrating and time consuming.

What services do Property Managers provide?

To keep your landlord insurance valid, your property manager should meet your landlord obligations so you don’t need to worry about them yourself.

Some of the other main services of a Property Manager include:

Finding new tenants when the house is empty

Assess prospective tenants’ suitability and review reference checks

Collect rental payments from tenants

Carry out regular property inspections to ensure you comply with your insurance policy.

Deal with and look after tenants – answer queries, book tradespeople for repairs, and generally act as a go-to for tenants.

Deal with the legislative ins and outs.

Regular rent reviews

Assess and recommend improvements to your property so that you can attract higher rents and better tenants

Can I give my property manager access to my initio account?

Yes – you’ll keep full control of your initio account as the property owner, but you can add your property manager as an authorised contact to help with day‑to‑day matters. The main login must remain in your name for security and legal reasons, as it allows managing policy details and payments. If you need to make a claim, you’ll need to submit the initial online claim yourself, then you can nominate your property manager within the claim form to assist with claim handling.

Your initio account is for you, the insured property owner. The main login always stays in your name so you can manage your policy, payments, and cover.

While your property manager can’t have their own login, you can add them as an authorised contact for claims. If you need to make a claim, you’ll start the process by submitting it online yourself. After that, you can nominate your property manager in the claim form so they can help manage the claim on your behalf.

This way, you keep control of your account, but your property manager can still support you when it comes to claims.

Can a property manager lodge a claim on my behalf?

Any claim must be initially lodged by yourself as the Insured, part of the claims form includes legal declarations and statements that only you can complete. You can, however, nominate a property manager or another agent as part of the lodgement who you authorise to act on your behalf once the claim has been submitted.

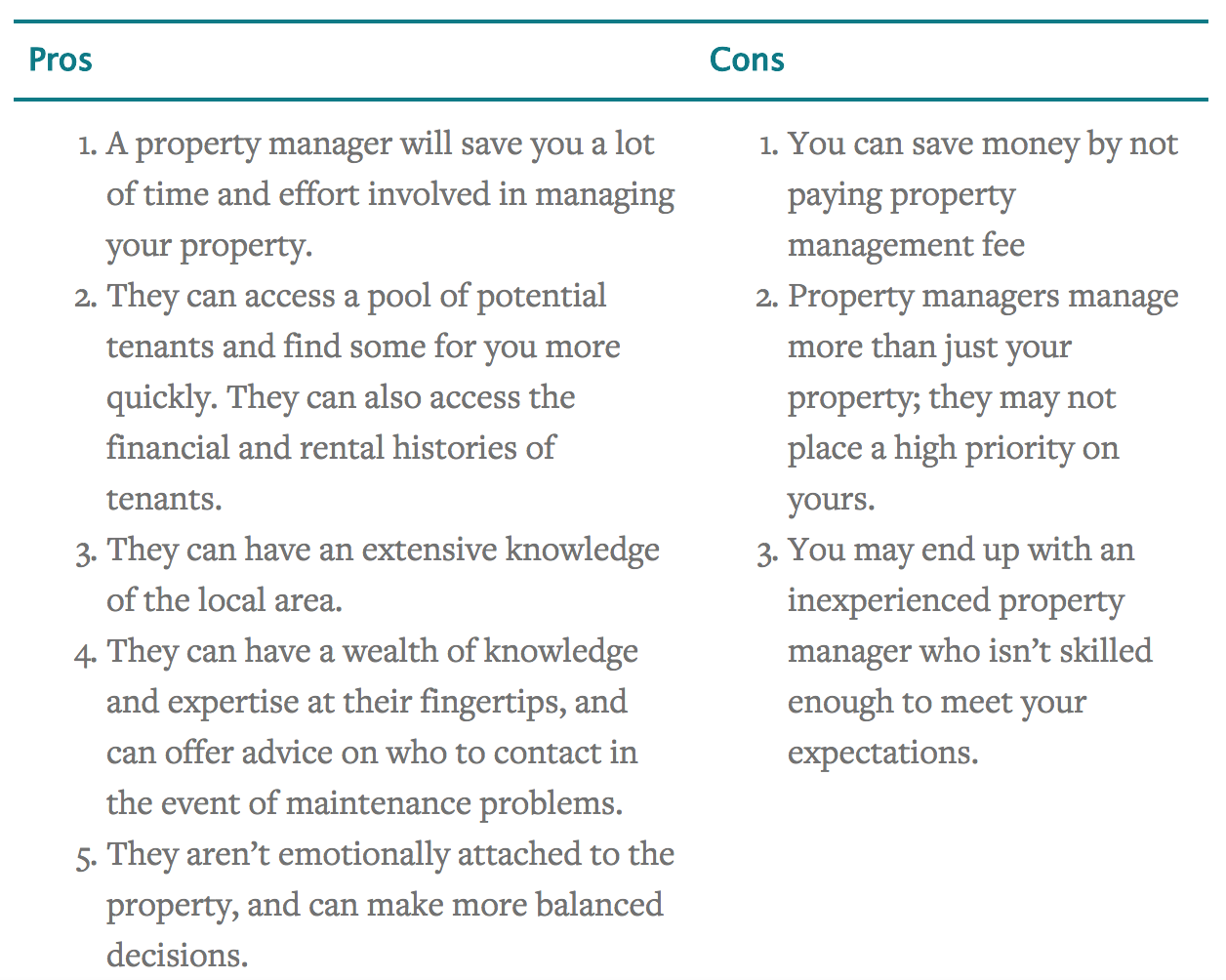

Pros and Cons of using a Property Manager

Pros and Cons of a Property Manager

While self management might save you a property management fee, having the right property manager could mean higher rents and less days unoccupied meaning more rental income.

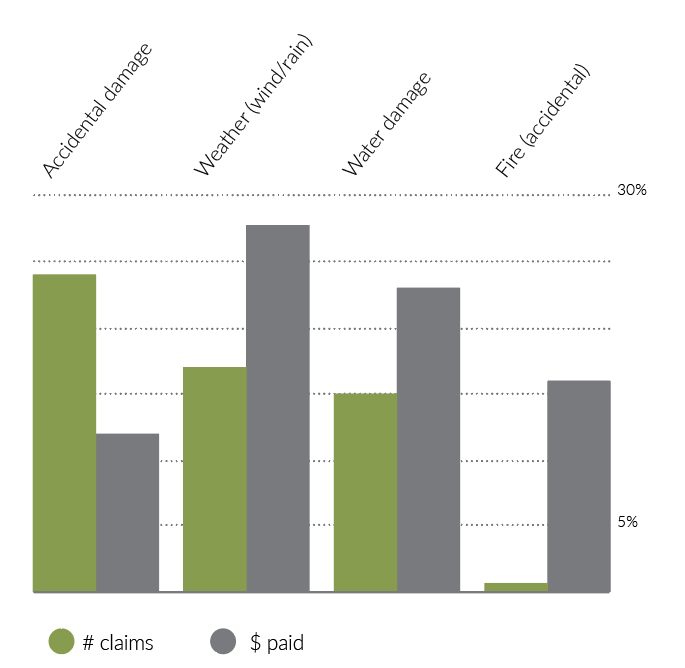

Another year has come and (nearly) gone so here’s a review of the year that was. This year, initio processed nearly 45% more claims when compared to 2021. We think you’ll agree, it’s a big increase and is indicative of both of greater rate of weather-related claims, and the significant support from kiwi homeowners (more policies, means more claims)

In relation to the house & contents claims we saw this year, accidental damage was claimed most frequently at 24% but only cost 12% of all payouts. On the flip side of this, pesky weather-related events (storms, flooding, wind, rain) were the cause of 17% of our claims but responsible for nearly 28% of our payments.

They were closely followed by various types of claims citing water damage as the cause (not including weather-related flood damage) costing 23% and (accidental) fire claims 16% of all payouts. It’s also worth noting here that less than 1% of all claims cited accidental fire as the reason. This means that while it might not be a common reason to claim insurance, it sure is costly.

Insurance is there to cover you for the unexpected, but sometimes the unexpected is also a little unusual. Our team have come up with the following claims that deviate from the usual reasons:

Dog + Robot Vacuum = Big mess

While modern technology is usually supposed to make life easier, sometimes it can go horribly wrong. This year we saw a claim involving someone looking after their parents’ dog. This person had to take a zoom meeting and during that time, the dog, unfortunately, had a code brown on a rug. This also coincided with their robot vacuum doing its rounds which tried its very best to help but ultimately made the situation much, much worse.

Both the vacuum and the rug needed to be replaced (but they kept the dog).

This year we saw 11 pet damage-related claims in total (1% of total claims). Our four-legged friends caused nearly $18,000 worth of damage this year – which doesn’t include one motor vehicle accident caused by swerving to avoid a cat. Dogs proved to be the most troublesome with the finger being pointed at them twice as often as cats.

Speaking of family members, children have also caused their fair share of damage this year. Although worth pointing out, the two-legged family members haven’t caused as much damage as pets.. We’ve only seen 6 claims involving children. These included:

Drew on lounge carpet with a marker (for two different claims)

Damaged fridge

Scratched television

Damaged walls

A toy was thrown at the TV – breaking the screen.

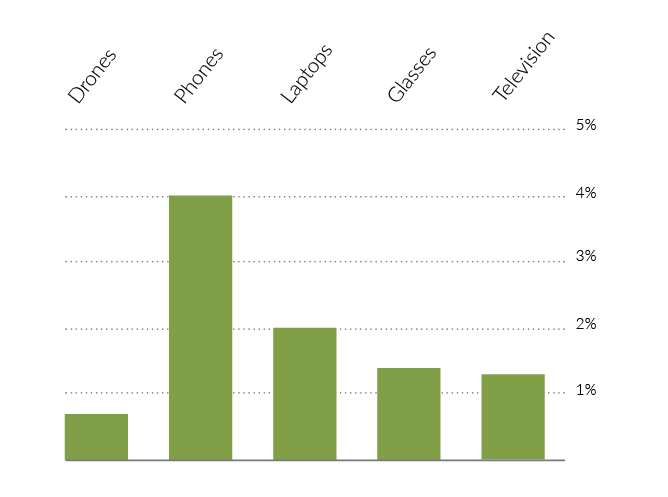

Technology has also been in the wars this year. We’ve seen 7 claims involving drones, which a couple of years ago wouldn’t have even been a blip on our radar. Phones are still the most commonly claimed gadget, but who knows what the future looks like?

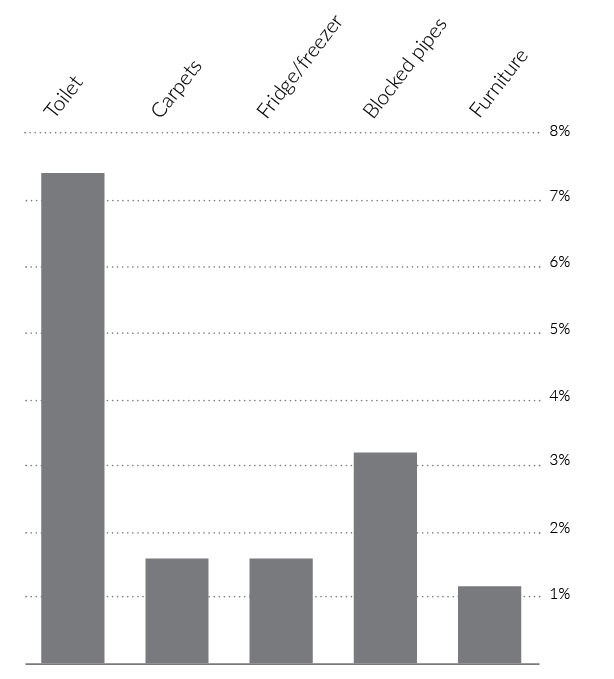

In terms of household items, toilets have been the most troublesome (including x2 phones dropped into the toilet) with blocked pipes coming in second.

We try to remove roadblocks in our claims process – there’s enough stress dealing with the event that you’re claiming for in the first place. We make an effort to alleviate some of that stress by processing claims as quickly and efficiently as possible.

Hopefully, you’ll never need to find out for yourself how good we are, but it’s nice to know we’re there for you when you need it

As a landlord, ensuring the safety of your tenants and property is paramount. Fire hazards pose a significant risk, but with the right precautions, their impact can be greatly reduced.

From an insurance viewpoint, fires accounted for approximately 1% of the total claims we processed in 2023. Although not the most frequent type of claim, their impact is significant in terms of cost, representing 26% of the total value of claims last year. Given the potential financial and personal consequences of fires, investing in preventive measures is undoubtedly worthwhile.

Below are some practical steps you can take as a landlord to minimise fire risks, safeguarding both your tenants and investment. The leading cause of fire is kitchen fires, particularly due to unattended stoves and combustible items left while cooking.

When anyone is faced with a kitchen fire, the immediate confusion and panic can result in uncertainty about how to respond effectively. This uncertainty may cause considerable damage and could even lead to hospital visits. So, the easier you can make it, the better.

All year; Kitchen fire safety

The kitchen is a common site for fires, but you can make it safer with a few measures:

Fire extinguishers: Ensure a fire extinguisher is available in the kitchen and make your tenants aware of its location and how to use it. It’s best placed within easy reach, such as in a cupboard that’s accessible or mounted on the wall close to the cooking area.

Choosing the right type of fire extinguisher: It’s worth noting that not all fire extinguishers are suitable for all types of fires – especially oil fires common in kitchens. Opt for an extinguisher with an F or B rating, designed for grease, cooking oil and fat fires, to ensure effectiveness. Learn more about fire extinguishers

Provide a fire blanket: A fire blanket is an invaluable tool for smothering fires. It’s a good idea to have one easily accessible in the kitchen, offering tenants a quick solution to douse flames before they spread.

Carbon monoxide monitors: They detect harmful gas from appliances, serving as an early warning to prevent fires. Their ability to sense invisible, odourless carbon monoxide can stop potential fires, ensuring the safety of home occupants.

It’s also important to note the impact of placing hot pots directly on wooden or laminate benchtops. Doing so can lead to significant damage, leading to costly repairs and labour. Ideally, stone or stainless steel benchtops offer greater resistance to heat, but these materials might not always be feasible in rental properties, where laminate or wooden benchtops are more common. Although not an immediate fix, considering more heat-resistant materials during renovations could mitigate future damage and maintenance costs. This foresight can enhance the longevity and appeal of your rental property’s kitchen.

Summer; Outdoor cooking precautions

BBQs are ideal for bringing people together, yet they can pose a risk of fire if not handled with care. Although you may not directly influence how your tenants use BBQs, you can oversee certain precautions during property inspections. Should the BBQ appear to be in poor condition, it’s wise to discuss its maintenance with your tenants. A gentle reminder about the measures they can adopt to maintain their household’s safety would be beneficial:

Regular Cleaning: Ensure that BBQs are thoroughly cleaned after use. Grease and fat build-up can ignite, posing a fire risk. There’s not always efficient absorbent material in the drip tray and once the BBQ reaches a hot enough temperature, this can lead to them spontaneously igniting. Gas can be turned off, but the fire will keep going because it has more than enough fuel to keep going with the build-up of fats and oils.

Safe Placement: BBQs should be kept at a safe distance from the property. This will prevent potential fires from spreading to the structure itself.

Winter; Fireplace safety

Fireplaces add warmth and ambience but require careful handling of embers:

Use Metal Buckets: Never place fire embers in plastic containers. Always use a metal bucket to prevent unintended ignition.

Install Fire Guards: Sparks can easily escape from fireplaces. A fire guard can help contain these sparks, reducing the risk of fires.

Smoke Alarms

Smoke alarms offer a crucial defence against fires, offering early detection that can save lives and property. Ensure that:

Smoke alarms are installed throughout the property.

Batteries are checked regularly and replaced as needed.

Tenants are aware of the smoke alarm testing routine.

Final thoughts

By taking these steps, you not only minimise the risk of fire in your rental properties but also demonstrate a commitment to the well-being of your tenants. Take preventive measures, such as inspecting fireplaces and managing barbecue safety. Regular maintenance, combined with the right fire safety equipment and tenant education, can significantly prevent fires.

The New Zealand Herald has recently put the spotlight on a major issue affecting houses all over the country, P Labs. Homeowners are forking out millions of dollars to decontaminate P-riddled properties in a crisis that could rival the leaky homes disaster.

In the worst cases, contaminated houses are destroyed. An industry specialist says 40 per cent of homes he tests contain traces of methamphetamine, known as P.

Housing NZ spends about $12 million to $13 million a year on remedial work. Five of its properties were demolished in the 2015 financial year because they were damaged beyond repair. But the problem isn’t confined to poorer areas and has seeped into even the most exclusive streets. A property on the market in a high-end suburb of Auckland was contaminated during a chemical explosion from a suspected P lab in the garage in 2005.

Home Owners and Buyers Association president John Gray said he knew of six homes that cost about $250,000 to decontaminate. Invariably the clean-up ranges from $1000 to a few hundred thousand, with hefty replacement costs for furnishings, curtains and wall coverings too.

From a risk management perspective, as a landlord you should have a systematic process for performing regular checks and meth testing at your property – before, during and after a tenant vacates. The cost of a contamination event at your property could be substantial, however if effective inspections and processes are put in place then this risk can be mitigated. Swab test kits can be purchased online and they provide an indication of contamination. A full laboratory evidential test is required to confirm the exact level of contamination.

On the insurance front – not all insurance policies are equal. It is therefore critical that you check the cover you have in place, specifically relating to P Lab cover. Most insurers do not offer P Lab insurance cover as part of their offer. We are pleased to advise that over the years the Initio has successfully responded to a number of P Lab contamination claims. We are seeing an increase in incidence of these types of losses, and no two P-lab claims are the same and each claim turns on its own set of facts. When receiving a P-Lab claim we take account of the landlords approach to property inspections which at a minimum should be every 6 months (refer policy wording).

A timely reminder that regardless of who your rental property insurer is, you should make sure you have a good risk management in place.

Being a landlord comes with unique benefits and advantages. However, there are also risks with having tenants or guests stay in your property.

To best protect yourself and your property, it’s important to know where to look and who to trust. In most cases, you can learn the most from other landlords who have been in business for a long time. Specifically, you’ll want to find landlords in your area, as they are likely to have a good understanding of local laws and regulations. The New Zealand Property Investors Federation is a great place to start and connect with your local property investors association.

Generally speaking, here are some of the top tips for reducing risks:

Everything goes in writing Absolutely everything needs to be in writing. In real estate, it’s commonly said that if it’s not in writing, it doesn’t exist. While it can be tempting to rush a lease agreement to a new tenant, you want to carefully ensure everything is included. From who can live in the residence and what activities are permitted, to when rent must be deposited and how non-payments are handled, only what is written is enforceable.

Get the right insurance

If you wait until an accident happens or a loss has already occurred, it’s too late. Get the right insurance policy in place from the start to protect yourself and your assets. Having a specialist insurance policy like Initio offers means you have the cover you need to protect your property. Click here to find out more about the cover offered by Initio.

Pay attention to the property

Again, waiting until something happens means it’s already too late. Keeping your tenants safe requires you to keep up with property maintenance and ongoing issues. If something is broken or potentially hazardous, have it inspected and take care of it. This allows you to stay on top of anything that comes up before it can develop into more serious damage.

Don’t ignore tenants

No matter how frustrating a tenant might become, you must always listen to them. If they claim something is broken or dangerous, attend to it immediately and take steps to prevent future issues. By not addressing something that a tenant points out, you are exposing yourself to consequences in the future.

Screen tenants

You can avoid many unnecessary risks by screening potential tenants effectively and appropriately. Do they have a job? Can they pass a background check? Do they have any prior history of evictions? These are all important questions to ask and research. When screening tenants, require them to provide you with prior references, ideally from former landlords because they are your best tool for gathering information.

Safeguard your business

While it’s great to get everything in writing, it’s only useful if you properly store and protect that information. If your documentation is in paper form, it’s best to store a digital copy as well. For digital files, it’s best to conduct regular backups and keep all virus software up to date. From an organisational point of view, clearly label all documents and keep files easily accessible.

Handle evictions carefully

Ending a tenancy is a serious matter and should not be started without carefully completing all of the lease and legal steps required. Always consult a lawyer before evicting a tenant and ensure you have all written documentation in place before proceeding. Never threaten a tenant with eviction as a means of getting a rent payment; the regulators and Courts don’t look highly upon landlords threatening tenants.

Develop relationships with tenants

Sometimes it simply comes down to personal interaction. By developing a reputation as an approachable and honest landlord, you can build trust and prevent circumstances from becoming confrontational. When there is a relationship, tenants are less likely to file a formal complaint over a minor matter.

Andrew King, of the New Zealand Property Investors Federation, has written a common sense article on the consequences of meth in rental properties.

The consequences of Meth in rental properties has been escalating over the last few years. Fortunately it isn’t the actual health consequences of meth in rentals (except for those actually consuming the stuff) but uninformed fear of what meth residue can do and the potential for highly expensive remediation if it is discovered in your rental.

Other factors have also meant that rental property owners need to be extremely careful around the meth situation. These include decisions by the Tenancy Tribunal and actions taken by insurers.

Previously the acceptable level of meth was .5 micrograms per 100 square centimetres. If a property contained a higher level than this it was said to be “contaminated”, an emotionally charged word that most people believe means toxic. In other words if you are living in a property over this level you are likely to get sick. However this isn’t true.

To put the level into perspective, imagine a piece of meth the size of a grain of salt divided into 1,000 pieces. The previous level amounted to find one of these pieces per 100 square centimetres. It is an amount that was estimated not to cause any effect on even a susceptible human, with a safety factor of 300 applied on top. In other words it was an extremely conservative level.

Despite this, the fear of meth has led to outcomes such as tenants immediately vacating properties if any level of meth was found and Tribunal awards against landlords providing an unclean and unhealthy property even when the level of meth was less than the acceptable levels.

So it was good that the Ministry of Health (MOH) revised its recommendations and increased the acceptable unmanufactured meth level to 1.5 if there was carpet in the property and 2 if there wasn’t any carpet. They kept the level the same if it could be proven that manufacture had taken place.

The rationale was that the .5 level should remain for manufacturing in a property so that you could be sure that other nasty chemicals that might be involved in the manufacture process are not present.

Although the MOH thought that the higher levels would apply unless manufacture was proven, some local authorities (who actually set the regulations) might take the view that the .5 level would remain unless it was proven manufacture didn’t occur.

To remove any possibility of confusion, the NZ Standards Meth committee decided to include a 1.5microgram level regardless of how the meth came to be in the property.

Both the MOH and NZ Standards Meth Committee recommendations were put into the draft Standard that went out for public consultation.

The final Meth Standard is likely to be released in June and may in fact be released by the time you read this.

At the higher 1.5microgram level, it means that many properties that would have required cleaning previously will no longer need it. Testing laboratories have advised that around 80% of the samples they currently test are less than the 1.5 microgram level.

The higher level will also make it easier for meth cleaning companies to get levels at or below the 1.5 level, so there is an expectation of good improvements through the new standard.

The cost of meth claims for Insurance companies has been increasing, so hopefully this will reduce when new standards are released. Despite this, insurance companies are changing their policies with regard to meth, increasing excess levels and reducing maximum claim amounts.

They are also getting firmer on holding rental property owners responsible for checking their properties. It is advisable to check how you are covered if you are unsure. Consider looking at using Initio, the rental property insurance policy that has a relationship with the NZPIF.

Regarding checking your property, the NZ Standard draft required landlords to know what they were doing if they were conducting their own meth tests, meaning undertaking training. There will also be a list of approved self test kits so that the quality of test gear can be guaranteed.

The draft Standard also contained standard procedures to standardise sampling and cleaning companies plus laboratories. The draft Standard also contained measures to protect consumers against conflicts of interests by ensuring sampling and cleaning companies are separate.

The rental property industry is certainly looking forward to the release of the NZ Meth Standard in June. While there will be steps and procedures that we will need to undertake, it is likely that the existing problems caused by the meth issue will be greatly reduced.

For more information on the New Zealand Property Investors Federation, and how they can benefit you, check out their website www.nzpif.org.nz.

We are excited to announce that initio has been named a finalist for the Underwriting Agency of the Year at the 2018 New Zealand Insurance Industry Awards.

A huge thanks to the initio team, our customers and supporters. Also, congratulations to all the finalists. Especially our friends at Frank Risk Management, finalist for Small-Medium Broking Company of the Year, a category they won in 2016 and 2017; and Rene Swindley (founder of Frank Risk and initio) who is a finalist in the Young Insurance Professional of the Year category. Click here for a full list of the finalists.

2018 has been an exciting year for initio, with lots of new web development making it easier than ever to manage your insurance online. We are very proud of our achievements to date, and this nomination is very gratifying. Winners will be announced on Thursday 29 November 2018.

You can pay your premiums monthly using a debit or credit card. Our month-to-month insurance will automatically renew by charging your card at the renewal date of your policy each month.

If there is ever a change in your monthly premiums, we will let you know. If you need to stop your monthly payments, you can easily login to your dashboard and cancel the policy yourself.

Learn more about how monthly insurance works here.